A Guide to Simplified AML Compliance in the United Arab Emirates

AML Compliance

December 24, 2024

- UAE Exits FATF Grey List

- From Luxury to Laundering, Dubai’s Hidden Financial Landscape

- DIFC, the Gateway to Regional and Global Markets

- AML Regulatory Bodies in the UAE

- Money Laundering Risks in High-Labor Sectors of the UAE

- AML/CFT Compliance Requirements in UAE

- UAE’s 2024-2027 National Strategy for AML

- Why AML Watcher Is Essential for the UAE?

- How Does AML Watcher Empower Financial Institutions in the UAE with Its AML Screening Solutions?

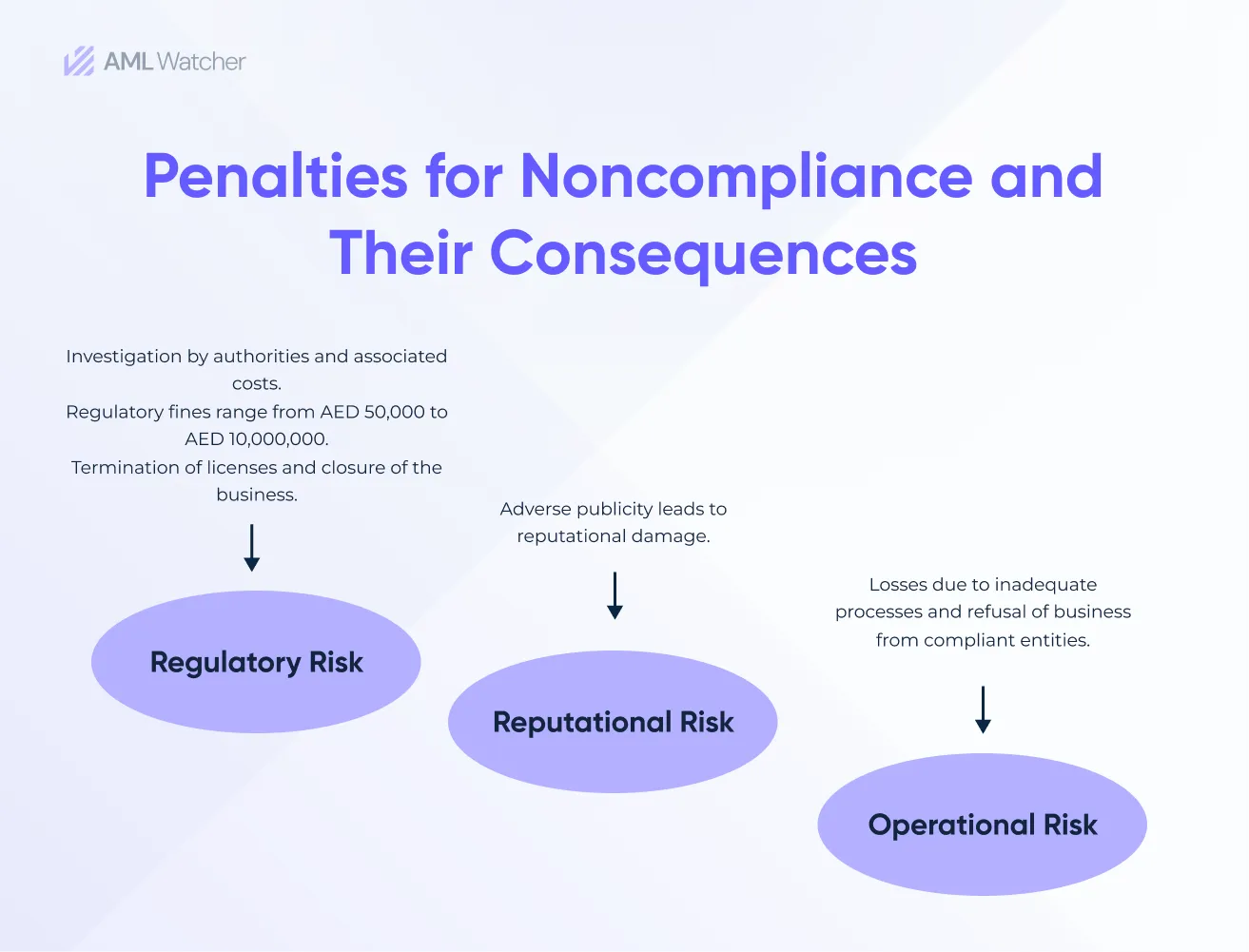

The Central Bank of the UAE (CBUAE) has imposed a financial sanction of “Dhs 5.8M” on a private bank for AML breaches. The bank had not taken proper AML measures to prevent money laundering and didn’t comply with AML laws “Federal Decree Law No. (14) of 2018 and Federal Decree Law No. (20) of 2018” in UAE.

These efforts show the UAE’s commitment to improving its financial oversight and heightened its efforts to ensure UAE AML compliance.

Read this article to get an in-depth insight into UAE AML compliance frameworks, UAE sanctions compliance, UAE FATF regulations, and the requirements of AML software UAE.

UAE Exits FATF Grey List

Adhering to AML regulations UAE shows commitment to combating financial crimes and maintaining global AML compliance standards.

UAE has improved its AML efforts by making amendments to its framework. For example, it increased investigations against financial crimes and enhanced its judicial actions in these illicit activities.

It increased collaboration with other countries. UAE Updated regulations for virtual assets such as cryptocurrencies to align with international AML standards.

These efforts were appreciated, and the UAE was removed from the FATF’s grey list, a great achievement for the country.

From Luxury to Laundering, Dubai’s Hidden Financial Landscape

Due to its exceptional strategic location, Dubai, one of the key emirates of the UAE, is considered an ideal global gateway. It acts as a bridge between Western and Eastern countries to promote trade and finance.

Dubai has developed advanced infrastructure and other trade opportunities and facilities that promote international business growth.

The emirate of Dubai has become one of the world’s important trading centers due to its established financial sector. It is focused on FinTech, robotics, and AI and has ranked in the top ten FinTech Hubs.

DIFC, the Gateway to Regional and Global Markets

The Dubai International Finance Centre (DIFC) is recognized as the leading financial hub in the MEASA region.

DIFC was founded in 2004 and covers hundreds of banks and financial institutions. Thus, Dubai is a target for financial criminals who want to invade its financial sector to promote their illicit activities.

It operates independently under its own rules and laws, and its regulatory framework is separate from regulations that apply to the rest of the UAE. It has its own financial regulatory body, the “Dubai Financial Services Authority (DFSA).”

It supervises financial crimes like money laundering (ML) and terrorist financing(TF). It evaluates the risks associated with illegal activities, understands and imposes regulations, and reports suspicious activities.

AML Regulatory Bodies in the UAE

Various regulatory bodies in the UAE oversee AML regulations. They set AML guidelines for financial institutions to follow, identify and evaluate risks, and report suspicious activities to FIU.

AML UAE strengthens measures against rising money laundering and illicit activities. They also set AML penalties to prevent AML breaches and preserve financial integrity.

Central Bank of the UAE (CBUAE)

The primary regulatory body in the UAE is the Central Bank of the UAE (CBUAE). It regulates financial institutions like banks and ensures AML/CFT compliance by implementing UAE AML laws to prevent illicit activities.

Financial Intelligence Unit (FIU)

Financial institutions and Designated Non-Financial Businesses and Professions (DNFBPs) in the UAE identify and report suspicious activities to the Financial Intelligence Unit (FIU).

It gathers information related to suspicious reports of financial crimes such as money laundering and then assesses it.

It collaborates with other entities in and outside the country to share financial intelligence globally and combat crimes effectively.

Ministry of Economy (MOE)

The Ministry of Economy supervises the “Designated Non-Financial Businesses and Professions (DNFBPs)” in the UAE to ensure AML compliance in this sector.

It implements AML screening measures such as risk assessments, identification, and reporting of suspicious entities to relative authorities to combat financial crimes.

The list of DNFBPs includes “Real Estate Agents, Dealers in Precious Metals and Precious Stones, Trust and Company Service Providers (TCSPs), Lawyers, Notaries, and Other Independent Legal Professionals, Accountants and Auditors and Casino and Gaming Establishments.”

Securities and Commodities Authority (SCA)

SCA monitors compliance with AML regulations UAE in “securities markets and commodities trading.”

It makes sure all the capital markets, investment firms, and brokerage agencies follow the same AML legislation and take measures to prevent illegal activities to promote trust worldwide.

Dubai Financial Services Authority (DFSA)

Dubai Financial Services Authority (DFSA) is an independent organization that supervises the financial services within Dubai International Financial Centre (DIFC).

DIFC ensures that all the banks, companies, and firms registered with DIFC follow the AML guidelines set by FATF.

Adhering to UAE FATF regulations is key to maintaining financial integrity and avoiding penalties for non-compliance.

It ensures compliance with international AML standards by implementing AML measures such as KYC and reporting suspicious activities in DIFC-registered companies. It encourages compliance with the AML policy UAE to build trust and combat financial crimes.

Thus, it prevents DIFC from collaborating with entities involved in illegal operations such as money laundering (ML) and terrorist financing (TF).

Financial Services Regulatory Authority (FSRA)

Financial institutions operating in the Abu Dhabi Global Market (ADGM) must be regulated, as they also play a significant role in finance. FSEA supervises these financial institutions and ensures their compliance with AML/CFT.

It offers AML guidelines to follow and monitors financial agencies associated with ADGM.

UAE complies with FATF and shows compliance with the international AML/CFT regime to prevent financial institutions from engaging in crimes and illicit activities

Executive Office for AML/CFT

It develops CFT/AML policies to ensure CFT and AML compliance across the UAE and compliance with FATF recommendations.

It coordinates with other international organizations to strengthen its AML framework. It shows compliance with the global AML/CFT regime to prevent financial institutions from engaging in financial crime risks and illicit activities.

Money Laundering Risks in High-Labor Sectors of the UAE

The Central Bank of the UAE (CBUAE) conducted a comprehensive Sectoral Risk Assessment (SRA) for all sectors with more focus on the DNFBP sector. The assessment aimed to enhance the understanding of ML/TF risks associated with various professions and businesses, including those with substantial labor components.

Under various reports the identified money laundering risk factors are;

1:Cash-Based Economies

- Construction, logistics, and manufacturing in the UAE heavily rely on cash payments for wages and operational transactions.

- The use of cash increases anonymity, making it easier to inject illicit funds into legitimate financial systems.

2: High Volume of Foreign Workers

The UAE has a large expatriate population and can be exploited for money laundering activities, as many workers may lack awareness of local laws and regulations, making them vulnerable to being used as conduits for illicit financial flows.

3: Worker Recruitment Agencies

- Recruitment agencies for low-skilled labor are often unregulated, creating opportunities for money laundering under the guise of fees or labor agreements.

- Payments routed through offshore accounts or shell companies add complexity to tracing funds.

4: Cross-Border Financial Flows

Foreign workers often send remittances back to their home countries. These cross-border financial flows can be misused for money laundering if not properly monitored, especially if they involve high-risk jurisdictions known for lax AML controls.

5: Name Variation Risks

The UAE’s diverse population and complex naming conventions present unique challenges in UAE AML compliance. Variations in spelling, transliterations, cultural naming norms, and common names like “Mohammed” or “Ahmed” can lead to operational inefficiencies and risks in money laundering detection.

6: Complex Supply Chains

- High-labor industries involve multiple layers of subcontractors, intermediaries, and vendors.

- These complexities can be exploited to launder funds, particularly when documentation is falsified or payments are disguised as operational costs.

7: Trade-Based Money Laundering (TBML)

- Labor-heavy industries, such as construction and manufacturing, often involve international trade.

- TBML risks include over/under-invoicing, misdeclaration of goods, and falsification of shipping documents.

8: Integration Through Real Estate

- High-labor construction firms are closely tied to the real estate sector, a known avenue for integrating illicit funds.

- Criminals may purchase properties outright or layer funds through subcontracted labor payments.

9: Shell Companies and Front Businesses

- Labor supply businesses are often used as fronts to layer illicit funds through inflated wage bills or non-existent workers (“ghost employees”).

AML/CFT Compliance Requirements in UAE

To combat Money laundering and Terrorist Financing, organizations operating in the UAE must comply with AML/CFT regulations that coordinate with Domestic and international AML/CFT standards.

goAML Registration

goAML is a platform for reporting suspicious transactions to the FIU. Entities are required to register with it.

Appointment of AML Compliance Officer

A well-qualified AML Compliance Officer who knows how to comply with legal obligations and implement internal AML policies and controls within the institution is needed.

AML Business Risk Assessment

Follow a risk-based approach to identify, evaluate, and mitigate the risks associated with financial crimes. Update them regularly to account for changing risks.

Regularly Update Internal Policies and Controls

Define internal UAE AML policies, controls, and procedures by considering AML/CFT laws and AML regulations. Review and update them to align with recent AML/CFT standards.

KYC (Know Your Customer)

Conduct KYC (Know Your Customer) measures on your customers by verifying their identity and assessing the risks associated with them to prevent illicit activities.

Companies must conduct enhanced due diligence (EDD) to identify and verify beneficial ownership and associated risks.

AML Screening

Screen the client name against the UNSC Consolidated List and UAE local lists. Choosing the right AML software UAE can help businesses ensure compliance with local and international AML regulations effectively.

Effective AML monitoring UAE practices is important for detecting and preventing suspicious activities.

After the screening, there will be three possibilities: the results will show a Full match, a partial match, or no match.

Full Match

If an existing client shows a full match:

- Its funds will be frozen.

- Its transactions will be blocked.

- It will be considered a “high risk.”

If the potential customer shows a full match:

- Refuse to make any transactions with him.

- Classify it as high-risk.

- Submit a “Freezing Funds Report” against it.

Partial Match

- Mark this customer as “high risk.”

- Suspend all transactions with him.

- Submit a report called “PNMR (Partial Name Match Report).”

No Match

- There will be no action against it

- Customers will be monitored to assess future risks.

Risk Profiling

If there is no match after screening against worldwide sanction lists and local UAE lists, then asses their risks on various factors such as checking customers’ behavior.

What kind of product/service/transaction types do they use, and how do they interact with business?

Continuously assessing UAE criminal risk allows businesses to identify vulnerabilities and strengthen compliance frameworks.

Enhanced Due Diligence (EDD)

Verify the source of funds (SOF) and source of wealth (SOW) for high-risk clients. Before starting any transactions, get approval from management.

Financial institutions that are conducted using a bank account officially registered with the customer’s name.

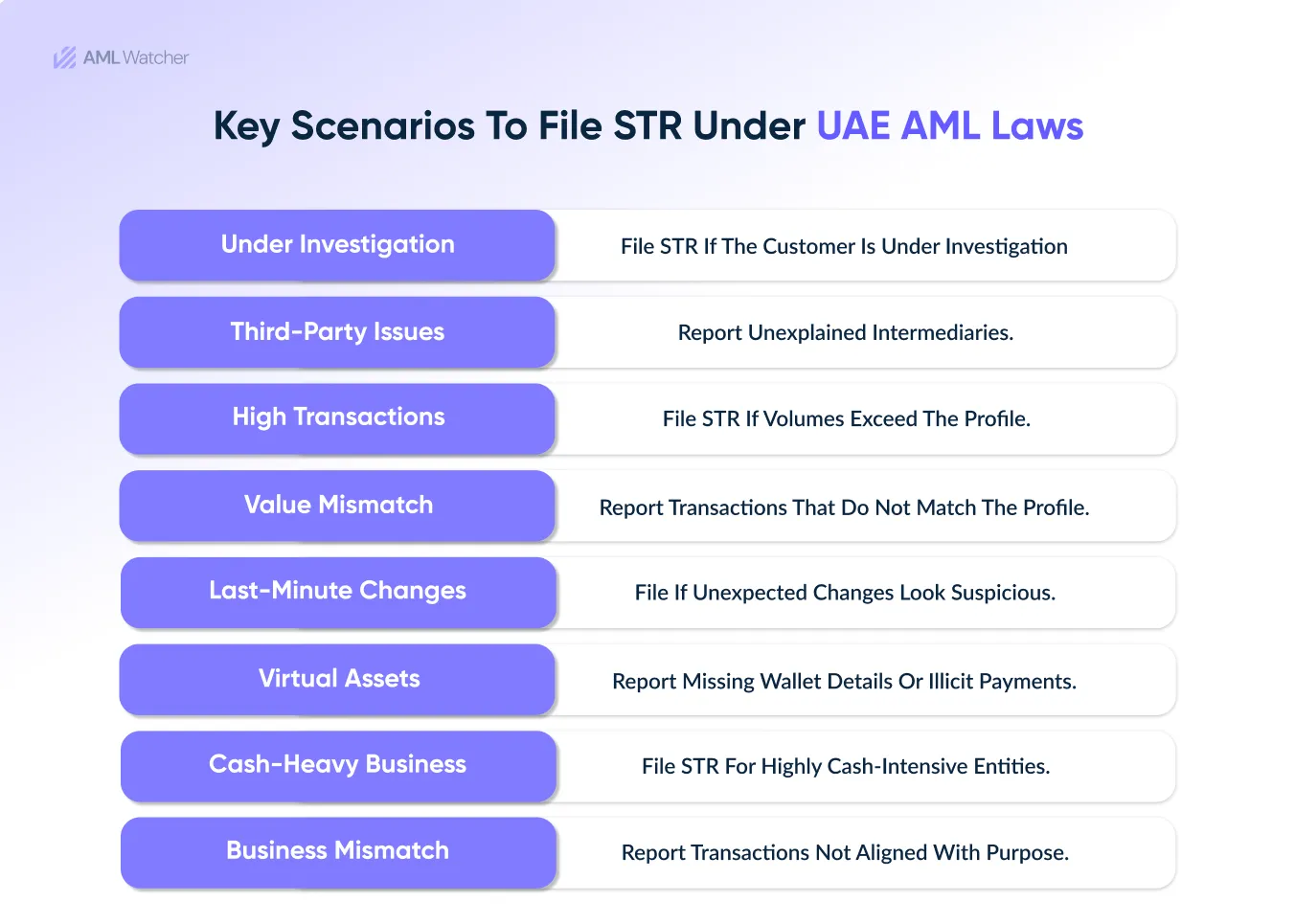

Submit STR/SAR

If Suspicious Transactions or Activities are identified, submit an STR (Suspicious Transaction Report) or SAR (Suspicious Activity Report) to the FIU.

If there are no suspicious activities in evaluation, continue regular operations, monitor client information, and update it.

Record Keeping

Maintain transaction records and all client information for at least five years. It will provide data for audit and ensure compliance.

Repeat Process

Repeat the process periodically to asses the changes and risks in the profile.

Other Requirements

- Appoint an independent auditor for AML/CFT reviews.

- Submit regular risk assessment reports for DNFBPs.

- Provide EDD reports for real estate and law firms.

- Share risk updates with senior management.

- Conduct AML/CFT training for staff.

- Submit annual risk assessment reports.

- Record high-risk accounts and transactions.

UAE’s 2024-2027 National Strategy for AML

The UAE’s 2024-2027 National Strategy for Anti-Money Laundering (AML), Countering the Financing of Terrorism (CFT), and Proliferation Financing (CPF) is a comprehensive framework aimed at strengthening the country’s financial integrity, reducing vulnerabilities to financial crimes, and aligning with international best practices. It includes:

Key Objectives of the Strategy

1: Strengthening Regulatory Frameworks

- Enhance legal, regulatory, and operational mechanisms to combat money laundering, terrorism financing, and proliferation financing effectively.

- Align UAE laws with international standards, including FATF (Financial Action Task Force) recommendations.

2: Improving Risk-Based Supervision

- Implement a risk-based approach to monitor high-risk sectors like real estate, gold and diamond trading, financial services, and DNFBPs (Designated Non-Financial Businesses and Professions).

3: Boosting Investigative and Prosecution Capabilities

- Increase the capacity of UAE AML law enforcement agencies and financial intelligence units to detect, investigate, and prosecute financial crimes.

- Leverage advanced technologies, data-driven screening solutions, and AML software UAE to analyze suspicious activities and uncover complex financial crime networks.

4: Enhancing International Cooperation

- Strengthen partnerships with global financial institutions, regulators, and international organizations to share intelligence and tackle cross-border financial crime.

5: Raising Awareness and Building Capacity

- Regularly conduct training for public and private sector stakeholders to improve their understanding of AML/CFT/CPF regulations.

- Promote awareness campaigns targeting industries vulnerable to financial crime.

Why AML Watcher Is Essential for the UAE?

As the AML laws in UAE strengthen its regulatory framework under the 2024-2027 National Strategy for AML/CFT/CPF, institutions need precise and efficient tools to tackle money laundering risks. AML Watcher, a specialized AML screening solution, empowers UAE institutions by streamlining compliance processes and enhancing risk detection.

How Does AML Watcher Empower Financial Institutions in the UAE with Its AML Screening Solutions?

In the UAE’s changing financial scenario, where regulatory compliance is paramount, AML Watcher shines as a powerful ally for financial institutions.

Its innovative screening solutions are particularly designed to navigate the complexity of Anti-Money Laundering (AML) requirements, assuring accuracy, efficiency, and peace of mind.

It offers:

Real-Time Screening for Unmatched Precision

AML Watcher’s proprietary screening databases provide real-time access to global and regional watchlist, sanction lists, and PEP screening ensuring institutions stay ahead of evolving risks:

- Sanctions and Watchlist Monitoring: Screens against 1,300+ global watchlists, and 200+ sanctions lists including UAE sanctions lists, UN sanction lists, and enforcement databases.

- UAE-Specific Data Coverage: Incorporates regional watchlists and UAE FATF regulations critical for compliance in a high-stakes financial hub.

- Global PEP Screening: Detects and highlights high-risk domestic to foreign politically exposed persons in UAE and their networks, a key requirement in the UAE’s PEP compliance framework.

Impact:: This ensures that institutions in the UAE meet local and international compliance standards effortlessly.

Tailored Solutions for the UAE’s Unique Compliance Landscape

The UAE’s role as a global financial hub attracts high-value transactions—and heightened scrutiny. AML Watcher provides tools to address these unique challenges:

- Localized Risk Assessment: Tailored to UAE AML policies and regulatory frameworks, such as Central Bank requirements and FATF guidelines.

- Customized Transaction Monitoring: Set tailored amount criteria that flag suspicious activities, such as large cash deposits, unusual transfers, or irregular transaction patterns, in real-time.

- Industry-Specific Focus: Supports sectors like real estate, fintech, and precious metals, which are often targeted for money laundering and terrorism financing.

Intelligent Name-Matching Algorithms

AML Watcher leverages advanced technology to account for variations in cultural names for anti money laundering UAE:

- Phonetic Matching: Identifies names with similar sounds but different spellings, such as “Mohammed,” “Muhammad,” or “Mohamad.”

- Fuzzy Matching: Detects partial matches, mitigating risks from misspellings or incomplete names.

- Transliteration Flexibility: Handles multiple transliterations of Arabic or non-Latin names, ensuring comprehensive coverage in screenings.

Benefit: Minimizes false positives or irrelevant alerts, enabling compliance teams to focus on genuine risks and improve operational efficiency.

Continuous Monitoring for Evolving Risks

Compliance doesn’t stop at onboarding. AML compliance officers need AML Watcher’s AML screening solution that offers continuous monitoring to detect risks as they emerge:

- Real-Time Alerts: Instantly flags changes in customer risk profiles, such as new UAE sanctions compliance or adverse media mentions. It efficiently manages a vast portfolio of risk profiles across medium, low, and high-risk thresholds in a custom risk-scoring feature.

- Proactive Risk Management: Empower institutions to act swiftly on emerging threats, safeguarding operations and reputation.

Advanced Risk-Based Screening

AML Watcher’s risk-based approach aligns with UAE’s emphasis on detecting high-risk sectors like real estate, trade, and gold.

- Enhanced Due Diligence (EDD): Deep screening for entities and individuals in high-risk sectors or jurisdictions.

- Dynamic Risk Scoring: Monitors customer profiles, transactions, and geographies to provide a comprehensive risk assessment.

- Industry-Specific Customization: Adjusts parameters for high-risk industries like real estate, fintech, and precious metals.

Impact: Focuses compliance efforts on the most critical risks, minimizing time spent on low-risk matches.

International Leaks Data Screening

AML Watcher provides access to international leaks data, such as the Panama Papers, Dubai Leaks, or Pandora Papers to help UAE institutions mitigate financial risks tied to high-risk individuals, politically exposed persons (PEPs), and their relatives (RCAs).

- Hidden Connections: Know undeclared assets and links to high-risk jurisdictions or shell companies.

- Enhanced Risk Profiling: Delivers insights into the financial activities of PEPs and RCAs to strengthen due diligence.

- Real-Time Alerts: Notifies teams of emerging risks and newly exposed data in real-time.

Impact: Strengthens compliance with AML regulations UAE, reduces reputational threats, and ensures a proactive approach to risk management.

Adverse Media Monitoring

With the UAE’s focus on strengthening investigations, AML Watcher’s data-driven adverse media screening uncovers hidden risks by analyzing global and regional news sources.

- Sentiment Analysis: Flags potential reputational risks tied to financial crimes.

- Historical Data Access: Screens up to 10 years of historical data to identify patterns of fraudulent behavior.

Impact: Eliminates irrelevant or outdated media matches, allowing teams to act on meaningful insights.

Keyword Refinement Tools

AML Watcher’s keyword refinement features let compliance teams focus on high-priority risks:

- Inclusion/Exclusion Filters: Allows institutions to include or exclude specific keywords or phrases that may cause irrelevant matches.

- Industry-Specific Filtering: Customizes keyword searches to focus on risks relevant to the UAE’s high-risk sectors, such as real estate and trade finance.

Impact: Ensures screening results are relevant to specific business needs, reducing irrelevant alerts.

Frequently Asked Questions

The first line of defence (1LoD) should continuously or at least daily monitor the customer transactions at the branch level. The frequency of monitoring depends on different factors, such as trigger events (structuring, regulatory thresholds, etc.) or the risk level of a customer (high-risk demand requires more frequent monitoring).

- No commitment needed

- Complete AML Database at your service

- Access our all-in-one dashboard

Tier-2 PSPs in ... must demonstrate automated monitoring, layered CDD, &...

See the Full Regulatory Expectation70–80% less manual work, 95% less fatigue, TruRisk Agent makes compliance effortless.

Experience Agentic AMLMove Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries