AML Regulations in the UK: A Comprehensive Guide

AML Regulations

May 10, 2024

Being a prominent Financial Action Task Force (FATF), a global transnational AML watchdog, the UK government has been coming up with policies and regulation since 1990 in line with the recommendations by the FATF and global compliance standards set by the European Union Directive on anti money laundering measures.

Countries are required to take stringent measures against money laundering to maintain their FATF membership. The UK government has been implementing anti-money laundering AML and counter terrorism financing CTF framework inspired by the international regulatory bodies.

As FATF members, the UK commits to developing and strengthening its AML and CTF framework in order to maintain membership; this is achieved through regulations that outlaw money laundering as well as other forms of corruption, and also require financial institutions to take action to combat these crimes.

UK’s principal regulation regarding the anti money laundering is mentioned in the Proceeds of Crime Act 2002, which are basically devised for banking, money transmission, and investment sector as well as certain other professions that are included in the regulated sector. Any money laundering related suspicions are reported to the UK regulatory authorities.

The UK financial system is safeguarded by the Money Laundering laws, which also aim to detect and prevent criminality. Controls are implemented to stop a business covered by these standards from being utilized for money laundering.

In the UK, money laundering is widely defined. In essence, handling or being involved with any money obtained by crime (or with funds or assets that stand in for money obtained through crime) may constitute a money laundering offense.

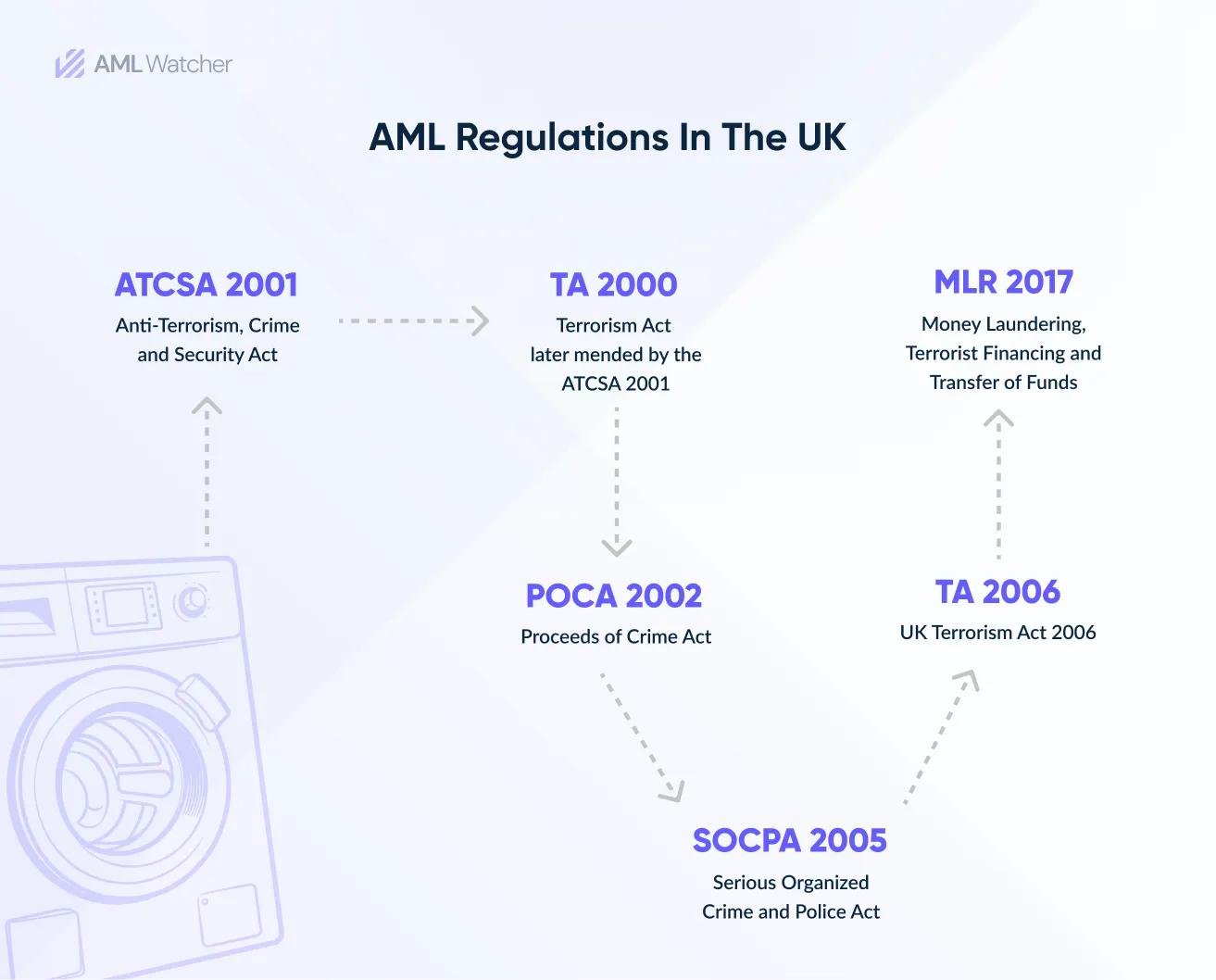

In the past two decades, UK Anti-money Laundering (AML) regulations laid out in the following regulatory guidelines and legislations passed by the British legislators and regulatory bodies.

- Proceeds of Crime Act (POCA) passed in 2002 which was later modified in 2005 by the

Serious Organised Crime and Police Act 2005 (SOCPA)

- Money Laundering, Terrorist Financing and Transfer of Funds (Information on the Payer) Regulations 2017 (MLR 2017)

- Terrorism Act (TA 2000). Later mended by the (ATCSA 2001)

- Anti-Terrorism, Crime and Security Act 2001 (ATCSA 2001)

- UK Terrorism Act 2006 (TA 2006)

Money laundering offenses in the UK are not restricted to the profits of major crimes or monetary thresholds, in contrast to several other countries (most notably the US and most of Europe). Financial transactions are considered money laundering offenses under UK law even if they have no intention or design to wash money. Since assets of any kind are covered by the money laundering Act in the UK, a money laundering violation does not even need to involve money. Therefore, under UK law, anyone who commits an impulsive crime in the country (i.e., one that results in a benefit in cash or any other kind of asset) also unavoidably conducts an illicit money laundering offense.

UK’s Money Laundering Regulations 2017

The primary objective of the recent money laundering regulation passed by the UK regulatory institution which came into effect in June 2017, was to make sure that anti-money laundering checks in the UK meet the recommendations and international standards set by the global AML watchdog known as Financial Action Task Force (FATF). It is designed in line with the European Union’s Fourth Money Laundering Directive. These regulations instituted massive changes in the UK’s AML framework now being widely known as the Money Laundering, Terrorist Financing and Transfer of Funds (Information on the Payer) Regulations 2017 (MLR 2017).

The Money Laundering Regulations 2003, which were superseded by the Money Laundering Regulations 2007, provide secondary regulation. The EU Directives 91/308/EEC, 2001/97/EC, and (via the 2007 regulations) 2005/60/EC serve as their direct sources of inspiration. The regulations enumerate several supervisory authorities whose responsibility it is to monitor the financial operations of their members.

UK’s Money Laundering Regulations 2019

The UK’s regulation regarding money laundering and terrorist financing which was designed in line with the EU Fifth Money Laundering Directive came into action on January 10th, 2020. These regulations make some limited but important amendments to the existing Money Laundering, Terrorist Financing and Transfer of funds (Information on the Payer)

This also applies to someone who, by illegal activity, avoids an obligation (like a tax liability)—a practice known by attorneys as “obtaining a pecuniary advantage”—since he is believed to have gained an amount of money equivalent to the liability avoided.

The maximum sentence for the main money laundering offenses is 14 years in jail.

As shown by the accountant’s professionally qualified position, the national risk assessment of money laundering and terrorist financing 2020 (NRA) claims that the capacity to employ accounting services to help criminals’ finances achieve legitimacy and respectability is what keeps them appealing to criminals.

UK National Risk Assessment

As shown by the accountant’s professionally qualified position, the national risk assessment of money laundering and terrorist financing 2020 (NRA) claims that the capacity to employ accounting services to help criminals’ finances achieve legitimacy and respectability is what keeps them appealing to criminals.

The accounting services that are thought to be most vulnerable to abuse are still: payroll, general bookkeeping, and company creation and termination. Other risk areas are also highlighted by the NRA, and these have been included in the risk sections below.

According to the NRA, when an accountant fails to put appropriate risk-based controls in place and fails to fully understand the risks associated with money laundering, they put themselves at the highest risk of being used or abused by criminals.

High Risk ML/TF Circumstances

The Accountancy AML Supervisors’ Group has issued recommendations outlining the principal risks and red flag signs that the AASG believes are relevant to the accounting sector. The AASG will update it on a regular basis to reflect the UK’s National Risk Assessment and other new threats and trends.

Firms should check their risk perspective on a frequent basis to ensure that they have recognized all areas relevant to their own business, especially as the risk may evolve as a result of changes in the firm’s client base, region, and services provided.

The Accountancy AML Supervisors’ Group has issued recommendations outlining the principal risks and red flag signs that the AASG believes are relevant to the accounting sector. The AASG will update it on a regular basis to reflect the UK’s National Risk Assessment and other new threats and trends.

Firms should check their risk perspective on a frequent basis to ensure that they have recognized all areas relevant to their own business, especially as the risk may evolve as a result of changes in the firm’s client base, region, and services provided.

Suspicious Activity Reporting (SAR) Regulation in UK

Individuals working within regulated organizations are required by Part 7 of the Proceeds of Crime Act to provide a Suspicious Activity Report (SAR) to the National Crime Agency if they are aware, suspect, or have reasonable grounds to believe that a person is engaging in, or attempting to engage in, money laundering or terrorist financing.

The National Crime Agency’s Financial Intelligence Unit receives about 460,000 SARs annually, with each report being analyzed for strategic and tactical intelligence before the most sensitive are picked and submitted to law enforcement or other organizations for inquiry.

SARs are frequently utilized for several objectives by various organizations. A SAR’s information may supply HM Revenue & Customs with tax information, local police with information about fraud and theft, and a government department with information on a financial product problem or issue. Reports can be submitted either electronically via the SAR online system or manually utilizing forms.

Financial organizations and other qualified individuals, such as solicitors, accountants, and estate agents, file Suspicious conduct Reports (SARs), which are an important source of intelligence on not only economic crime but also other types of criminal conduct. They give private sector information and intelligence that law enforcement would not otherwise have access to – The National Crime Agency

Noncompliance with AML requirements in UK

Failure to follow AML regulations and legislation can have substantial implications, criminal as well as civil. These punishments might range from infinite fines and brand damage to sanctions, license revocation, and even jail time.

Furthermore, HMRC is required to publicly disclose the information of any entity that has failed to comply with MLR 2017. This list is published in the public domain and includes a company’s name and address, the laws that were violated, the amount paid, and whether the company is appealing the penalty.

The number of instances of firms failing to follow anti-money laundering legislation is high. Nearly a million (901,255) SARs were filed with the NCA between April 2021 and April 2022, according to its annual report, representing a 21% rise over the same period the previous year.

And this only includes cases that have been registered! It is difficult to determine how many cases of money laundering go unnoticed and unpunished.

With the number of money laundering cases skyrocketing, we look at some of the most major instances from recent years, as well as some record-breaking penalties for AML and CTF violation

- No commitment needed

- Complete AML Database at your service

- Access our all-in-one dashboard

Tier-2 PSPs in ... must demonstrate automated monitoring, layered CDD, &...

See the Full Regulatory Expectation70–80% less manual work, 95% less fatigue, TruRisk Agent makes compliance effortless.

Experience Agentic AMLMove Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries