9 Essentials of AML Compliance Checklist In 2024

AML Compliance

April 2, 2024

On 5th March 2024, the Financial Conduct Authority– a Financial Regulatory Body, sent warning letters to more than 1000 different financial institutions, which have had compliance deficiencies revealed by the audits of anti-money laundering procedures.

This is not the first time that any regulatory body has been advised to adopt strict AML compliance measurements. 2023 witnessed huge fines and penalties imposed by worldwide regulators for failing to comply with the AML Checklist. The changing laws and fraud enabled by artificial intelligence have penalized financial institutions over $7 billion in 2023.

This rising number of compliance fines and strict penalties has created the urgency and the responsibility for financial advisors to ensure that AML Checks and compliance are maintained. Such policies are beneficial because they prevent client funds from being accessed by other means even by people who are trusted advisors. According to anti-money laundering compliance, rules and regulations of your business, you must strictly follow, not to lose any of your client assets.

With the aid of AML check online, key standards are available to give you a comprehensive view of your new client’s business, its financials, transactions, and the nature of business activities. Through that, you can provide more scrutiny to any focal points or areas of concern as well as the opportunity to know your client better.

Since we understand that, what is the fundamental role of an AML for your financial institution? The important question is what are the AML checklists for 2024?

We put the key values on the map, and introduce you to the latest anti-money laundering checklists for financial institutions.

But first, grab the idea of AML regulatory checklists

What Is The Concept Of An AML Check list?

Anti-Money laundering checklist is the process that involves screening and verifying the identity of persons, groups, or entities to prevent money laundering, financial fraud, financing of terrorist activities, and any relevant monetary crimes. The principal intent of AML checks is to make certain the organization adheres to the laws and regulations, as well as keep up the stability of the financial system.

The common procedure usually involves collecting an individual’s details and analyzing activities to verify their identity together with the evaluation of the possible danger associated with the client’s involvement in funding terrorism or other illegal activities.

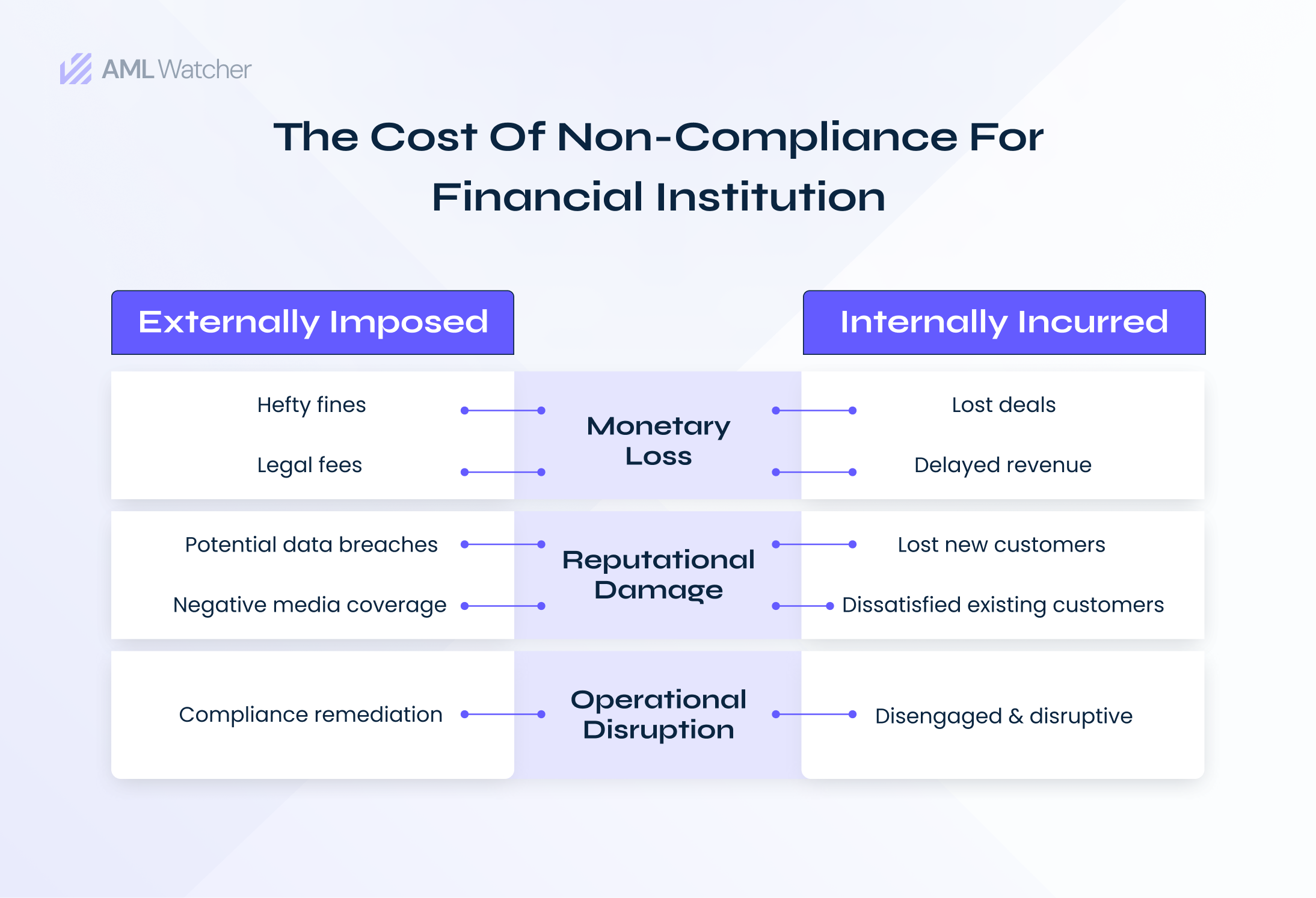

The Significance Of AML Compliance In Financial Institutions

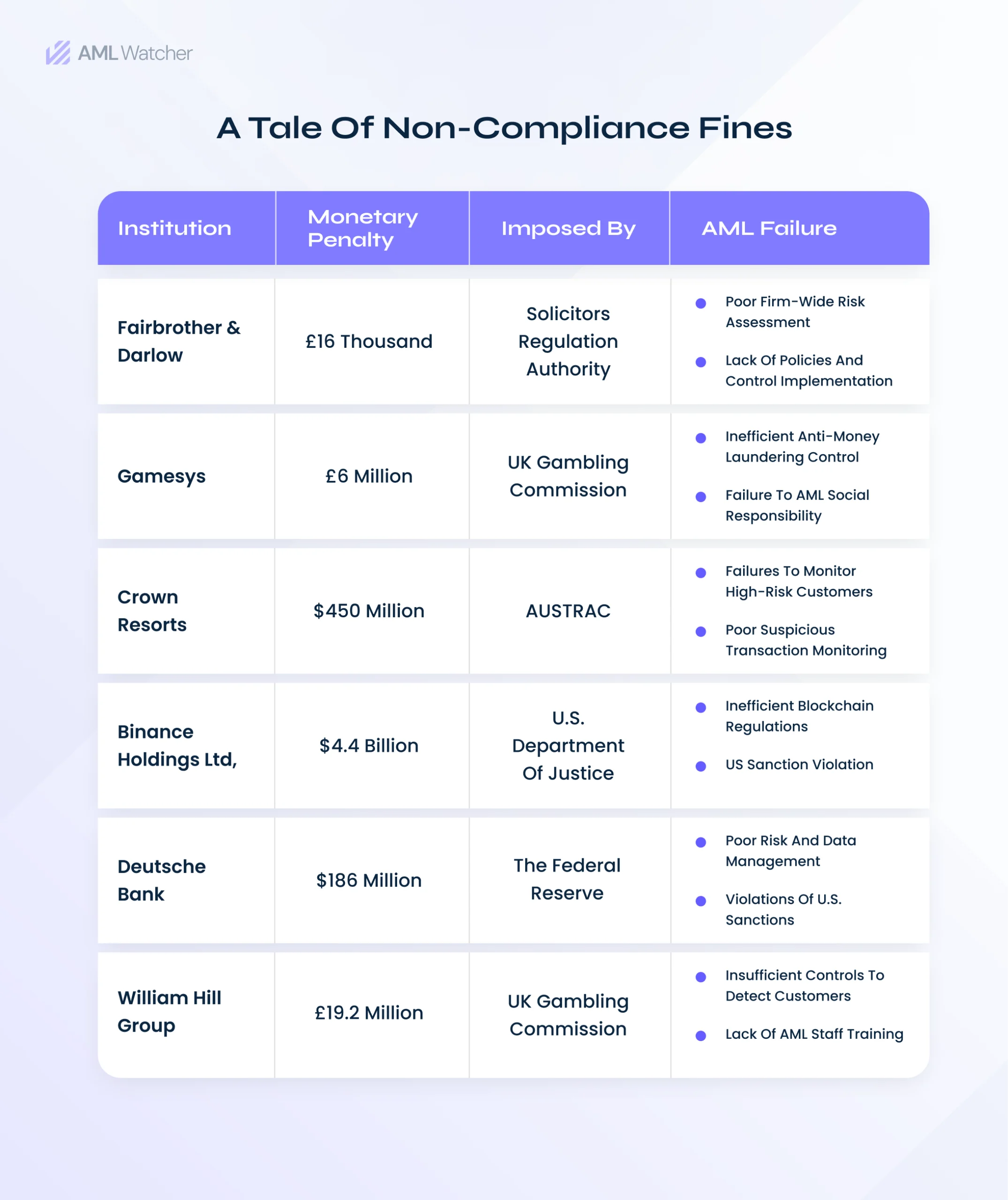

AML compliance is crucial, complemented by legislation such as the Bank Secrecy Act, SRA regulation, FCA guidelines, EU obligations, and the USA PATRIOT Act, and non-compliance may have critical consequences. So it won’t be wrong to say that AML non-compliance may come with big costs. There are multiple scandals like 1MDB in Malaysia, Danske Bank in Europe, the Credit Suisse case, Binance failure, Deutsche Bank AML lapses, JP Morgan Chase settlement, Crown resort non-compliance, and SkyCity fines clear the picture of confusion, why multiple AML regulations are very important and applicable in the current financial world.

Let’s move forward and read about the top AML checklists authorized by major international regulatory bodies.

Paradigm Of 2024 AML Compliance Checklists

Financial advisors are prime sources to understand the unlimited effect of financial crimes and the importance of implementing AML regulations as a key part of their professional practice. The 2024 anti money laundering compliance checklist includes;

Conduct an In-depth Risk Assessment

Performing an end-to-end risk assessment would be the key step of the FI’s AML compliance checklist. As per FATF regulations; recommendation 1, institutions have to implement the risk-based AML approach. The main purpose of these risk assessments is to identify, understand, and mitigate potential money laundering and terrorist financing risks related to customers, products, services, and geographies. It contributes to defining value for money spent, as well as designing AML programs that carry out specific risk assessments by:

- Evaluate customers’ risk based on money transfer patterns & transaction nature

- Set up parameters of risk tolerance characterized by the risk appetite and strategy

- Examine the unusual transaction response or red alert systems

- Analyze AML risks in different operations and locations

- Set the thresholds for balancing compliance and risk exposure.

Create Internal AML Policies

Risk assessment complete. The next step for your FI’s AML CTF checklist is to determine the weaknesses in the internal controls. Have you organized your internal control rules as well as AML processes?

Ensuring that the firm has an elaborate listing of its AML compliance practices documented will be part of the Compliance manager’s strategic tasks. As regards the US firms, their BSA-AML authorities must comply with the rules and regulations established by the FINRA, the financial market regulator in the US, regarding rule 3310.

Any financial institution’s internal AML procedures should include:

- A checklist to review the standards of the new product.

- Transaction monitoring measures

- Internal reporting procedures for suspicious activities

- Internal reporting ideally has to be regulated by the procedure.

- Detailed onboarding process with complete client verification

- Hiring compatible persons to check regulatory measures and prepare reports.

Regular Watchlist And Sanction Lists Screening

Conducting business with sanctioned personalities and entities under various international sanctions listing regimes causes relevant financial institutions great problems. FIs have to check outdated screening lists and must maintain the latest data that consider both those sanctions and risk-related screening lists, including customers and persons who are politically exposed to their relatives, or close associates. Banks in the USA, for instance, are obliged to screen customers via the Office of Foreign Assets Control sanctions lists and the United Nations Security Council sanctions list.

- Maintain high-quality customer data derived from identified sources.

- Utilize the appropriate technology for fast and automated sanctions screening

- Implement systems for screening customers and transactions against international sanctions lists

- Create an effective plan to counter each Red Flag

Reliable Customer Due Diligence

Identity verification is a crucial component of a risk-based AML/CFT strategy: banks need to identify the parties they are interacting with and their possible risks to take proactive actions. FIs should develop their customer due diligence beyond the basic operational and transactional patterns of the customers, by including interactions made and behavior profiles as a part of the customer’s risk profile

The AML checklist must start with identity verification using the detailed CDD measures and proceed to EDD for high-risk clients. A sound CDD measurement must follow:

- Verify their ID/DOB/other personal data substantially.

- Evaluation of potential risks corresponding to customer profile.

- Define the purpose and the dynamics of the client’s relationship.

- Assess their international transactional activities

Transaction Monitoring & Reporting

The FIs must recognize that AML compliance is an ongoing procedure and they must adopt continuous monitoring of financial activities to avoid facing penalty charges for non-compliance. They should create risk-based transaction monitoring protocols to pinpoint potentially dubious behavior and should file to SAR in such a situation. Firms would benefit from developing and using client risk scores in their review and decision-making processes and from enriching the data set in their respective AML and TM software.

- Transactions above regulatory thresholds.

- Monitor Unusual transaction patterns.

- Transactions from high-risk jurisdictions.

- Dealings with PEPs or sanctioned persons

- Transactions from customers with a negative history

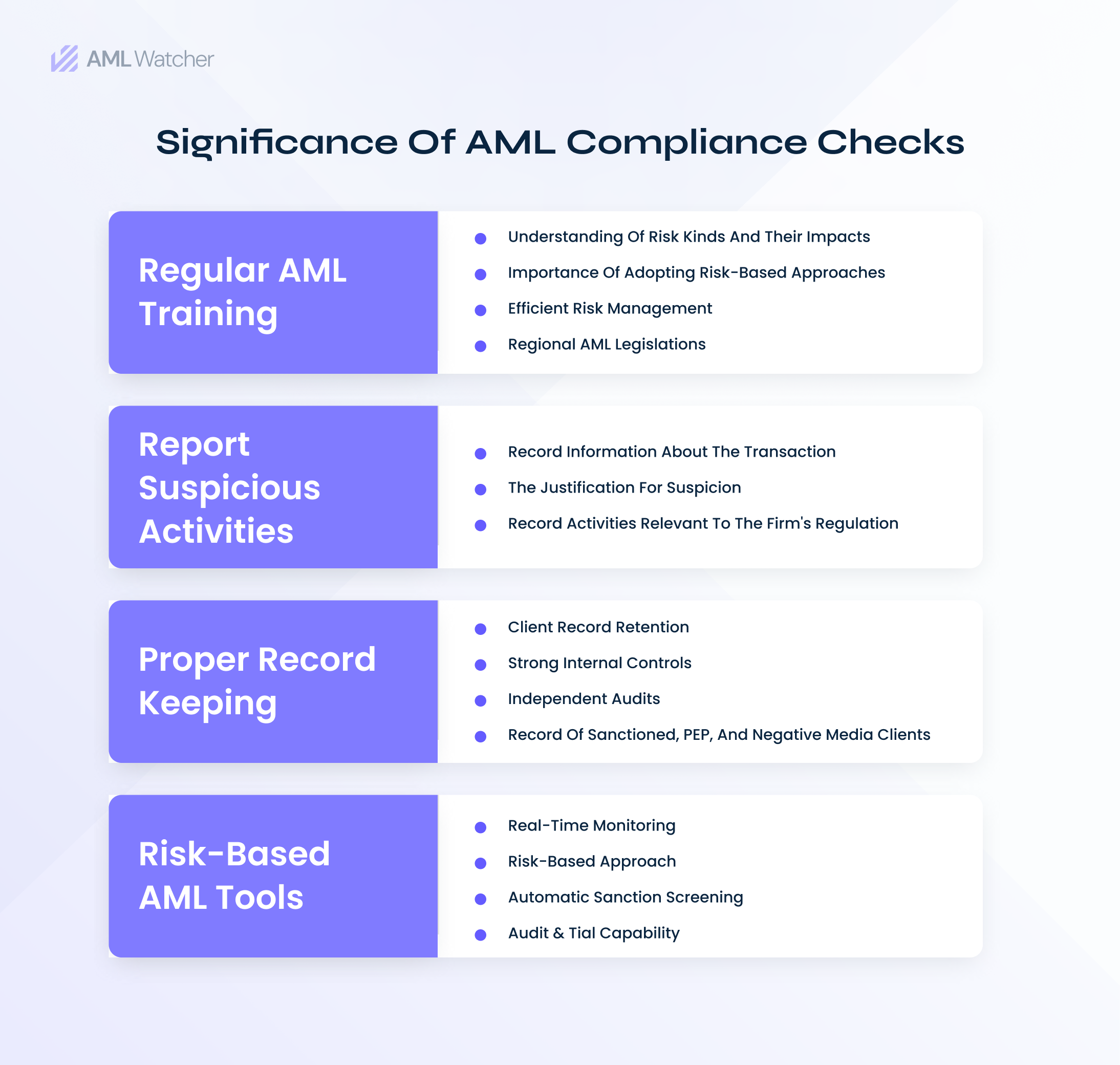

Conduct Regular AML Training

As per FATF regulation, staff members of financial institutions must undergo AML training to stay competent to detect red flags that are evidence of money laundering or terrorism funding. Additionally, the AML compliance checklist should contain an ongoing AML training schedule for operational to managerial level employees, to adapt to changing AML to new legislation, with a focus on the following:

- A clear understanding of risk kinds, categories, and possible impacts.

- Importance of adopting risk-based approaches

- Efficient Risk management

- Regional AML legislations

Report Suspicious Activities

The fact that bank accounts and transactions of clients are under deep scrutiny because they’re used to finance terrorism, launder money, or other illegal activities. Financial institutions need an advanced and transparent process for submitting the SAR to regulatory authorities.

The SAR submission process must be quick and confidential so that it won’t create an alert to make the suspected entity aware, recording:

- The organization’s authorized identity

- Information about transaction

- The justification for doubt

- Activities relevant to the firm’s regulation

Proper Record-Keeping

Traceability or audit trail is an indispensable part of AML Checks. It is imperative to preserve documentation for all AML process points, as banks assess the threat level through the client’s information. This type of information should be retained for the period that is lawfully required for any jurisdiction in compliance with the rules and regulations. It contains:

- Client verification and identification documents

- Transparency on transaction and institution role

- CDD records maintained via onboarding

- Information linked to clients’ wealth sources

- Record of sanctioned, PEP, and subject to negative media clients

Also, they are expected to keep all the documents of their formal risk-based assessment, anti-money laundry, terrorist financing, and sanctions compliance policies. Any revisions to these regulations need to be noted.

Utilize Risk-based AML Tools

Lastly, a financial institution must pay attention to the fact that it is imperative to combine automatic compliance tools and technology to reinforce the bank’s framework on compliance. The usage of these instruments, including the implementation of automatic systems for sanctions screening and dealing with dubious transactions, in addition to the introduction of ML algorithms in checks of fraud, watchlists, sanctions, and the negative media, can all serve as efficient gatekeepers if used and calibrated correctly.

To conclude, the regulatory system is changing its course, business corporations are required to direct huge attention to the AML Checklist and compliance regulation. Through AI-based AML compliance banks and fintech can develop a secure process without invading the freedom of the market, and thus deep financial frauds are avoided.

While the AML compliance program is 100% doable, it takes a huge time and effort for proper implementation, mostly when it is done manually, not to mention the growth of the transactions which comes with complexities. Thus, you may end up spending more time on compliance rather than running the business as usual.

Despite the challenges, effective AML software systems are available to help make the process faster. By automating essential processes such as data collection, identity validation, and watchlist checks companies can ease the burden of ensuring AML compliance while reducing the complexity that one usually encounters.

At AML Watcher, through our simplified and straightforward sanction screening solutions, we make AML compliance quick and easy. Our trusted global compliance databases streamline the task of screening new or existing users, regularly monitoring each member, generating quick risk alerts, keeping track of audit trails, and rapid response to implement new sanction policies among many other responsibilities. Also, your conversion rate can be significantly increased by giving users a screening experience that is suited for your platform and providing dynamic fraud checks appropriate to each user’s risk profile.

Are you ready to follow the latest AML compliance checklist and adhere to global AML regulations? Contact our experienced staff today to get AML Solutions to screen any individual.

We are here to consult you

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries