How BSA/AML Help With Fighting Financial Crimes in 2024?

Anti Money Laundering

February 20, 2024

Fostering a globally stable financial ecosystem where the delicate balance of technological innovation to screen out corrupt actors and regulatory reforms, the BSA AML (Bank Secrecy Act/ Anti-Money Laundering) offers an immunity to the financial institutions against laundering of illicit money collected through organized crimes. Endorsement of the BSA/AML compliance is not just restricted to businesses but the associated individuals are required to follow the same rules.

Consented to pay $100,000 in Jan 2024, a former BSA Officer at NYSEFCU (New York Federal Employees Federal Credit Union), Gyanendra Kumar Asre was imposed with a civil money penalty (CMP) for violating the Bank Secrecy Act (BSA) and regulations. Absence of efficient AML compliance measures lead to the dissolution of NYSEFCU which leaves a reminder for institutions to conduct effective BSA/AML risk assessment for compliance.

How can the BSA/AML program be deployed to ensure compliance while overcoming the possible challenges is what we will be digging in today. Let’s dive in to navigating the web of regulations and building resilience against emerging financial crimes.

When did Money Laundering Become a Federal Crime?

The so-called and infamous term of money laundering was derived from the phenomenon of turning illicit proceeds to clean assets and allowing the gold-washed assets to push into established financial flow with minimum to no clue left for crime fighters leaving a blind spot of suspicion.

Typically executed in a well structured way, laundering the dirty money involves its placement into a clean financial system, an illusionary movement of the proceeds is created to blindfold the tracking usually dubbed as layering, and followed by the integration into a legitimate financial system until the money appears clean while the illusionist performs the dazzles with hand sleights. The deteriorating nature of money laundering not only facilitates the organized and united crime actors in accessing their drug and terror related money but also sustains the globally declining economy. The nature of events to launder money can be visualized in the below display.

With the evolution of civilizations and businesses across the globe, the tracking of complex transactional web and laundering networks has become more challenging for the regulatory gatekeepers and business owners. The growing concern of money laundering gave birth to the Bank Secrecy Act (BSA) followed by the Money Laundering Control Act in 1986 while establishing money laundering as a federal crime. If you are wondering what BSA/AML is, let’s get right to that.

What is BSA/AML?

Currently governed by the Financial Crime Enforcement Network (FinCEN), the BSA/AML was passed in 1970 with a mission to protect institutions to facilitate the money laundering and associated predicate crimes such as terrorist financing and proliferation funding. The bank secrecy act which is also referred as anti-money laundering (AML) law and the Currency and Foreign Transaction Reporting Act advises the following,

- A clear recordkeeping and reporting of suspicious activities by the financial institutions and associated individuals.

- Identification of source, nature, and route of the transactions or monetary proceeds happening in the U.S.

- Submission of the Currency Transaction Reports (CTRs) when the threshold of cash transfer exceeds $10,000 and Suspicious Activity Reports (SARs) to be reported by the financial institutions.

To support the effective combating of money laundering and financial illicit activities under the umbrella of BSA/AML regulation, numerous other statutes and laws were hosted by the institutions to meet the AML regulatory requirements.

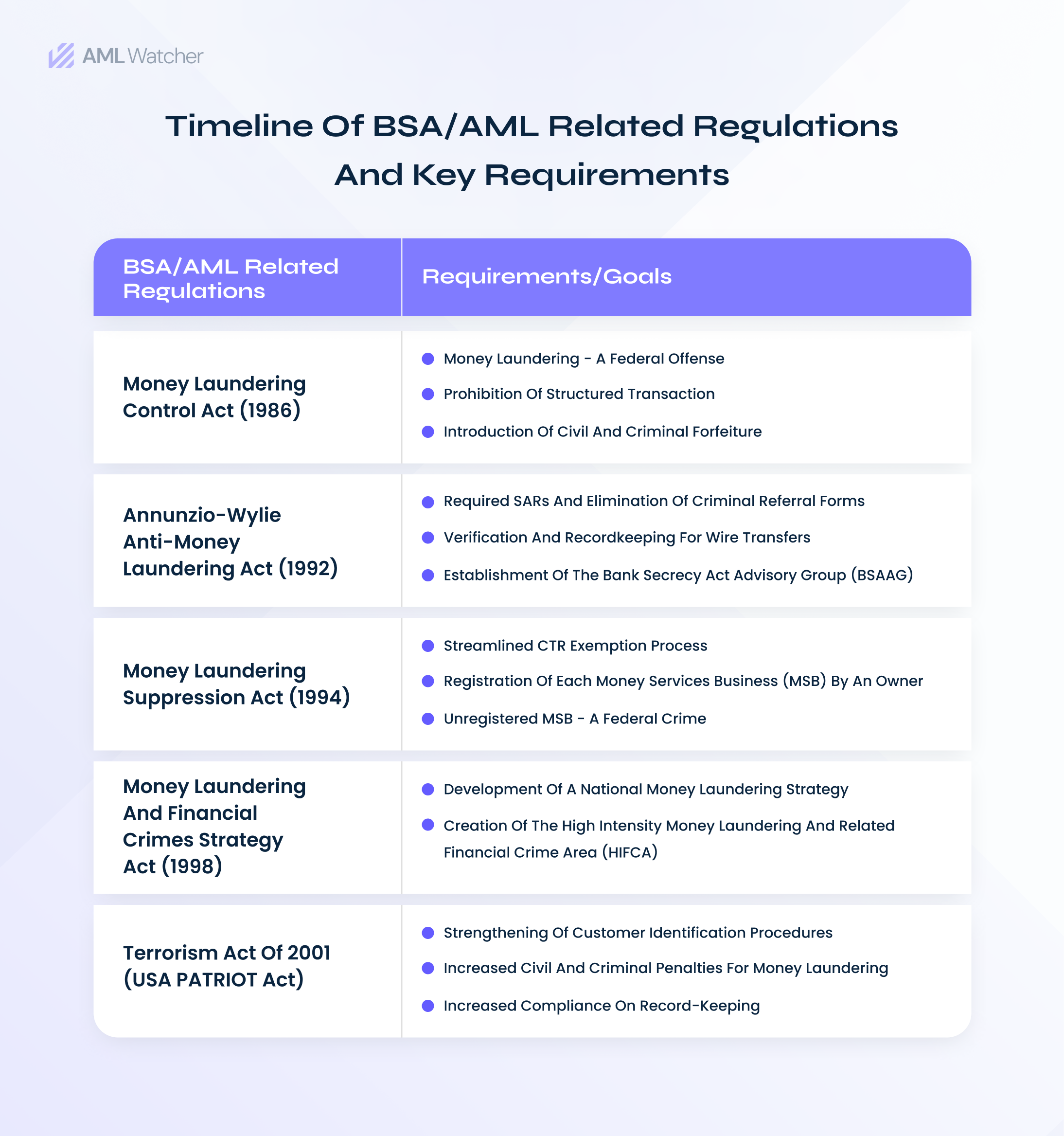

BSA/AML Related Regulations You Should Be Aware of

After the enactment of BSA/AML to meet record-keeping and reporting requirements, several amendments in the act were made to empower its guidelines and implementation. The general guidelines and enforcement of the related laws have been demonstrated below.

What Does the Future of BSA/AML Amendments Look Like?

After the passage of one of course changing developments in the regulatory environment, the AMLA (anti money laundering act), ENABLERS (Establishing New Authorities for Businesses Laundering and Enabling Risks to Security) proposes more stringent compliance measures. It redefines the definition of financial institutions that are required to implement BSA in their compliance framework, which includes lawyers, accountants, art and antique dealers, financial advisors, and third party payment service providers. However, the final form of the act will decide the exclusion or inclusion of businesses to be obliged under the act.

It is equally important to understand if your business comes under the obligation to BSA/AML policy.

Who Comes Under the BSA/AML Obligations?

The BSA/AML risks require the individuals, financial institutions (banks), and non-bank financial institutions in the United States and members of its jurisdictions to adopt effective processes and tools to combat financial crimes and meet the AML compliance demands. The Department of Treasury (FinCEN) classifies the general types of businesses that covers the category of non-bank financial institutions which are,

- Currency dealers or exchangers

- Check cashers

- Issuers and sellers of money orders or travelers’s checks

- Money transmitters

While no one is above the board when it comes to meeting the compliance requirements, the violations to BSA/AML compliance cost hefty monetary (civil money penalties) and reputational damages. The absence of effective AML measures indifferently facilitates the corrupt doers in rusting the global economy through illicit financial activities and loss of business integrity comes as a cherry on the top. It is crucial to align your business compliance with the all rounder BSA/AML guidelines to prevent the legal and monetary consequences as shown in the below visual.

Does your Compliance Program Meet BSA/AML Guidelines?

Looking at the gore consequences of mere negligence in BSA/AML compliance measures might make one wonder how to identify and overcome the loopholes of existing compliance measures. It is difficult but not impossible to navigate through. Let’s dig into the consolidated and imperative compliance measures which require an intricate alignment with the bank secrecy act.

Establishment of Policies & Procedures

The record-keeping and reporting requirements of the BSA/AML act must be established through outlining a well-written policies and procedures approved by the higher authority, for instance board of directors. The policies and processes are required to be outlined in a way that they must address the evolving AML risks associated with the business.

Internal Control & Ongoing Monitoring

The BSA regulatory expectations must be met through implementation of internal controls and ongoing monitoring of high-risk profiles along with conducting customer due diligence, transaction monitoring, and effective AML case management. To keep pace with the evolving regulatory demands and stem advanced money laundering ways, the businesses are required to ensure regular and ongoing monitoring by means of integrating technology into compliance tools and training of compliance forces.

Customer Screening & Assessment

The development of customer identification program (CIP) coupled with the risk-based approach to screen and monitor your customer or business partner is certain to meet the BSA/AML requirements. Endorsing the enhanced due diligence and FinCEN requirement to obtain beneficial ownership information, businesses are advised to verify and screen their customers. It also requires the assessment of their affiliation with entities who are more likely to abuse the financial system. Various screening tools such as adverse media screening, politically exposed persons check, and sanctions check enables the institutions to do the needful.

Evaluation of Program & Information Sharing

The established policies and procedures are required to be evaluated by the determined examination authority to check if the existing measures meet the evolving demands of BSA/AML risks. These findings should be then communicated to the relevant bank management in the form of a report of examination (ROE). Based on the assessment, the required adjustments to the existing compliance program need to be documented and supported.

Is it Possible to Find a Consolidated Solution to Meet BSA/AML Requirements?

It’s undebatable how the regulatory requirements of the BSA/AML are changing to stem the illicit financial activities. Where the unforgiving regulatory environment shows no mercy, the question arises is it possible to adopt a consolidated and automated solution which not only aligns with the evolving regulations but creates resilience against the launderers to infiltrate into the financial system? A perfect blend of human and artificial intelligence can create such a wonder where compliance is driven by research and innovation. AML Watcher brings you the ease of regulatory burden while the screening of your new clients and monitoring of existing clients is easier than ever.

Staying compliant is not a piece of cake but the right decisions at the right time creates an everlasting impact. Explore AML Watcher’s live screening tool and stay ahead of the compliance ambiguities.

We are here to consult you

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries