What is KYC in Banking?

Others

July 30, 2025

Ever wonder how financial firms make sure that the millions of transactions they carry out each day are safe and free from any illicit origins?

From facilitating investments, granting loans to transferring funds all across the world, banks end up carrying out millions of transactions every given second.

Banks find themselves compelled to protect the legitimate financial systems and prevent millions of dollars in regulatory fines in an attempt to reduce the risks of increasingly prevalent financial crimes such as money laundering, terrorist financing, corporate frauds, embezzlement, human trafficking, drug trafficking, corruption, and bribery.

This is the point at which Know Your Customer, or KYC in banking becomes relevant.

Banks are required to follow a legal practice known as ‘Know Your Customer’ which is meant to minimize legal issues associated with serving high-risk customers

KYC banking is the most important regulation to make sure that financial institutions do not conduct business with people who have a criminal record.

It involves gathering and verifying specific information about a potential customer before onboarding, such as their identity cards, formal name, addresses, and source of income.

This verification procedure identifies and verifies the customer’s identification, and makes certain that they are who they say they are.

The banking industry spends an average of $48 million annually on KYC compliance.

KYC is the founding compliance framework of financial compliance. Its importance cannot be exaggerated. In today’s financial world, no bank can survive without complying with the KYC regulations. It is often regarded as banks’ supreme barricade against financial crimes.

This one regulatory system makes sure that banks can operate securely and safely in this kaleidoscopic financial world. And finally, it boosts business trust between banks and their consumers.

How Has the Practice of KYC in Banking Improved Over Time?

KYC protocol implementation, like any other regulatory practice that emerged in the late twentieth century, dates back to the 1970s.

With the rise of modern banking and the increased risk of financial crimes such as drug trafficking, money laundering, corruption, fraud, bribery, and corruption, banks were pushed to take action, resulting in the Bank Secrecy Act in the United States.

This rule requires the banking industry to report suspicious activities to the regulatory authorities and retain detailed records of client transactions.

Establishment of the Financial Action Task Force (FATF) in 1989 was a turning point for the financial world.

For the first time in history, its establishment introduced international standards for anti-money laundering (AML). It later included countering-terrorist financing among its key focuses.

Following 9/11, KYC banking evolved to include countering terrorist financing, thanks to legislation such as the USA PATRIOT Act.

What are the pillars of Compliance in AML (Anti Money Laundering) Programs?

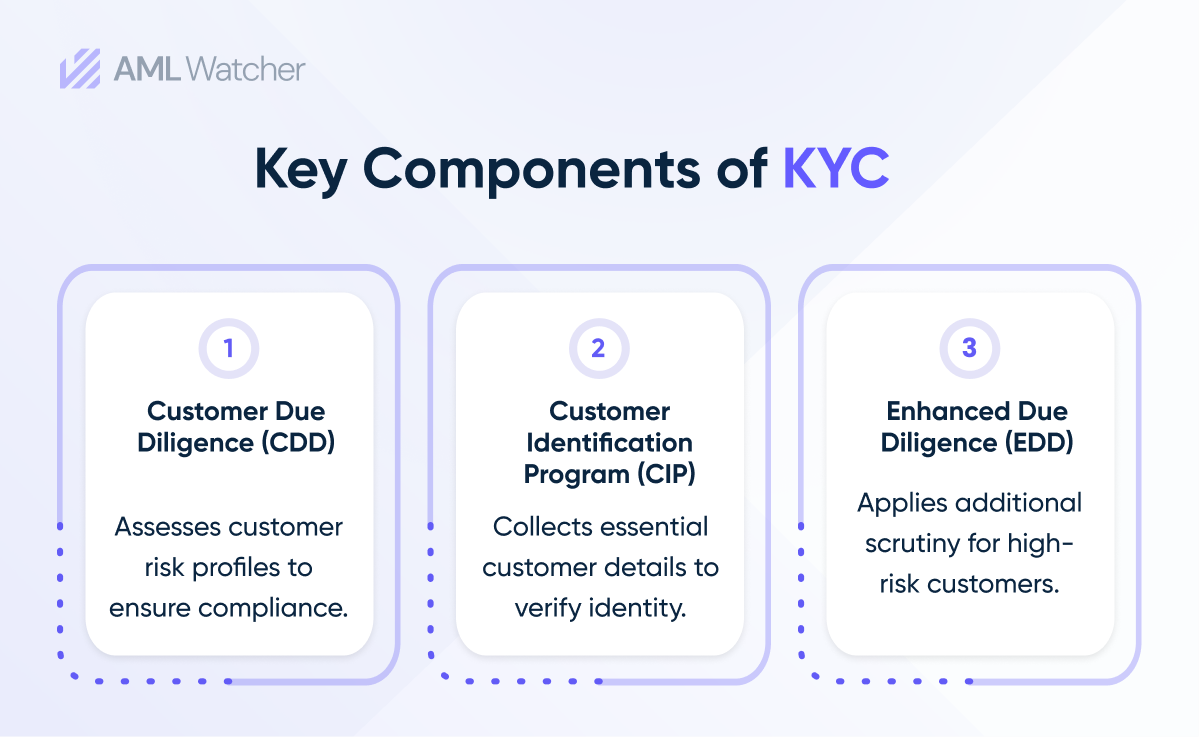

Elements of KYC

Know Your Customer (KYC) framework has three elements practiced all around the banking industry. These key components includes:

- Customer Identification Program (CIP)

- Customer Due Diligence (CDD)

- Enhanced Due Diligence (EDD)

Each of these components has its own dynamic role in detecting risky clients, illicit gains and helps firms avoid millions of dollars in regulatory fines.

Customer Identification Program (CIP)

The very foundation of KYC banking is the Customer Identification Program and its the main protocol that helps financial institutions verify the essential details of a customer like their mailing address, name, permanent address, official identity card.

This protocol helps institutions build trust that they are dealing with a legitimate individual or entity.

Customer Due Diligence (CDD)

After carrying out the above foundational step comes customer due diligence which conducts a deeper identification of the potential customer and evaluates their risk profile.

For the the following factors comes onto account:

- Customer’s source of income

- Their geographic location

These factors help financial firms analyze the potential risks associated with conducting business with a potential client.

Enhanced Due Diligence (EDD

For individuals or entities flagged as high-risk, Enhanced Due Diligence (EDD) kicks in.

This advanced layer of scrutiny involves rigorous checks, such as verifying the purpose of the account, conducting background investigations, and monitoring transactions.

EDD is especially designed for high risk politically exposed persons (PEPs) or entities operating in high-risk regions, which acts as a tough barrier against illicit activities like money laundering and terrorist financing.

Together, these components provide protection, which helps build safer financial ecosystems across the globe.

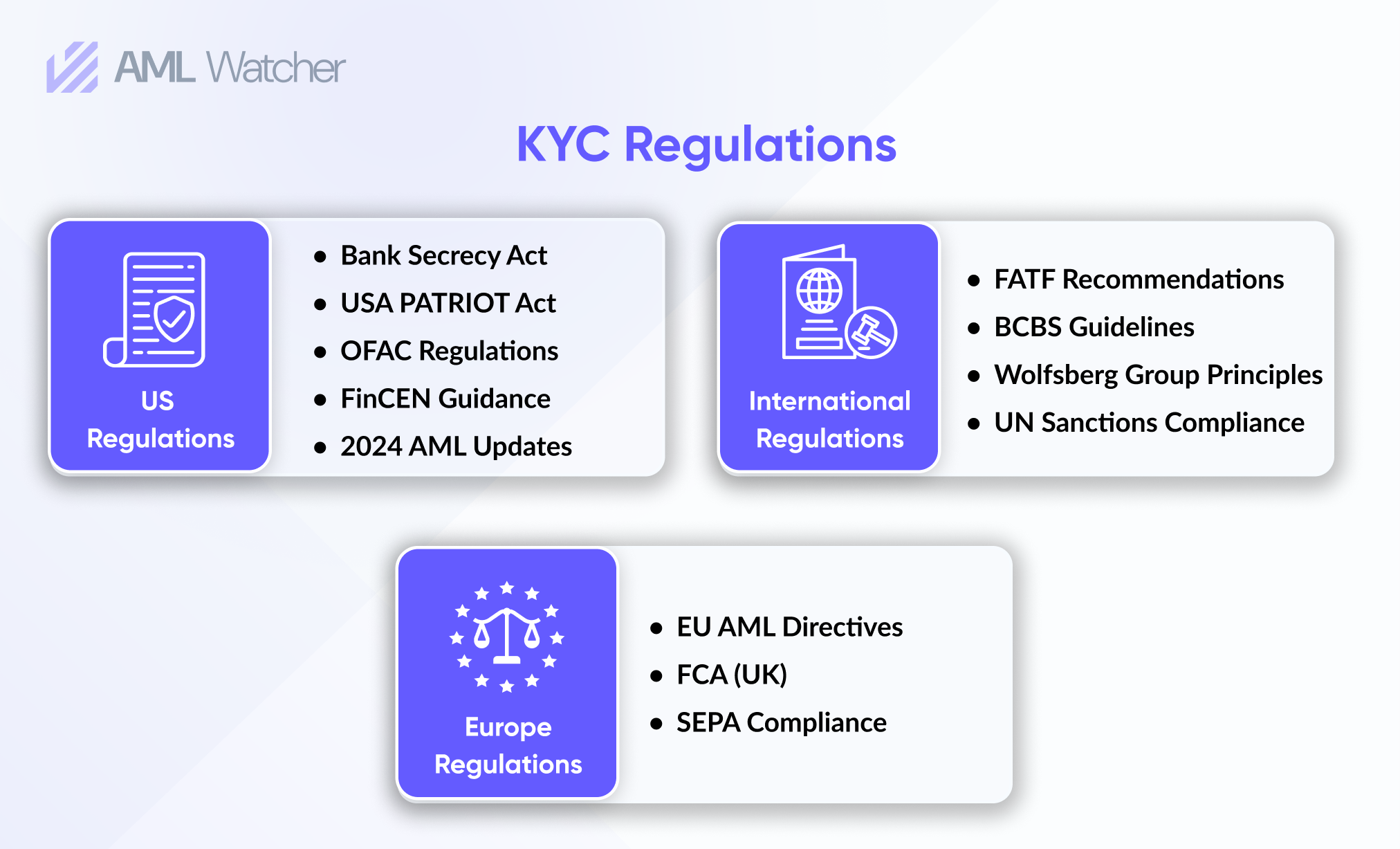

Regulations Directing KYC

Countries around the world have their own set of regulations for the implementation of KYC in the banking sector.

These KYC regulations are not uniform. They vary from country to country.

Some differences in terms of KYC laws are negligible, whereas sometimes the differences are humongous.

KYC In the United States

In the United States, as mentioned above, the Bank Secrecy Act (BSA) passed in the 1970 was the first of its kind to counter financial crimes like corporate fraud, terrorism financing, and money laundering.

The BSA created the standard framework for customer identification systems by mandating banks to verify consumers’ identities before opening accounts.

Amendments to the BSA, such as the USA Patriot Act of 2001, have further supplemented KYC banking standards by providing stronger due diligence methods for high-risk consumers and increasing reporting requirements.

Banks must verify their customer’s official name, residential address, date of birth, and identification number (or a taxpayer identification number like EIN or SSN ) before onboarding them.

Financial Crimes Enforcement Network (FinCEN), Financial Industry Regulatory Authority (FINRA) and US Securities and Exchange Commission (SEC) are responsible to oversee the enforcement of all AML/KYC regulations in the United States.

KYC In European Union

In Europe, the evolution of KYC regulations has been driven by the EU Anti-Money Laundering (AML) Directives.

Starting with the First AML Directive in 1991, these directives have been regularly updated to grapple with the evolving financial threats.

The Fourth and Fifth AML Directives upgraded KYC banking requirements by mandating stricter customer due diligence, including the verification of beneficial ownership and enhanced scrutiny of high-risk countries.

Earlier, the EU member states used to have their own set of KYC legislation.

However, after the adoption of the Anti-Money Laundering Authority (AMLA) in June 2024, all AML/CFT measures are harmonized among all the EU member states to boost coordination among all EU states.

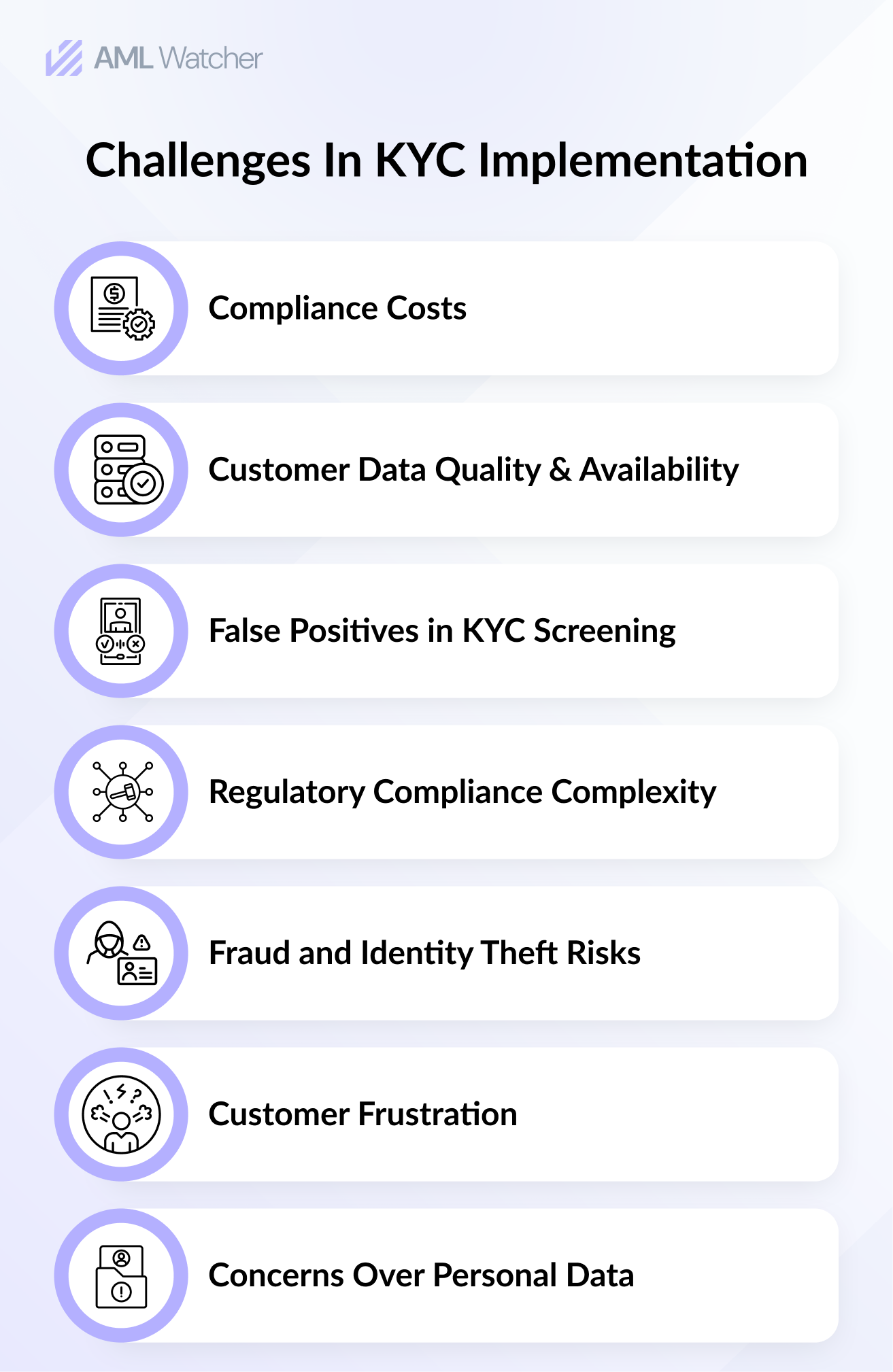

Problems Faced in KYC Implementation

As essential as Know Your Customer (KYC) processes are, implementing them comes with their own set of challenges.

Compliance Costs

The first compliance hurdle is the massive compliance cost.

Powerful KYC systems mean big investments in technology and human resources.

For giant banking organizations in big cities, handling these big costs is somewhat manageable.

However, for financial institutions operating in small or remote areas, such enormous compliance costs are quite restrictive.

Resultantly, small financial firms struggle to keep pace with complex regulatory requirements which results in a competitive disadvantage.

One example to explain it further is that integrating advanced KYC tools such as AI-driven verification systems means substantial upfront and ongoing expenditures.

This eventually makes it hard for the small players to compete with large organizations.

Customer Data Quality and Availability

For efficient KYC implementation, banks are dependent on complete and accurate data quality.

Sometimes the data is outdated (unverified address) or missing or inconsistent (misspelled names), which results in delays in manual onboarding or slow onboarding and hurts the integrity of the KYC process.

Poor data entry, customers providing partial information or a lack of digital records make KYC implementation tricky, especially when dealing with international clients or organizations that use complex corporate structures to hide UBOs.

False Positives in KYC Screening:

An inefficient KYC system typically leads to a large number of false positives that inaccurately indicate false alarms to the PEP lists, sanction lists, and adverse media.

It could flag a legitimate customer as possibly high-risk due to common names, name similarities, or outdated/irrelevant information in government or public databases.

For instance, a common name like “Lisa Robert” could get flagged 100+ times due to it being a common name.

Such false positives lead to manual investigation by MLROs and compliance teams to examine if it’s a genuine match. This diverts the resources from investing their time and attention in the genuine risks.

Sometimes, a massive number of false positives causes genuine red flags to be missed due to “alert fatigue” among analysts

Regulatory Compliance Complexity:

The anti-money laundering industry and the KYC regulations are never static. They keep on changing with the evolving financial crime landscape.

Moreover, the KYC regulations vary from country to country and region to region.

This becomes particularly tricky for banks that are operational on an international scale and functioning in other countries.

Regulations on what constitutes a “high-risk” customer, how to verify them, what information to collect about them and reporting obligations all make up a labyrinth of different rules.

Moreover, they may also have diverse interpretations. So implementing changes across multiple regulatory frameworks requires substantial legal, compliance, and IT resources.

Fraud and Identity Theft Risks:

Banks today are now grappling with identity theft attempts, which represent another rising challenge for successful KYC implementation.

Sometimes, the potential clients may use stolen credentials, deepfakes, synthetic identities, or forged documents to fool the verification systems.

Therefore, fake accounts made by fraudsters may facilitate terrorist financing, embezzlement, money laundering, and crime risks.

Resultantly, banks may suffer for paying the cost of remediating breaches and investigations for fraudulent transactions.

Banks take an average of 24 days to onboard customers, due in large part to the complexity of KYC and AML.

Concerns Over Personal Data

Implementing KYC also comes with major concerns over personal data.

Financial firms are required to collect and store sensitive customer data like their financial histories, identification cards, sources of income, etc.

This raises real privacy issues.

Even though there are regulations like the General Data Protection Regulation (GDPR) that mandate strict data protection standards.

Nevertheless, implementing these measures is costly and an uphill battle.

For banks, it’s like pulling teeth to build a delicate balance between regulatory compliance and assuring customer trust by safeguarding personal information.

Any breach in this procedure could not only lead to legal repercussions but also hurt the institution’s prestige.

Customer Frustration

KYC processes usually tend to be lengthy and complex.

This often leaves customers up in arms, particularly during the onboarding phase.

Customers expect swift and seamless banking experiences, but extensive verification procedures can feel intrusive or pointlessly time-consuming.

This is particularly an issue in terms of digital banking, where customers want speed and convenience.

To grapple with this, banks can invest in advanced solutions such as e-KYC, which streamlines identity verification without compromising on security.

A balanced approach is they key, from employing tech to reduce costs and simultaneously making sure the data privacy through strong security measures and improving customer experiences through smooth processes.

How can AML Watcher help you comply with KYC protocols?

AML Watcher offers the following key features to help you comply with KYC regulations.

Comprehensive Customer Screening: We provide you with over 3,500 global watchlists, including sanctions lists, Politically Exposed Persons (PEPs), and adverse media sources. This will help you screen out clients that are flagged by government organizations, regulatory bodies and law enforcement agencies all around the world.

Enhanced Due Diligence (EDD): For you to have a detailed awareness of a higher risk client and their financial activities, AML Watcher provides continuous monitoring and extensive risk evaluation.

Customizable Risk Scoring: We offer scalable risk assessment and industry-specific risk management. You can now risk score clients based on their transaction behaviour, industry and geography.

Contact us today to see how AML Watcher can secure your financial future!

- No commitment needed

- Complete AML Database at your service

- Access our all-in-one dashboard

Tier-2 PSPs in ... must demonstrate automated monitoring, layered CDD, &...

See the Full Regulatory Expectation70–80% less manual work, 95% less fatigue, TruRisk Agent makes compliance effortless.

Experience Agentic AMLMove Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries