How E-Commerce Money Laundering Undermines Online Retail Success

Money Laundering

November 18, 2025

- Why E-Commerce is Fertile Ground for Money Laundering

- Common Money Laundering Typologies in E-Commerce

- What Regulators Expect from E-Commerce Marketplaces.

- AML Regulations in E-Commerce

- AML Measures for E-Commerce Platforms that Reduce Risk Without Delaying Growth

- Operational Challenges and How to Prioritize Risk

- How AML Watcher Assists in Securing E-Commerce Growth and Revenue

What if a mid-sized online marketplace overnight sees a surge of high-value purchases from dozens of new accounts, many of which are linked to fake e-commerce stores or suspicious merchants? Is this a product defect, an advertising spike, or the classic layering phase of a money laundering scheme dressed up as retail activity?

For many online retailers, repeated purchases, unexpected refunds, or odd payments are perceived as a system failure or a business irregularity, but in reality, it may reflect how launderers exploit refund and online payment gateways to disguise illicit money flows.

Digital businesses have turned into an attractive conduit for laundering illegal funds under the name of legitimate retail transactions. How do regulators and compliance teams separate the actual alerts from the false positives, and what specific AML measures for e-commerce platforms should online businesses take to stop participating in a money laundering scheme unintentionally?

It is important that e-commerce retailers understand and know how to detect anomalous customer behavior, align it with applicable regulatory standards, and design AML programs that reduce risk in the ecommerce sector.

Why E-Commerce is Fertile Ground for Money Laundering

E-commerce combines speed, size, and multiple ways to make payments, such as through cards, wallets, bank transfers, and even third-party marketplaces. This convenience also creates many low-friction entry points for illicit funds.

Criminals exploit these features by returns and refunds, vouchers, staged purchases, and multi-account schemes to obscure the money trail. Some even use high-value goods as a store of value, and create fake e-stores that generate phantom sales.

PSPs often face this challenge, as fake store schemes may seem authentic and use multiple payment rails to hide illegal activities.

E-commerce sites and payment providers of all sizes face more exposure to money laundering because cross-border transactions, remote onboarding, and rapid refunds have a high potential of hiding criminal proceeds.

The Financial Action Task Force (FATF ) has published a detailed report with case studies on how vulnerabilities in commercial websites and internet-based payments are exploited for layering and integration of criminal funds.

Common Money Laundering Typologies in E-Commerce

The standard money laundering typologies that the online retailers should be aware of are:

- Return/refund laundering: Criminals buy expensive items with illicit funds, then return them to obtain refunds to a “clean” account or card.

- Voucher/coupon laundering: Offenders convert cash into store credit or vouchers and pass value between accounts.

- Merchant collusion: Fake merchants or complicit vendors process payments to obscure the fund origin.

- Fake E-Commerce Store Laundering: Scammers build e-shops that have their presence solely to generate fake transactions, transferring illegal funds with the help of payment gateways, without actually serving the purpose they are built for.

- Account takeover/mule networks: Compromised or synthetic accounts funnel payments across many small purchases without triggering alerts.

- Layering via marketplaces: Criminals use multiple marketplaces, currencies, and payout systems to create complex trails.

With appropriate merchant authentication and monitoring of payout flows and unusual transaction patterns, PSPs can detect the linked risks effectively. Static rule thresholds alone are not enough for the advanced systems that need contextual, cross-channel correlation.

What Regulators Expect from E-Commerce Marketplaces.

With the expansion of e-commerce, regulators are increasingly focused on regulated payment entities such as Payment Service Providers (PSPs) and Electronic Money Institutions (EMIs), which handle customer payments and facilitate financial transactions for online stores. In recent developments, some jurisdictions, such as New Zealand, have explicitly extended AML obligations to e-commerce marketplaces.

This means that if a marketplace transfers money or value for customers or manages payment instruments, it is obligated to develop a risk-based AML CFT program. Platforms like Amazon, which operate payments systems (Amazon Pay) are obliged to comply with certain AML obligations in different jurisdictions.

Despite jurisdictional differences, the majority of the AML regulators converge on a few requirements for the merchants and platforms. These key AML procedures in e-commerce are:

- Risk-based Due Diligence: Know your merchants, sellers, and buyers. Categorize the level of risk for each transaction and apply enhanced checks where appropriate.

- Sanctions and PEP Screening Across Customers and Merchants: Platforms must screen when onboarding and periodically thereafter.

- Transaction Monitoring Tuned for E-commerce Fraud Behaviors: Track for irregularities like rapid high-value purchases, unusual refund patterns, multiple accounts using similar payment instruments, or geographic mismatches.

- Recordkeeping: Keep sufficient proof for inspections and file SARs when activity suggests criminal origin.

- Merchant cooperation with Payment Processors and Banks: Both online platforms and payment services providers must closely track transactions. PSPs can identify shady merchants and high-risk payouts before the platform itself does. Regulators also expect the e-commerce platforms to identify real merchants and be alert to sellers or e-commerce stores that have only a paper presence.

These principles map to concrete controls such as customer identification (CIP), seller verification (KYB), ongoing screening, automated surveillance, and effective case management. However, the crucial challenge that e-commerce platforms face is the seamless alignment of user experience with the severity of AML obligations.

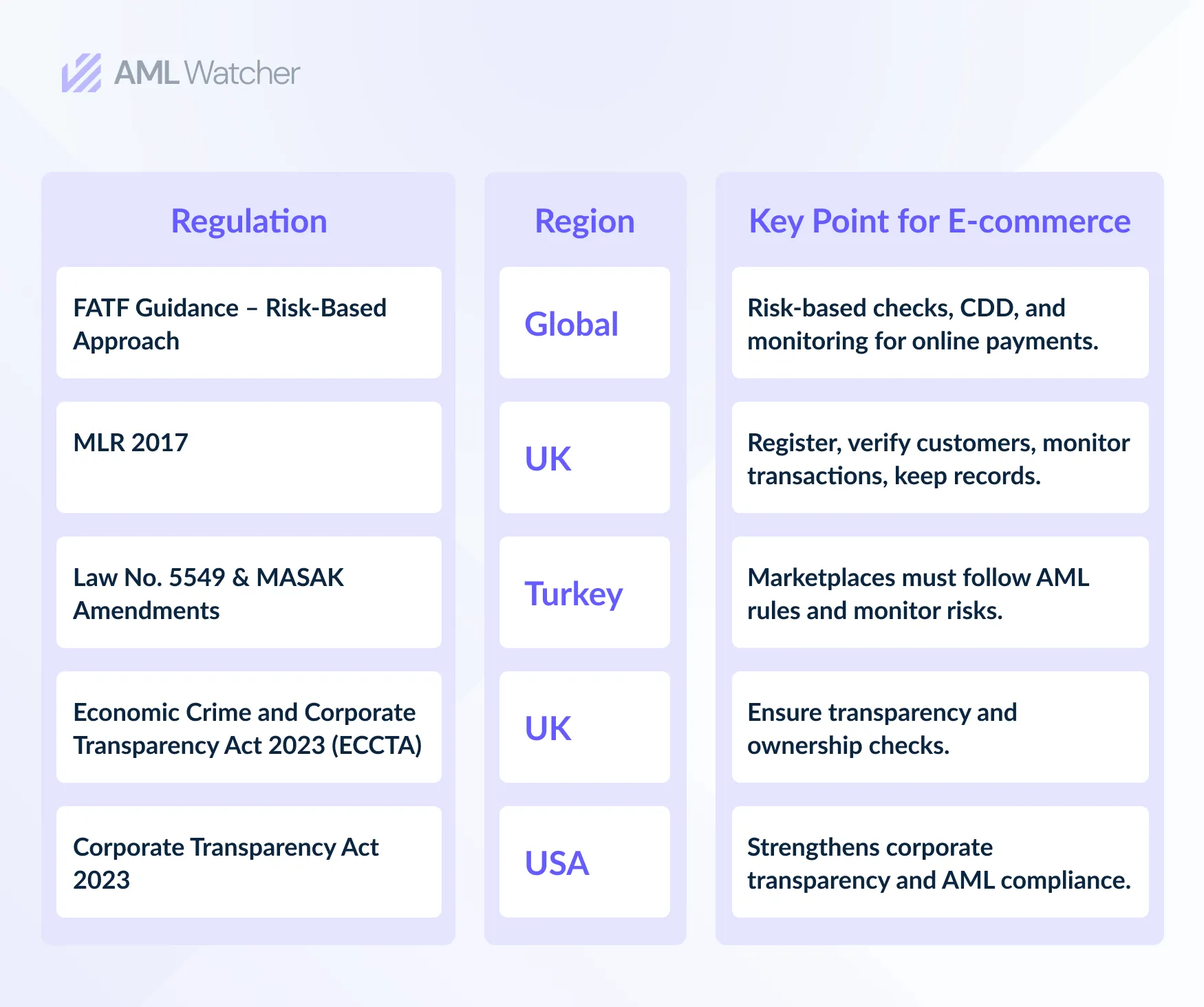

AML Regulations in E-Commerce

Here’s a list of AML regulations for online businesses that help them stay on track without going through huge penalties and reputational damage. Furthermore, compliance teams are required to prioritize the appropriate tracking e-stores and merchants that do not exist and generate fake transactions indicative of money laundering.

AML Measures for E-Commerce Platforms that Reduce Risk Without Delaying Growth

E-commerce businesses can take the following practical steps to meet regulatory expectations without slowing their growth.

1) Apply Layered Risk-Based Approach

E-commerce businesses must adopt a tiered risk-based approach for identification. They must use lightweight friction for low-risk buyers and enhanced due diligence for high-value transactions, new sellers, or payout requests.

For marketplaces, they must apply Know-Your-Business (KYB) checks on merchants and verify beneficial ownership where applicable. Furthermore, e-commerce businesses should look for the merchants and e-stores that are present solely to process anomalous transactions.

Businesses are required to identify signals such as IP geolocation, email age, and phone verification. The addition of this context will help distinguish fraud in e-commerce from genuine shoppers.

2) Enhance Payment Transparency with Provenance Data

They should capture payer instrument metadata, including card tokenization, issuer country, wallet ID, routing paths, and intermediary processor IDs. Correlating payment provenance with customer behavior makes refund laundering and rapid cash extraction easier to detect. Payment enrichment is essential for triaging alerts and for investigative handovers to banks.

3) Improve Risk Detection with Context-Driven Insights

Online businesses must move beyond static thresholds. They should deploy continuous media monitoring and context-driven risk assessment, so that compliance teams can identify suspicious entities linked through shared identifiers or recurring adverse patterns. This helps expose fake stores, refund abuse, and merchant networks attempting to conceal illicit funds.

4) Optimize Alert Accuracy

Legacy AML systems produce high false positives, which drain compliance resources. Digital businesses must invest in alert-scoring that combines identity, payment provenance, and behavior, along with feeding high-value alerts into a compact case management workflow with clear escalation to SAR filing. There, they have continuous feedback loops, where investigators label outcomes and improve model precision.

5) Integrate Sanctions, PEPs, and Adverse Media Screening

E-commerce businesses must screen customers and merchants at onboarding and periodically thereafter against updated sanctions, politically exposed persons (PEPs), or watchlists for human review. For cross-border platforms, embedding sanctions compliance directly into payment routing and payout controls to block prohibited beneficiaries. Automated sanctions checks can seamlessly reduce legal exposure and preserve marketplace integrity.

6) Collaborate with Payment Partners and Banking Rails

Digital businesses are required to design data-sharing contracts and APIs with acquirers, payment processors, and virtual wallets. Initial involvement with payment service providers is a great way to identify whether the merchants and e-commerce stores are fake, which prevents illegal gains from entering the systems. Aligning on shared data standards and escalation protocols assists in closing detection gaps across the ecosystem.

By integrating these best practices, e-commerce businesses can seamlessly adhere to the evolved regulatory requirements while protecting users and sustaining growth.

Operational Challenges and How to Prioritize Risk

Compliance owners frequently face three tradeoffs:

- False positives vs. missed laundering

- Customer friction vs. security

- In-house build vs. buying detection capability.

Risk Prioritization

For prioritizing risks, e-commerce businesses should start with a risk map. This map includes:

- A list of which products, merchants, or geographies create the largest monetary exposure.

- They must highlight the onboarding/KYB gaps and refund paths that enable fast cash extraction.

- They are required to automate low-confidence decisions; reserve human review for high-impact or ambiguous cases.

- They must regularly validate models with known typologies and red-team tests (shadow runs against synthetic laundering scenarios).

How AML Watcher Assists in Securing E-Commerce Growth and Revenue

E-commerce platforms face increasing exposure to refund laundering, mule networks, and sanctions breaches. A scalable compliance program must evolve with the product roadmap, balancing growth and risk control. Let AML Watcher help you with that by identifying the fraudulent merchants, fake e-commerce stores, and suspicious multi-account networks. It empowers compliance and product teams by delivering:

- Context-driven and customized risk scoring that fuses identity, payments provenance, and behavior.

- An all-in-one dashboard to perform automated sanctions, PEP, and watchlist screening at onboarding and payout.

- Transaction monitoring for identifying suspicious transactions.

- Cross-functional compliance tools for both compliance and product teams.

- Case management with an investigator feedback loop that reduces false positives and shortens time-to-disposition.

E-commerce businesses can strengthen compliance and protect revenue by integrating AML Watcher’s continuous screening and transaction monitoring to detect risks in real time.

Move Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries