A Complete Guide to Transaction Monitoring in 2026

Transaction Monitoring

May 04, 2026

October 1, 2024

- What is Transaction Monitoring?

- Why Transaction Monitoring Matters in 2026

- Regulatory Requirements for Transaction Monitoring

- How Transaction Monitoring Works

- Types of Transaction Monitoring Systems

- Key Challenges in Transaction Monitoring

- The Role of Synthetic Transaction Monitoring

- Transaction Monitoring Trends for 2026

- Strengthening Transaction Monitoring Frameworks

- Why Transaction Monitoring Is Now a Strategic Necessity

- How AML Watcher Supports Transaction Monitoring

Financial institutions process thousands of transactions every second, yet identifying which ones indicate financial crime remains a persistent challenge. Regulatory pressure continues to rise as authorities expect firms to detect suspicious behavior in real time while maintaining accuracy and auditability.

In the United States alone, financial institutions filed approximately 4.8 million Suspicious Activity Reports (SARs) in FY2025, around 12,600 reports per day, highlighting the sheer scale of monitoring required. In parallel, Europe’s SEPA Instant Credit Transfer scheme requires participating institutions to process euro payments within 10 seconds, placing additional pressure on firms to perform real-time sanctions screening and transaction monitoring before funds are cleared.

The scale of this challenge is accelerating rapidly. According to recent industry market analysis, the real-time payments market is projected to grow at a compound annual growth rate (CAGR) of 46.7% between 2024 and 2029, significantly increasing the volume and speed of transactions that financial institutions must monitor.

To address this, transaction monitoring enables firms to identify unusual activity, investigate risks, and comply with anti-money laundering obligations. However, evolving fraud techniques and increasing transaction volumes have made traditional monitoring approaches less effective.

This guide explains how transaction monitoring works, why it matters in 2026, and how financial institutions can strengthen their approach to meet regulatory expectations.

What is Transaction Monitoring?

Transaction monitoring refers to the process of reviewing, analyzing, and assessing financial transactions to identify unusual patterns that may indicate money laundering, fraud, or other illicit activities.

Financial institutions apply monitoring controls to evaluate whether customer transactions align with their known profile, expected behavior, and source of funds. When activity deviates from this baseline, alerts are generated for further investigation.

This process is a core component of anti-money laundering programs and helps firms maintain visibility into customer activity throughout the business relationship.

Why Transaction Monitoring Matters in 2026

Transaction monitoring has moved beyond a compliance requirement and has become a central function in financial crime prevention. Several factors explain its growing importance.

Rising Complexity of Financial Crime

Criminal networks use layered transactions, mule accounts, and cross-border transfers to obscure the origin of funds. These methods make it difficult for static monitoring systems to detect irregularities without advanced analysis.

Cross-border Payment Complexity

This complexity is amplified by global payment flows, where around 33% of cross-border retail payments still take more than one business day to settle, often involving multiple jurisdictions and screening requirements.

Increased Regulatory Expectations

Global regulators require continuous monitoring aligned with customer risk profiles. The Financial Action Task Force emphasizes ongoing due diligence, while jurisdictions such as the United States and the European Union mandate reporting of unusual transactions.

Failure to meet these expectations has resulted in enforcement actions where institutions faced financial penalties due to gaps in monitoring frameworks.

Growth in Digital Transactions

The expansion of digital banking, fintech platforms, and instant payments has significantly increased transaction volumes. This creates pressure on compliance teams to review more data within shorter timeframes.

Need for Real-Time Detection

Delayed detection increases exposure to fraud and regulatory breaches. Real-time monitoring allows firms to respond to unusual activity before it escalates into larger financial or reputational damage.

Regulatory Requirements for Transaction Monitoring

Regulatory frameworks across jurisdictions require financial institutions to perform ongoing transaction monitoring, ensuring that customer activity is continuously assessed and that suspicious behavior is identified and reported within defined regulatory timelines.

United States

The Bank Secrecy Act requires financial institutions to maintain transaction records, perform due diligence, and report suspicious activity through SARs to FinCEN, making ongoing monitoring a fundamental AML program requirement.

European Union

The 5th and 6th AML Directives require continuous transaction monitoring and reporting to Financial Intelligence Units, while emphasizing risk-based controls, transparency in beneficial ownership, and stronger enforcement across member states.

United Kingdom

Under the Money Laundering Regulations 2017, firms must conduct ongoing monitoring aligned with customer risk profiles, while the FCA expects effective systems to detect, assess, and report suspicious financial activity.

Singapore

The Monetary Authority of Singapore requires institutions to implement ongoing monitoring within AML and CFT frameworks, ensuring transactions are consistent with customer profiles and capable of identifying unusual or higher-risk behavior.

United Arab Emirates

The UAE Central Bank mandates continuous monitoring under AML and CFT regulations, requiring institutions to detect unusual transaction patterns and report suspicious activity to the Financial Intelligence Unit without delay.

Hong Kong

The Hong Kong Monetary Authority requires ongoing transaction monitoring, ensuring institutions assess transaction consistency with customer profiles and identify complex, unusual, or high-risk patterns that may indicate financial crime.

Canada

Under the PCMLTFA, institutions must monitor transactions and report suspicious activity to FINTRAC, with a strong emphasis on risk-based monitoring and maintaining accurate, complete transaction records for regulatory oversight.

Australia

AUSTRAC requires reporting entities to maintain effective transaction monitoring programs that detect suspicious activity, ensure systems align with customer risk levels, and identify unusual transaction behavior for timely reporting.

Global Standards

FATF requires ongoing monitoring to ensure transactions align with customer profiles, business relationships, and sources of funds, forming the global foundation for risk-based AML compliance frameworks across jurisdictions.

These requirements highlight that transaction monitoring is not a one-time activity but an ongoing obligation throughout the customer lifecycle, regardless of jurisdiction.

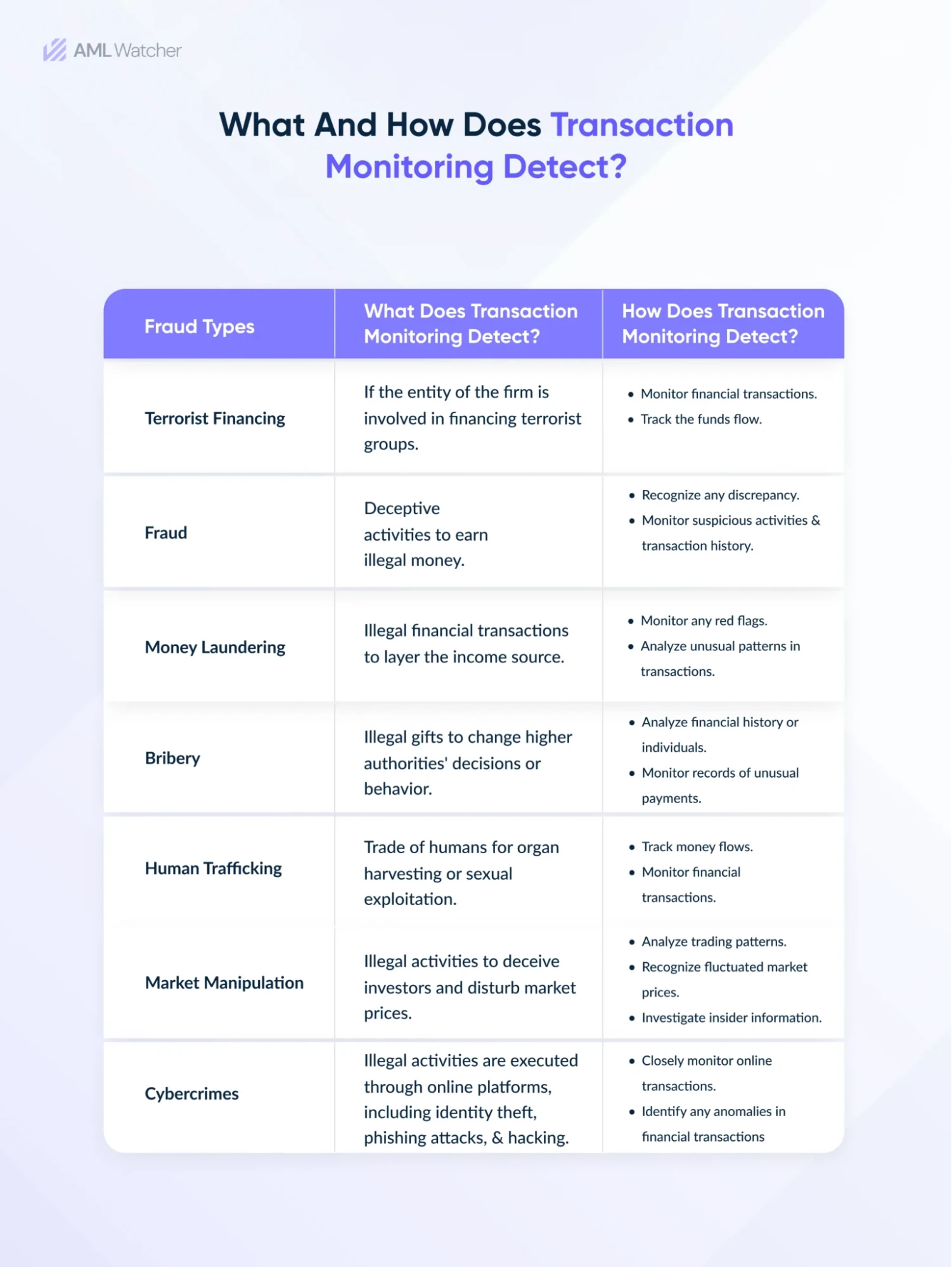

How Transaction Monitoring Works

An effective transaction monitoring framework relies on a structured process that transforms raw transaction data into actionable insights.

Data Collection

Monitoring begins by collecting transaction data from internal systems, such as payment platforms and customer accounts, as well as external data sources. This data includes transaction amounts, frequency, geographic details, and counterparties.

A comprehensive dataset enables firms to build a clear picture of customer activity.

Data Analysis

Collected data is analyzed to identify patterns and deviations. This involves structuring and validating data to remove inconsistencies and ensure accuracy.

Advanced analytics techniques help uncover hidden relationships and unusual behavior that may not be visible through manual review.

Rule-Based Evaluation

Predefined rules are applied to detect known risk indicators. These rules may include thresholds for transaction amounts, geographic risks, or transaction frequency.

When a transaction matches a rule, the system generates an alert for further review.

Alert Generation and Reporting

Alerts are prioritized by risk level. High-risk alerts require immediate investigation, while lower-risk alerts may be reviewed as part of routine compliance processes.

Reporting tools help firms document findings and meet regulatory reporting requirements.

Case Management

Compliance teams investigate alerts through case management systems that allow documentation, collaboration, and decision tracking. This ensures transparency and supports audit requirements.

Types of Transaction Monitoring Systems

Different monitoring approaches are used to address varying levels of complexity and risk.

Rule-Based Monitoring

Rule-based systems rely on predefined thresholds and scenarios to identify unusual activity. These systems are easy to implement and provide clear, logical guidance for compliance teams.

However, they may generate high volumes of alerts and struggle to detect complex or evolving patterns.

Machine Learning-Based Monitoring

Machine learning models analyze large datasets to identify patterns that evolve over time. These systems adapt to new behaviors and improve detection accuracy.

They are particularly useful in identifying previously unknown risk patterns and reducing false positives.

Statistical Monitoring

Statistical methods analyze historical data to identify deviations from expected behavior. These models assess whether changes in transaction activity are significant or within normal variation.

Behavioral Monitoring

Behavioral monitoring focuses on customer-specific patterns by analyzing historical activity. It identifies deviations from expected behavior, allowing firms to detect unusual activity with greater context.

Real-Time Monitoring

Real-time systems analyze transactions as they occur. This allows immediate identification of high-risk activity and enables firms to take prompt action.

Key Challenges in Transaction Monitoring

Despite its importance, transaction monitoring presents several operational and technical challenges.

High Volume of Alerts

Many systems generate excessive alerts, making it difficult for compliance teams to prioritize investigations. This can lead to delays and inefficiencies.

Mapping Regulatory Scenarios into Monitoring Rules

Translating regulatory expectations into practical monitoring scenarios remains challenging. Firms must continuously update rules to reflect evolving guidance, typologies, and enforcement actions while maintaining accuracy and auditability.

False Positives

Rule-based systems often flag legitimate transactions as unusual, increasing workload and reducing operational efficiency.

Data Silos

Fragmented data across systems limits visibility and affects the accuracy of monitoring processes. Incomplete data reduces the ability to assess risk effectively.

Evolving Criminal Techniques

Financial crime methods continue to change, requiring systems to adapt quickly. Static monitoring approaches struggle to keep pace with these developments.

Cross-Border Complexity

Transactions involving multiple jurisdictions require firms to comply with different regulatory standards, adding complexity to monitoring processes.

This inefficiency comes at a high cost, with U.S. banks spending an estimated $25 billion annually on AML compliance, much of it dedicated to alert investigation and manual review.

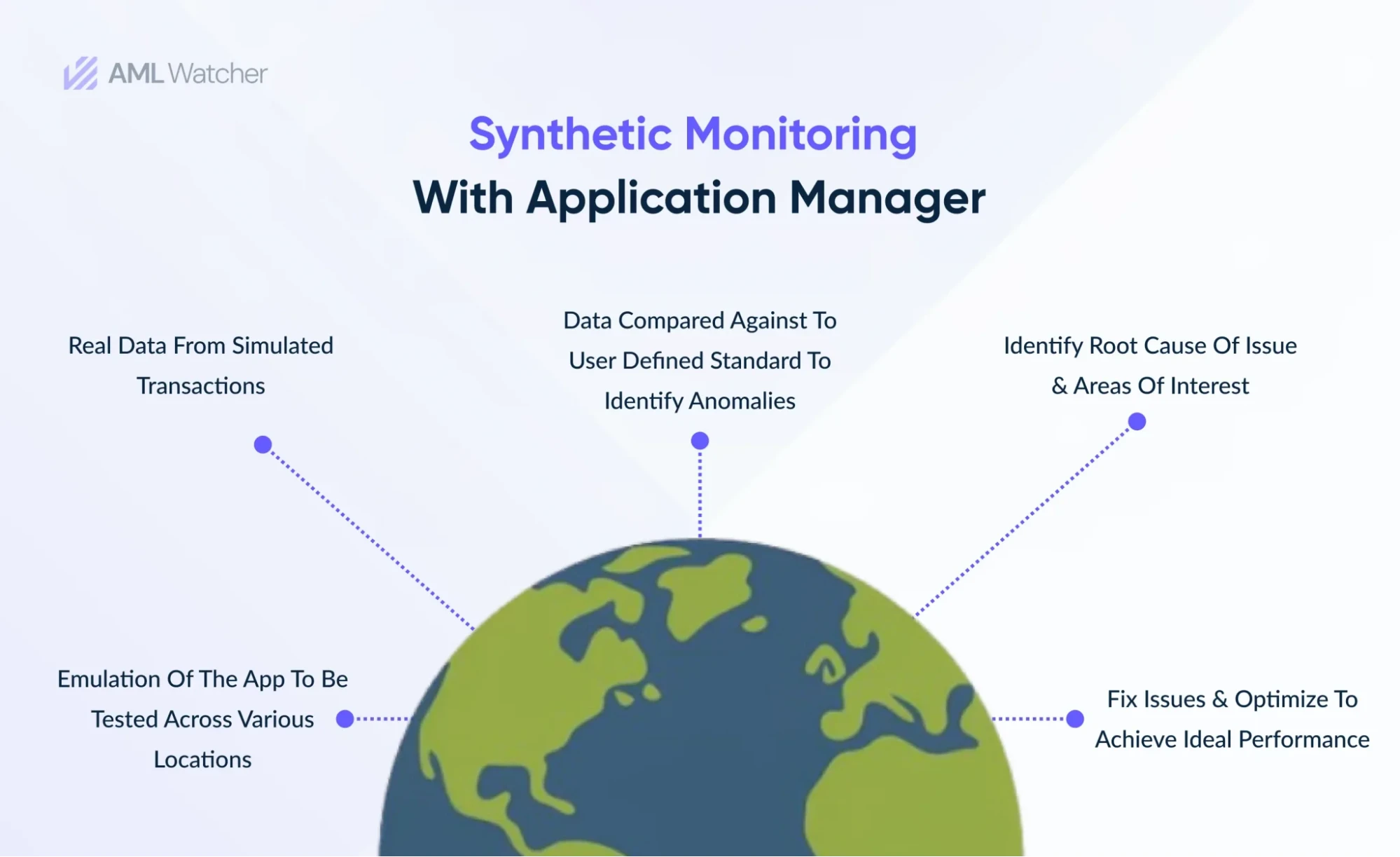

The Role of Synthetic Transaction Monitoring

Synthetic transaction monitoring involves simulating transactions to test the performance and reliability of monitoring systems.

These simulated transactions replicate real user behavior under controlled conditions, allowing firms to evaluate how their systems respond to different scenarios.

Why Synthetic Monitoring is Relevant

Financial institutions depend on digital systems to process transactions. Any disruption or weakness in these systems can affect monitoring capabilities.

Synthetic monitoring helps firms:

- Identify system weaknesses before they impact real transactions

- Test alert generation and response mechanisms

- Evaluate system performance under different conditions

- Improve overall monitoring accuracy

This approach supports operational resilience and ensures that monitoring systems function as expected.

Transaction Monitoring Trends for 2026

Transaction monitoring continues to evolve as financial institutions adopt new technologies and respond to regulatory changes.

Shift Toward Real-Time Monitoring

Regulators expect faster detection of unusual activity. Firms are moving toward real-time systems that enable immediate response.

Integration with Customer Risk Profiles

Monitoring systems are increasingly linked with customer due diligence processes. This allows better alignment between transaction activity and customer risk levels.

Adoption of Artificial Intelligence

AI-driven monitoring enhances detection capabilities by analyzing complex datasets and identifying hidden patterns. It also helps reduce false positives.

Focus on Data Quality

Accurate data has become essential for effective monitoring. Firms are investing in data management to improve the reliability of their systems. However, implementation challenges remain. Industry surveys indicate approximately 65% of institutions cite data quality and integration issues as a major barrier to effective monitoring.

Greater Regulatory Scrutiny

Authorities continue to increase oversight, requiring firms to demonstrate the effectiveness of their monitoring frameworks.

Reflecting this shift, the global AML software market continues to expand as financial institutions invest in advanced monitoring capabilities, with growing emphasis on customizable systems that adapt to evolving risks, regulatory expectations, and business models.

Strengthening Transaction Monitoring Frameworks

Financial institutions need a structured approach to improve monitoring effectiveness.

This includes:

- Aligning monitoring systems with risk-based frameworks

- Regularly updating rules and scenarios

- Incorporating advanced analytics for better detection

- Enhancing collaboration between compliance and investigation teams

- Maintaining clear audit trails and documentation

A strong framework not only supports compliance but also improves the ability to detect and prevent financial crime.

Despite these investments, only a small fraction of alerts typically indicate genuine financial crime, reinforcing the need for more precise and intelligent monitoring systems.

Why Transaction Monitoring Is Now a Strategic Necessity

Transaction monitoring has become a critical capability for financial institutions operating in an increasingly complex, fast-moving environment. As transaction volumes grow and financial crime techniques evolve, firms must move beyond static monitoring approaches toward more adaptive, data-driven frameworks. Strengthening monitoring systems is no longer just about regulatory compliance, it is essential for maintaining operational resilience and protecting the financial system from emerging risks.

Common Transaction Monitoring Red Flags”

- Structuring/Smurfing

- Rapid movement of funds

- Dormant account activity

- High-risk jurisdictions

How AML Watcher Supports Transaction Monitoring

Financial institutions often struggle with rigid monitoring systems that fail to adapt to evolving risks and regulatory expectations. AML Watcher addresses this challenge by offering a highly customizable, no-code environment that enables firms to design and refine transaction-monitoring rules tailored to their specific risk appetite and compliance requirements.

Its platform integrates multiple data sources to enhance risk visibility while enabling compliance teams to configure scenarios, thresholds, and workflows without heavy technical dependency. This level of flexibility allows institutions to operate with the control and adaptability of an in-house system while maintaining efficiency, accuracy, and regulatory alignment.

- No commitment needed

- Complete AML Database at your service

- Access our all-in-one dashboard

Tier-2 PSPs in ... must demonstrate automated monitoring, layered CDD, &...

See the Full Regulatory Expectation70–80% less manual work, 95% less fatigue, TruRisk Agent makes compliance effortless.

Experience Agentic AMLMove Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries