AML for Conveyancers: Understanding Threats and Compliance Needs

AML Compliance

April 10, 2025

Wondering why you have to go through rigorous AML checks when buying a house?

A Transparency International UK report found that more than £11.1 billion of suspected funds have been invested in the UK’s property market since 2016.

Of this, £5.9 billion was funneled through shell companies registered in British Overseas Territories, with the British Virgin Islands accounting for over 90% of these transactions.

The property market is a complex sector involving many legal, financial, and economic factors at play simultaneously. Over the past few decades, various scandals and offshore leaks have emerged, demonstrating how the property sector was exploited by corrupt politicians, public officials, and criminals to obscure and hide their ill-gotten monies.

As gatekeepers of property transactions, conveyancers hold a vital responsibility not only to facilitate smooth transfers of property ownership but also to hinder the infiltration of illicit funds in the real estate sector.

With growing awareness of the threats in the real estate sector, anti-money laundering (AML) compliance has become a critical aspect of the conveyancing process.

Impact and Scale of Money Laundering in Real Estate

A recent study found that an estimated £50 billion worth of UK properties are held by corporations registered in offshore jurisdictions or tax havens.

This is around five times larger if compared to the aggregate holdings of firms registered in foreign non-haven nations like the US, Japan, and France.

These offshore jurisdictions offer secrecy and obscure real ownerships behind shell companies, often facilitating tax evasion and money laundering. Establishing beneficial ownership is a key requirement in AML compliance.

With increasing scrutiny from regulatory bodies, such as the Council for Licensed Conveyancers (CLC), Solicitors Regulation Authority (SRA), and HM Revenue & Customs (HMRC), a robust understanding of necessary AML checks for solicitors, conveyancers, and real estate agents is unavoidable.

What Does Money Laundering Have To Do With Conveyancers?

Money laundering in the property sector is a prime target of criminals for several reasons. Unlike other laundering techniques where illicit funds tend to decrease in value through various transactions, real estate is known for its potential to appreciate over time.

The relative stability and appreciation of real-estate value not only offers capital gains but also generates revenue in rents. Additionally, the fact that real estate is a very high-value asset allows for the laundering of large sums of illicit funds in a single transaction.

The in-built complexity and scale of real estate transactions offer various means to hide the true source of funds. Complex corporate structures, spread across multiple jurisdictions and involving various bank accounts, can be used to obscure the real owners and origins of funds.

In some cases, properties are sold at artificially inflated prices to blend illicit funds in capital gains. Due to these heightened risks, clients have to go through money laundering checks when buying a house in the UK.

The AML Regulatory Landscape for Conveyancing

AML Supervisors for Conveyancers

The regulatory framework governing AML in the real estate sector is segregated among different supervisory bodies. The Council for Licensed Conveyancers (CLC) is the specialist authority for conveyancers and probate lawyers in England and Wales.

Whereas anti-money laundering checks for solicitors, including the conveyancing, are guided and supervised by the Solicitors Regulation Authority (SRA).

HM Revenue & Customs- HMRC is particularly entrusted with the supervision of estate agents and letting agencies. This multi-layered system ensures that there is robust monitoring and enforcement of AML in real estate sector.

Legislations and Regulations for Conveyancers

Legislation such as the Proceeds of Crime Act 2002 (POCA) and the Money Laundering, Terrorist Financing and Transfer of Funds (Information on the Payer) Regulations 2017 (MLR 2017) provide a solid legal foundation for AML compliance.

Conveyancers authorized or regulated by CLC must ensure compliance with its AML/CTF Code (Anti-Money Laundering & Combating Terrorist Financing Code). In addition, CLC also publishes an AML/CTF Guidance to help Conveyancers meet the requirements of this Code.

AML Compliance Trends in Conveyancing

According to the 2024 Annual Report of CLC, during the 46 inspections conducted, there were 25 inspections that were classified as non-compliant.

The CLC report mentioned that 80% of non-compliance inspections found a lack of documented policies & procedures and inadequate CDD procedures, whereas 44% were found to have no or inadequate records of client risk assessment.

The report further highlights that individuals and practices found to be non-compliant faced license revocations, disqualifications, and monetary fines.

Another 2023-24 AML Report by the Solicitors Regulation Authority (SRA) spotted that conveyancing services face the highest level of risks within the legal sector.

SRA highlighted that 73% of the total suspicious activity reports they filed to the NCA involved residential conveyancing.

Key AML Obligations for Conveyancers

Following is a summary of key money laundering checks for conveyancers:

- Conducting Firmwide AML Risk Assessment

- Conducting Client/Matter Level Risk Assessment

- Having written and risk-based AML policy, procedures, and controls

- Conducting client due diligence appropriate to identified risks

- Filing Suspicious Activity Reports (SARs) to the National Crime Agency (NCA)

- Maintaining compliance records and client identification documents for at least 5 years

- Continuous training and awareness program for staff on regulatory requirements

Three compulsory Legislations in Conveyancing

Firmwide Risk Assessment in Conveyancing

Risk assessment is a fundamental element of effective AML compliance. Conveyancers must evaluate the overall risk profile of their business environment, which varies widely depending on factors like geographic location, the nature of clients, and the types of transactions processed.

For example, a conveyancing practice operating in a major metropolitan area with an international clientele inherently faces a higher risk compared to a firm on the high street of a small town.

Similarly, transactions involving high-net-worth individuals or super-prime properties ask for enhanced due diligence (EDD), particularly when complex legal entities or offshore structures are involved.

Understanding these risk dynamics is not only necessary to ensure regulatory compliance; it’s also about protecting your business from unknowingly becoming a channel for criminal activity.

Effective risk assessments ensure that EDD measures are applied where necessary, preventing situations where suspicious activities might otherwise go unnoticed.

Integrating Client/Matter Risk Assessment

UK National Risk Assessment 2020 and CLC Risk Assessment 2024 both have identified high money laundering risks in real estate.

Research highlights that both the scale and complexity of real estate transactions enable criminals to exploit gaps in due diligence and risk management. It has become clear that geographical factors, the nature of the client base, and even the timing of transactions can all influence the risk profile of a deal.

Conveyancers are advised to embed these research findings in their day-to-day operations by taking into account firm and client-level risk assessments.

These should not be limited to static checklists but should instead be dynamic processes that evolve as new risks emerge.

Modern compliance software offering customized solutions and ongoing staff training programs are instrumental in ensuring that the latest risk factors are integrated into day-to-day compliance operations.

Risk-Based Client Due Diligence (CDD)

Risk based due diligence means applying enhanced due diligence for high-risk clients and various monitoring standards for other day-to-day clients not assessed as high risk.

Whereas the businesses are not expected to apply reduced/simplified due diligence in the real-estate transaction as the industry is overall assessed as high risk.

Customer Due Diligence (CDD)

- Identifying all vendors, buyers, sellers, trustees, and beneficial owners and verifying their identity.

- Obtaining information on the purpose and intended nature of the business relationship (although in most cases this will be self-evident)

- Establishing source of funds and wealth in all conveyancing transactions

- Understanding the ownership and control structure of a customer who is a trust, company, legal person, or a foundation

Enhanced Due Diligence (EDD)

In addition to CDD, enhanced scrutiny should be applied to high-risk clients, such as politically exposed persons (PEPs) or clients from high-risk jurisdictions. Including:

- Obtaining sufficient evidence to verify the source of funds and source of wealth

- Obtaining senior management approval for continuing or establishing a business relationship

In order to meet the EDD obligations, firms should have effective PEP identification systems such as those provided by commercial databases offering PEP screening.

2025 Money Laundering Red Flags for UK Property Market

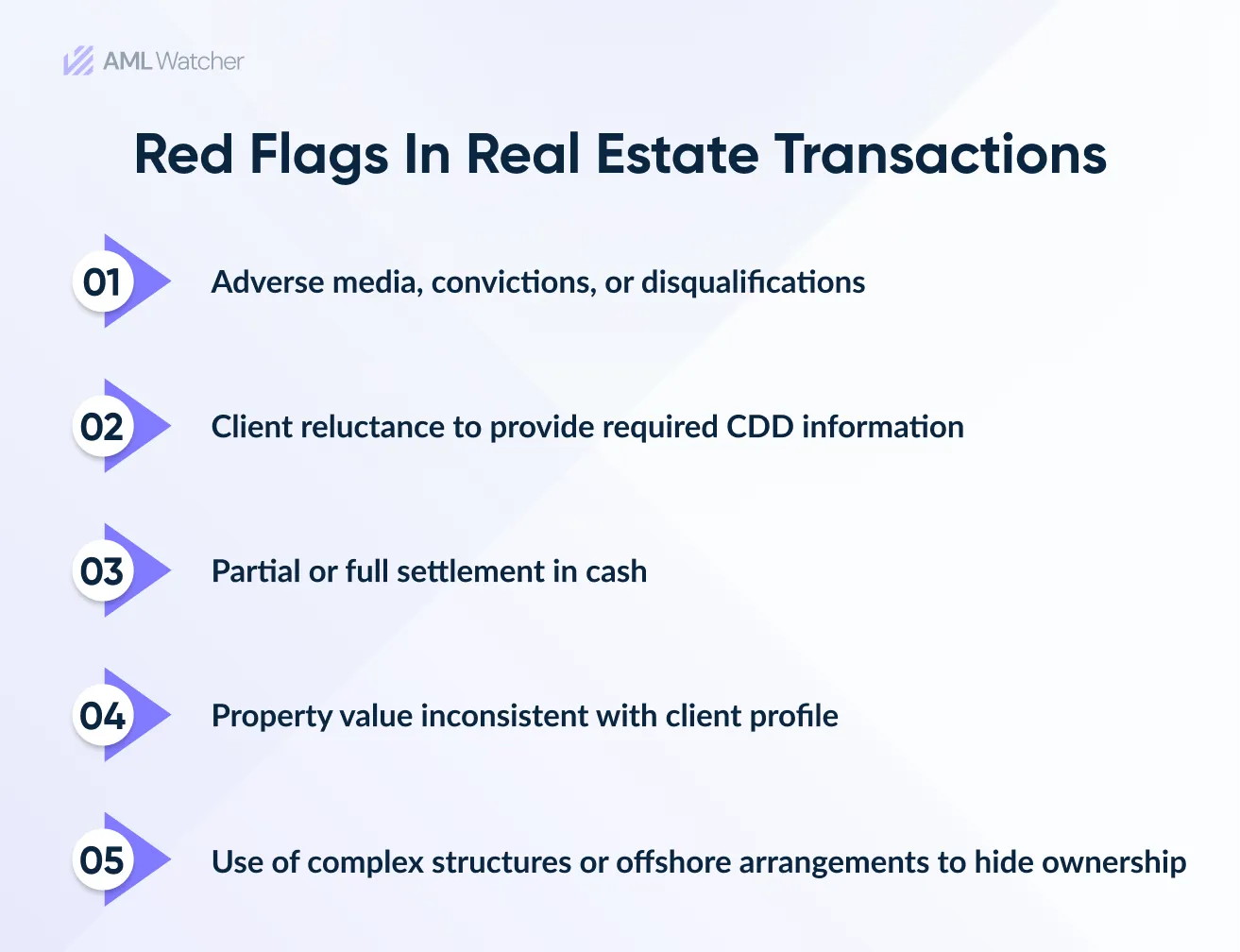

Depending on the circumstances of each case, the following are some indicators of risks or potentially suspicious behavior (but that’s not all) for AML checks for conveyancers.

These are the latest red flags in the UK:

- Searches on a party/associates to a transactions show presence of adverse media, disqualifications as a director, convictions for dishonesty or allegations of bribery

- Being evasive or reluctant to provide required customer due diligence information

- The person is trying to use intermediaries to protect their identity or hide their involvement

- Non-UK residents using intermediaries where it makes no commercial sense

- Part or full settlement in cash or foreign currency, with weak reasons

- Use of cash in a quick sale or tenancy agreement, or cash exchanges directly between clients – perhaps including a cash deposit

- Poor explanation for the early redemption of a previous mortgage

- The property value doesn’t fit the customer’s profile

- The ownership is not transparent and uses complex trusts, offshore arrangements, or multiple companies, possibly involving multiple countries

- Reluctance to employ a solicitor or other professional for conveyancing

Way Forward For AML Compliance

Sanctions Screening

Implement risk-based systems to screen customers and transactions against financial sanctions lists, as recommended by the Financial Crime Guide (FCG 7.2.3) of the Financial Conduct Authority (FCA).

FCA guide specifically recommends that a firm should have effective, up-to-date screening systems appropriate to the nature, size, and risk of its business.

In light of this recommendation and legal obligations, conveyancers should have an appropriate sanctions screening system in order to check their clients and parties to any real estate transactions against the applicable sanctions lists.

Adverse Media, Sanctions, and PEP Screening

The Legal Sector Affinity Group (LSAG), which comprises all legal sector regulators and representative bodies in the UK, has published an extensive and updated AML guidance for the legal sector.

This guidance provides detailed consideration, which should be undertaken for adverse media screening, PEP screening, and sanctions screening systems.

Staying informed of the changing regulatory environment and utilizing modern technologies that facilitate a risk-based approach are the best defenses against the sophisticated tactics of money launderers.

Prioritize AML compliance today to invest in a future where the property market and the financial system as a whole are protected from criminals.

The AML framework of 2025 will necessitate a proactive approach to compliance for success. In addition to providing excellent client service, conveyancers can protect themselves and their businesses by keeping up with legislative developments and having strong AML procedures in place.

Seeing compliance as a chance to improve your company’s standing and competitive edge rather than as a burden is crucial.

AML Watcher offers automated and customizable solutions for PEP, adverse media, and sanctions screening, catering specific needs of conveyancing services. Its proprietary database consists of regulatory enforcement records, criminal watchlists, global sanctions, PEP lists, and court records, providing an all-encompassing view of a customer’s risk profile.

- No commitment needed

- Complete AML Database at your service

- Access our all-in-one dashboard

Tier-2 PSPs in ... must demonstrate automated monitoring, layered CDD, &...

See the Full Regulatory Expectation70–80% less manual work, 95% less fatigue, TruRisk Agent makes compliance effortless.

Experience Agentic AMLMove Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries