Transaction Screening vs Transaction Monitoring: A Quick AML Guide

Transaction Monitoring

January 24, 2025

- What is Transaction Screening?

- What is Transaction Monitoring?

- Transaction Screening vs Transaction Monitoring

- FATF Standards: The Basis for Monitoring and Screening

- What Happens When Transaction Monitoring Systems Fail?”

- What Qualities Should a Transaction Monitoring Solution Have?

- Streamlining Transaction Monitoring & Screening with AML Watcher

On 15 January 2025, Block Inc., a renowned Cash App, agreed to pay an $80 million settlement for BSA/AML violations from 2018 to 2021.

Fines will be paid to “a coalition of 48 state financial regulators,” and an independent consultant will be hired to supervise its compliance with the BSA (Bank Secrecy Act) and its AML program.

The Block will also submit a report about its AML deficiencies to the authorities.

What could be the potential reasons behind this fine?

BSA/AML regulations require financial institutions to confirm the identity of their clients, report any suspicious behavior, and implement controls for high-risk accounts. State regulators found Block non-compliant, possibly allowing for money laundering, financing of terrorism, or other illegal actions.

This case highlights the significance of customer due diligence, detailed transaction screening, and regular transaction monitoring.

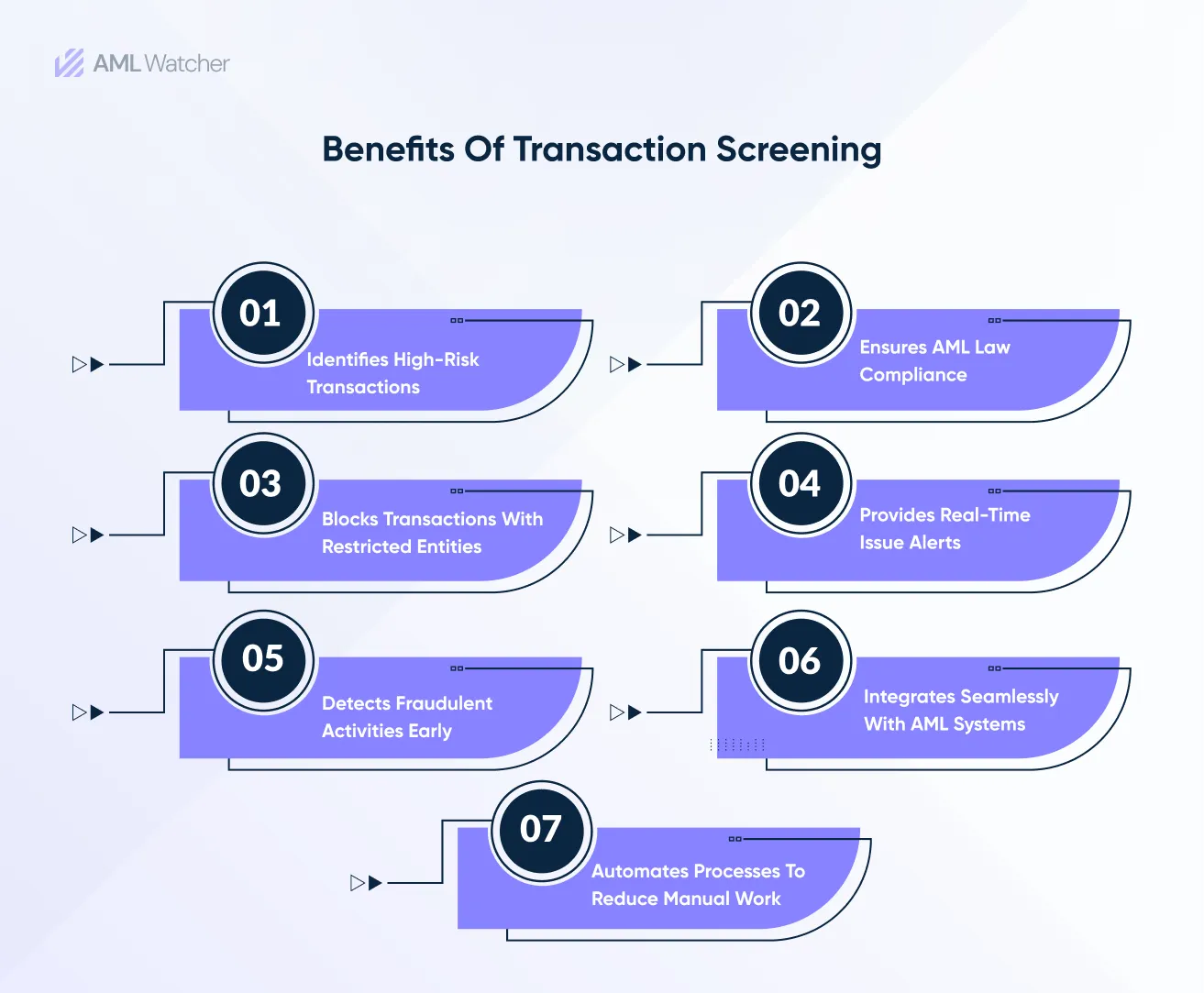

Transaction screening and monitoring are essential for preventing illicit activities such as money laundering, terrorist financing, and financial fraud.

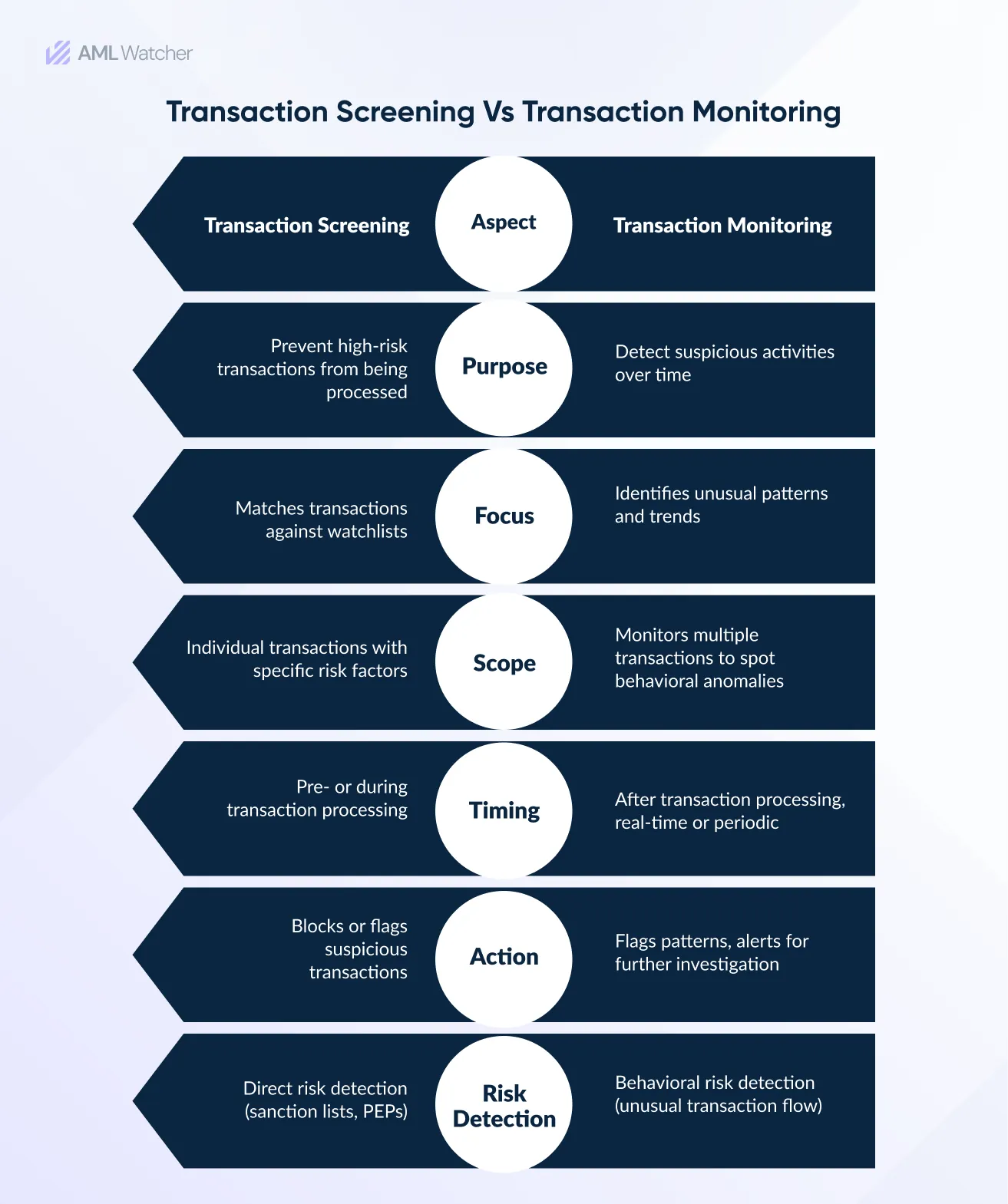

Although both have different purposes, they work together to establish robust AML compliance in the organization.

Transaction screening involves screening the transaction before it starts to evaluate the risks involved. It determines whether a transaction is approved or rejected.

Businesses can identify odd or suspicious transactions and stop financial crimes by monitoring the current transactions. It protects your company from hefty fines and reputational damage.

Governments are highly motivated to stop money laundering, which results in a global strategy of stringent AML laws.

For instance, in order to reduce the risk of money laundering and other crimes, the Financial Action Task Force (FATF) has released a series of 40 recommendations pushing countries to implement measures including screening and monitoring.

To protect your business from record-breaking fines, you must learn and understand the significance of transaction monitoring and screening and implement them effectively.

Let’s read this article for this.

What is Transaction Screening?

Transaction screening is a key element of the customer due diligence (CDD) procedure conducted in financial organizations and DNFBPs to prevent illicit activities such as money laundering, terrorist financing, and fraud.

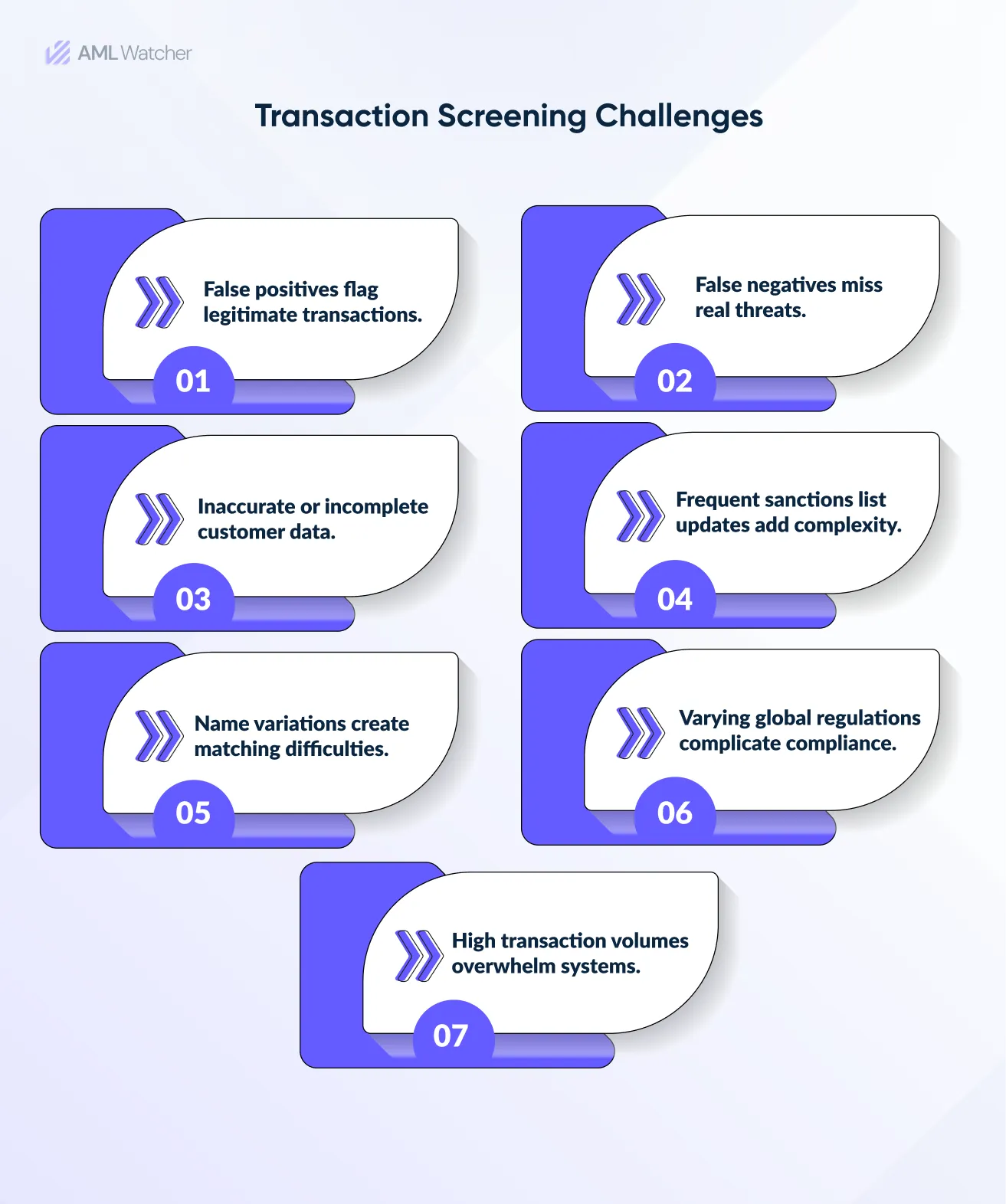

Transaction screening in AML assists in identifying and blocking high-risk transactions by checking them against PEP lists, sanctions lists, and other AML Watchlists.

It ensures compliance with AML/CFT regulations and protects the firm from financial and reputational risks.

When confirmed, the transaction is free from suspicious activities or red flags, such as money laundering, terrorist financing, weapons proliferation, sanction evasion, and fraud.

Core Features of the Transaction Screening Solution

An effective AML Transaction screening solution should have data related to internal and external risk insights to comply with legal requirements and the company’s enterprise-wide risk assessment (EWRA).

The main features are:

- Thorough checks should be conducted before transactions are approved to detect and mitigate potential risks at the start of the process.

- Identify the sanctioned entities, individuals, high-risk locations, and activities. Relay on the latest sanctions lists that are continuously refreshed after any regulatory updates.

- It should alert about updates in AML watchlists, sanctions lists, and PEP lists to ensure that the client whose transaction is being processed is not present in these lists.

- Integrate seamlessly into the company’s past risk data, use internal and external risk data to assess risks, and ensure its compliance with regulations to mitigate risks effectively.

- It should be able to understand risk analysis to experts clearly, assist them in evaluating risk alerts, and analyze the flagged activities.

By now, you must have a clear understanding of transaction screening. Let’s move forward and dive deeper into transaction monitoring.

What is Transaction Monitoring?

Transaction monitoring is a continuous process of monitoring completed transactions to evaluate the risks.

All incoming and outgoing transactions are monitored to assess the associated risks of illicit activities “such as money laundering, terrorist financing, and fraud.”

Transactions are also monitored to prevent dealing with sanctioned people/countries/entities. AML Transaction monitoring detects deviations from the company’s regular pattern or pre-defined threshold.

The list covers money services companies (MSBs), payment service providers (PSPs), virtual asset service providers (VASPs), and digital banks in addition to the obvious, such as banks and financial institutions.

Good AML software shows all alerts and other key information, such as client’s background checks and risk assessment data. It allows analysts to understand and mitigate risks quickly.

AML transaction monitoring rules are established to detect and prevent suspicious activities by assessing client transactions.

Transactions are evaluated based on various risk factors defined under varying AML regulations.

Core Features of Transaction Monitoring Solution

An effective AML transaction monitoring solution should

- Real-time tracking and flagging of suspicious transactions allow for prompt action.

- Recognize any odd trends that could point to fraudulent activities.

- Report transactions involving high-risk activity to compliance staff.

- Continue to abide by most AML/CFT laws to avoid fines and reputational damage.

- Adjust monitoring procedures to the business’s size and complexity.

- Use innovative data analytics to increase accuracy and decrease false positives.

- Adapt monitoring practices to the unique risk profile of the company.

- Make sure the company’s present IT infrastructure integrates seamlessly.

- Produce reports for internal audits and regulatory compliance automatically.

- Sort customers and transactions into groups according to their risk tolerance.

- Respect global laws and uphold robust data security measures.

Curious about transaction monitoring vs. transaction screening? Discover how these two essential AML tools work together to protect your business from financial crimes.

Transaction Screening vs Transaction Monitoring

What’s the difference between catching a red flag today and spotting hidden patterns tomorrow?

Understanding the similarities and differences between transaction screening and monitoring is important to protect organizations from financial crimes.

FATF Standards: The Basis for Monitoring and Screening

FATF recommendations are linked with transaction monitoring and transaction screening.

Recommendation 6

FATF Recommendation 6, “Targeted Financial Sanctions Related to Terrorism and Terrorist Financing,” mandates that firms screen transactions against all sanctions lists to prevent sending or receiving money from entities or individuals on those lists.

If a transaction involves such individuals or entities, the company must block all transactions to combat illicit activities such as terrorist financing and money laundering.

Recommendation 7

Recommendation 7 states, “Targeted Financial Sanctions Related to Proliferation.” Companies must screen transactions to ensure they don’t entertain the individuals who are sanctioned being involved in the proliferation of weapons of mass destruction.

Recommendations 10 and 20

Recommendation 10, which is related to Customer Due Diligence (CDD), states that at the start of a customer onboarding or conducting occasional transactions, if a financial organization suspects that transactions are linked with illicit activities, then the firm should identify and verify the client’s identity, which is part of transaction screening.

If, after establishing the client relationship, they detect suspicious transactions and submit suspicious activity reports to FIU as per Recommendation 20, it comes under transaction monitoring.

Recommendation 12

FATF recommendation 12 mandates financial institutions detect the client’s status as politically exposed persons before payouts. If higher risks are detected in their profile, they must alert senior authorities and review the policyholder relationship.

They must also submit a suspicious activity report (SAR). It comes under transaction monitoring, as risks are identified and flagged at payout to prevent the misuse of funds in illicit activities.

Recommendation 31

It is stated as “the Powers of Law Enforcement and Investigative Authorities.”. It allows law enforcement bodies to retrieve data from transaction monitoring systems during investigations.

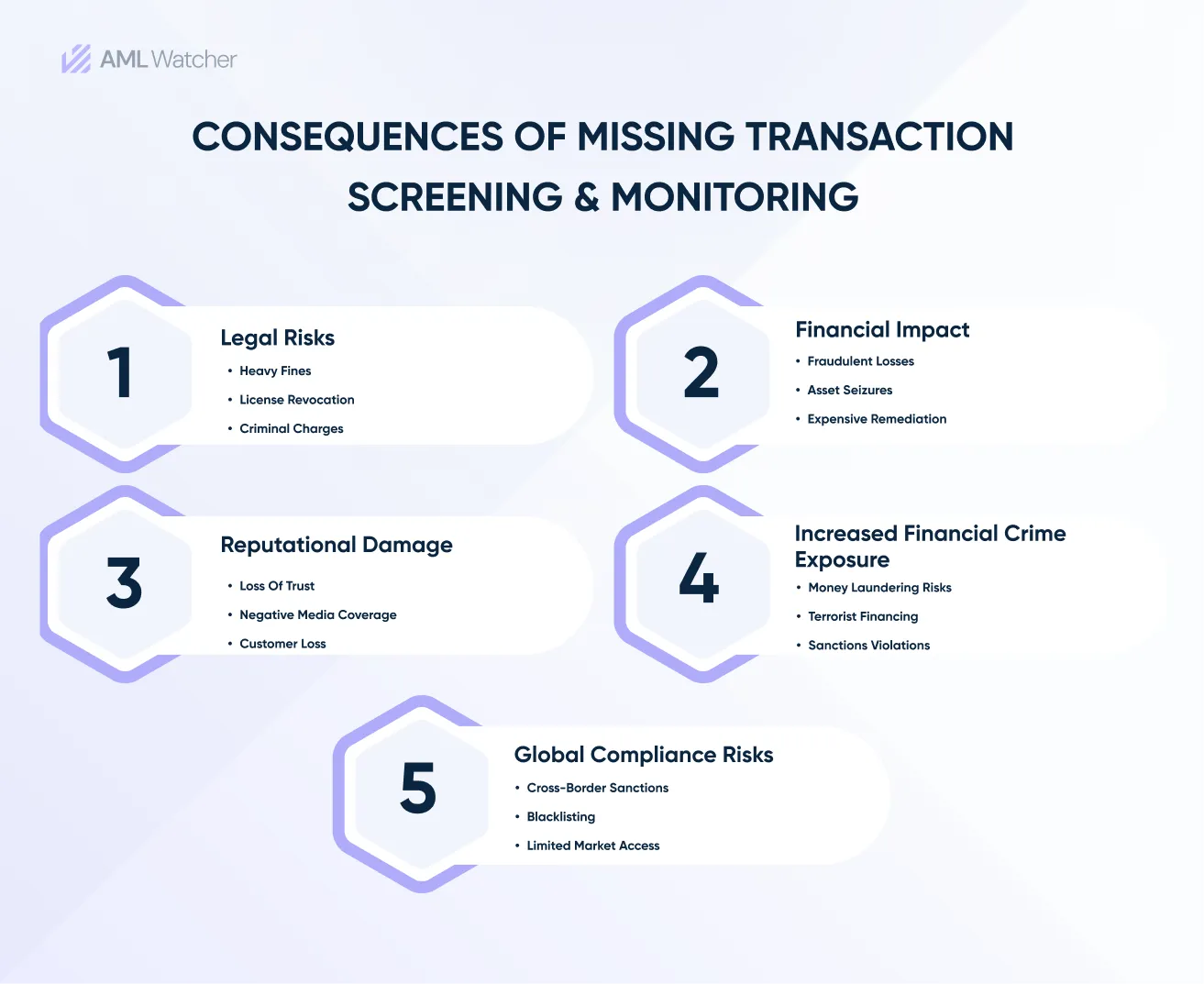

What Happens When Transaction Monitoring Systems Fail?”

Several financial institutions have been subject to severe fines for their failure to put in place suitable transaction screening and monitoring systems.

Some noteworthy examples are as follows:

Bank Metro Scandal – 2024

The Financial Conduct Authority (FCA) in the UK imposed a fine of £16 million.

Problem

From 2016 to 2020, 60 million transactions totaling £51 billion could not be tracked.

Cause

Despite internal warnings, automated systems with flaws were unable to identify high-risk transactions.

Impact

Regulatory action was taken due to inadequate monitoring methods.

Starling Bank Case- 2024

The FCA fined the company £29 million for failing to implement proper financial crime controls.

Problem

Inadequate transaction monitoring system that failed to check clients against various sanctions lists.

Cause

During 2021–2023, 54,000 accounts were established for high-risk clients without enough checks.

Impact

Potential risk of money laundering and financing terrorism.

What Qualities Should a Transaction Monitoring Solution Have?

In addition to smoothly tracking and monitoring previous transactions, ideally in real-time—an efficient transaction monitoring system should also integrate other risk data, such as transaction screening or data from prior investigations.

A strong transaction monitoring system helps analysts in evaluating risks and providing important answers:

- Is the customer starting a transaction with a high-risk recipient, such as someone on a watchlist, sanctions list, or politically exposed persons (PEPs) list?

- Does the transaction exceed the amount required for record-keeping (e.g., the US payment order threshold of $3,000-$10,000)?

- What is the source of the transaction? Do regulatory organizations like FATF see either of the locations as high-risk?

- Has the consumer’s spending grown dramatically in the last hour or less?

- Is the client engaging in a pattern of transactions below the reporting threshold, which is referred to as money laundering, smurfing or structuring?

However, when compliance professionals can evaluate warnings within other important components of the risk management system, they can handle them more skillfully.

This comprises Know Your Customer (KYC), collected transaction screening information, and corporate data related to the anti-money laundering (AML) data.

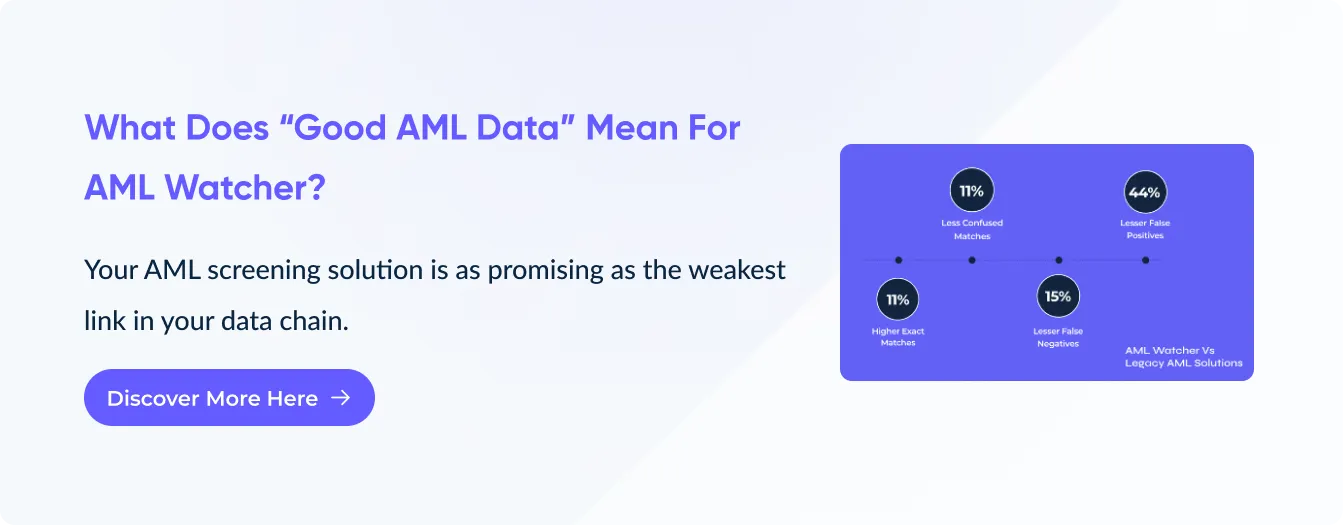

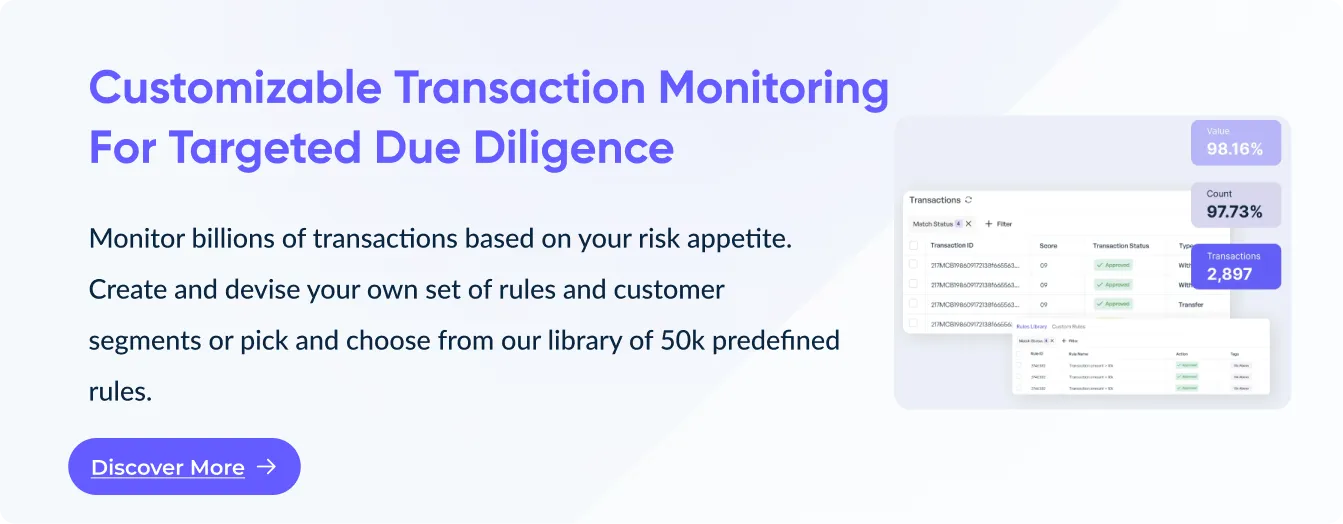

Let’s explore one of the best Transaction Monitoring solutions that offers customized evaluation with a library of 50k predefined rules.

Streamlining Transaction Monitoring & Screening with AML Watcher

AML Watcher assists organizations in maintaining AML compliance with its robust Transaction Screening and Monitoring solutions, by offering all-inclusive, real-time, and adaptable features.

How?

Real-Time Monitoring

AML Watcher offers ongoing transaction monitoring, ensuring that transactions are assessed in real time for any questionable trends or anomalies.

This enhances the organization’s capacity to promptly detect instances of money laundering or terrorism funding.

Global Data Coverage

AML Watcher offers thorough coverage, assisting institutions in adhering to international AML requirements by providing access to more than 100,000 data sources, such as sanctions lists, watchlists, PEP data from 235 nations, negative media, and other high-risk information.

Customizable Risk Profiles

Institutions can customize their screening procedures based on their risk appetite, to make sure that only the most pertinent transactions are marked for additional examination

Augmented Intelligence

AML Watcher’s advanced AI and machine learning algorithms increase transaction monitoring accuracy by lowering false positives and making sure that high-risk transactions are given priority.

Real-Time Screening

AML Watcher checks transactions in real-time, making sure that each transaction is instantly compared to the most recent sanctions lists, PEP lists, and high-risk businesses to assist institutions spot and detect suspicious activity before it is processed.

Tailored Alerts and Rules

Organizations may create personalized rules and alerts that correspond with their own AML specifications, ensuring that the system highlights transactions that satisfy predetermined risk criteria.

Smooth Integration

AML Watcher’s screening solution minimizes interference and improves the organization’s capacity to identify illegal behavior by integrating seamlessly with current systems.

- No commitment needed

- Complete AML Database at your service

- Access our all-in-one dashboard

Tier-2 PSPs in ... must demonstrate automated monitoring, layered CDD, &...

See the Full Regulatory Expectation70–80% less manual work, 95% less fatigue, TruRisk Agent makes compliance effortless.

Experience Agentic AMLMove Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries