A Comprehensive Guide to AML for Money Service Businesses

Anti Money Laundering

October 6, 2023

- Introduction to Money Service Businesses

- Defining the Boundaries: Who Qualifies as an MSB?

- Navigating KYC & AML in the MSB Landscape: Essential Requirements

- Understanding the Challenges of MSBS

- Ensuring Rigorous Compliance in Money Service Businesses

- AML Watcher: The Ultimate Solution to MSB’s AML Challenges

Money Service Businesses (MSBs) are currently in the spotlight as money laundering has evolved into the banking industry’s silent pandemic. These companies have unintentionally become the channels for illicit financial transfers as a result of the increased globalization of our society, making them the new front in the fight against financial crime. Even if these companies didn’t intend to contribute to the issue, figuring out the Anti-Money Laundering (AML) compliance maze has proven to be a daunting undertaking.

Introduction to Money Service Businesses

Defining Money Service Business (MSB)

An MSB is any entity or individual that specializes in money conversion and transmission. This broad category encompasses a range of businesses, from post offices and currency dealers to modern digital platforms like mobile payment applications. With the digital revolution, the MSB umbrella has expanded to include emerging financial services such as online marketplaces, cryptocurrency exchanges, crowdfunding platforms, and more. Explore AML Watcher guide to understand the AML intricacies of MSBs and ensure your business’s legal compliance.

Distinguishing MSBs from Traditional Banks

MSBs offer services similar to banks, such as foreign exchange and fund transfers, but operate under distinct regulations. Unlike banks, MSBs adhere to specific laws governing their operations, including cash conversion and fund transfers. With the rise of crypto exchanges and digital banking, many modern service providers now fall under the MSB category. Traditional client verification methods are resource-intensive and error-prone. However, neglecting AML regulations can lead to financial penalties and erode public trust.

Regulatory Compliance and MSBs

FinCEN has provided a comprehensive list of entities falling under the MSB category, which includes firms offering cash checks, money orders, stored value products, money transfers, and currency exchange services, whether for traditional or digital currencies. However, entities registered with the Commodity Futures Trading Commission or the Securities Exchange Commission are exempted from this classification.

Defining the Boundaries: Who Qualifies as an MSB?

The Financial Crimes Enforcement Network FinCEN made changes in 1999 to the rules concerning certain financial entities. These changes specifically affected non-bank financial institutions. The updated rules created a new category for these institutions called “money services businesses” or MSBs. If a business aligns with the definitions set for an MSB, it’s recognized as one. Being recognized as an MSB means that the business has to adhere to the rules and regulations set by the Bank Secrecy Act, both as a general financial institution and based on its specific MSB type. The following types of businesses can be categorized as MSBs:

- Currency traders or exchangers: This category excludes individuals who offer these services to facilitate the purchase of goods or services or for legitimate investment objectives.

- Check cashers: Businesses that cash check, money orders, or other forms of payment on behalf of the general public.

- Traveler’s checks, money orders, and stored value issuers: The companies that offer these financial instruments are referred to here.

- Traveler’s checks, money orders, and stored value buyers: The issuers or companies that cash or redeem these instruments are on the other side of this.

- Money transmitter: Any individual or organization that offers remittance or money transfer services, domestically or internationally.

- Providers and sellers of prepaid access: This refers to businesses that provide access to funds or the value of funds in a digital or electronic form, like prepaid cards.

Navigating KYC & AML in the MSB Landscape: Essential Requirements

Across the global money services business sector, adherence to Anti-Money Laundering (AML) regulations is paramount. MSBs must implement robust AML measures, encompassing:

- Documented AML strategies

- An appointed AML representative

- Educational initiatives

- Ongoing Assessment Measures

The core aim of the aforementioned regulations is to ensure strong KYC operations to reveal original customer identities.

Understanding the Challenges of MSBS

In 2017, Western Union faced heavy charges from regulatory bodies of the US because they failed to fag wire fraud and other corrupt practices happening within the umbrella of their business. The bank agreed to pay more than $580 million in order to pay for the damage caused. Coverage of more similar cases includes:

- American Express paying $25 million in cost of not having sufficient controls to stop corrupt practices.

- Thomas Haider, who was ascribed the task of monitoring that MoneyGram follows AML control, was fined $1 million as he intentionally chose to not follow the controls.

- Ripple Labs Inc. was fined $ 700,000 as their operations were being held without legal registration, giving authorities a credible reason in hand to block their operations.

Need for AML Compliance for MSBs

Money Services Businesses (MSBs) need to follow AML protocols for major reasons, coverage of some of them are as follows:

- Global and Legal Obligation: All MSBs are legally required to adhere to AML regulations to prevent money laundering and financing of terrorist activities. AML regulations are a global concern, and MSBs must comply with these rules regardless of their location.

- Financial Security: Non-compliance can result in severe penalties, loss of licenses, and reputational damage, which can be financially crippling for MSBs.

- Customer Verification: MSBs need to perform identity verification of their customers on priority and ensure that they are not facilitating any illicit activities.

- Changing Landscape: AML regulations are evolving very rapidly. Staying updated with the latest AML trends and regulations is crucial for MSBs.

Understanding MSB Challenges

The money services business (MSB) sector is strictly regulated because of its heightened potential for fraud and illicit activities.

Legitimate MSB operations encompass:

- Remittances by overseas workers to their families in different regions.

- Transactions for goods or services across vast distances or international borders.

- Business dealings between entities in different jurisdictions.

However, there are malicious intents, such as:

- Money launderers aiming to legitimize funds from unlawful endeavors.

- Terrorist organizations transfer money to support operations in the target zones.

- Deceptive individuals enticing investors with fraudulent schemes.

While the goal is not to hinder genuine transactions such as familial support, there is an imperative to prevent malicious activities such as terrorism or fraud.

The fintech sector is increasingly leveraging MSB licenses to introduce novel services, broadening the MSB definition. For instance, in Canada, cryptocurrency dealers fall under MSB regulations. However, the suitability of MSB stipulations for emerging financial services remains debatable in the absence of clear regulatory directives. Engaging with regulatory bodies proactively to ensure compliance is crucial before launching any service.

Ensuring Rigorous Compliance in Money Service Businesses

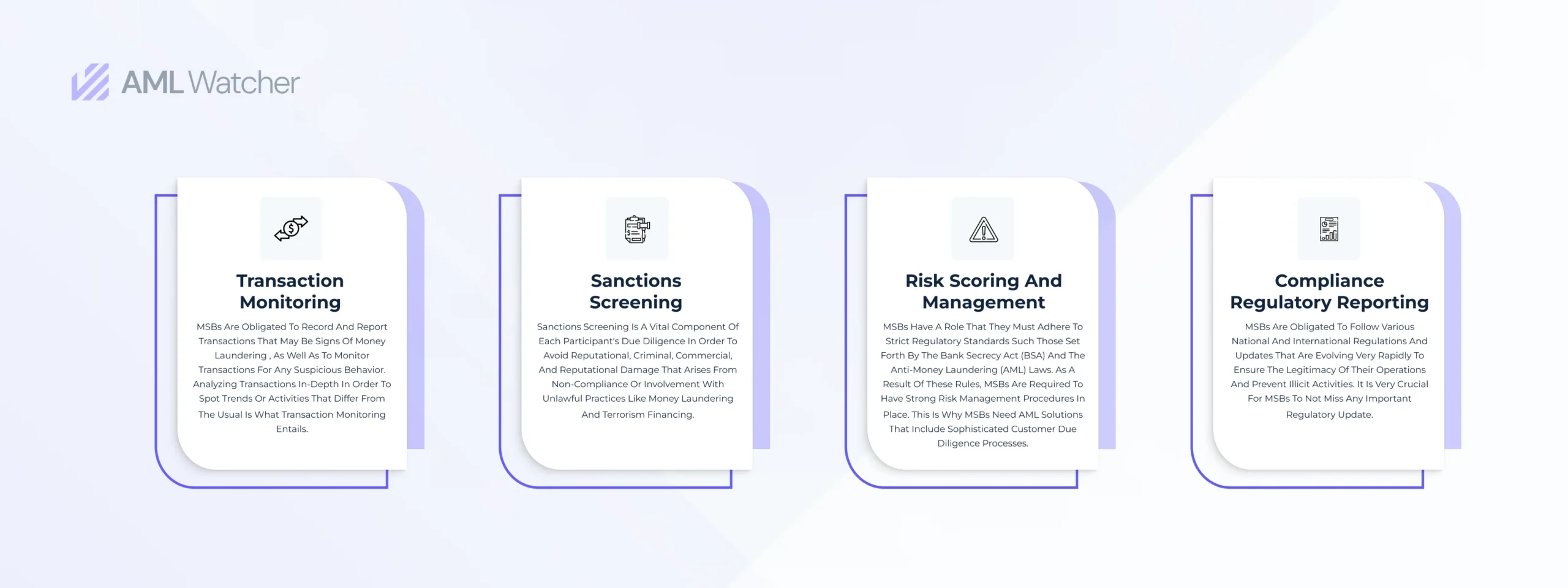

Anti-Money Laundering (AML) compliance technology has gone from being an option to becoming an absolute necessity in the world of Money Service Businesses (MSBs) due to the need to manage a sizable amount of clients, transactions, and regulatory reports.

Software specifically designed for MSB AML compliance must be given top priority when MSBs explore technological solutions because many of the available solutions, designed for conventional banking, depend on access to extensive customer data that is not usually available to MSBs. The most effective solutions combine all aspects of compliance on a single platform, enabling an efficient AML procedure. Effective transaction monitoring, keeping track of client risk scores, automating the preparation and submission of regulatory reports, and screening and filtering for sanctions lists are all crucial components to examine.

Transaction Monitoring

MSBs are obligated to record and report transactions that may be signs of money laundering , as well as to monitor transactions for any suspicious behavior. Analyzing transactions in-depth in order to spot trends or activities that differ from the usual is what transaction monitoring entails.

Sanctions Screening

Sanctions screening is a vital component of each participant’s due diligence in order to avoid reputational, criminal, commercial, and reputational damage that arises from non-compliance or involvement with unlawful practices like money laundering and terrorism financing.

Risk Scoring and Management

MSBs have a role that they must adhere to strict regulatory standards such those set forth by the Bank Secrecy Act (BSA) and the Anti-Money Laundering (AML) laws. As a result of these rules, MSBs are required to have strong risk management procedures in place. MSBs might reduce losses by monitoring and managing the risks and making informed choices. This is why MSBs need AML solutions that include sophisticated customer due diligence processes. This entails verifying the identity of customers, assessing their risk profiles, and monitoring their transactions for suspicious activities as robust CDD measures contribute to accurate risk scoring.

Compliance Regulatory Reporting

MSBs are obligated to follow various national and international regulations and updates that are evolving very rapidly to ensure the legitimacy of their operations and prevent illicit activities. It is very crucial for MSBs to not miss any important regulatory update. For example, regulatory updates related to STRs and SARs involve changes in reporting criteria or additional guidance on what constitutes a suspicious transaction. Being aware of these updates is crucial for MSBs to continue identifying and reporting potentially illicit transactions effectively.

AML Watcher: The Ultimate Solution to MSB’s AML Challenges

In today’s rapidly changing financial landscape, MSBs face the dual challenge of adhering to strict regulations while outpacing cunning criminals. The cornerstone of a successful AML compliance program lies in its adaptability, technological integration, and foresight into emerging best practices.

AML Watcher emerges as the ultimate solution to these challenges, offering a comprehensive platform that seamlessly integrates all essential AML components. With its cutting-edge analytics, it sets the gold standard in industry practices. For a future-proof, robust AML compliance strategy tailored for MSBs, look no further than AML Watcher.

Reach out to us to discover how we can strengthen your compliance journey.

- No commitment needed

- Complete AML Database at your service

- Access our all-in-one dashboard

Tier-2 PSPs in ... must demonstrate automated monitoring, layered CDD, &...

See the Full Regulatory Expectation70–80% less manual work, 95% less fatigue, TruRisk Agent makes compliance effortless.

Experience Agentic AMLMove Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries