What is Section 314(a) of the USA PATRIOT Act?

Legal & Law Enforcement

September 10, 2025

Where financial crime is constantly on the rise, collaboration between law enforcement agencies and financial institutions has become imperative. The aim of Section 314(a) of the USA PATRIOT Act, signed into law shortly after the 9/11 terrorist attacks, was to promote such collaboration. Section 314(a) equips the United States Department of the Treasury Financial Crimes Enforcement Network (FinCEN) with a tool for targeted, retrospective information sharing between law enforcement agencies and financial institutions.

To tackle financial crime, Section 314(a) directs financial institutions to act quickly, accurately, and confidentially when prompted by law enforcement. In practice, however, operational complexity and fragmented AML databases challenge even the most seasoned compliance teams to comply with the legal obligations of Section 314(a).

What is Section 314(a) of the USA PATRIOT Act?

In the fight against financial crime, Section 314(a) of the USA PATRIOT Act serves as a regulatory mechanism that bridges the gap between law enforcement agencies and financial institutions. Administered by the FinCEN, this legal provision enables law enforcement agencies to request from financial institutions information about individuals, organizations, or entities “engaged in or reasonably suspected based on credible evidence of engaging in terrorist acts or money laundering activities.”

This section establishes procedures for cooperation between financial institutions, law enforcement, and regulatory authorities to identify and disrupt terrorist financing and money laundering. It focuses on tracking financial links between terrorist groups, narcotics traffickers, and non-profit organizations, and ensures that institutions can identify suspicious accounts and transactions related to these groups.

SEC. 314(a)(2) of the US PATRIOT ACT

However, it is important to note that Section 314(a) operates within a confidential, need-to-know framework, as opposed to publicly available watchlists or sanction lists. The operational purpose of Section 314(a) is not continuous monitoring of individuals or entities. Rather, it is a tool to be used for targeted retrospective information to track illicit financial activity that may have otherwise evaded detection.

Note: Section 314(a) should not be confused with Section 314(b) of the PATRIOT Act. The former section permits law enforcement agencies to request information about suspected individuals from financial institutions, while the latter allows financial institutions to voluntarily share information with each other about suspected money-laundering activity.

As of September 2, 2025, FinCEN’s office has processed 8,125 requests. With 886 cases of Terrorist Financing and 7,239 cases of Money Laundering.

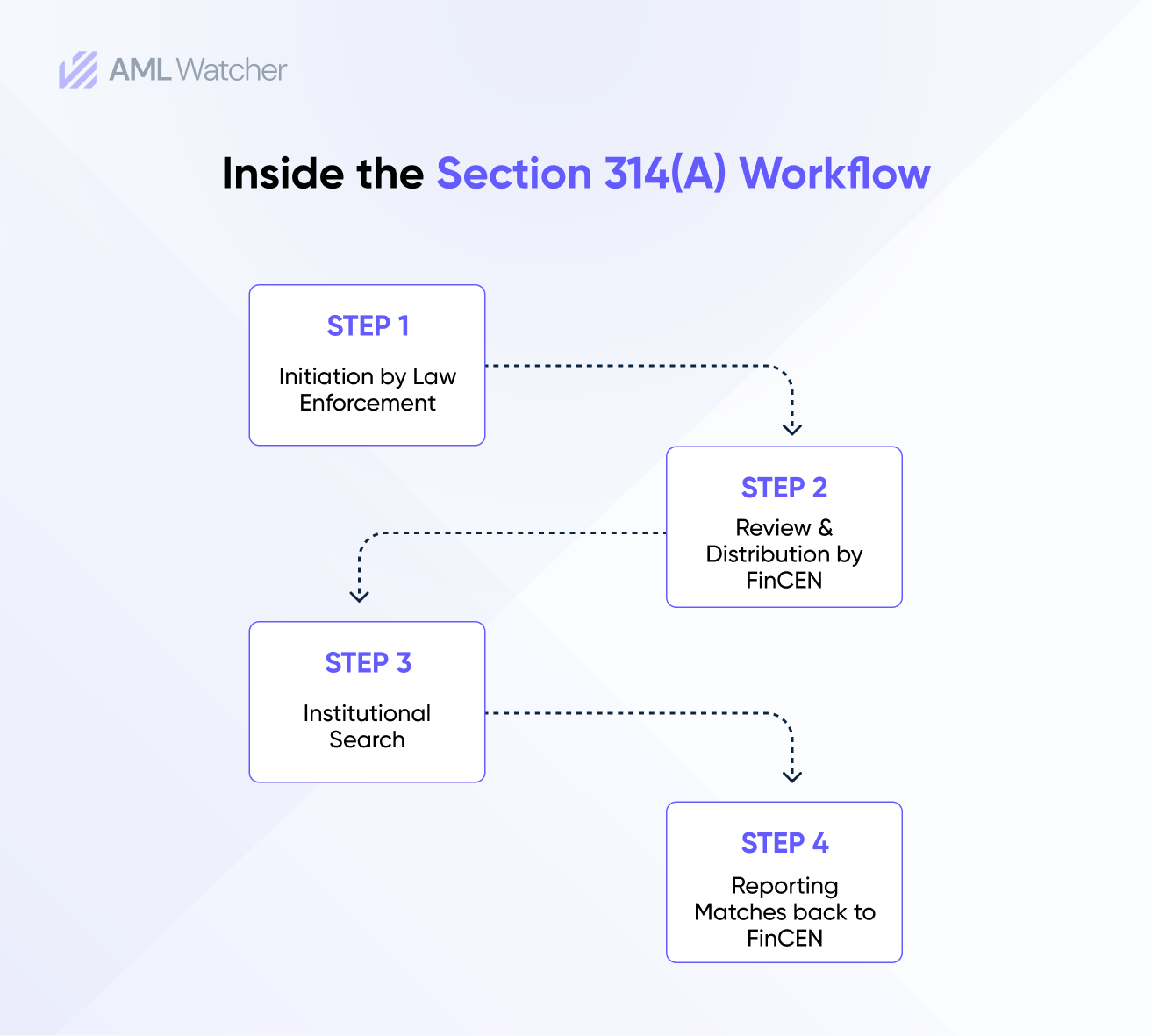

How does the Section 314(a) request process work? A step-by-step guide:

1. Initiation by Law Enforcement:

Under the scope of 314(a), law enforcement agencies, ranging from tribal law enforcement to Federal agencies, can submit a request for information from FinCEN. So, for instance, a particular law enforcement agency is actively pursuing an individual under suspicion of an illicit financial crime. To aid their investigation, a request for information is made to the FinCEN, which contains names, dates of birth, and any other relevant data of the suspected entity.

2. Review and Distribution:

If the request falls within specific parameters, FinCEN distributes the query sent by the law enforcement agency to a registered network of financial institutions via the Secure Information Sharing System (SISS).

3. Institutional Search:

Within 14 days of the distribution by FinCEN, the registered financial institutions shall search their databases for any matches related to the list of individuals/entities. This activity includes any account activity within the past 12 months and non-account holder transaction data from the last 6 months.

Essentially, financial institutions try to find a match for the list of individual entities in their systems.

4. Reporting Matches:

Where the financial institution has identified a positive match, it must report directly to FinCEN with the information. However, if no match is found, the financial institution is not required to respond to FinCEN.

5. Confidentiality Requirements:

Section 314(a) dictates that the flow of information throughout steps 1-4 above shall be confidential. Strict information measures are taken to ensure that the disclosure of these requests is made to the designated compliance personnel only, as the slightest breach of information can invite serious legal consequences.

The Multi-National Impact of Section 314(a)

While Section 314(a) of the USA PATRIOT Act is a US federal legislation and only financial institutions in the US are obligated to respond to Section 314(a) requests, it has a global impact. Financial institutions and international banks that operate in or with the U.S financial systems are obligated to follow the provisions of Section 314(a). Thus, institutions around the world should be prepared to respond to Section 314(a) requests from FinCEN – rendering compliance a global effort.

Failure to comply with the directions of section 314(a) not only risks financial penalties from regulators but also adversely impacts correspondent banking relationships with national regulators. In line with today’s interconnected financial system, where the occurrence of financial crime in one nation-state invariably has an impact on the rest of the world, a financial institution’s ability to satisfy the obligations under section 314(a) vividly demonstrates its AML competency in the financial world.

What are the compliance hurdles for financial institutions obligated under Section 314(a)?

For financial institutions, satisfying section 314(a) obligations is not a straightforward task. Although the process looks simple from the outset, it can turn into a compliance nightmare for financial institutions:

-

Fragmented Databases:

Critical data, such as customer or transaction information, is often spread across various legacy data systems, subsidiaries, or geographies. Compliance officers responding to a Section 314(a) request frequently have to pull information from various data systems – such as core banking data, transaction monitoring tools, and data from international subsidiaries.

The dispersed nature of such data makes it difficult to conduct timely and comprehensive searches when requested by FinCEN. In practice, compliance teams spend days chasing siloed data, which risks missing critical matches.

-

Resource Strain from Manual Workflows:

Most financial institutions lack automated systems to respond to a Section 314(a) request. Instead, compliance teams have to manually query multiple databases and reconcile the results into one document. All within the 14-day deadline. For a large financial institution with millions of records, such an effort can very easily overwhelm the compliance department.

-

Burden of Audit and Recordkeeping:

Financial institutions must ensure complete documentation at every step of the process when responding to a Section 314(a) request, maintaining a meticulous log of searches and outcomes for regulators. As is obvious, this task creates enormous pressure, as any gap in the audit trail can be treated as non-compliance—even if the searches themselves were carried out diligently.

Risk of Missed Matches and False Negatives:

Incomplete identifiers, coupled with transliteration issues and inconsistent data, may very quickly result in overlooked/missed matches. A single false negative would indicate that a terrorist financier or a money launderer remains undetected in the system, which might lead to regulatory fallout and adversely impact the institution’s reputation.

Confidentiality risk:

As discussed above, Section 314(a) requests are highly sensitive. They require a detailed guideline on data protection so that crucial information about this request is not made public. However, many financial institutions lack the infrastructure needed to guarantee security and restrict visibility to relevant personnel only.

For instance, although financial institutions can share the details about Section 314(a) requests with third-party vendors, they cannot provide direct access to the secure list of suspicious individuals sent by FinCEN.

An accidental exposure of sensitive details, even internally, can result in substantial penalties and compromise law enforcement investigations.

Global Complexity:

In addition to the above, multinational companies face the hurdle of coordinating and documenting data that spans multiple territories. Differences in data protection laws, system architecture, and legal obligations effectively mean that even the most routine 314(a) requests can turn into cross-border logical nightmares.

The cumulative effect of these challenges, then, is daunting. For Section 314(a) requests, compliance teams are often sandwiched between pressure to deliver rapid, accurate results to FinCEN and inefficient tools and fragmented data. For such compliance teams, each new Section 314(a) request feels less like a routine compliance duty, and more like a race against the clock – with the sword of potential regulatory and reputational consequences if anything is overlooked hanging over their heads.

What is the Smarter Way to Handle 314(a) Compliance Obligations?

Amid the pressure, what often feels like a compliance burden can be transformed into a structured, reliable process with the right AML solution. That is where AML Watcher comes in – a purpose-built AML solution software to dissolve the frustration and inefficiency of Section 314(a) responses.

Here is how each obstacle becomes manageable:

Central Database:

AML Watcher consolidates data from global, system-wide sources into one central AML Database, allowing you to run one unified search across sanctions, PEPs, Watchlists, and adverse media – as opposed to chasing fragmented data.

Batch Screening Capability:

With automated batch capabilities, API integration, and real-time screening services, AML Watcher helps you screen the entire FinCEN request list and displays search results in seconds – make sure that you report back to your regulator within the 14-day timeline.

Smarter Matching:

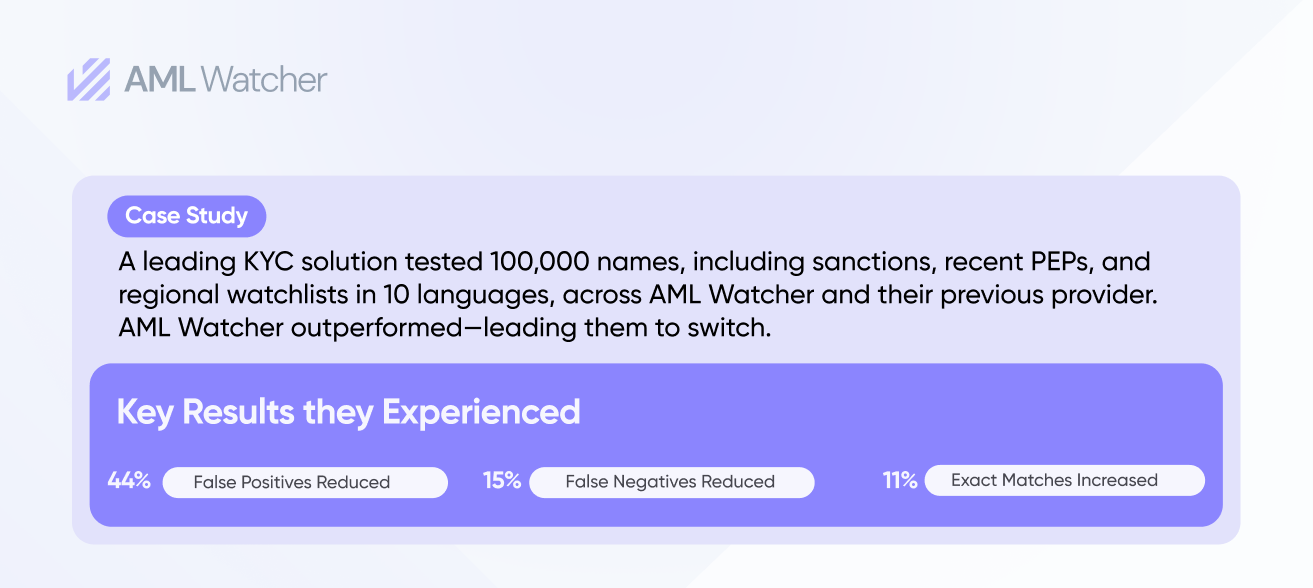

To counter false negatives and incomplete matches, AML Watcher’s proprietary name-matching algorithms, biometric AML, and cultural transliterations reduce false negatives by up to 15%

Confidential Access:

AML Watcher is fully GDPR-compliant and holds ISO 27001 certifications. This ensures that the confidentiality required under Section 314(a) is not only preserved but demonstrably auditable to the highest international benchmarks.

Contextual Insights:

Each match comes enriched with PEP, sanctions, adverse media, and watchlist data, complete with sentiment-scored news, which provides you with contextual insights, not just hits.

Transparent Audit Trails:

Every query, reviewer action, and output is logged with a transparent audit trail, rendering compliance reviews and internal accountability efforts simple.

Global Coverage:

To address your multi-national needs, AML Watcher’s global data coverage includes 2.6 million + PEP profiles across 235 countries, 80+ language support, and 3500+ specialized watchlists to ensure multinational coverage with consistent functionality across borders.

Compliance with Section 314(a) of the US PATRIOT Act is a test of speed, accuracy, and discretion. The right tools turn it from a regulatory burden into a demonstration of compliance strength – and with AML Watcher, that transformation is within reach.

- No commitment needed

- Complete AML Database at your service

- Access our all-in-one dashboard

Tier-2 PSPs in ... must demonstrate automated monitoring, layered CDD, &...

See the Full Regulatory Expectation70–80% less manual work, 95% less fatigue, TruRisk Agent makes compliance effortless.

Experience Agentic AMLMove Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries