Fintech Banking and its impacts on Financial world

Others

October 7, 2024

- How Does Product Change Is Being Seen In Digital Space And Banking?

- How Are Financial Crimes Translating In Financial Controls?

- With Respect To Technology, Are Regulators Doing Enough?

- Is There Lack Of Information Shared In Order To Evolve The Method To Fight Fincrime?

- Why Should Fintech Companies And Banks Collaborate?

- Key Takeaways

It’s fascinating and a bit concerning to see how technological advancements impact almost everything from scams to regulatory practices.

In this episode of AML Watcher’s webinar, we’ll talk about the current challenges facing financial institutions, how they’re tackling issues of compliance, and the role that new technologies play in all of this.

Here are the the key points that will be addressed below:

- How is the product change being seen in digital space and banking?

- Does Fintech banking money services have the license for making cross border transactions?

- How Are Financial Crimes Translating In Financial Controls?

- Is there a lack of information shared between the company in order to evolve the method to fight fincrime?

So, grab a cup of coffee and let’s get into exploring the complexities of this modern financial world!

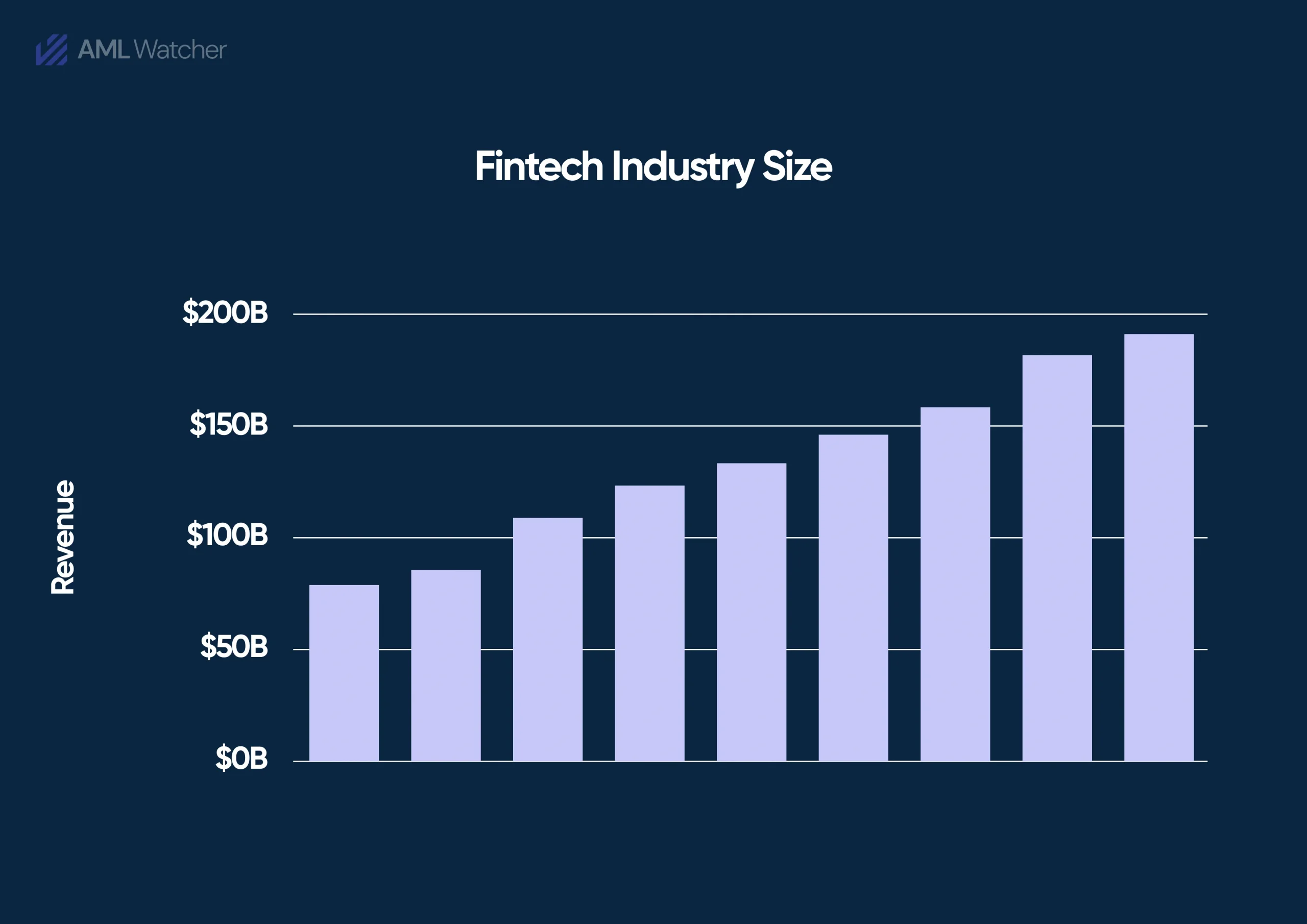

The global fintech market has witnessed significant expansion over the past decade. The market was valued at approximately $167.54 billion, with projections estimating it will reach $514.9 billion by 2028. This represents a compound annual growth rate (CAGR) of 25.18%.

How Does Product Change Is Being Seen In Digital Space And Banking?

When asked about the product change in digital space, Sarah Beth raised the concern that, ‘’As far as the growth of the product is concerned, fiat and digital currency both are changing as per the consumer need.

When it comes to AML regulations, FATF is covering the fiat and digital currency in recommendation 15 which is doing the disservice to both of them as per their nature.

So it’s a recommendation for FATF to actually make 41 recommendations for the digital asset convertible and virtual current currency. ‘’

It also came to notice that the biggest mistake we made in crypto space is to call it “crypto currency” and that has blurred all of the lines because there is a consideration of currency.

It’s high time for a distinction to be made between fiat and non fiat to make it easier. When it comes to AML and financial rules, it’s just very basic whereas compliance officers are trying to protect institutions, integrity of the financial systems and customers from financial crime.

Does Fintech Banking Money Services Have The License Of Cross Border Transactions ?

There is the entry point to the banking system through payment gateway and they are clearly not regulated and money is moving non regulated into the people’s bank accounts.

On our way to upgradation, there are things which are not protecting banks and the users as well

Sarah Beth answered that not all FinTech companies in the U.S. are considered MVTS (Money Value Transfer Services) under FATF rules.

Only those that deal with sending or transferring money, like remittance services or crypto exchanges, fit this category. Other FinTechs, offering things like loans or investments, wouldn’t be classified the same way.

The reason the USA leads in FinTech startups is that it’s often easier to launch a FinTech there with less strict AML (Anti-Money Laundering) regulations compared to other countries.

In many places outside the US, the same product would face tougher regulations and be treated like a traditional financial institution, making it harder to operate. This regulatory flexibility in the US makes it more attractive for FinTech entrepreneurs.

The majority of fintech companies that come to mind when discussing the sector in the U.S. are actually partially regulated.

When it refers to these fintechs, it’s important to note that while certain aspects of their business operations such as the P2P (peer-to-peer) side that may fall under their Money Services Business (MSB) registration, much of what they engage in does not fall under stringent regulatory oversight.

Financial crime typologies are evolving at a rate quicker than we can regulate them. Attempting to keep pace with these developments can be a mistake, as sophisticated criminals often stay two steps ahead of regulatory frameworks.

This evolution underscores the need for more adaptable and responsive regulatory mechanisms.

How Are Financial Crimes Translating In Financial Controls?

With respect to this particular concern, Sarah Beth mentioned that there should be more education for everyone about technology and its related stuff, whether it is safe and does not have the tendency to do something illegal under the carpet.

It is definitely high time for the States that they should create awareness and education for elderly and disabled people as well.

People are changing, their lifestyle is changing and so do their banking styles. It’s a very interesting fact that the central bank digital currency (CBDC) is opening a much wider range of banking systems.

But at the same time, this initiative is facing a lot of opposition in terms of increased control on the currency regulation

As it recently came into notice that the Consumer Financial Protection Bureau is mandating people to report when they get scammed in tech environment levels.

With Respect To Technology, Are Regulators Doing Enough?

According to our esteemed guest, AI and machine learning represent a significant opportunity for improving monitoring frameworks, as they can help identify complex networks of illicit activity.

For instance, HSBC has publicly shared their experience in adopting Google AI within their risk management framework.

This integration allowed them to uncover complex networks in their transactions that they were previously unaware of. However, it’s important to emphasize that AI should never replace human judgment in decision-making processes regarding alerts or potential threats.

The effectiveness of AI models is intrinsically linked to the quality of training they receive. If the individuals responsible for training these models lack experience in the AML space, there is a significant risk of producing inadequate or biased outcomes.

Get to know more about the deployment of AI in Compliance in one of our other webinars.

Is There Lack Of Information Shared In Order To Evolve The Method To Fight Fincrime?

Sarah shared her perspective that there are few observations, many fintech conferences are predominantly focused on innovation and technology while neglecting to address AML and regulatory concerns.

There are around 15 fintech conferences that took place in the U.S. this year, gathering data on attendance. Across these events, which attracted over 60,000 participants, only two panels addressed AML topics.

Both of those panels discussed how AML in FinTech is driving change, yet there was a glaring absence of discussions on AML typologies, sanctions issues, or what fintech companies should consider when seeking funding from venture capitalists.

Some unregulated platforms, such as OnlyFans, are implementing stringent controls to protect their users, even when they are not mandated to do so by law.

Thus, increased awareness and preparedness can lead to better compliance and ultimately protect the financial system from illegal activities.

Why Should Fintech Companies And Banks Collaborate?

The purpose of FinTech companies and banks collaboration is to partner and play a role to improve, compliance, and accelerate digital transformation in finance through following measures:

Cost Deduction

Banks and FinTech companies can reduce the costs associated with developing and integrating new technologies and strategic partnership.

Such kind of savings can be passed on to customers via lower fees and more competitive product offerings.

For example: If a credit bank collaborates with a FinTech which works on cloud-based banking fintech software. It eliminates the need for expensive on site infrastructure and reduces maintenance expenses.

Improved security

FinTech companies usually rank security and data protection as their priority. Banks can enhance their security measures and mitigate the risk of cyber threats by collaborating with FinTech.

Customer Centric Approach

Fintech companies have command of their innovative approach to customer experience. They are actually known for being faster, affordable, efficient, and secure than traditional banks.

FinTech’s customer-centric approach can be adopted by banks which can lead to better service for customers and increase their trust in the bank.

Level of Transparency

FinTech companies are very transparent when it comes to their commitment.

Banks can adopt more transparent practices through collaboration with FinTech which result in greater trust with the customers.

Key Takeaways

It might take long but we can definitely wrap up our heads around the key takeaways before you sign off.

- The distinction between fiat and digital currencies is crucial, and existing AML regulations (like FATF’s Recommendation 15) fail to address their unique needs. Clearer, more customized regulations are required to effectively manage both asset types.

- While technology can greatly improve daily financial operations, consistent and adaptable legislation is necessary. Including individuals with hands-on AML experience in regulatory processes can enhance the sector’s ability to fight financial crime.

- Many fintechs lack the appropriate licenses for cross-border transactions, especially in the U.S., where fintech startups often operate with minimal AML regulations compared to stricter oversight in other regions.

- AI and machine learning have significant potential to enhance financial crime detection, but their success depends on proper training and oversight by AML professionals. These technologies should complement, not replace, human judgment in risk management.

- No commitment needed

- Complete AML Database at your service

- Access our all-in-one dashboard

Tier-2 PSPs in ... must demonstrate automated monitoring, layered CDD, &...

See the Full Regulatory Expectation70–80% less manual work, 95% less fatigue, TruRisk Agent makes compliance effortless.

Experience Agentic AMLMove Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries