The New AMLD7: Revolutionizing Compliance or Overburdening Businesses?

AML Compliance

May 5, 2025

- The Compliance Burden: Why was this a Necessary Step?

- History Behind Anti-Money Laundering Directives

- The New AML Regulation- But Why?

- What Changes with the new Anti-Money Laundering Directive?

- AMLD7/AMLR: Which Sectors are being Affected the Most?

- Impact on Businesses? A Difficult Trade-off or an Opportunity for Growth

- Turn compliance into your Strategic Edge

- Will there be an Official AMLD7?

- Striking the Balance between Compliance and Innovation

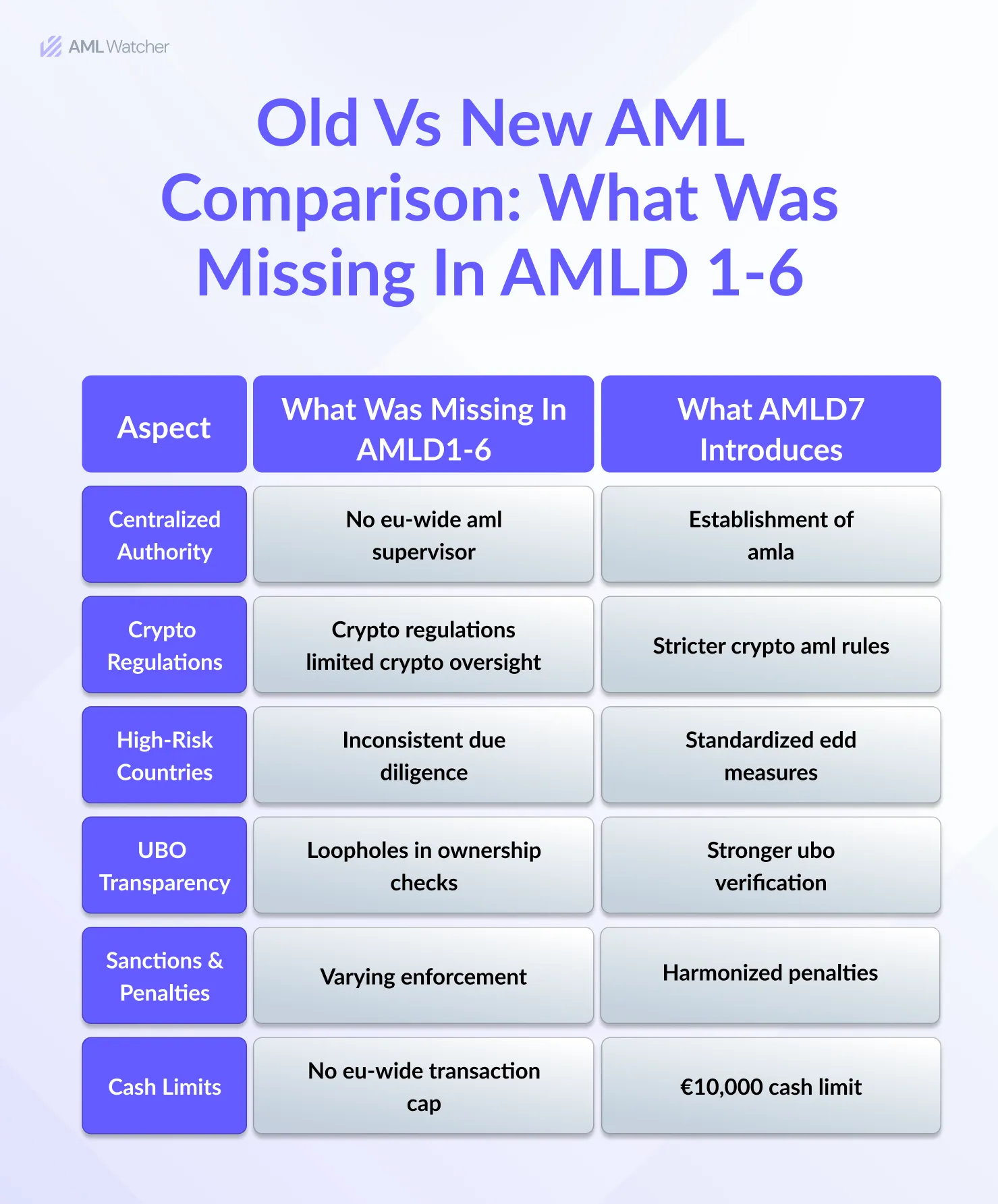

For years and years, the European Union introduced Anti-money laundering directives (AMLDs) that required individual member states to transpose and adapt them into their national laws.

This approach, however, led to inconsistencies in enforcement, as some countries implemented stricter measures while others lagged behind.

Initially, the EU planned to introduce the Anti-money laundering directive AMLD7 to enhance financial crime prevention. However, the idea of another directive or a regulation with the suffix directive attached to it has not come to fruition yet.

Instead,

The EU introduced the Anti-Money Laundering Regulation AMLR- a directly applicable law that does not require national transposition.

This move effectively consolidates AML rules across all member states and fully adopts the provisions of AMLD6, thus ensuring uniform enforcement across the EU.

Experts are referring to this package adopted on May 30, 2024, as the 7th Anti-Money Laundering (AML) Directive. However, the EU Council has not officially used this term in its communications.

With the new AMLR, businesses will have to comply with even more regulations. Let’s analyze it in detail.

The Compliance Burden: Why was this a Necessary Step?

The AMLD7 aims to fill the regulatory gaps and ensure that European Union States comply with the toughest practices. Why was this necessary? You might wonder.

In recent years, Europol and Eurojust have dismantled several major organized crime groups, highlighting how money laundering remains a serious issue across the European Union.

A key reason behind this is the lack of a harmonized approach to AML enforcement across member states.

Organized crime often spans across borders, creating complex challenges for law enforcement agencies, as highlighted in an EPP paper on how to combat organized crime in EU countries.

These criminal networks operate in multiple countries, using sophisticated methods to avoid detection and prosecution.

A prime example is related to the EU’s regulatory authorities’ recent crackdown on a group of suspects who primarily operated in Spain and utilized the Hawala system, a traditional, informal method of transferring money, to move large sums of cash.

The funds, mainly generated from drug trafficking, were then laundered through a network of companies owned or controlled by the suspects.

Investigators believe the gang was conducting daily cash transactions, with some days seeing amounts as high as EUR 300,000. This is just one of the many gangs and operations that operate within the EU.

History Behind Anti-Money Laundering Directives

The EU’s anti-money laundering directives, first introduced in 1991, are issued by the European Parliament and incorporated into member states’ laws. Over the years, they’ve been updated to enhance efforts against money laundering and terrorist financing.

Before we assess the new regulation, let’s look at the history of AMLDs in the EU.

1. AMLD1 (1991)

The first directive targeted money laundering from drug trafficking. It applied mainly to the financial sector and introduced basic due diligence and record-keeping requirements.

2. AMLD2 (2001)

Expanded the scope to cover all serious crimes, not just drug-related offenses. Moreover, it introduced scrutiny for politically exposed persons (PEPs).

3. AMLD3 (2005)

AMLD3 aligned EU rules with FATF recommendations and promoted a risk-based approach. Additionally, it extended obligations to legal professionals, accountants, and real estate agents.

4. AMLD4 (2015)

The next step was to strengthen AMLD risk assessments and introduce central registers of beneficial ownership. AMLD4 also required enhanced due diligence for high-risk third countries.

5. AMLD5 (2018)

AMLD5 responded to global scandals by increasing transparency in virtual currencies and company ownership. Additionally, it brought in new rules for prepaid cards, art dealers, and crypto service providers.

6. AMLD6 (2021)

AMLD6 aimed to harmonize definitions of money laundering and expand the list of predicate offenses. Moreover, it made aiding and abetting money laundering a punishable crime across the EU. The new AMLR was proposed on 20th July 2021 as part of its broader AML/CFT reform package.

The New AML Regulation- But Why?

The AMLR is Europe’s boldest attempt to close some loopholes. It aims to ensure regulatory compliance by ensuring

- stricter oversight

- harmonized rules

- creation of a central authority

However, this poses an important question: Are these changes enough? Will the AMLR (also known as the seventh AMLD) protect the system or bury businesses under its weight? Let’s find out in this blog.

What Changes with the new Anti-Money Laundering Directive?

On one side, we have the AMLDs and AMLR, which are designed to strengthen financial systems, unify regulations, and clamp down on money laundering.

On the other side, businesses face the challenge of navigating:

- Stricter compliance rules, such as dealing with a transaction limit

- Increased costs of conducting enhanced due diligence

- Complex reporting obligations requiring multiple officers

For SMEs and fintech startups, the question looms large: How do they meet these demands without stifling their growth or innovation? Although AMLD7 promises a modernized compliance framework, its ambitious scope may overwhelm smaller businesses.

Striking a balance becomes critical, and businesses need to adapt to ensure that compliance with AML regulations does not become an insurmountable hurdle.

AMLD7/AMLR: Which Sectors are being Affected the Most?

AMLD will target many previously-ignored sectors, such as crypto, in its mix. Moreover, it aims to harmonize rules and regulations across the EU. Let’s discuss each of these changes in detail.

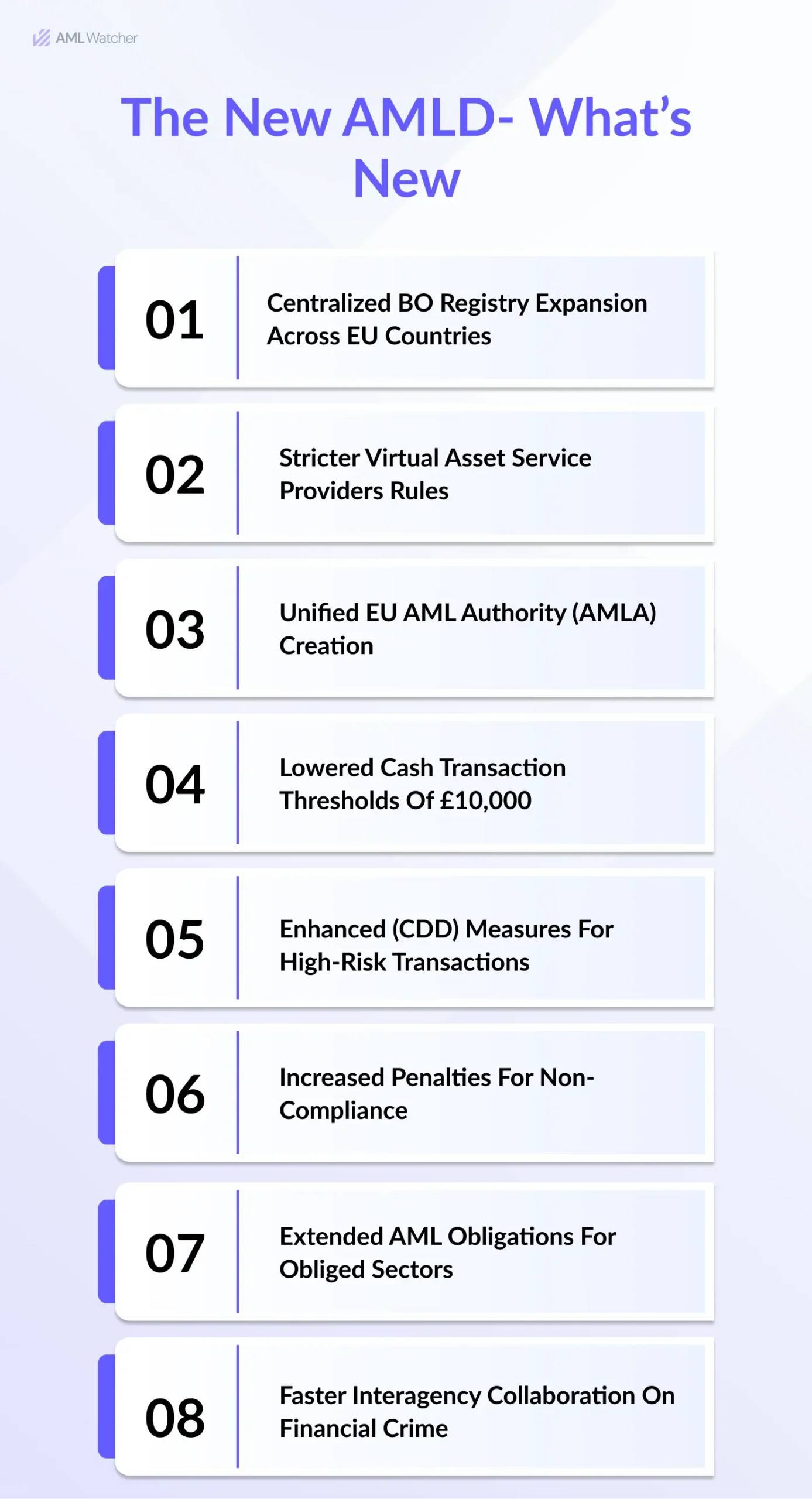

1. Obliged Entities are Expanded

For starters, the new AMLR increases the list of obliged entities to incorporate sectors like football clubs, crypto, and luxury goods.

2. Establishment of a Centralized Authority

The previous directives left supervision to national authorities. With the AMLR, the Anti-money laundering authority will have direct oversight of high-risk financial institutions and coordinate with national regulators to ensure uniform compliance. The authority aims to close regulatory gaps, enhance cross-border cooperation, and impose stricter AML penalties for non-compliance.

3. Stricter Assessment of High-Risk Third Countries

The new AMLD7 will also ensure that high-risk countries identified by the FATF will be thoroughly assessed by the AML supervisors. The directive requires these institutions to apply extensive due diligence measures when they are dealing with customers or transactions from high-risk countries.

4. Cash Payment Limits

The AMLD7 also places a limit on any transactions above the threshold of €10,000. If any transaction exceeds this threshold, the individual will have to justify the source of the funds; otherwise, they will be subjected to criminal liability. All this ensures that large cash movements are flagged and scrutinized pre-emptively.

5. Central Records of UBOs7

One of the most important aspects of the AMLD7 is to create a central record of all the UBOs. The Ultimate beneficial ownership data needs to be accessible to the public in order to ensure transparency.

Impact on Businesses? A Difficult Trade-off or an Opportunity for Growth

Whenever a new regulation is introduced, businesses often panic, thinking they’ll need to pour more money and resources into AML compliance.

However, compliance with these new regulations becomes a real issue only when the compliance tool they use generates a high number of false positives, leading to increased manual review costs.

AML Watcher’s risk screening solution is based on the core foundation of accurate AML data in line with global and jurisdiction-specific AML compliance regulations. This comprehensive approach leads to a reduction in false positives up to 44%, dropping AML compliance costs by 50%.

Turn compliance into your Strategic Edge

Within Europe, many startups dealing with legacy compliance systems may have been taken aback by the emergence of AMLD7. Here’s what they can do to lessen the panic around the new regulation.

- Use an AML Screening solution based on comprehensive and accurate data, which assists in customer risk screening according to the requirements of the regulation.

- Use of AI-based transaction monitoring systems that could easily consider the transaction limit and filter out cases for compliance officers.

- Building strong in-house teams that could follow a consistent and thorough due diligence pattern, or finding good AML consulting services to outsource to.

- Adopt a phased implementation to limit the drainage of resources and ensure the in-house teams are able to adapt to the systems better.

Will there be an Official AMLD7?

The Anti-Money Laundering Regulation (AMLR) is often informally referred to as AMLD7, though the European Union has not officially designated it with this title.

This has led to some confusion, as the EU traditionally follows a Risk-based approach, such as with the previous Anti-Money Laundering Directives (AMLDs).

Looking ahead, there is uncertainty about whether the EU will continue this pattern by introducing an official AMLD7 or shift toward a new regulatory framework entirely.

Striking the Balance between Compliance and Innovation

For SMEs and even for large-scale financial institutions, early adaptability is the best solution. AML Watcher provides powerful anti-money laundering solutions to help your company maintain full KYC compliance. Partner with AML Watcher and benefit from:

- Access to 3,500+ global watchlists for thorough sanctions screening

- Coverage of 415+ risk categories for detailed adverse media checks

- Multi-level PEP screening tailored to local legal requirements

- Screening against Crypto addresses

- Real-time database updates every 15 minutes to proactively manage regulatory risks

Moreover, AML Watchers empowers businesses to do enhanced due diligence for risk assessment and ongoing transaction monitoring to detect and get real-time insights into the evolving risk status of their customers.

It’s crucial in high-risk scenarios to ensure institutions fully understand their clients and activities.

Get in touch with us to enjoy software that offers multilingual capabilities, real-time screening, advanced name matching, and the ability to detect nuanced risks through adverse media screening.

- No commitment needed

- Complete AML Database at your service

- Access our all-in-one dashboard

Tier-2 PSPs in ... must demonstrate automated monitoring, layered CDD, &...

See the Full Regulatory Expectation70–80% less manual work, 95% less fatigue, TruRisk Agent makes compliance effortless.

Experience Agentic AMLMove Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries