May, 20 2025

October 3, 2024

What is Bank Secrecy Act (BSA)?

The BSA (Bank Secrecy Act) is a United States act that helps prevent money laundering by involving financial institutions that keep financial records and file daily reports for suspicious activities.

It is also known as the Currency and Foreign Transactions Reporting Act or referred to as simply the anti-money laundering law.

President Richard Nixon passed this law by the US Congress in 1970. The law provides regulations for the financial institutions that further help the Financial Crimes Enforcement Network (FinCEN), a bureau of the U.S. Department of the Treasury, to enforce and combat money laundering around the country.

According to the Bank Secrecy Act, specific rules are defined:

Who Is Responsible For Establishing The Bank Secrecy Act (BSA)?

The Bank Secrecy Act (BSA) is enforced by the Financial Crimes Enforcement Network (FinCEN) of the United States Department of the Treasury. FinCEN is responsible for establishing financial institutions’ responsibilities in combating money laundering and terrorism financing, as well as investigating suspicious actions reported to them.

Although the Office of the Comptroller of the Currency (OCC) is not the principal entity in charge of BSA regulation, it does monitor national bank compliance with the act’s standards and ensures that financial institutions follow its regulations.

What Are The BSA Rules For Financial Institutions

The “$10,000 Rule” of the Bank Secrecy Act (BSA) requires financial institutions to record transactions involving more than $10,000, either as a single transaction or several transactions by the same individual within 24 hours.

Transactions must contain cash, which includes both domestic and international currency, coins, and monetary instruments such as cashier’s checks and money orders. Personal checks, regardless of denomination, do not qualify as currency.

What Is The Main Purpose Of The Bank Secrecy Act?

The Bank Secrecy Act (BSA) prohibits financial institutions from assisting unlawful acts, including money laundering.

The BSA regulates banks, lenders, and other financial institutions, requiring them to collaborate with the government and disclose suspected activity connected to financial crimes such as tax evasion.

To ensure compliance, the Financial Crimes Enforcement Network (FinCEN) monitors BSA implementation and establishes clear recommendations for financial institutions.

Senior management in these firms must have an extensive understanding of the BSA to effectively fulfill compliance obligations.

Compliance Guidelines

- All financial institutions must verify the identity of persons opening and conducting transactions using the Know Your Customer (KYC) process.

- All financial institutions should include mandated AML regulations in their BSA/AML compliance program.

- A thorough BSA/AML risk assessment should also be carried out regularly to ensure that financial organizations detect and mitigate the risks associated with money laundering and terrorist financing.

Suggested Read: AML Compliance Guide 2024

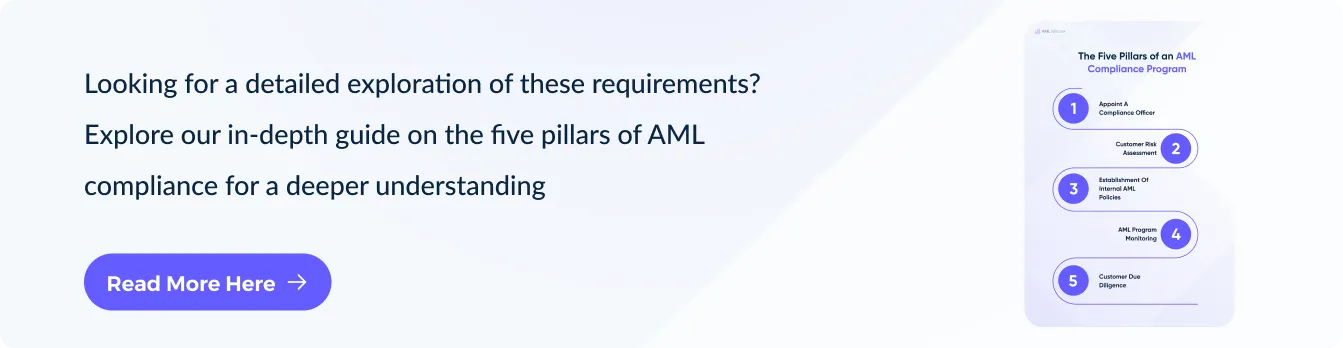

What Are The Five Pillars Of The Bank Secrecy Act?

The BSA has outlined a comprehensive five-pillar AML compliance program to help financial institutions in complying with AML requirements. As per BSA, all FIs must include in their operations.

The five primary components, or pillars, of AML compliance are

-

Compliance Officer Appointment

Designate a dedicated person to monitor and manage all AML-related activities inside the company.

-

Create Internal policies

Create and implement policies to detect suspicious activity and ensure reporting to regulatory bodies.

-

Conduct Employee Training

Create thorough AML training to help staff recognize suspicious activity and follow BSA regulations.

-

Independent Testing and Audits

Conduct frequent third-party audits and tests on AML policies to ensure they are effective and up to date.

-

Risk-based Customer Due Diligence

Execute a risk-based approach to customer screening and due diligence to better analyze possible threats.

Types Of BSA Reporting & Filing

The Bank Secrecy Act (BSA) requires financial institutions to comply with certain filing obligations and submit reports to FinCEN, including:

- CTR (Currency Transaction Report) – Form 112

- SAR (Suspicious Activity Report) – Form 111

- FBAR (Foreign Bank Account Report) – Form 114

- DOEP (Designation of Exempt Person) – Form 110

- CMIR (International Transport of Currency or Monetary Instruments) – Form 105

- MIL (Money Instrument Log) – Form 105

The BSA filing requirements may fluctuate depending on the institution’s nature and services. Financial institutions must electronically submit these documents via the BSA E-Filing system, which provides secure interaction with FinCEN and access to warnings and system upgrades.

To comply with BSA laws, financial institutions must submit the proper documents for each eligible transaction.

The forms below are used to record transactions regulated by the BSA:

Form 112: Currency Transaction Report (CTR)

Filed when a currency transaction, such as a deposit, withdrawal, currency exchange, or payment, exceeds $10,000. If several transactions totaling more than $10,000 are carried out by or on behalf of the same person, they are merged into a single transaction.

Form 111: Suspicious Activity Report (SAR)

Filed when a transaction is suspicious, such as when an insider is involved in fraud (regardless of the amount), fraudulent transactions totaling $5,000 or more by a known suspect, transactions over $25,000 by an unknown suspect, or transactions totaling $5,000 that are regarded as suspicious.

Form 114: Foreign Bank and Financial Accounts (FBAR)

Filed when an individual or financial institution has financial accounts in foreign countries worth more than $10,000, whether in securities or accounts.

Form 110: Designation of Exempt Person (DOEP)

Filed when a consumer qualifies for ‘exempt’ status from CTR filings. Only banks, not other financial institutions, can give this exemption, and they must verify the customer’s eligibility on an annual basis.

Form 105: International Transportation of Currency or Monetary Instruments (CMIR)

Filed when cash or monetary items worth more than $10,000 are physically transferred into or out of the United States by any entity, including financial organizations. (This is why Customs checks whether you have cash to report at the airport.)

Form 105: Money Instrument Log (MIL)

While not reported frequently, this form records cash purchases of monetary instruments (cashier’s checks, bank drafts, money orders, etc.) having a face value of $3,000 to $10,000. The MIL must be retained for at least five years and made available for audit purposes.

If a transaction or series of connected transactions totals less than $10,000 but is deemed suspicious, financial institutions are required to disclose it under BSA requirements.

Fines & Penalties

- The Financial Crimes Enforcement Network (FinCEN) will impose heavy fines and prison sentences on persons in financial institutions such as banks and businesses who fail to file CTRs, MILs, or SARs.

- If a person does not file (FBAR) for foreign financial holdings, he will be fined 10000$ each month until filing.

- The institutions that provide prior information about filed SAR will suffer severe consequences for violating the Bank Secrecy Act (BSA) because of their involvement in Money Laundering.

Suggested Read: TOP AML Fines Penalties You Should Avoid in 2024

While it remains a consistent challenge to abide by changing regulations, make compliance easier with an all-encompassing AML Solution.

Contact us to discuss your compliance challenges and let our experts solve that for you!

Buyer’s Guide for AML Screening Solution

Master your skills of finding the right screening solution for your business to lower false positives, achieve AML compliance, and enhance your business's efficiency.

Read Now

We are here to consult you

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries