How Can FIs Enhance Compliance with Advanced AML Models?

Anti Money Laundering

September 19, 2025

Monitoring financial crimes is a continuous struggle for banking, insurance, and payment-related firms. On this issue, The Wolfsberg’s Group issued a statement on “Effective Monitoring for Suspicious Activity”. This statement highlights that static AML models are not enough to address contemporary FinTech industry problems such as low-quality outputs, poor governance, high compliance costs, and insufficient adaptability to evolving threats.

Static AML models mostly identify the red flags only after they occur, which means businesses can only stay reactive rather than taking proactive steps. That’s how businesses working with such models usually struggle to keep pace with emerging threats and changing regulatory expectations.

This limitation results in genuine challenges in adherence. Static rules can only spot suspicious patterns after the fact, which means that potential money laundering can go unnoticed while it’s happening. As a result, preventing risks becomes challenging, and compliance costs rise because resources are wasted on investigating alerts that do not give useful predictions.

When AML models cannot accurately predict risk, they not only fail to prevent financial crime but also drive up operational costs.

Let’s dive in and understand what kind of AML models are a requirement of today’s world and why, FIs can integrate them, and what their benefits are:.

How Exactly Are Money Laundering Threats Evolving?

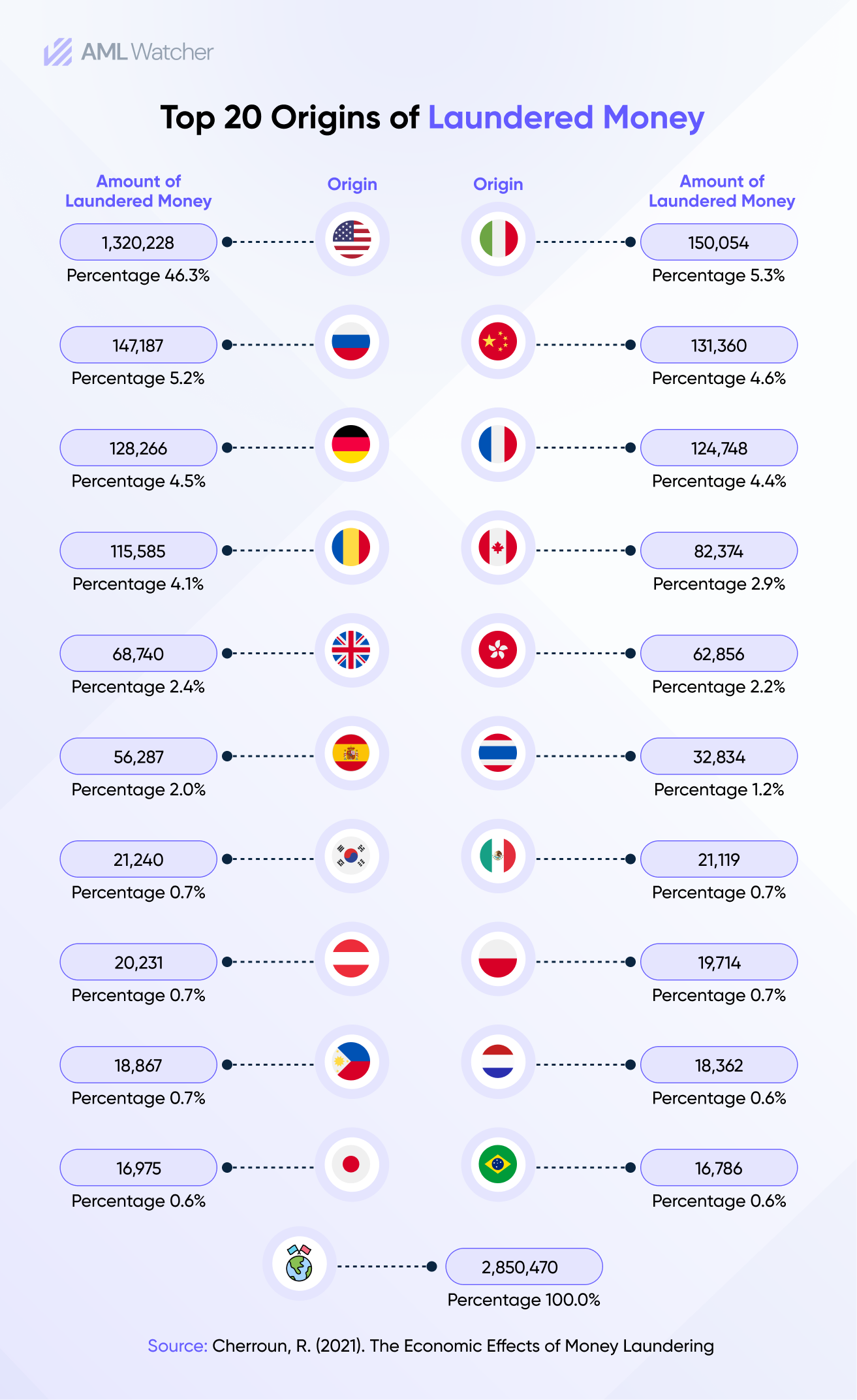

Money laundering is no longer confined to shell companies or traditional layering. Criminals now use more advanced strategies that involve fraud typologies and even cybercrime. Fraud schemes such as mule accounts and identity theft generate billions that are laundered through financial institutions, while organized crime groups take advantage of loopholes across different countries’ financial systems and regulatory expectations..

At the same time, crypto mixers, privacy coins, and shifting geopolitics create new risks. For instance, a country once seen as low-risk can later become high-risk. This dynamic environment makes it clear why financial institutions need solutions that can adapt to fast-changing data, analyze risk in real time, and capture hidden links across fraud, cybercrime, and illicit networks.

Why Static AML Models No Longer Work?

Static anti-money laundering models must be replaced because they are archaic, inflexible, and unable to adapt to changing regulatory requirements. The anomalous behaviors of customers are difficult to understand through these rule-based systems, which are pre-configured and don’t take into account evolving threat typologies. This ultimately led to inefficiencies like high false positives and ignoring the genuine risks.

To make a more precise and cost-effective environment, FIs must prioritize AML model development that integrates dynamic and AI-powered approaches.

Businesses must replace the static AML models, which can have certain limitations, including:

-

Inability to Detect Transactions Related to Latest Typologies

When stagnant AML models don’t take into account the latest threats, they can’t detect suspicious transactions associated with advanced money laundering techniques. This indicates that rule-based AML modules can avoid high-risk transactions, leaving ample room for money laundering.

-

Inflexible and Outdated Algorithms

Legacy systems mostly use batch processing and outdated algorithms, which prevent them from handling real-time data and adapting to emerging regulatory shifts.

-

Dynamic Customer Behaviour

The risk level associated with a customer also changes over time. A customer who is considered low risk during onboarding may later show suspicious behavior, such as transacting with a customer based in high-risk jurisdiction. Moreover, the very definition of what constitutes a high-risk jurisdiction can also change due to reasons like geopolitical conditions. This means if the company has integrated static models, they are unable to accept these changes and might end up onboarding a launderer.

-

Focus Shift from High-Risk Cases

Reliance on legacy AML risk assessment models generates a lot of false alerts, and handling this massive volume can be resource-intensive and even a diversion from the actual high-risk cases.

-

Consequences of Non-Adherence with Real-time Updates

Regulatory enforcement updates its requirements with time, which makes the static models struggle to adapt, resulting in heavy fines and reputational damage.

-

Over monitoring of Low-Risk Clients

Legacy models mostly result in blanket approaches for investigation that lead to over-monitoring of low-risk clients and the wasted use of expensive investigative resources.

-

Rising Costs

Static AML models increase the overall cost of ownership by diverting the resources’ focus from high-risk cases and creating gaps in the investigation throughout.

What Should FIs Opt For?

Here are a few aspects that will help FIs in deciding what kind of AML models they must look for when moving towards an advanced solution.

-

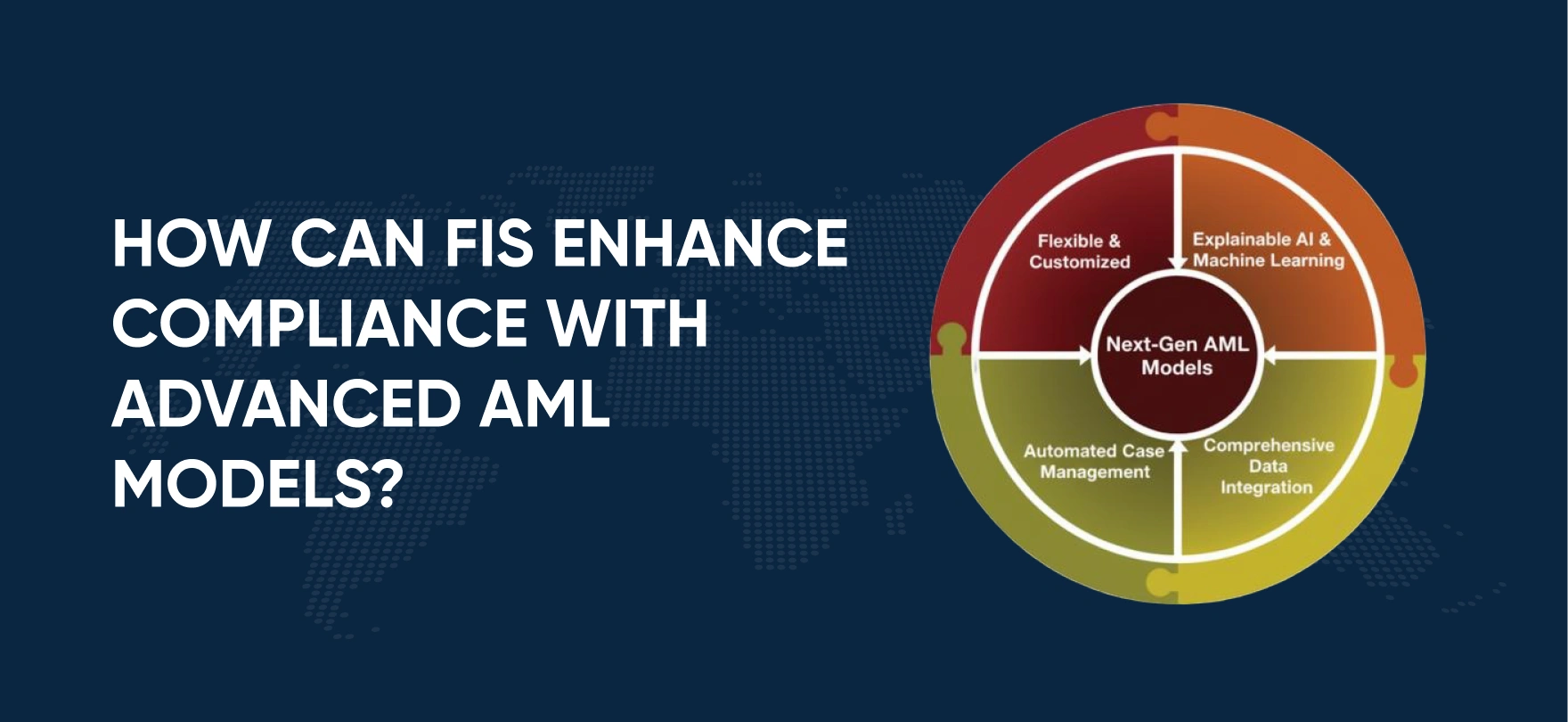

Explainable AI and Machine Learning for Enhanced Detection

FIs must look for advanced solutions powered by Machine Learning and AI to spot anomalies in real-time. These tools learn hidden patterns in large transaction data sets and continuously adapt to evolving laundering schemes. Leading solutions even tag each alert with explainable “reason codes” or scores so analysts can audit why a transaction was flagged. This explainable-AI approach aligns with regulatory expectations, which leads the respective financial institution to “own” their models by validating and documenting every decision.

-

Comprehensive Data Integration and Coverage

High-quality and precise data is the basic requirement of an effective AML detection. FIs must look for advanced AML models that have a proprietary database sourced from authoritative lists such as OFAC, HM Treasury, OFSI, United Nations Security Council, or corporate ownership data. The model must be equipped with continuous adverse media monitoring. Instead of weekly manual updates, screening and transaction checks happen in real time as new customer data or transactions arise.

-

Automated Case Management and Workflow

Automated case management reduces manual work by auto-populating cases with customer data, transaction history, rules, and linked intelligence. These systems also route cases to the right analysts and create audit trails for regulators. But rules and risks change all the time, sanctions shift, and countries and people both can quickly move from low to high risk. That’s why automation must be paired with human insight. Augmented intelligence combines both to ensure faster reviews without losing sound judgment.

-

Customized and Flexible Approach

FIs must look for a solution that is flexible enough to integrate with the existing systems without expensive upgrades. These flexible platforms must offer open APIs, a modular design to plug into core banking, EDD/CDD systems, data warehouses, or payment gateways without a full overhaul, which can be deployed on-premises or in the cloud. This modularity allows customization, for example, enabling industry-specific risk rules or custom dashboards for different compliance teams.

-

Clear Reasoning within Investigation

FIs must look for modern AML platforms that emphasize explainable AI because in them every alert comes with documented justification (feature importance, reason codes, or risk scores) so examiners can understand why a transaction was flagged. In addition to Built-in AML model validation tools, advanced AML model risk management helps compliance teams test changes safely (often in sandbox environments) and generate performance reports on alert volumes, hit rates, and turnaround times. This auditability makes it easier to demonstrate to auditors that models are sound and thresholds are well-governed.

Turn AML Compliance into a Strength with AML Watcher

Traditional AML models often feel like a costly checkbox; the wrong one can drain resources and leave dangerous blind spots. But with the right strategy and tools, AML can become a market differentiator for financial sectors aiming to expand while navigating the risks. Firms that invest in robust risk-scoring models, diligent validation, and modern detection technology can promptly detect illicit finance, satisfy regulators, and operate more efficiently with greater transparency. The benefit is not only that FIs can save them from fines, but it can also protect clients and the entire financial system.

If your business wants to switch to an AML Solution that evolves according to your dynamic risk exposure, consider a partnership that helps you comply in line with your compliance program. AML Watcher is designed to address a comprehensive range of compliance challenges by offering the following capabilities:

- Global coverage across 215+ jurisdictions from sanction lists, including OFAC, OFSI, HM Treasury, and the EU, to help institutions stay compliant with evolving regulatory requirements.

- An AI-powered adverse media screening platform that is built to reduce manual exertion of data gathering for flagging a sanctioned, watchlisted, or PEP entity.

- Real-time risk scoring using machine learning and advanced analytics to enhance detection accuracy or speed, and reduce false positives.

- Integrated model governance tools, including safe testing environments and performance analytics, to help institutions validate model changes and track alert efficiency.

- Explainable AI alerts for compliance officers to see exactly why a transaction is flagged.

- A configurable platform with open APIs that plug into existing systems and an adaptive system that is customized to a business’s unique risk profile.

Partner with AML Watcher to gain AI-powered screening and monitoring tools that help you comply in line with your risk exposure and risk appetite, and encompass the regulatory requirements.

- No commitment needed

- Complete AML Database at your service

- Access our all-in-one dashboard

Tier-2 PSPs in ... must demonstrate automated monitoring, layered CDD, &...

See the Full Regulatory Expectation70–80% less manual work, 95% less fatigue, TruRisk Agent makes compliance effortless.

Experience Agentic AMLMove Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries