Top 4 Stages of Customer Profiling in AML Risk Assessment

AML/CFT

April 15, 2025

In December 2024, a legal action was taken by AUSTRAC, the Australian watchdog against Entain Group, which operates Ladbrokes and Neds.

The action was taken because the company failed to adhere to the predefined AML standards and allegedly accepted $152 million in bets from high-risk entities that were involved in illegal activities.

This legal action was primarily taken because the company failed to adequately monitor its clients’ risk profiles and track suspicious transaction patterns.

Moreover, according to AUSTRAC, the company even hid the identities of high-risk clients and ignored large foreign deposits and bets. This case showcases the significance of customer profiling in AML solutions and how it is essential in mitigating financial crimes.

Let’s dive in to learn more about customer profiling and why there is a need for such mechanisms in AML adherence.

What is Customer Profiling?

Customer profiling in terms of anti-money laundering refers to the collection, analysis, and evaluation of a client’s information, background, and financial behavior to assess potential risks for money laundering or terrorist financing.

These processes are performed to assess the risk levels related to potential participation in money laundering or terrorist financing activities.

With customer profiling in AML, financial institutions and AML-obligated sectors can easily implement measures for effective due diligence and ongoing monitoring.

One good example of this is the Australian Commonwealth Bank, which enhanced its client risk assessment framework by integrating advanced ID protection technology.

Rather than solely addressing identity conformation, this initiative helps assess customer risk levels by detecting potential links to high-risk factors such as politically exposed persons (PEPs), sanctioned entities, regulatory enforcement subjects, or individuals from high-risk jurisdictions.

The adoption of this technology was driven by the rising need for robust risk assessment measures, given the growing threats of financial crime.

With these effective scam prevention measures in May 2024, approximately 1000 alerts to over 6000 users were issued through this technology, preventing huge fraud cases along reducing ID theft incidents.

It is crucial to ensure that an accurate customer risk assessment is based on the principle of filtering the actual risk and not the genuine clients.

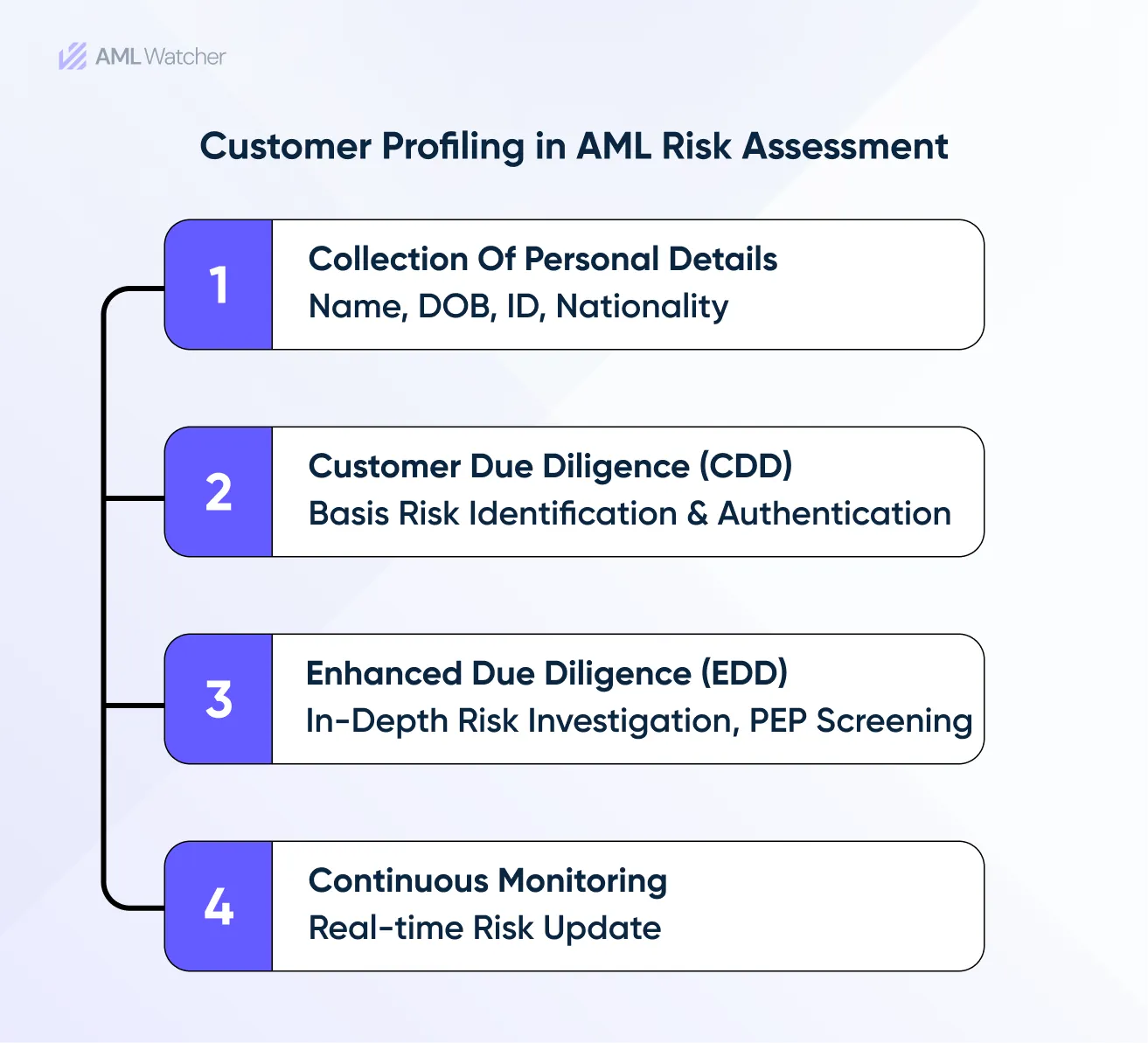

How Does Customer Profiling Take Place for an AML Risk Assessment Process?

Customer profiling is an essential component of AML risk assessment. The primary factors involved within this are:

Stage 1: Collection of Personal Details

The first step involves the collection of a client’s personal details to identify who they actually are. This information includes the following:

- A client’s name

- Date of Birth (DOB)

- Government-Issued ID Card

- Nationality

Cross-checking of these details is a necessary part of the customer identification process, and it sets the stage for accurate risk assessment.

Stage 2: Customer Due Diligence (CDD)

The second step is to assess the objective behind the client’s association with the company to establish their risk profile. Customer risk assessment plays a key role in customer due diligence (CDD) to detect potential threats.

The significant factors include PEP status, which increases corruption risk, sanctions lists, where entities are legally restricted, criminal watchlists indicating prior offenses, and regulatory enforcements, signaling compliance issues.

Client due diligence, or CDD, is necessary for regulated organizations to evaluate customer risks, ensure adherence to AML/KYC requirements, and reduce financial crime.

This process includes comprehension of a client’s:

- Occupation

- Sources of Funds

- Expected Account Activity

- Finance-based Transactions

CDD aims to know the client’s financial behavior to detect suspicious activities before they harm the company’s reputation from money laundering, fraud, and regulatory violations.

High-risk clients require enhanced due diligence (EDD) and continuous monitoring.

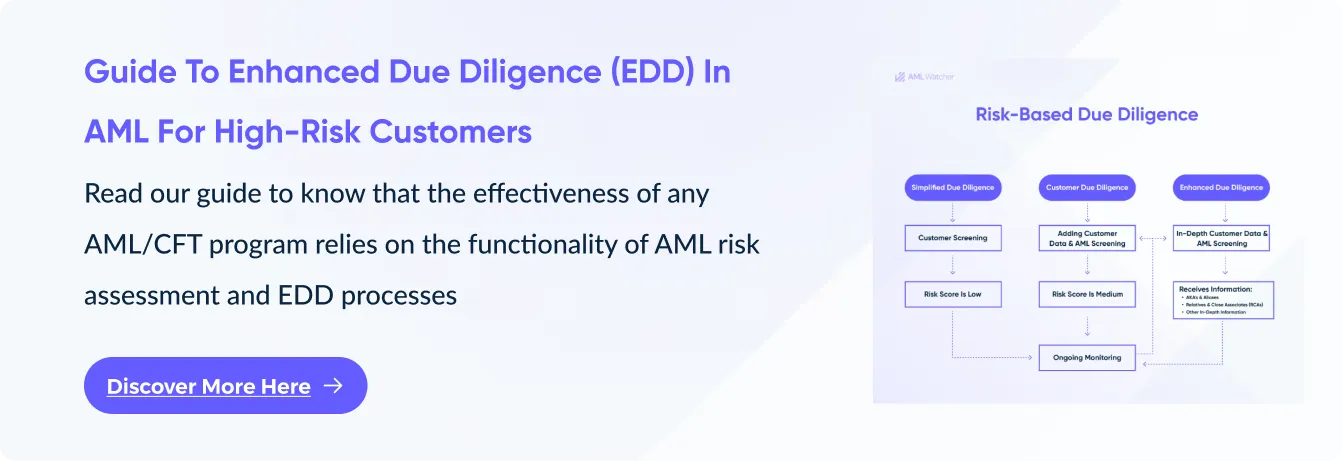

Stage 3: Enhanced Due Diligence (EDD)

Customer Due Diligence (CDD) lays the foundation for risk assessment, but Enhanced Due Diligence (EDD) expands on it by adding more steps to provide a deeper understanding of high-risk clients.

For the high-risk clients, a more comprehensive investigation is conducted, entitled Enhanced Due Diligence (EDD), in which the following elements are involved:

- Assess the business and individual connections of clients to determine if they are linked to high-risk entities. These connections may include both companies and individuals. That should be the primary requirement for every business. All these connections are checked to identify entities that are flagged for doing suspicious activities, regulatory enforcement, and sanctions.

- Focusing more on Politically Exposed Persons (PEPs) or those in positions that might be abused for money laundering.

- Track accounts to monitor suspicious financial activities.

Enhanced Due Diligence is a way to ensure that high-risk clients are more closely investigated to minimize the potential dangers such as money laundering, terrorist financing, and other fincrimes.

Stage 4: Continuous Monitoring

It is necessary to detect the anomalies and patterns that might cause money laundering in the future. For this, businesses require continuous monitoring. It will help them adopt the following approaches:

- Regular updating of client credentials.

- Evaluation transactions based on a client’s behavior.

- Implementation of automation to flag suspicious financial activities.

It is worth noting that the status of a person may change over time. Absence from PEP, sanctions, or enforcement lists during onboarding doesn’t ensure future compliance. PEP status may change, sanction lists may update, and adverse media can emerge at any time.

Ongoing monitoring assists businesses in instant anomaly detection and ensures real-time responses to potential risks.

With these above stages, a financial institution can effectively perform customer profiling by assessing the risk levels and implementing appropriate scrutiny measures.

When a company follows a structured, risk-based approach, it can easily ensure AML compliance and enhance the overall integrity of a finance-based system.

Is Customer Risk Scoring a Need?- Explore Through a Case Study

The case study of Morgan Stanley is essential in clearing the point: “Why is robust Customer Profiling a need of the business world?”.

Morgan Stanley, a global leader in financial services, faced numerous challenges in screening customers, especially internationally and in Latin America, which ended up increasing the risks for the business.

In response to this, regulatory bodies like the U.S Department of Justice and the SEC investigated the client detection and monitoring processes occurring at Morgan Stanley.

These imposed regulations instigated the response of the firm, in which they implemented different strategies to enhance their compliance and due diligence procedures.

These tactics were:

- Hiring AML compliance-trained staff to improve risk oversight.

- Implementing Artificial Intelligence for enhanced fraud detection.

- Planning new technology systems to improve instant tracking and customer profiling.

This case highlights the significance of customer risk scoring for the FinTech industry to minimize risk, ensure legal adherence, and maintain a protected financial environment.

Effective Customer Profiling – Know the Best Practices to Follow

To improve customer profiling practices, the FinTech industry should consider the following best practices:

- Risk-Based Approach

To apply the right tracking strategies, customers should be categorized based on risk levels.

-

Up-to-Date AML Screening Data

Use updated AML screening data on PEPs, sanctions, watchlists, warnings, and regulatory enforcements to ensure accurate risk assessment and compliance.

- Global Data Coverage

Implement a screening solution with global data coverage to detect suspicious activities and improve the accuracy of risk scoring without any limitation..

- Ongoing Updation

Customer profiles and transaction patterns should be updated instantly to ensure accurate risk assessments.

- Regulatory Compliance Training

A company must offer AML compliance training to its personnel to stay updated with the ever-changing standards.

- Law Enforcement Collaborations

Businesses must collaborate with financial intelligence units and regulatory authorities to hinder financial crimes and exchange insights.

Ensure Legal Adherence with AML Watcher’s Enhanced Customer Profiling

Are you a business owner or an entrepreneur who deals with diverse clients every day? Manual risk assessments with error-prone or costly procedures slow down your company’s progress?.

Therefore, if you want to get results faster, AML Watcher’s customer profiling based on customized risk assessment will be your guide in this way.

It empowers you with:

- Real-time risk scoring for accurate client assessments

- Timely update to PEP risk status in line with jurisdiction-specific regulations

- Quick Sanctions changes and delisting

- Ongoing monitoring of adverse media screening

Don’t let the inefficient profiling put your compliance at risk! Book a Free Demo today and see how AML Watcher can transform your customer risk assessment strategies.

- No commitment needed

- Complete AML Database at your service

- Access our all-in-one dashboard

Tier-2 PSPs in ... must demonstrate automated monitoring, layered CDD, &...

See the Full Regulatory Expectation70–80% less manual work, 95% less fatigue, TruRisk Agent makes compliance effortless.

Experience Agentic AMLMove Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries