How Does Hawala Pose High Money Laundering Risks?

Money Laundering

November 5, 2024

- Hawala System In a Nutshell

- Is Hawala Network a Concealed Risk or Potential Advantage?

- How Does Hawala Operate In Current Financial Ecosystems?

- AML Regulatory Approaches to Hawala

- Legitimate Hawala Operational in Dubai

- Is Hawala a Good Source for Transferring Money?

- Hawala Categorized by Illegal and Legal Usage

- How Hawala Creates Risk for Money Laundering?

- A Practical Pathway To Addressing Money Laundering Risks

- How?

Unlike the common assumption that bank transfers are the most prevalent method of sending money, ancient and informal methods never dissipate; they quietly flow beneath the radar.

Hawala, known for its anonymity and reliance on trust over formal records, presents a challenge for financial institutions.

Is Hawala pushing financial organizations to rethink the very basics of their anti-money laundering strategies?

Catch up on this blog to find out the history of the Hawala system, how it works, and how the Hawala banking system finances terrorism and money laundering.

Hawala System In a Nutshell

The word “ Hawala” in Arabic, Hindi, and Urdu stands for “trust”. It refers to the traditional and informal method of money transfer from one location to another.

Originating in the 8th century, hawala served as one of the main forms of transferring money.

Unlike the traditional banking system, the Hawala network is based on trust rather than in-depth records and continuous reporting.

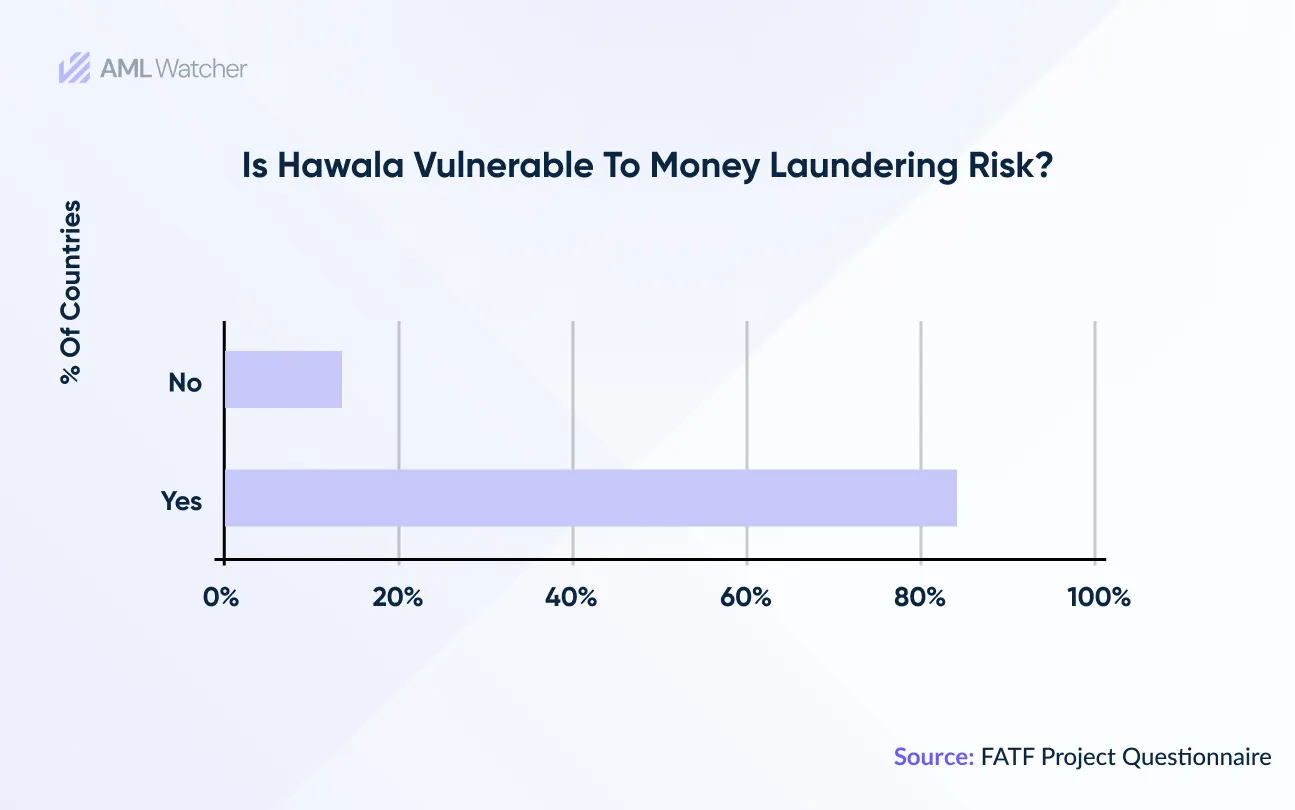

As the famous proverb says, “Where there’s a will, there’s a way”, while it served as an alternative to the formal banking system, it also served as a source to facilitate money laundering as well. As per a 2019 survey, money laundering institutions share $258.9 billion through the Hawala network each year, highlighting the not-so-prominent yet prevalent use of the Hawala network to channel money

Is Hawala Network a Concealed Risk or Potential Advantage?

Unlike common assumptions, there are appealing advantages along with dangers of the hawala network involved.

As a historical and more frequent way of transferring option, especially in underdeveloped countries, it helped to be an alternative form of banking but also paved the way for illicit money transfers and gave rise to chances of money laundering.

Although the majority of the proceedings in Hawala networks are legitimate a small percentage of transactions make the network more prone to money laundering. Its limited recording and less paper trail characteristics bring a lack of due diligence, which makes it easier for criminals to make illicit transactions.

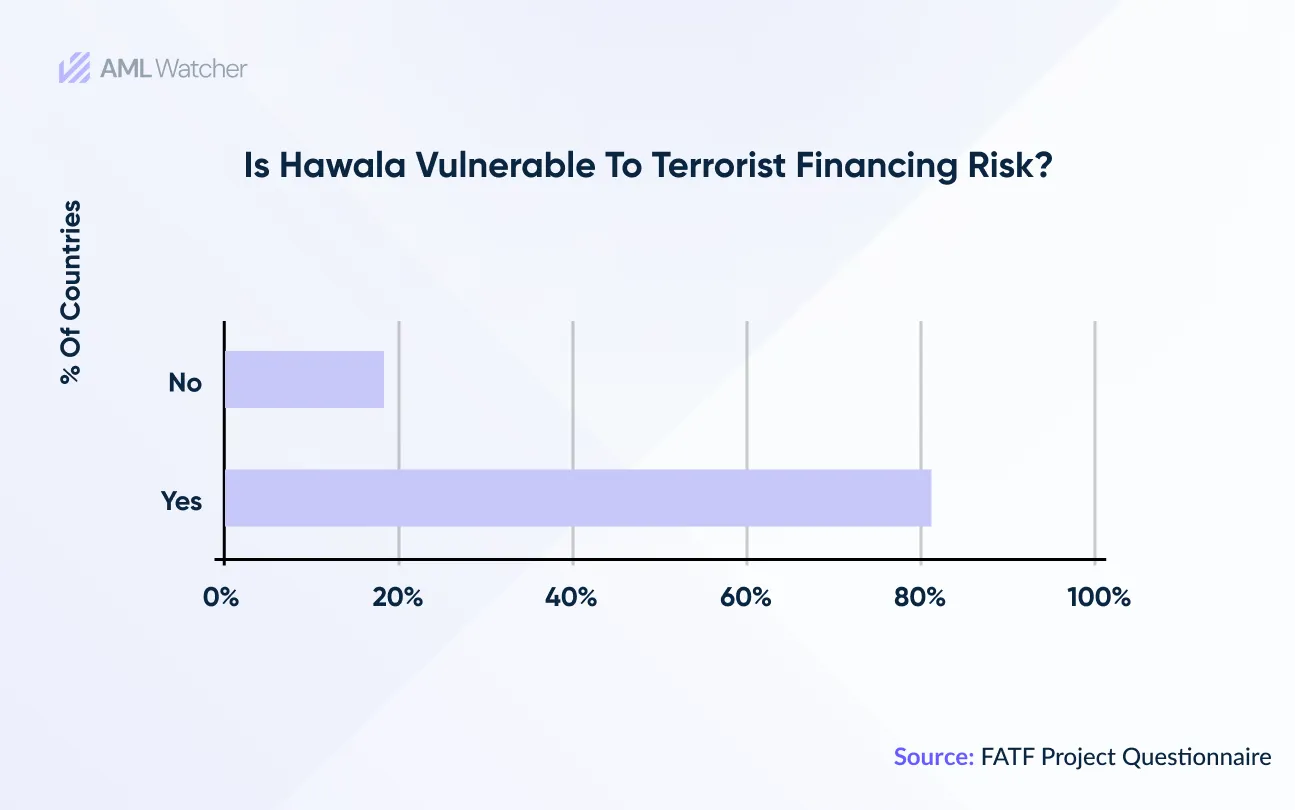

Furthermore, anonymity also makes it easier to exploit the network for money laundering. Major terrorist groups to this date, utilize this network to distribute funds across the network. Al-Qaeda continues to use the Hawala system to transfer funds across the globe.

The United Nations Office on Drugs and Crime estimated that the Taliban collected nearly US$150 million annually in drug profits through taxation schemes and earnings on opium cultivation that were transferred through Hawala.

How Does Hawala Operate In Current Financial Ecosystems?

Notably, after the United States and the United Nations attempted to restrict Iran’s access to the global financial system due to the regime’s insistence on continuing to enrich uranium, the usage of Hawala increased dramatically.

By rerouting traded commodities from Europe, Asia, and the United States through Dubai, hawala networks were able to get under Western sanctions. This made it very difficult to determine which items were headed for the United Arab Emirates instead of Iran.

AML Regulatory Approaches to Hawala

The US Department of Treasury defines Hawala as the Informal Value Transfer System (IVTS), highlighting that Hawala operations are subject to FinCEN regulations.

The USA PATRIOT Act of 2001 mandates that persons involved in non-conventional financial markets such as hawala and hundi are subject to mandatory reporting requirements outlined in the Bank Secrecy Act.

However, different countries react to Hawala differently. Some consider it illegal, while others consider it legal if properly registered or licensed.

Under the protocols required for registration, the service provider has to undergo complete identification, provide certain information, and grant a license to engage in money transfer activities.

In 2002, the UAE Central Bank introduced a registration and reporting system to license and regulate hawala operators in the UAE.

Legitimate Hawala Operational in Dubai

According to circular No. 24 of 2019, any person, including hawala agents or legal entities having a valid residency visa, should register themselves in the Central Bank of UAE (CBUAE), and ensure that hawala brokers are registered and keep a formal record that must align with the Financial Action Task Force (FATF) recommendations on AML/CFT.

In September 2021, the Central Bank of the UAE (CBUAE), Dubai Financial Services Authority (DFSA), and Financial Services Regulatory Authority (FSRA) stated the actual number of registered hawala agencies in UAE is 149, with approximately 95% located in the Mainland. As a result, the mainland jurisdiction has a higher chance of financing money laundering and terrorism.

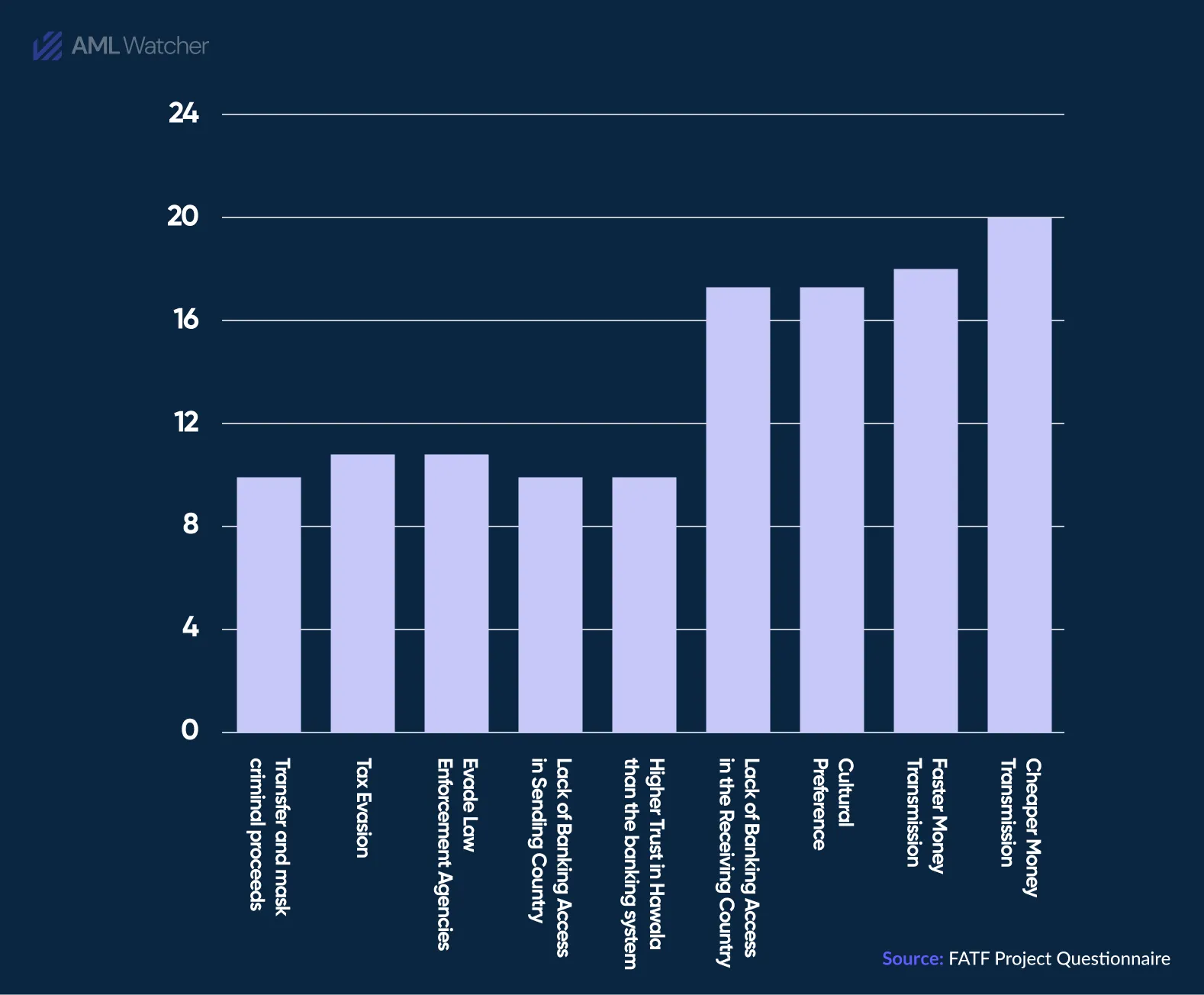

Is Hawala a Good Source for Transferring Money?

There were no banking systems to transfer cash, so people invented the Hawala system because it was convenient, cheaper, and had no tax system. The network is still effective for two reasons:

Cheaper Transaction Fee

Hawala usually charges 25-50% transaction fees, and the total amount depends on the money transfer destination.

The majority of people choose the Hawala option to send money because it has minimal transaction fees and because a hawaladar provides a better transfer rate than any formal financial organization.

Escape Higher Taxes

Hawala brokers usually evade taxes because they are not formally making records or any other financial statements, so it’s impossible to track the origin and destination of financial transactions.

Businesses that don’t want to pay taxes because they are involved in any money laundering usually prefer the hawala network.

You can also get clear insight from the stats mentioned below to understand why people use hawala services to send money.

Hawala Categorized by Illegal and Legal Usage

Financial Action Task Force (FATF) has categorized hawala into the following three types:

Pure Traditional Hawala

Decades ago, people used a money transmission system to transfer money, and this process is used by generations in an unregulated environment.

This system is also used in different countries for personal remittances and trade finance under the supervision of regulatory bodies.

UAE Hawala Facts

In May 2002, the International Conference on Hawala convened in Abu Dhabi, where 300 delegates from 58 countries discussed the UAE’s regulation of the Hawala system. The UAE Central Bank oversees the system to prevent money laundering misconduct.

Pure traditional hawala transfers low-value remittances like migrants in the United Arab Emirates use hawala to send salaries to their hometowns.

With this flow, high-risk individuals have exploited it to do money laundering or terrorism financing.

Hybrid Traditional Hawala

Designated non-financial businesses and professions (DNFBPs) are used to fulfill illegal goals like money laundering or terrorist financing across borders through this system.

They especially use the Hawala networks to evade currency controls, escape taxes, and avoid AML sanctions.

Criminal Hawala

In many countries, criminals are increasingly using Hawala networks for money laundering. Therefore, this poses a high risk of terrorist financing, corruption, tax fraud, and currency offenses.

Criminal hawala services are usually part of vast criminal networks. They don’t want to get exposed, so they work under the umbrella of pure traditional hawala.

How Hawala Creates Risk for Money Laundering?

Hawala’s lack of regulation and informal nature make it attractive to money laundering as Hawala funds transfers are done through cash and don’t leave any trace to identify the original source and funds destination.

Hawala networks usually operate across borders, so it’s challenging for law enforcement agencies to regulate and trace the inflow and outflow of cash.

How Hawala Supports Terrorism Financing?

Usually, terrorist financing is done through hawala because it transfers cash without any formal paper trail, and its informal nature makes it complicated to regulate its use.

A Practical Pathway To Addressing Money Laundering Risks

Institutions engaging with legal Hawala networks face significant AML compliance risks due to the system’s anonymity and strict regulatory monitoring. Failure to meet AML requirements in these networks can lead to serious fines and reputational damage.

AML Watcher offers a comprehensive AML screening solution to ensure these institutions stay ahead, maintaining AML compliance, and establishing confidence in each business activity.

How?

-

Through Global Database Coverage

Screens clients across 235 countries and over 100,000 data sources, and ensures complete AML compliance in the areas where Hawala networks may operate.

-

Sharing Real-Time PEP & Sanction Screening

AML Watcher continuously monitors PEPs and sanctions lists to make sure that your institution deals with any Hawala operators and high-risk associates following international AML regulations.

-

Via Negative Media Coverage

Detect high-risk individuals through negative media alerts, highlighting possible illegal activity connected to any potential Hawala operators.

-

Providing Personalized Risk Assessment

When working with high-risk individuals belonging to Hawala networks, assign risk levels tailored to your specific business needs to ensure complete AML regulatory compliance.

-

Supporting Multi-Language coverages

Covers 80+ languages, allowing for thorough AML screening across linguistic obstacles that are frequently encountered when dealing with any fund transfer activity from another region.

-

Via Enhanced Screening in High-Risk Zones

Provides AML data coverage from conflict zones and high-risk jurisdictions, and helps reduce exposure to financial crime when working with fund exchange networks.

- No commitment needed

- Complete AML Database at your service

- Access our all-in-one dashboard

Tier-2 PSPs in ... must demonstrate automated monitoring, layered CDD, &...

See the Full Regulatory Expectation70–80% less manual work, 95% less fatigue, TruRisk Agent makes compliance effortless.

Experience Agentic AMLMove Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries