SEPA Regulation – Why Does it Matter for the Payment Service Providers?

AML Regulations

February 20, 2025

SEPA Instant Payments are now the standard, making euro transfers faster than ever. Instant Payments Regulation (IPR), effective from January 9, 2025, mandates, transactions must be processed within 10 seconds.

This requirement pressures banks and Payment Service Providers (PSPs) to keep up with that speed. The instant SEPA Cross border payments challenge compliance teams, who are expected to verify the entities within a matter of seconds.

Under Regulation (EU) 2024/886, PSPs are expected to screen their clients before onboarding. However, the instant speed makes it difficult to verify the payments and sometimes leads to rejected payments.

Another significant change in SEPA Cross border payments and SEPA banking is coming on October 9, 2025, with new rules for outgoing payments and Verification of Payee (VoP).

Adapting to SEPA Instant Payments requirements isn’t just about upgrading technology; it’s about following EU regulations and building customer trust in the SEPA Zone. However, many banks are still unprepared.

As Yoann Vandendriessche, Chief Product Officer at Intix, points out, only “1 in 3 European banks feel ready for mandatory instant payments”.

With the above-mentioned challenges, the key questions that came to an individual’s mind are:

- Are EU financial institutions truly prepared for SEPA?

- How can European Union PSPs screen clients for EU restrictive measures in under 10 seconds?

Let’s read this article to find all these answers about What is SEPA and SEPA regulations.

The Dawn of SEPA – A Unified Vision

SEPA stands for Single Euro Payment Area; it was created by the European Payment Council (EPC) with support from the European Commission and European Central Bank (ECB) to harmonize EU electronic payments across Europe.

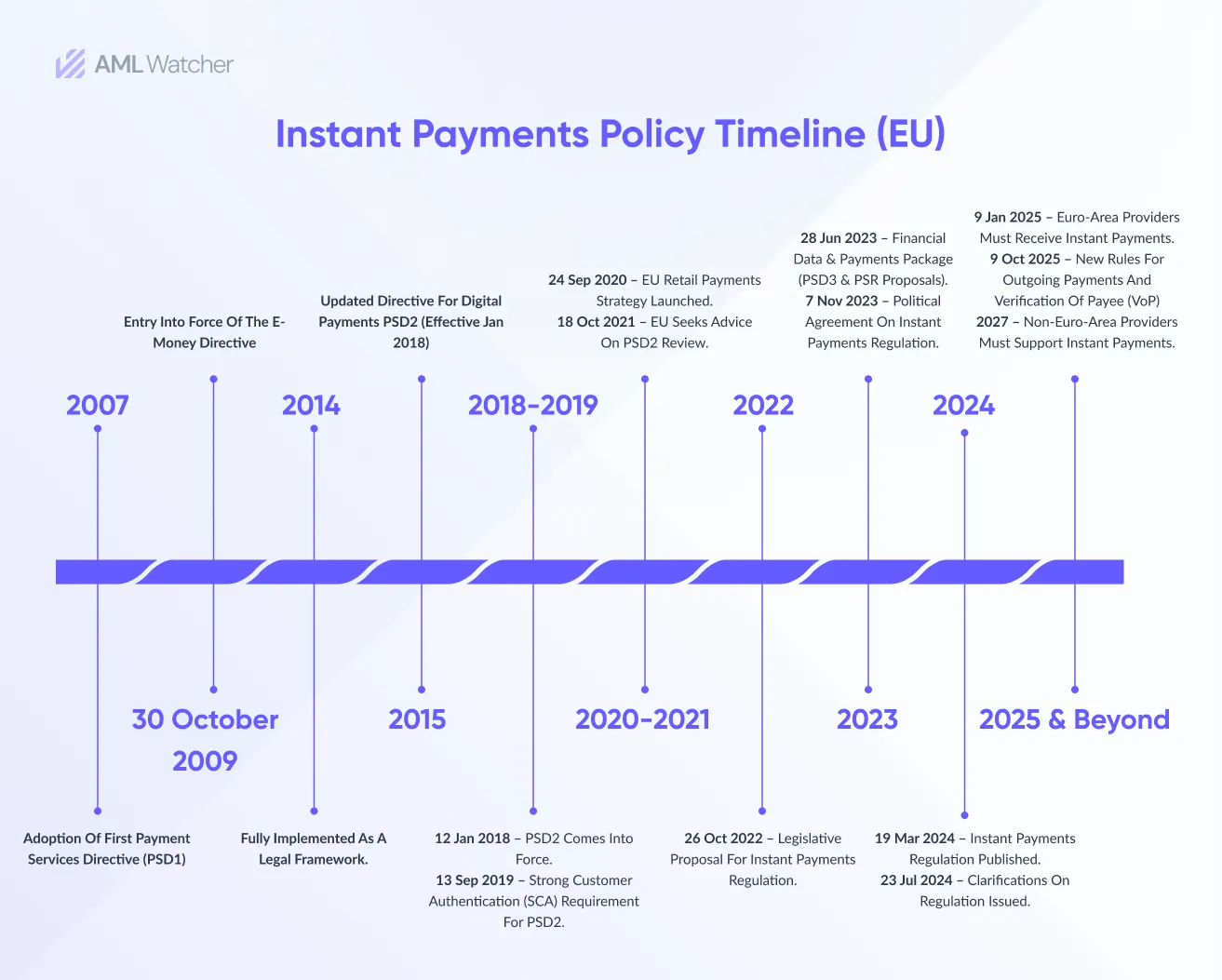

Its legal framework was initiated for credit transfers in 2007 under Payment Services Directive 2007/64/EC. 2014 was the year when SEPA was fully implemented with a deadline in the Eurozone countries.

Later on, in 2016, this regulation was extended to include some non-European countries. In 2017, it started to cover card payments, introducing SEPA for cards and instant credit transfers (SCT inst.).

In January 2024, new instant payment regulations were enacted, mandating real-time euro credit transfers. As of Jan 2025, payment service providers (PSPs) must offer instant payments within 10 seconds.

Developers are continuously working on enhancing SEPA regulation’s security, efficiency, and cross-border payment capabilities within or beyond the eurozone.

These enhancements align with the EU’s also focus on anti-money laundering (AML) measures for payment service providers (PSPs).

SEPA Regulation – Know Why it Matters?

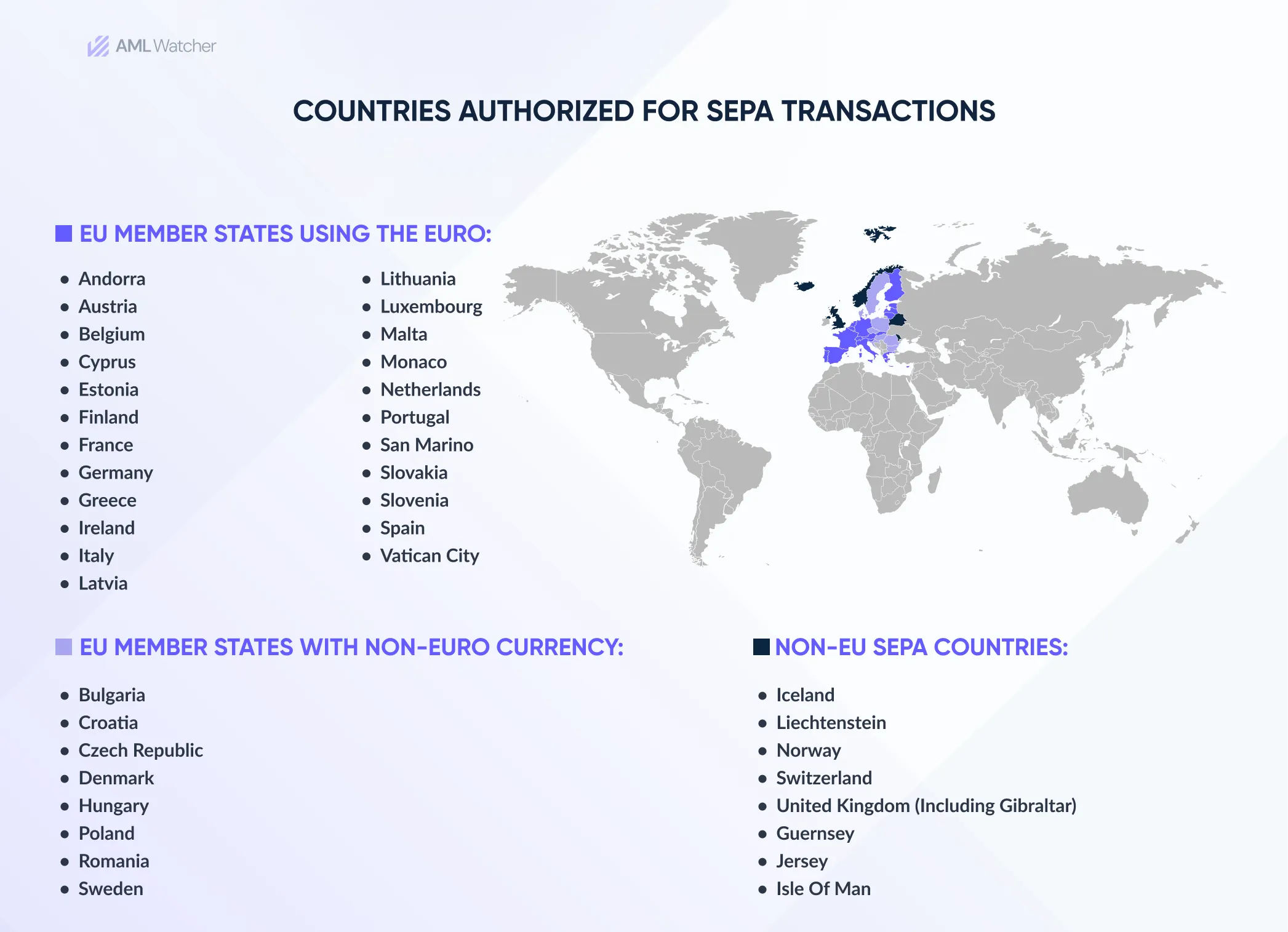

SEPA Meaning Single Euro Payment Area is a financial initiative taken by the EU to streamline and standardize the Euro payments across European countries. It consists of 38 European countries, including many that are not part of the euro region.

The primary objective of this initiative is to make cross-border payments as convenient and quick as domestic payments.

Before SEPA, payments were challenging to proceed, as each European country had its own banking rules that slowed down cross-border payments and made the processes way more costly.

SEPA Payment Processing Schemes

The SEPA zone was formulated to support the European Union’s (EU) single market. SEPA payment schemes have rules for:

SEPA Credit Transfer Scheme (Operational in January 2008)

This scheme was used to transfer payments between two bank accounts existing in the SEPA participating countries using the Euro currency.

SEPA Direct Debit Business-to-Business Scheme (Operational in November 2009)

SDD scheme is a business-to-business plan used to pay bills. In these transactions, entities must submit the payments one business day before they are due.

SEPA Direct Debit Core Scheme (Operational in November 2009)

Such transactions were used for paying bills online in the SEPA Zone. In these transactions, no card payment is involved; it’s the process of sending money from one bank to another bank in Europe.

SEPA Instant Credit Transfer Scheme (Operational in November 2017)

The SEPA instant credit transfer scheme made real-time payments from banks to vendors, retailers, or virtual sellers. Such transactions are mostly done from cell phones and internet-based e-commerce deposits.

SEPA Instant Payments | Key Takeaways for Banks

Deadlines for the first SEPA Instant Payments Regulations have been passed, and all EU banks are now required to process SEPA instant payments.

However, they can extend with permission. As the next deadline approaches, reflecting on the lessons learned is important, and preparing for what’s ahead is important.

Here are the key takeaways from SEPA banking:

Embrace the 10-Second Rule

SEPA Instant requires payments to be processed within 10 seconds, which means daily customer screening for EU sanctions lists is crucial.

This shift reduces transaction screening but can lead to increased rejections if not properly managed. Accept that some rejections are built into the system and focus on minimizing customer impact.

Review Your Compliance Process

A high number of rejected payments often indicates false positives. Therefore, review your sanctions regularly while utilizing AI technology to minimize false alerts. It also streamlines compliance processes.

Enhanced Fraud Prevention

Name-checking services are now required to ensure that the account holder’s name matches the payment information before transferring cash thus lowering the risk of SEPA fraud.

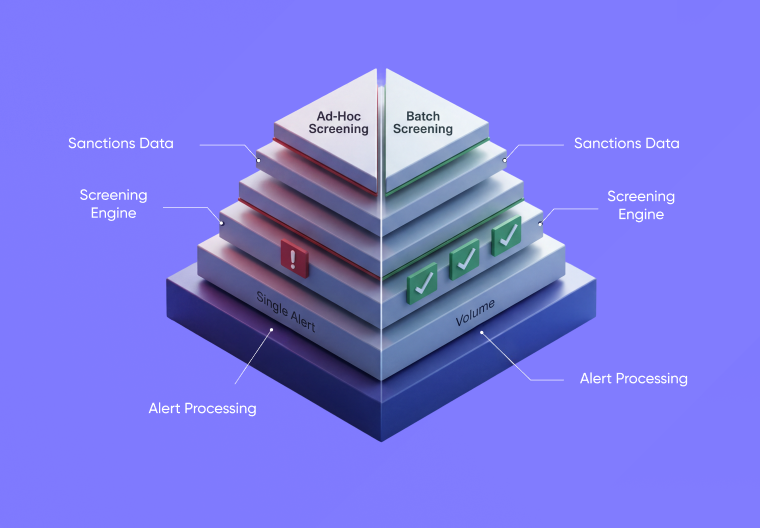

Optimized Sanctions Screening

PSPs may now conduct sanctions screening regularly, rather than for each transaction, balancing regulatory compliance with efficiency.

-

Prepare for Larger Transactions

With the €100,000 transaction cap currently in place, there’s a growing demand for higher-value SEPA Instant payments. Ensure your bank has bilateral agreements for transactions exceeding this limit to avoid missed opportunities.

-

Stay Ready 24/7

Payments after hours have exceeded expectations, which highlights the need for payment systems to handle the demand at any time. The flexible 24/7 systems are critical to meet client needs.

Explore the Top 5 Benefits SEPA Payments

Single Euro Payment Area provides the financial sectors with numerous perks, some of them are:

- SEPA regulation ensures quick transaction management and ensures real-time payments. All Single Euro Payment Area transactions are done within one business day.

- Single Euro Payment Area is a great initiative for providing convenience and streamlining payments across all European countries.

- SEPA cuts down the additional fee and comes with clear pricing, making it easier for the users to understand.

- SEPA maintains standardization in payment forms and procedures, resulting in faster, error-free transactions and shorter processing times.

- Enhanced security measures are essential for a SEPA payment. These can be readily implemented by storing AML in EU payment service providers.

- This financial initiative offers entities lower fees than conventional cross-border payments, resulting in high-cost efficiency.

SEPA payments offer all the above-mentioned benefits, but the question of verifying the clients in real-time remains still unclear.

Therefore, businesses must take shelter under the capabilities of advanced sanction screening solutions to get answers to that question.

Struggling to find reliable vendors offering sanction screening solutions that comply with SEPA payment regulations?

Look no further – AML Watcher has you covered.

How?

Get Instantly Screened Clients in SEPA Payments with AML Watcher

SEPA provides instant payment transfers, but who will promise entities, organizations, and countries with non-sanctioned clients?

AML Watcher offers credible AML screening solutions to ensure that banks comply with SEPA requirements, especially in the context of immediate transactions and SEPA Cross border payments.

It offers:

Global Database Coverage for SEPA Compliance

AML Watcher provides access to a wide range of global AML databases, including more than 3500 AML watchlists, 250 plus sanctions regimes, 2.6m Politically Exposed Persons data, and 50,000 plus adverse media domains assisting banks in meeting SEPA’s obligation to screen high-risk individuals for any applicable international financial restrictive measures.

Sanctions Screening for SEPA Instant Payments

AML Watcher checks customers against more than 250 sanction regimes like EU sanctions lists and other international standards, ensuring compliance with SEPA’s daily sanctions checks and preventing restricted payments from being completed.

Efficient Compliance for SEPA Banking

AML Watcher simplifies the AML screening process, allowing banks to maintain SEPA compliance without sacrificing transaction speed, which is critical for SEPA Instant Payments.

Enhanced Due Diligence (EDD)

AML Watcher facilitates the enhanced due diligence process by allowing institutions to flag high-risk customers and transactions, which is critical for remaining compliant with SEPA’s larger regulatory environment.

Name Matching Accuracy

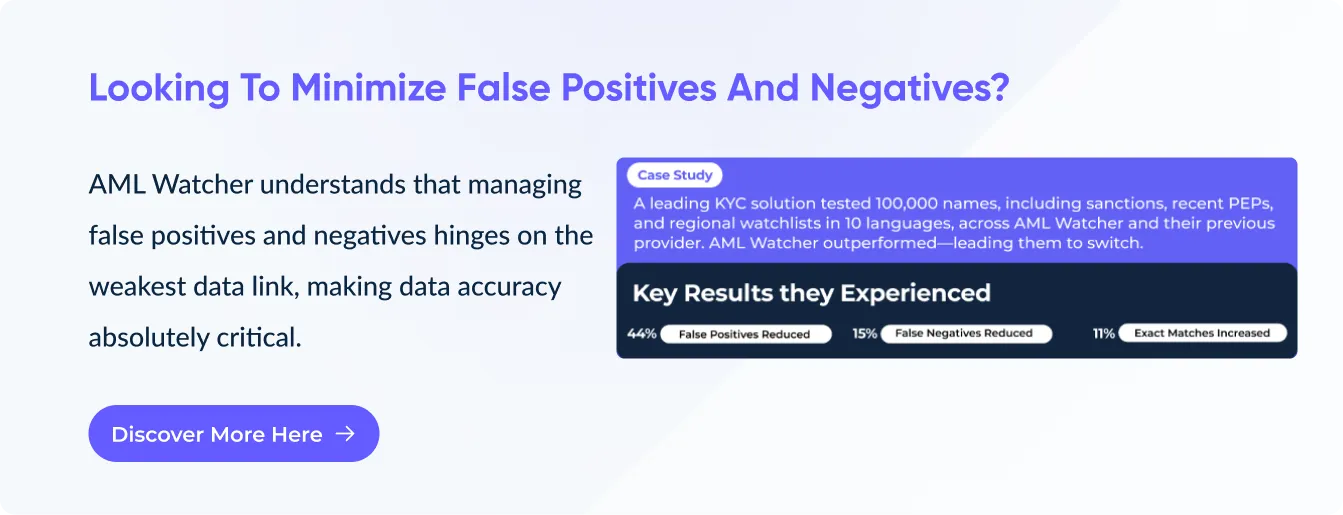

AML Watcher’s advanced name-matching approach provides high accuracy by cross-referencing several global sanction lists and watchlists, decreasing false positives and flagging only actual threats, resulting in quicker and more reliable transaction processing.

Detailed Risk Assessment

AML Watcher allows institutions to conduct thorough risk assessments by screening transactions and customers against global sanctions lists, identifying high-risk entities for further investigation while maintaining the speed and efficiency required for SEPA Instant Payments.

Scalable Solutions for Increasing SEPA Demands

As the amount of SEPA Instant Payments grows, AML Watcher’s scalable solution ensures that institutions can manage more transactions while maintaining seamless and efficient compliance operations.

Frequently Asked Questions

How can Payment Service Providers Screen Customers

against EU Restrictive Measures in Seconds?

What is the Difference Between Swift and SEPA?

- No commitment needed

- Complete AML Database at your service

- Access our all-in-one dashboard

Tier-2 PSPs in ... must demonstrate automated monitoring, layered CDD, &...

See the Full Regulatory Expectation70–80% less manual work, 95% less fatigue, TruRisk Agent makes compliance effortless.

Experience Agentic AMLMove Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries