Anti Money Laundering In Banking Sector

Anti Money Laundering

February 1, 2024

Do you know that the stability of a bank depends on the execution of two basic principles: 1) a bank’s business strategy and 2) its risk policy. When one of them fails, the results are catastrophic.

In the first quarter of the year 2023 alone, the finance industry witnessed this hands-on.

Three banking giants and one real estate firm were fined by regulatory bodies approximately $3.8 million in legal penalties for their failure to maintain risk ratings of high-risk clients, implement robust risk management, and non-compliance with anti-money laundering regulations.

Hence, for this blog, we will address the Aml meaning in banking, five most crucial and frequently asked questions one might ponder more often whenever they hear about how AML in the banking sector impacts the global financial ecosystem.

Let’s learn deeper into it before you allow a potential banking compliance risk into the financial fabric of your business.

What is AML Process in Banking?

AML stands for in banking as regulations, laws, and policies, which are designed to avert the exploitation of the financial system and prevent financial crimes such as money laundering, terrorist financing, fraud, proliferation financing, and corruption.

Since the banking sector stands on the frontlines of the global financial system to combat financial crimes, it is obligated to comply with AML regulations to avoid legal repercussions.

In other words, AML regulations act as an immune system for the financial sector, particularly banks. It helps inhibit financial crimes like money laundering from infiltrating the global economic system. And it inhibits the launderers in converting their illicit proceeds to legitimate assets.

Banks, since they are on the frontlines of the fight against financial crimes and are the first point of contact for criminals to launder their black money, are required to implement resilient and effective AML reforms and prevent the exploitation of the financial system.

What is the AML Act for the Banking Sector?

Money laundering damages the stability and integrity of both local and international financial institutions by facilitating a variety of crimes, including drug trafficking, terrorism, weapons smuggling, corruption, bribery, human trafficking, embezzlement of state funds, and many more.

Therefore, the Bank Secrecy Act, which was established in 1970, mandates financial businesses to monitor their clients and their transactional activities along with maintaining CTRs (Currency Transaction Reports), and report immediately in case of suspicious transactions.

To further strengthen alert AML procedures, the Money Laundering Control Act (MLCA) was created in 1986 to supplement the current BSA requirements. These measures include:

- Money laundering should be considered a federal offense, while penalties and other legal consequences must be imposed to counter money laundering.

- Preventing the generation of CTRs when transactions exceed their limit ($10,000) through dividing them into smaller segments should be avoided at any cost.

- Assets gained through the violations of the BSA Act should be seized as a legal punishment.

- Banks are mandated to implement efficient AML compliance measures along with maintained audit trails and recordkeeping as per the BSA requirements.

Importance of AML in banking

AML is a vital pillar for banks to support ethical business practices, regulatory banking compliance, and financial security.

The Finance industry (banking sector, insurance firms, hedge firms, credit unions, stock brokers, investment firms, etc) is the lifeblood of the international economy.

It facilitates everything from massive corporate investments to a single person’s savings.

They are the prime targets of financial criminals who seek to hide the origins of their ill-gotten gains and integrate them into the legitimate financial system.

A bank could clearly end up becoming the conduit of criminal activities like drug and human trafficking, corruption, embezzlement, terrorism financing, and so on.

Below is the comprehensive list of big banks penalized with hefty fines by the regulatory bodies as a consequence of AML non-compliance.

What are the Common Practices of AML in Banks?

Banks that operate internationally are required to integrate AML policies into their business strategy. Non-compliance leads to the reputational and legal risks associated with money laundering at all levels.

What are the Types of AML in Banking?

As per the Financial Action Task Force (FATF) on anti-money laundering, a responsive compliance culture, along with a strategic risk management framework, can be built through implementing the following key areas.

Customer Due Diligence (CDD)

A globally endorsed AML measure, customer due diligence is primarily guided and regulated by the Financial Action Task Force (FATF) to be a foundation of active risk management and banking compliance programs.

Implementation of CDD requires financial institutions to ensure key areas of compliance, including,

- Collection of customer data for identification and verification of the data through reliable means.

- Assessment of the magnitude of risk associated with a client by understanding the nature of the client’s business.

- Maintaining the updated information of clients throughout the business relationship.

- Building risk profiles of every customer to conduct risk-based assessments.

- Enhance the risk assessment for high-risk clients such as politically exposed persons (PEPs)

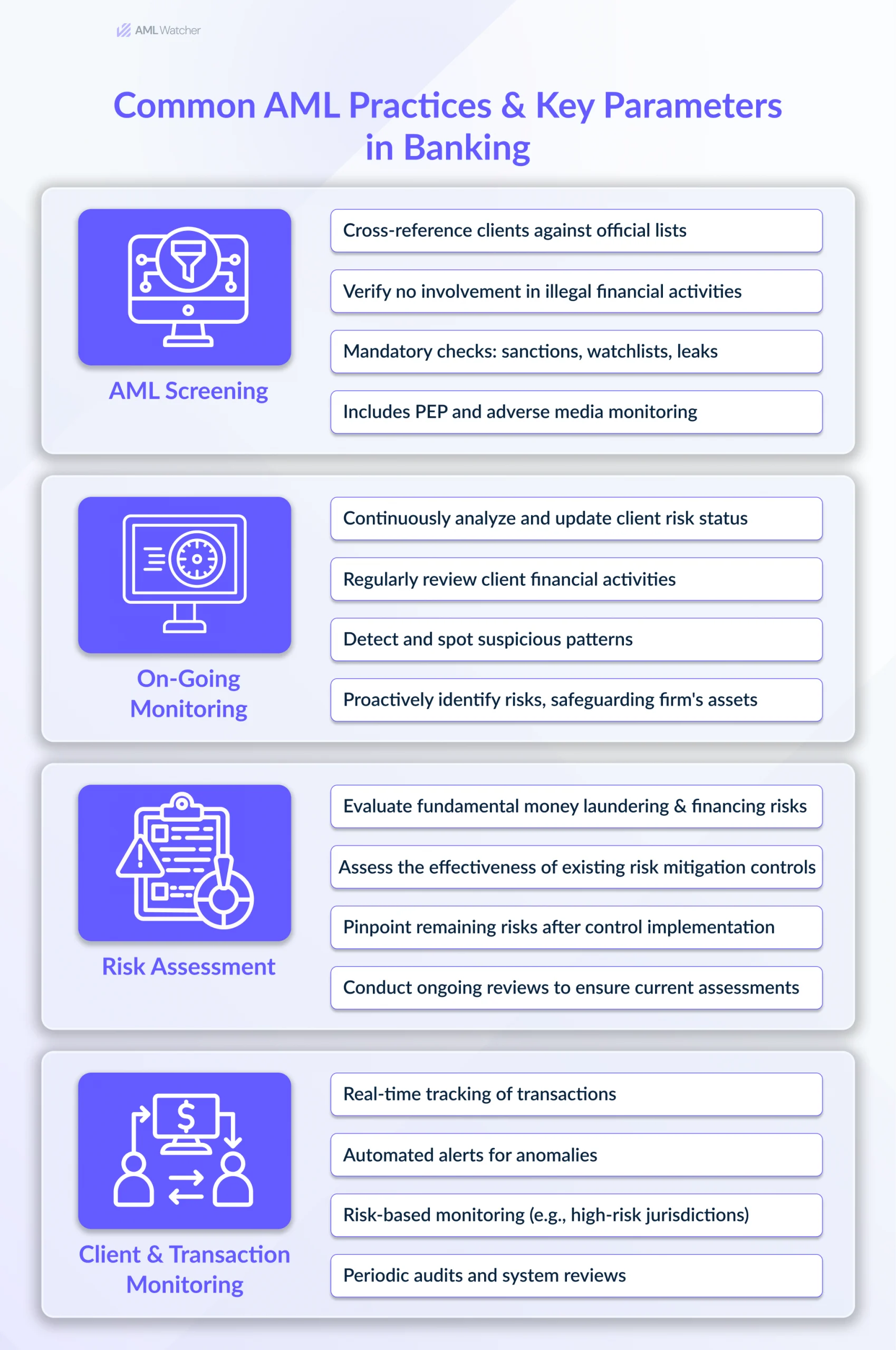

AML Screening

AML Screening is a risk-based approach, used by banks to cross-check their potential and existing clients against official lists issued by governmental organizations, law enforcement agencies and regulatory bodies.

AML screening process is conducted to verify the clients are not involved in any illegal activity, including terrorist financing, embezzlement of state funds, money laundering,

Banks are mandated to conduct the following protocols as part of AML screening processes, including sanctions & watchlist screening, the International Leaks Database, crypto wallet & vessel screening, and PEP & adverse media monitoring.

On-going Monitoring

Banks conduct ongoing monitoring of their existing clients to consistently analyze and update clients’ risk status and review clients’ activities, like their financial transactions, to detect and prevent money laundering, terrorist financing, or other financial crimes.

This proactive approach helps them with the early identification of potential risks before the occurrence of financial misconduct, and helps safeguard the firm’s assets and long-term reputation.

Risk Assessment

Banks employ risk assessment to understand, assess, and identify anti-money laundering risks. They conduct AML/CFT protocols to have a risk-based approach (RBA)

Banks conduct risk assessment by continuously updating their clients’ profiles to spot any suspicious behaviour in the clients’ transaction activities that can pose a potential threat.

Risk assessments and risk profiling help firms prevent fraud when investigating suspicious activities or freezing assets to prevent loss of reputation of the institution and loss of its customers.

It helps firms sustain their stability as illicit activities are detected, spotted, reported, and prevented before they even occur.

Client and Transaction Monitoring

Businesses can proactively detect and stop any money laundering activities and maintain compliance for a global cause by using sophisticated technology (AI/ML) to measure the effectiveness of AML procedures within the banking aml compliance system and client and transaction monitoring.

To counter financial crimes, the Financial Conduct Authority (FCA) of the UK and the Office of the Superintendent of Financial Institutions (OSFI) of Canada have established AML guidelines for banks enforcing strong AML procedures through client and transaction monitoring.

- Employment of real-time and ongoing monitoring systems that oversee the changes in client data and transaction behaviors.

- Automation of trigger alerts when the status of a client changes in any database to initiate a need-based assessment.

- Establishment of risk-based monitoring for high-risk profiles and robust maintenance of the risk profiles of every client.

- Regular and need-based audits and reviews of monitoring systems and processes to identify any loopholes.

Why Banks Fail to Implement Functional AML Compliance?

The vitality of AML compliance required by the financial sector, particularly banks, does not negate the fact that it comes with its own particular and global challenges, making it an overwhelming task.

Let’s dive into the intricacies of AML that expose the banks to non-compliance and unwanted reputational falls.

Dynamic Regulations and Implementation Lag

To keep pace with evolving laundering practices, the regulations keep getting stricter and open to uncertainties, while leaving the institutions off guard and vulnerable to non-compliance.

The evolution of regulations causes banks to lag in implementing them in the existing compliance framework.

Integration of Evolving Technology

The ease of compliance empowered by technological advancements is unquestionable; however, technology has also facilitated the crime actors in carrying out money laundering activities with more sophistication.

Continuous upgradation of technology to cater to the evolved criminal pathways often leads banks to use outdated technology, which in turn results in AML compliance failure.

Resource Constraints & Complex Screening Tools

Draining the resources of institutions for regular training of compliance forces to align with monitoring requirements, the complexity of screening tools for AML checks makes it difficult for banks to identify and manage AML risks.

Harmonizing Compliance & Customer Experience

A sophisticated balance between compliance measures and customer experience is an essential parameter to measure the effectiveness of a bank’s business strategy.

The prolonged customer identification and verification procedures put the customer on hold, resulting in reduced customer satisfaction.

To secure the business or meet client expectations, banks often overshadow the apparent risks and onboard the clients without performing the required due diligence.

How AML Watcher Can Help You Stay Compliant?

AML Watcher, with its fully automated screening tools, helps you to meet evolving tech and regulatory requirements.

We at AML Watcher offer a comprehensive AML solutions for banks that includes crypto wallet & vessel screening, sanctions & watchlist screening, the International Leaks Database, and PEP & adverse media monitoring.

From Fintech to Gambling, Crypto to Legal sector, we secure the world’s most sensitive financial operations.

Book your FREE DEMO and overcome the compliance challenges that might be costing your business.

Frequently Asked Questions

In banking, AML stands for regulations, laws, and policies designed to prevent the use of the financial system for financial crimes such as money laundering, terrorist financing, fraud, proliferation financing, and corruption. Since the banking sector is at the forefront in combating financial crimes, it is obligated to comply with AML regulations to avoid legal repercussions.

The stages of AML in banking from an AML compliance program perspective include customer identification and verification, screening, risk assessment, risk-profiling, ongoing monitoring, transaction monitoring, and suspicious activity reporting.

AML checks in banking mean conducting anti-money laundering procedures to detect and report any suspicious activity about a customer being involved in illicit activities such as money laundering, corruption, terrorist financing, and fraud. AML checks include KYC, CDD, risk assessment, including screening for adverse media, PEP lists, sanctions, and watchlists.

The primary body that imposes sanctions on countries and individuals in the US is the Office of Foreign Assets Control (OFAC), a part of the US Department of the Treasury.

- No commitment needed

- Complete AML Database at your service

- Access our all-in-one dashboard

Tier-2 PSPs in ... must demonstrate automated monitoring, layered CDD, &...

See the Full Regulatory Expectation70–80% less manual work, 95% less fatigue, TruRisk Agent makes compliance effortless.

Experience Agentic AMLMove Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries