5 Major AML Laws In The US That Shape Your Compliance Program

AML Regulations

April 4, 2024

Crimes generate tons of black money that must be made clean through laundering. I have not come across a better way to explain how money laundering works than the way Saul Goodman exfoliated the layers in Breaking Bad. You can binge-watch it later as we are going to dig deeper into laws that stem money laundering, known as AML rules in the US.

These AML laws and regulations established to promote anti-money laundering (AML) measures are not as forgiving as Skyler White, beloved wife of Walter White who could escape law enforcement for a long time.

Before I lose your attention to a fictional series, let me pin down the fact that violations of global AML laws and inefficiency in employing robust compliance measures have cost businesses billions of dollars. Since 2000, financial institutions (FIs) have been penalized for non-compliance with AML rules, totaling $387.559 billion in fines.

Adherence to these regulatory requirements demands a clear understanding of their application, limitations, and expectations, which we will discuss in this blog. Before outlining the details of major AML laws in the US, let’s explore the regulatory bodies, and their requirements for AML controls to be implemented in designated businesses.

Which Financial Sectors Are Subjected To AML Laws?

More than 50 years of regulatory precedent gave birth to AML laws which cover several financial institutions and expect organizations to detect and prevent money laundering and associated predicate crimes through in-house controls.

- Financial institutions such as insurance firms, banks that are FDIC-insured, credit card companies, credit unions, and casinos. Cryptocurrency, gaming, and several fintech businesses are also identified as institutions obligated to ensure AML compliance.

- Money service businesses (MSBs) also come under the financial institutions category that deal with money transactions worth $1000 and conduct money-related business with one one person a day. For instance, prepaid card providers, currency exchanges, money transmitters, and check cashers.

- The United States Postal Service is considered as a financial institution under the BSA law. The Department of Treasury is allowed to make regulations and guidelines to redirect the financial dealings of businesses that deal in cash.

Who Regulates AML Laws, Other Than FinCEN?

AML laws in the US are administered and enforced by the infamous watchdog, the FinCEN (Financial Crimes Enforcement Network) which works under the U.S Department of Treasury. Other than holding a significant role in regulating AML laws, it also maintains the status of being a FIU (financial intelligence unit).

However, enforcement of BSA/AML law is also ensured by several federal regulatory authorities including the following.

- SEC (the Securities and Exchange Commission)

- OCC (Office of the Comptroller of the Currency)

- Federal Reserve (the Board of Governors of the Federal Reserve)

- FDIC (the Federal Deposit Insurance Corporation)

- NCUA (the National Credit Union Administration)

To enforce global AML and combat terrorist financing, several federal bodies govern the laws in the US. Let’s dig deeper into five major anti money laundering rules in the US that shape compliance within an institution.

5 Major Federal AML Laws Compliance Revolves Around

-

The Bank Secrecy Act (BSA)

Introduced in 1970, the BSA also referred to as the ‘Currency and Foreign Transactions Reporting Act’ requires financial institutions to do the following.

- Facilitate law enforcement agencies in identifying and addressing potential acts of money laundering & terrorist financing.

- It is the responsibility of every citizen, bank, and other FIs to timely report unlawful activities associated with money laundering and maintain recordkeeping.

- Generate CTRs (Currency Transaction Reports) for transactions over $10,000 along with maintaining a structured trail of transactional records.

Providing a benchmark to stem money laundering and associated predicate crimes, several other laws were designed by making amendments in the BSA.

-

The Money Laundering Control Act (MLCA)

An amendment to BSA was made in 1986 which introduced some ground breaking rules to curb money laundering in the region. MLCA mandates the following,

- Money laundering is a federal crime while violations to BSA can cause criminal and civil forfeiture

- CTR filings should not be avoided by using structured transactions

- Banks are required to maintain recordkeeping and effective reporting under the BSA and ensure compliance through monitoring.

-

The Annunzio-Wylie Anti-Money Laundering Act (AWAML)

Effective from 1992, AWAML empowered the employment of BSA guidelines. Its clauses are,

- Refurbished penalties for BSA violations particularly, sanctions.

- Replaced Criminal Referral Forms with SARs (Suspicious Activity Reports).

- wire transfers should be conducted with verification and recordkeeping.

- Bank Secrecy Act Advisory Group (BSAAG) was brought to life under AWAML.

The USA Patriot Act

Amendments in BSA witnessed a significant change after 9/11 with enforcement on curbing money laundering to facilitate terrorism. Known as the International Money Laundering Abatement and Financial Anti-Terrorism Act of 2001, USA Patriot act presents its clauses as follows.

- Established financing of terrorism a criminal offense and endorsed customer identification measures

- Financial institutions should not work with foreign shell companies.

- Reformed AML compliance program with customer due diligence and enhanced due diligence for high-risk or international accounts.

- Extended boundaries of AML laws to all financial institutions with increased fines for non-compliance.

- Regulatory requests must be met within 120 hours to facilitate authorities with transaction information when needed.

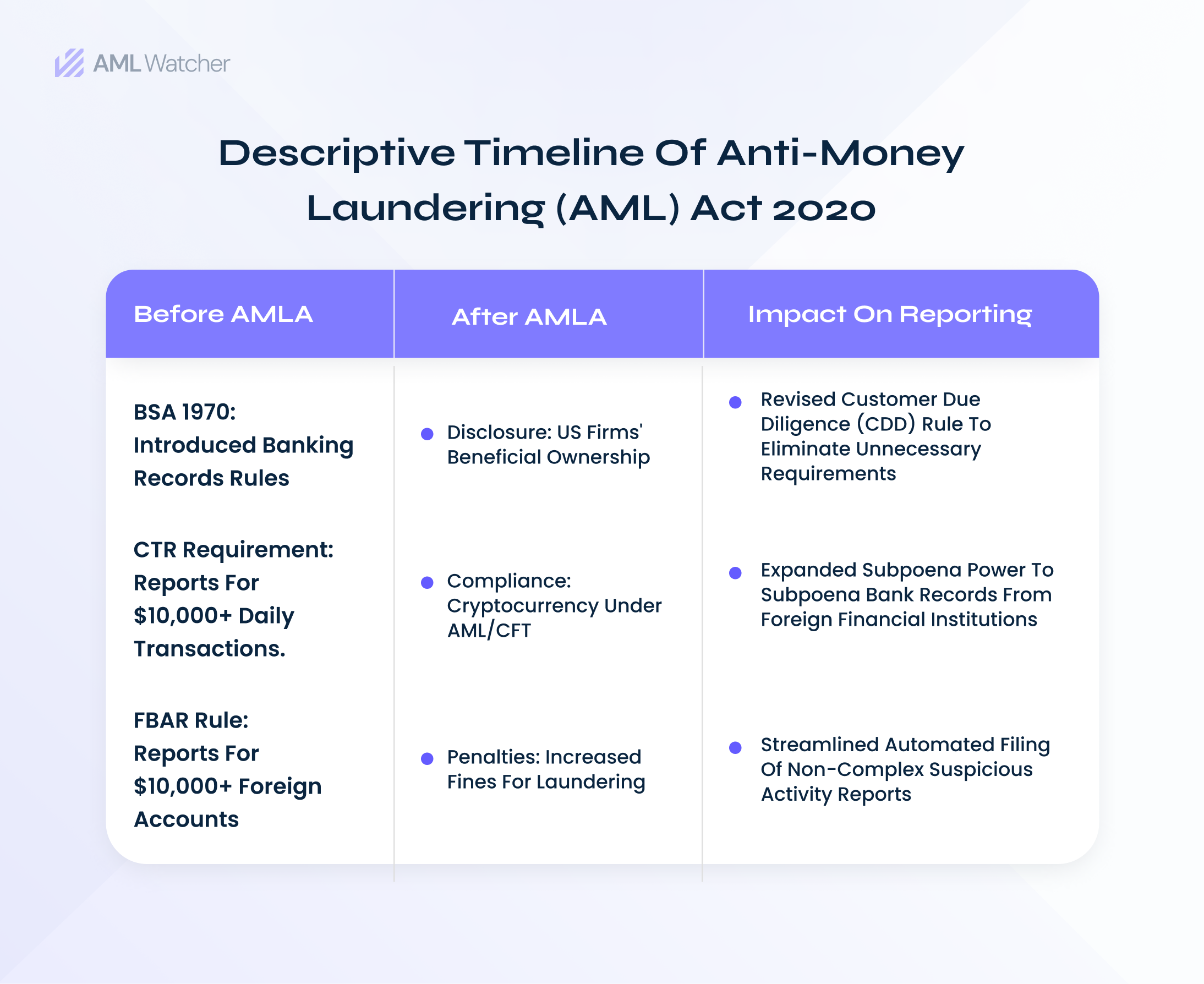

The Anti-Money Laundering Act (AMLA)

With inclusion of the CTA (Corporate Transparency Act), anti money laundering act (AMLA) was introduced in 2020, which presents a modern day solution to increasing money laundering activities. It includes,

- Requirement of identifying and reporting information on beneficial ownership while establishing a tech leveraged system to store the data safely.

- Every firm must have AML priorities to combat money laundering and financing for terrorism.

- Strengthen whistleblower program to facilitate identification of criminal activities.

Below is a detailed map of AMLA requirements of an AML compliance program.

These laws were formulated to empower the good guys law enforcement and regulatory bodies against the bad guys who launder their black money by exploiting the financial systems. It is evident that an AML compliance program is inevitable if one wants to abide by the laws, but what are the requirements of this AML compliance program? How can you reconstruct your compliance program to meet evolving needs of dynamic regulations? Let’s get into it.

3 Ways to Align Compliance with AML Rules

We have extracted the crux of AML rules in US that act like primary pillars of an AML compliance program and strengthen institutional efforts against money launderers. Let’s get right to that.

Training & Awareness of Compliance Team

Effectiveness of a compliance program relies on the understanding of the compliance team regarding regulatory requirements, emerging challenges in detecting any suspicious activity, and how the world is responding to these financial risks. FIs are encouraged to have a well aware compliance team who not only can design a customized compliance program tailored to the business needs but encourage a whistleblower program to facilitate those who help in identifying the crime.

Structured Reporting Mechanisms

The said AML laws have enforced establishment of tracking transactions and recordkeeping. Meeting the regulatory requirements of audits and reviews, institutions are required to maintain and keep records of suspicious transactions through SARs. The laws also require firms to generate CTRs if the transaction exceeds the threshold of $10,000 and keep trails of transactions.

Enhanced Due Diligence

The core objective of the laws is to combat money laundering and financing of terrorism by identifying the suspicious transactions or entities before facilitating them unknowingly. Therefore, enhanced due diligence and customer due diligence ensures to verify every existing and new client along with maintaining their changing information to effectively monitor any suspicious activity. The new AML act 2020 requires FIs to collect information on beneficial ownership to stem money laundering through shell companies.

Having that said, I would like to add that navigation through a complex web of anti money laundering laws is as tricky as navigating a maze. A complete understanding of these laws requires to be supplemented with a proactive approach, best industry practices, and compliance partners that empower your efforts.

How AML Watcher Can Help You?

AML Watcher, where research and innovation meet, our compliance partnership and technology driven approach empower you to fight against the odds and help in finding the right solution for your unique business needs. Being well-equipped with AML rules in US and other countries, our AML tools aid you to unearth complex and hidden connections of high-risks individuals.

Meeting the regulatory requirements is not a smooth process but with the right compliance partnership and expert advice, you can develop and maintain a compliance culture robust enough to fight financial crimes.

Test our screening tool for free or contact us to address your customized compliance concern.

- No commitment needed

- Complete AML Database at your service

- Access our all-in-one dashboard

Tier-2 PSPs in ... must demonstrate automated monitoring, layered CDD, &...

See the Full Regulatory Expectation70–80% less manual work, 95% less fatigue, TruRisk Agent makes compliance effortless.

Experience Agentic AMLMove Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries