How Can Banks Manage High-Risk Clients with Advanced PEP Screening Solutions?

PEP

May 2, 2024

- How Did Regulators Respond To This Situation?

- The Concept of Politically Exposed Persons

- What is a PEP Screening?

- PEP Screening and Categorization

- Managing High-Risk PEPs Under Global Regulatory Guidance

- Avoid De-Risking of Politically Exposed Customers-PEP

- Emphasize On Risk-Based Approach For PEPs

- Invest In the Latest for Effective AML PEP Compliance

- AML Watcher & Global PEP Compliance

You must be surprised to learn that former UKIP leader Nigel Farage’s bank account was closed by the private bank ‘Coutts, a subsidiary of NatWest.’

Nigel Farage claims he was blocked because he is a PEP—a Politically Exposed Person—and that his political beliefs conflict with the bank’s principles, whereas the bank maintains that a lack of funding was the reason for blocking his account.

In either case, his situation does shed light on simple and persistent banking issues that “politically exposed persons,” or “PEPs,” have to deal with.

Shortly after the Farage story, it was not just another citizen who was speaking out, but the chancellor of the exchequer Jeremy Hunt who had been turned down for an account by Monzo, an online bank.

These instances create an unpredictable and complex situation for PEPs being blocked out without any valid reason and for financial institutions to avoid dealing with potential high-risk clients.

Ever wonder how global regulatory bodies respond to these challenges and what a financial institution should do to keep onboarding such high-risk customers and stay compliant with AML laws?

How Did Regulators Respond To This Situation?

In response to complaints made by politicians from the United Kingdom, Andrew Griffith, the economic secretary to the Treasury has written a letter to the FCA where he has urged it to accelerate a proposed consultation on its guidance to banks regarding handling of PEP customers.

He also pointed out that it has become rather evident that some of the financial institutions might not be getting the proper balance between adopting a proportionate strategy based on a thorough assessment of the real risk and taking the appropriate action.

Mr. Griffith said: “The government is very determined that domestic PEPs should be managed according to the risk they pose and that banks should not be closing individuals’ accounts because that person is a ‘PEP’.

The Treasury has stressed in the past that it would be a ‘real issue’ if financial services were being denied to those who had a legal right to freedom of speech.

Under the Financial Conduct Authority (FCA) PEP regulation 2024, instructed banks to ensure that PEPs and their families are not subjected to discrimination during AML compliance checks.

The FCA review assesses how firms can define PEPs, evaluate their risk, apply extra checks, decide when to close accounts, communicate with PEPs, and update their AML controls.

Before moving forward why not find out what is the concept of PEP around the world, and how PEPs are categorized based on their various risk levels?

The Concept of Politically Exposed Persons

A “politically exposed person (PEP) is any person holding or who has held a position in a government office who is thus vulnerable to bribery, financial fraud, or corruption”.

According to the Financial Conduct Authority (FCA): “A PEP may be in a position to misuse his/her public office for private benefit and a PEP may use the financial system to facilitate money-laundering of the proceeds from this misuse of office.”

The Financial Action Task Force (FATF) defines “PEPs as those individuals who are or have been trusted with public function.”

PEPs are considered “high risk” since international lawmakers and other transparency organizations state that these individuals might be more vulnerable to bribery and other types of corruption than regular customers.

What is a PEP Screening?

Taking a PEP as a customer, financial institutions (FIs) are required to conduct detailed evaluations to assess the risks associated with them— that is through PEP screening.

As per FATF in its Recommendation 12, the FIs such as banks and other designated non-financial businesses and professions (DNBPs) under AML compliance are encouraged to employ a PEP compliance program to fight money laundering and potential financial crimes.

PEP Screening and Categorization

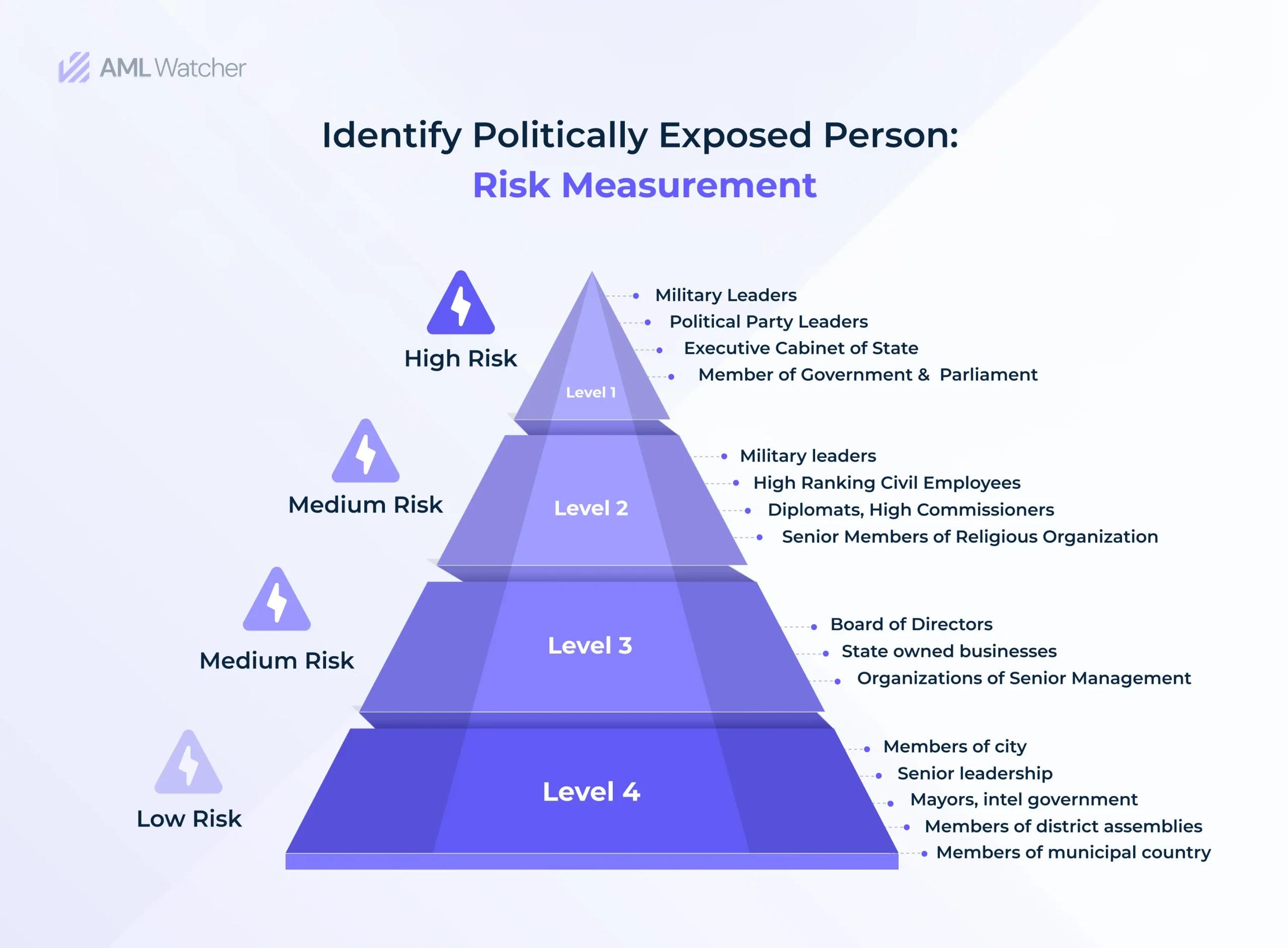

When conducting PEP screening, it is essential to pinpoint politically exposed individuals, as well as their relatives and close associates (RCAs). Additionally, it’s important to note that not all PEPs carry the same level of risk, as there are distinctions within the PEP category itself.

Categorization Based on 4 Levels of Risk

Different PEPs present different levels of AML/CFT risk. In light of this, it is possible to categorize the PEP risk levels into the following 4 risk levels:

With this PEP screening importance, one must be curious to understand how PEP client handling can be a complex issue for financial institutions, what international regulatory authorities advise and how financial institutions can resolve such issues.

Managing High-Risk PEPs Under Global Regulatory Guidance

After a detailed analysis of the Farage case and multiple other similar cases, international authorities like the FCA, FinCEN, and FATF have stressed that banks can manage high-risk PEPs without automatically excluding them.

- FATF: FATF recommendations 12 and 22 have established special measures that set the rules for improved due diligence, which enables banks to reduce the risks and at the same time, provide equality in access to banking services.

This approach complies with the regulations of various countries for example United States Bank Secrecy Act and the United Kingdom Proceeds of Crime Act.

- United States: PEP regulations under the Bank Secrecy Act (BSA) and Patriot Act require risk-based AML/CFT programs with customer due diligence (CDD) and enhanced due diligence (EDD) for high-risk PEPs. Firms must report suspicious activities to FinCEN.

- United Kingdom: FCA mandates PEP screening MLR 2017 & ATCSA 2001 similar to EU standards; ongoing review of PEP treatment by banks and financial firms, with findings expected in 2024.

- Canada: Under the Proceeds of Crime (Money Laundering) and Terrorist Financing Act (PCMLTFA), PEP screening is mandatory, with foreign PEPs always considered high-risk. The Financial Transactions and Reports Analysis Centre of Canada (FINTRAC) enforces these PEP regulations.

- European Union: Uniform PEP screening policy under AML Directives especially the 6AMLDs, following a risk-based approach aligned with FATF standards.

- Australia: The Australian Transaction Reports and Analysis Centre – AUSTRAC oversees AML/CTF compliance, requiring financial institutions to conduct PEP screening and adhere to CDD guidelines.

All these AML regulatory bodies emphasize one key point in the case of efficient PEP screening.

Guess what!

Avoid De-Risking of Politically Exposed Customers-PEP

As per the global AML regulations, cutting business ties with PEPs or refusing to deal with new ones does not reduce risk, instead, it forces these people into less regulated “shadow banking” networks, increasing monitoring challenges and decreasing transparency for financial intelligence units.

The process of de-risking everyone is a vague approach to terminate all PEPs including those who present minimal risks such as former officeholders, their families, or those with unavoidable political exposure, even when they pose minimal risk.

Rather financial institutions must focus on risk-based strategies to counter various risks associated with PEPs.

Emphasize On Risk-Based Approach For PEPs

The risk-based approach is an important component of AML/CFT compliance for financial institutions that must be proportional to the risk profile of their clients – for instance using EDD measures on high-risk customers while low-risk customers are subjected to lighter measures.

When it comes to recommendations for the PEP screening practices businesses should make sure their PEP definition is as inclusive as possible to cover all the PEP positions, relations, and affiliations owned or controlled by individuals.

Blanket de-risking does not conform to the above principle which means it relocates the risk into the less regulated regions and puts an end to policy transparency.

Now the major concern here is how financial institutions can implement a stringent risk-based approach for handling such complex situations where they are obliged to onboard PEP clients and also keep a strict monitoring on their activities for any possible suspicious act.

The simple solution is to invest in advanced technologies— an efficient AML screening solution.

Invest In the Latest for Effective AML PEP Compliance

To manage PEP screening cases, regulators like the FCA and the U.S. Treasury encourage banks to invest in innovative technologies. For instance, a Custom risk-scoring engine allows financial institutions to evaluate risk based on specific criteria such as location, transaction patterns, and customer behavior.

Banks can better prioritize high-risk clients and streamline AML compliance efforts, by assigning tailored risk scores to each profile. This ensures a more targeted and effective approach to monitoring and addressing PEP risks at all levels.

Thus, for instance, the U. S. Treasury currently instructs banks to “remain evaluating the opportunities, threats, and challenges of innovative and new technologies for AML/CFT compliance solutions. ”

Similarly, the FCA expected that advancement in technology must “enhance, accelerate and reduce the cost of AML compliance. ”

Therefore, there is a need for the right technique to conduct efficient PEP screening, that is integration of technology and a risk-based approach. This would be vital for banks to remain compliant with the latest AML regulations and deal with the rising financial crimes.

Financial institutions need to use advanced AML screening technologies, such as those offered by AML Watcher, to expedite the process of identifying and classifying PEPs.

AML Watcher & Global PEP Compliance

Combating the alarming challenges in meeting PEP compliance, AML Watcher adopts a risk-based approach, applying AML/CFT measures customized to each client’s risk level, and providing enhanced due diligence (EDD) for PEPs that pose a higher risk.

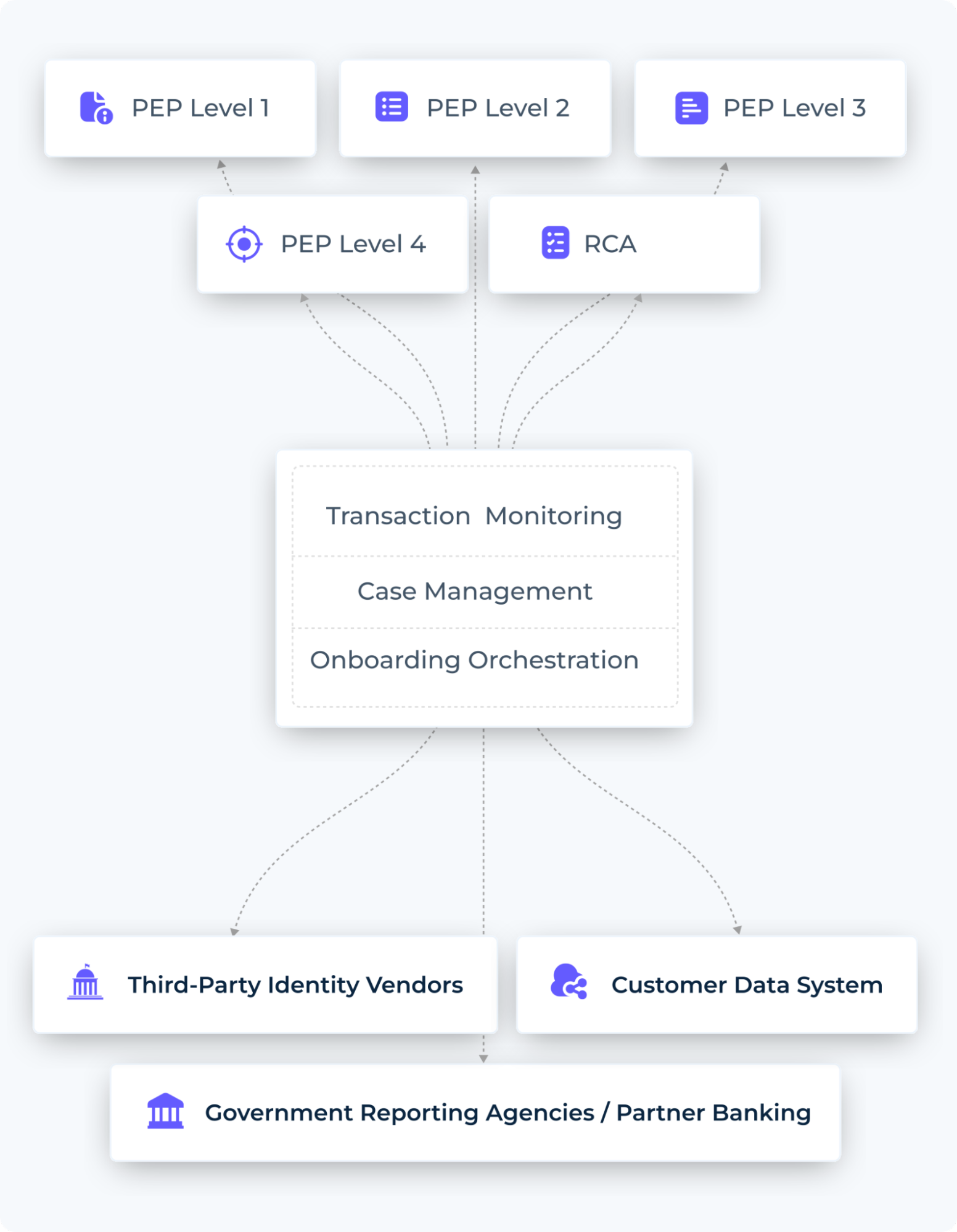

Implementing the risk-based approach recommended by FATF, AML Watcher strengthens its PEP screening software with an extensive network of PEP databases to screen individuals from more than 235 countries.

The automated database includes:

1. Broader PEP Definitions Datasets

Why take a chance on limited definitions that might fall short? Extend your reach.

AML Watcher ensures that no politically exposed individual falls between these gaps by providing a wider range of PEP data from more than 235 regions to ensure that financial institutions can assess PEP from each lesser-known to high-risk area.

Our platform removes the hassle of navigating multiple, frequently contradictory sources by providing a single, reliable dataset that covers every aspect of politically exposed individuals.

AML Watcher has unified all PEP definitions from FATF, FinCEN, FCA, Wolfsberg, and other sources into a single, unified database, making us the most comprehensive source of politically exposed persons (PEPs) data.

This unified approach ensures that you have access to the most comprehensive and up-to-date PEP data available no matter where your clients are or which jurisdiction they fall under.

Financial institutions can better manage risk and prevent blocking clients with this feature that helps them to distinguish between different kinds of PEPs as per different regions and different regulatory bodies.

2. PEP Level 1-4 Risk Assessment

Why go for partial PEP screening covering a few PEP risk levels when the risks are so high at every level and FATF mandates screening for each risk level? AML Watcher has you covered across each risk level.

AML Watcher offers detailed PEP screening coverage across all risk levels, from 1 to 4, ensuring that no political figure—regardless of their prominence or power—escapes investigation.

Although this client risk assessment at each level is mandated by FATF, many industry solution providers tend to overlook lower-risk individuals. However, AML Watcher understands the importance of PEP screening at every level where risk matters.

Our comprehensive PEP data gives you unmatched confidence that your AML compliance is flawless by closely monitoring everyone, from powerful political figures at the top to those with lower-risk individuals in less significant roles.

Our screening covers the full spectrum of PEP risk levels, ensuring thorough monitoring and reducing exposure to potential threats.

3. Always Current, Always Compliant

Is your PEP screening solution keeping up with the AML regulatory world’s pace? Ours does.

AML Watcher’s PEP Screening data is updated with the most recent global data regularly.

Our solution adapts to new laws and changing political circumstances to keep the screening procedure accurate and up to date.

Whenever there is a delisting of a sanctioned entity or the addition of an entity to the watchlist or sanction list for thorough evaluation, our system automatically updates our solution within 15 minutes.

This dynamic integration lowers the chances of AML compliance violations and allows financial institutions to take quick, well-informed actions without blocking client accounts.

AML Watcher protects your company against possible fines and reputational harm by making sure it stays compliant with the most recent regulatory standards.

4. PEP Coverage in Conflicted or Isolated Regions

Why leave any single area uncovered? Ensure AML compliance, even in the conflicted regions.

AML Watcher’s PEP data isn’t limited to geographical boundaries. Our solution extends to conflicted, less-known, or isolated regions where data can be scarce, but the risks are real.

We fill the gap, offering you the global insights you need to stay compliant, no matter where your business takes you.

AML Watcher’s ability to screen in controversial, conflicted, and isolated areas such as Northern Cyprus, a key offshore financial hub, Kashmir, a politically sensitive region with complex cross-border transactions, and Palestine, where economic sanctions and political instability increase AML compliance risks.

As financial dealings in these areas involve increased exposure to politically exposed persons (PEPs), our solution enables institutions to identify potential threats and maintain AML compliance with rising PEP risks.

AML Watcher helps businesses navigate geopolitical challenges, ensuring a proactive and compliant approach to AML regulations, by covering such complex regions.

5. Customized Regional Risk Relevancy

Why apply generic risk levels to a complex PEP world? Customize your strategy.

AML Watcher’s PEP Screening allows you to customize AML risk assessments based on regional relevance. Our system adapts to deliver the most accurate and pertinent risk profiles, regardless of whether you’re working in high-risk locations or areas with specific regulatory regimes.

Financial institutions can keep strict monitoring for PEPs who pose lower to higher risks from different regions and adhere to local AML laws because of this targeted strategy, which avoids treating PEPs uniformly.

6. Comprehensive RCA Mapping

Why only focus on the actual PEP when you can get information about their relatives too?

AML Watcher uses a complex combination of data analytics, proprietary algorithms, and access to international databases to provide a thorough screening of Relatives and Close Associates (RCAs).

Our solution maps relationships and finds potential RCA connections by looking at publicly available data, PEP histories, and social media insights.

Our continuous global coverage and real-time updates enable the system to detect new RCAs as they are added to global databases or when new data becomes available.

On a concluding note, avoid adopting a one-size-fits-all strategy for your PEP screening requirements rather go for a customized solution that caters to your organization’s risk appetite.

With a smart choice in the smart times, let’s move forward to a safer financial climate with a balanced and risk-based screening approach.

In cases like Nigel Farage, financial institutions must have robust anti-money laundering and countering the financing of terrorism (“AML/CFT”) compliance programs that do not include general “de-risking” guidelines for particular customer classes, groups, or statuses.

Since denying or canceling accounts based only on PEP status can have detrimental effects on reputation and customer trust, financial institutions must carefully balance risk management with respecting clients’ rights.

- No commitment needed

- Complete AML Database at your service

- Access our all-in-one dashboard

Tier-2 PSPs in ... must demonstrate automated monitoring, layered CDD, &...

See the Full Regulatory Expectation70–80% less manual work, 95% less fatigue, TruRisk Agent makes compliance effortless.

Experience Agentic AMLMove Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries