How to Build Better Fraud Scores With AML Data

Fraud Prevention

October 30, 2025

With Generative AI and realistic deepfakes being created at scale, businesses in general and financial service providers in particular are becoming more vulnerable to fraud. In a hyper-connected digital economy, Fraud is no longer just a couple of bad transactions; it is an evolving phenomenon that shifts by channel, season, and product. To counter this increase in fraud attempts, businesses now require anti-fraud mechanisms to protect their users, revenue, and reimbursement costs.

While some fraud attempts may be easier to identify, other evolving fraud techniques are challenging to tackle. Businesses must understand the complexities of different types of fraud to counter such fraudulent activity. This includes understanding the meaning of fraud, its typologies, how such attempts can be identified, and how a fraud and risk scoring system can help protect your business.

This is exactly what a fraud score does. It analyzes data about a customer or transaction into a risk number so businesses can approve, reject, or monitor the action in question with confidence. In this way, a precheck on customers and transactions allows companies to easily identify fraudulent activity through the rating of a fraud score.

What is a Fraud Score

At its core, a fraud score analyzes data and quantifies it into a number. It is an algorithm that estimates the likelihood of fraud by assigning a value to anomalous patterns in actions such as logging in on different devices, frequently changing bank details (such as PIN Number), and making purchases that do not match previous purchase patterns.

Based on certain factors, the fraud score check essentially indicates the likelihood of fraud in a particular action. So, for instance, if a suspicious transaction generates a high value of fraud score, this indicates that the chance of fraud is higher in this action.

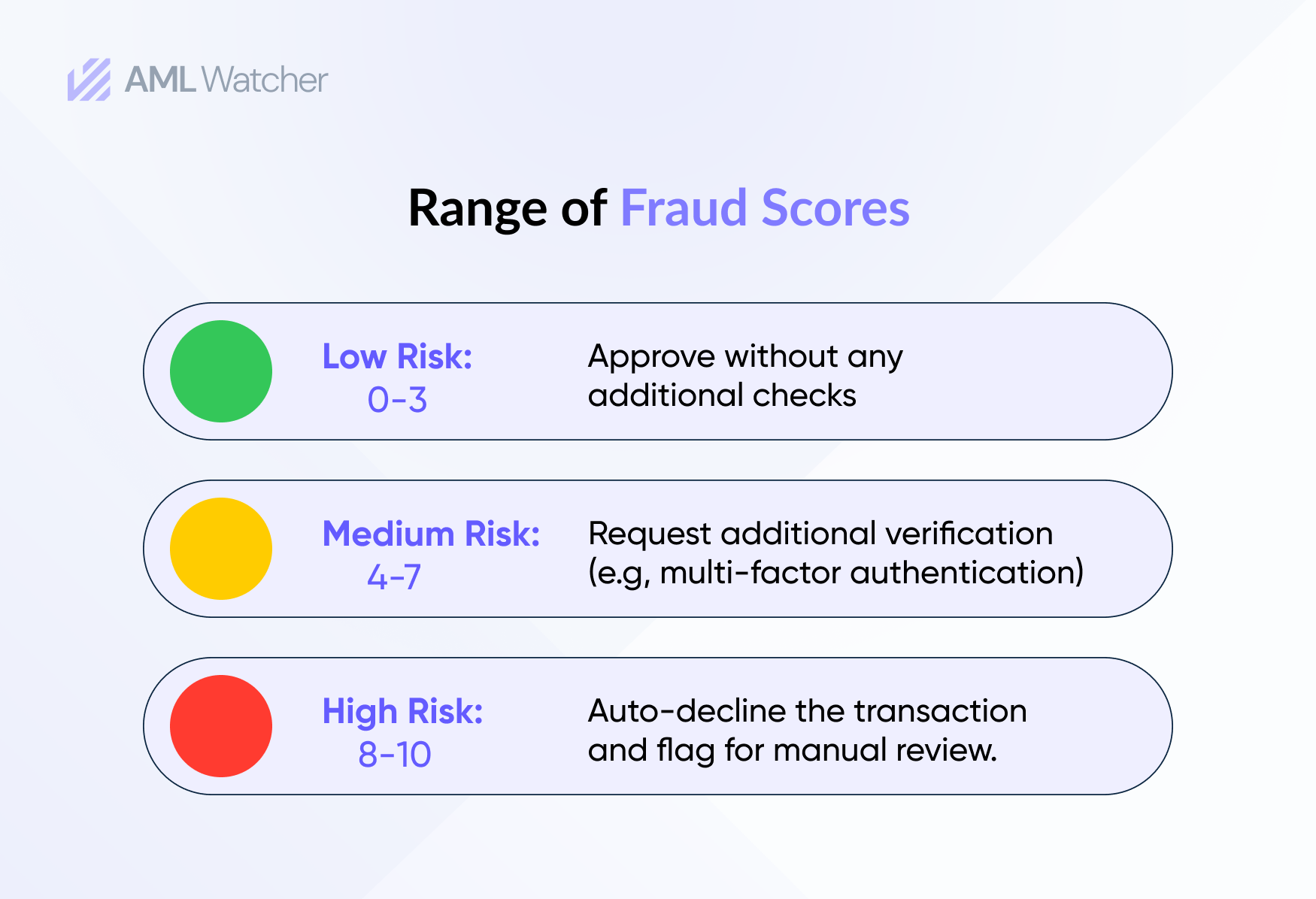

While fraud scores do not have a universal standard way of representing numerical values, the range of fraud may be expressed in different ways. For example, it can be expressed from 0-10, with 0 being a low fraud score and 10 the highest.

How a fraud score system calculates the chance of fraud depends on the model used (rule-based, machine learning or hybrid). Regardless of what model is used, the key to a reliable fraud scoring system is the variety of signals and the quality of data that is feeding the score.

Why is a Fraud Score Important

A fraud score has great utility:

- Control and Efficiency: A fraud score typically generates a result in milliseconds. Businesses can generate fraud scores for a multitude of events or entities and quickly approve multiple cases, while sending the higher fraud score results for further review.

- Consistency across channels: Data received from a customer or a transaction can be cross-checked against external sources (such as credit bureaus, telecom providers) to verify the authenticity of details such as addresses and phone numbers.

- Transparency: An effective fraud score system explains the score why the fraud score was high or low, so analysts and auditors can understand why that risk of fraud appeared.

What Are the Early Warning Signs of Fraud:

Although there is no set list of every early warning sign of fraudulent activities, there are some common patterns that often result in fraud:

- A brand new device for a known customer.

- Consistent attempts at resetting passwords and failed login attempts.

- Details that do not fit together, such as the IP address appearing from a place far apart from the registered city.

- Sudden changes to bank accounts or personal addresses right before the withdrawal of money.

- The same phone, email, and bank details are being shared across multiple accounts.

- A high risk due to adverse media reports of the individual.

- Individuals are being named in criminal watchlists.

How is a Fraud Score Calculated in Practice?

Generally, fraud scores analyze certain sets of data to generate a numerical value that indicates the chance of fraud of a particular action or entity. Here is a simplified breakdown of how fraud scores are calculated:

Data Collection:

The first step in calculating fraud scores is to gather data from different sources. This data can include:

- Transactional data such as time of day, transaction history, amount, etc.

- Identity data that includes phone numbers, addresses, emails, and IP addresses, etc.

Feature Engineering:

The raw data collected previously is then translated into a language that the fraud scoring system can understand. For instance:

- Transaction velocity: the frequency of transactions.

- Geographic consistency: whether the customer’s location matches their registered address.

- Device Consistency: Checking if the customer is using a familiar device or if there is a sudden change (such as logging in on a new device or a new browser).

Scoring Model:

The features are then fed into the fraud detection model the businesses has selected. There are two common types of fraud scoring models:

- Rule-Based Models use static predefined rules (for example, if the transaction is over $500 from a high-risk jurisdiction, assign a high-risk score)

- Machine Learning Models are trained on large amounts of data to detect patterns and behaviors that are indicative of fraud. These models are not static and can adapt over time to identify new fraud patterns.

Weighing:

Each data input is not equal in value. For instance, repeated attempts to log in to a bank account might weigh more than a discrepancy in the registered address. Weights are assigned to different features based on their significance.

Fraud Score Calculation:

After the features are processed and weighed, the fraud scoring system calculates a numerical value within the set range – indicating whether the act was high-risk, medium-risk, or low-risk. This score is a composite of all the data points fed into the system.

Final Decision:

The final step of this process is for businesses to decide the course of action based on the fraud score. If the score is high, the business may block the transaction. If it is low, the fraud score system can approve it without any additional checks.

Quick FAQ!

Is a fraud score the same as an AML risk score?

No. A fraud score estimates the chance of immediate misuse or loss. An AML Risk score assesses the long-term financial crime and regulatory exposure of an entity. However, AML signals further augment fraud scoring

When Should You Run a Fraud Score Check?

Fraud score checks are not a one-time activity, they are required throughout the customer’s journey. For instance, an initial check can be conducted at onboarding, with further checks during suspicious activities such as unusual transactions and repeated login attempts.

Given the vulnerability of e-commerce platforms and payment service providers to phishing and other fraudulent attempts, multiple checks are required.

- Onboarding: At the time of onboarding, to catch fake identities early by behavior and identity signals..

- Logins and resets: When a customer has repeated login or reset attempts, including unusual device swaps.

- Account Changes: When updates or changes are made to a bank account.

Payments and Payouts: At the time of unusual transaction sizes, large withdrawals, and suspicious behavior, such as unusually high purchase frequency and failed login attempts.

How Can Businesses Integrate Fraud Scoring

1. Build a baseline

Create/integrate a fraud scoring system with transaction, device, and behavior features.

2. Add external intelligence:

Integrate fraud scoring by incorporating sources like FRAML, which combines AML screening (PEP, sanctions, adverse media) with fraud risk indicators.

This integrated approach provides a holistic view, allowing companies to identify potential fraud while ensuring compliance with anti-money laundering regulations.

3. Monitor:

Track your model’s performance weekly, maintain a clean inventory, and keep a version history for auditors.

4. Testing:

Review thresholds and, on a frequent basis, retire rules that add friction and create roadblocks.

How AML Watcher Helps Fraud Scoring:

Whether you decide to integrate or create a fraud scoring system for your business, Most fraud score solutions focus on transaction-related risk intelligence, but AML Watcher enhances this by adding watchlist proximity—linking customer risks to adverse media data (which includes screening against news sources that tag negative news reports for crimes such as fraud and corruption) and Risk-Based Transaction Monitoring – which allows incorporation of risks as they evolve with time.

A fraud scoring system aligned with the FRAML approach thus enables your businesses to gain a more comprehensive view of potential criminal activity.

Move Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries