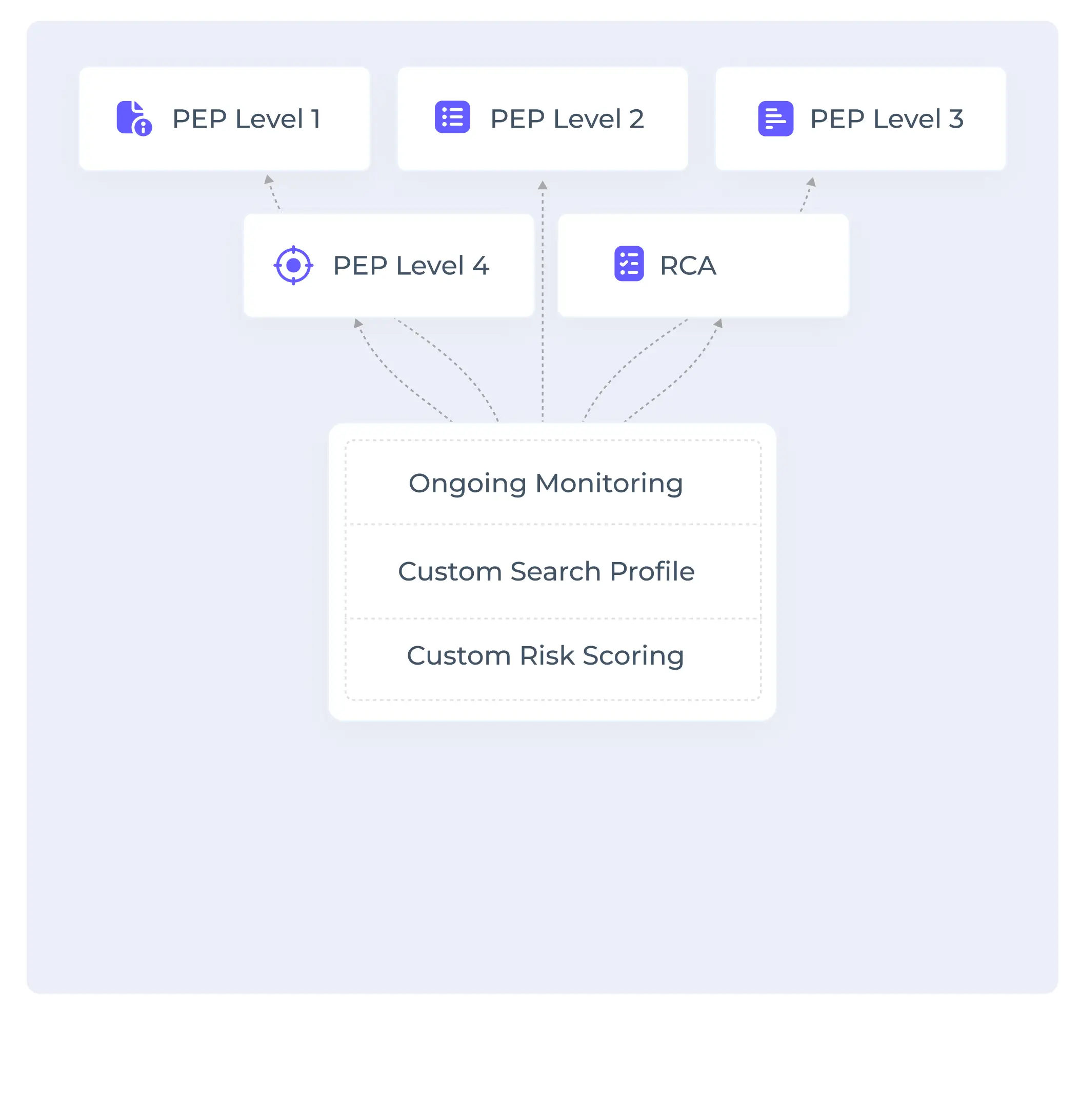

PEP Screening software for Local, Foreign, RCAs and AKAs

Screen foreign and domestic PEPs from anywhere in the world using our 100,000+ data sources with the exclusive availability of ‘PEP Level 4’ screening.

Book Free Demo

PEP Dashboard

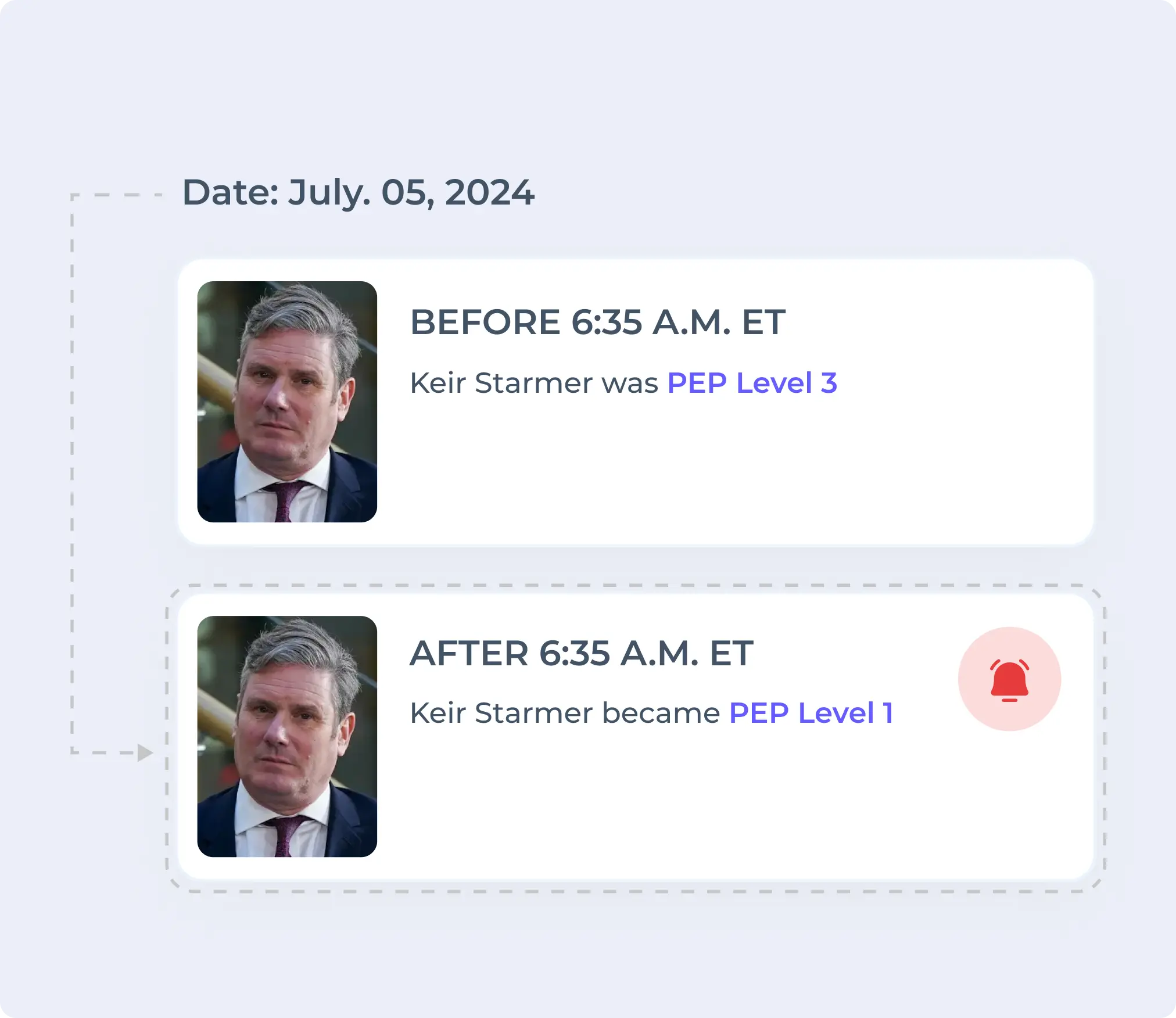

Access Recent updates on PEPs and their RCAs

From the majestic mountains of Patagonia to the serene shores of Sydney, track changes in PEPs from every corner of the globe with just one click. Visit Us weekly to see all latest changes in PEP statuses.

Sahil Babayev is appointed as finance minister of Azerbaijan.

The House of Representatives votes to impeach Vice President Sara Duterte (215 of 306 votes) in Philippines.

The government of Prime Minister François Bayrou survives two no-confidence motions in france.

Doug Burgum is sworn in as secretary of the interior of United States.

Sheikh Abdullah Ali Abdullah Al Salem Al Sabah is appointed and sworn in as Kuwait’s defense minister.

Doug Burgum is sworn in as secretary of the interior of United States.

PEP Dashboard

Access Recent updates on PEPs and their RCAs

From the majestic mountains of Patagonia to the serene shores of Sydney, track changes in PEPs from every corner of the globe with just one click. Visit Us weekly to see all latest changes in PEP statuses.

The government of President Louis Mapou collapses as the Caledonia Together party withdraws. (New Caledonia)

The appointment of Pak Thae Song as premier is announced(North Korea).

Former governor of Rio Grande do Sul (1991-95) Alceu de Deus Collares dies(Brazil).

In the first round of presidential elections, incumbent Zoran Milanovic wins 49.7% of the vote(Croatia)

Grand Duke Henri announces he will abdicate on Oct. 3, 2025. (Luxembourg)

Former prime minister (2004-14) and foreign minister (2005-06) Manmohan Singh dies. (India)

The government of President Louis Mapou collapses as the Caledonia Together party withdraws. (New Caledonia)

Former chairman of the National Military Council (1980-88) and president (2010-20), Desi Bouterse dies(Suriname)

What Makes Us Stand Out

We cover all PEP list even the local ones

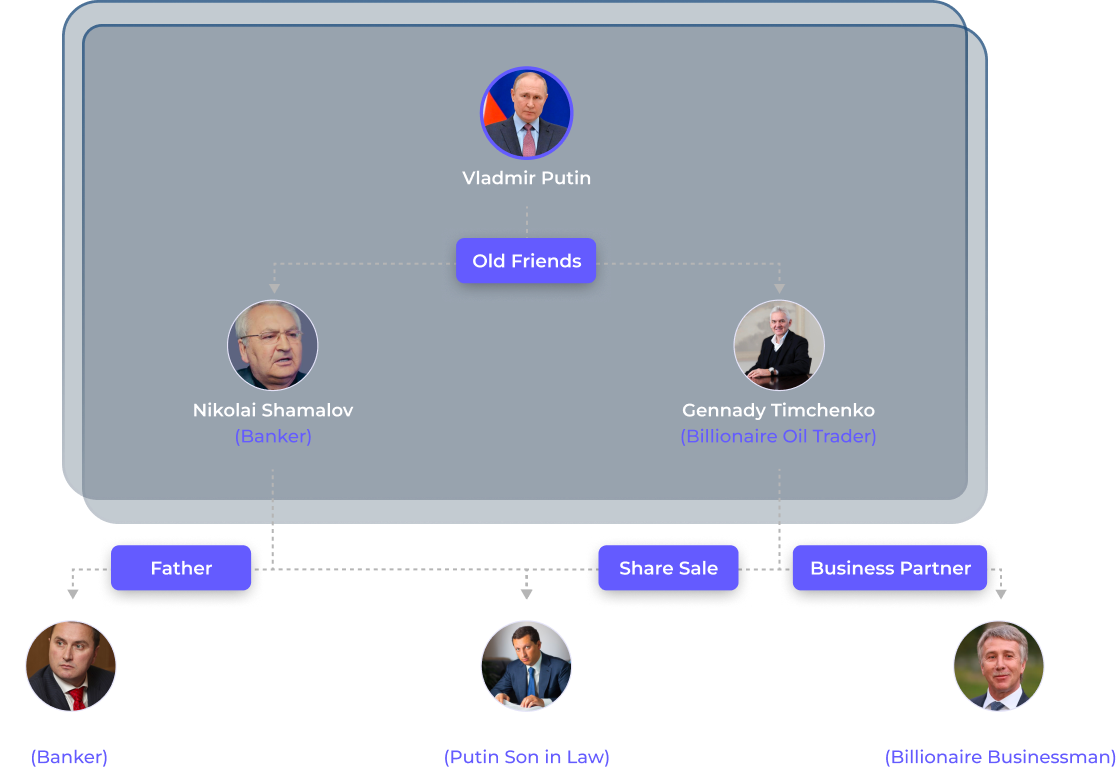

AML Watcher’s PEP Screening checks for politically exposed persons, their family members and close associates, aligning with both domestic and international regulatory standards.

Screen ‘Level 4’ PEPs, Exclusive To AML Watcher

Unifying All PEP Definitions Into A Single Framework For Fewer False Negatives.

Access PEP Lists Of Even Those Territories That Legacy AML Vendors Miss

Get Updates of Changes In PEPs Status In Seconds

Automated PEP Screening With 95% Fewer False Positives - Powered by TruRisk

TruRisk

Find true positives faster and automate your screening. Focus on reviewing cases instead of matching names. Get instant, intelligent PEP analysis with real-time risk assessment, phonetic matching, and automated compliance reasoning.

Experience Our Impact

Better PEP Data, 44% Fewer False Positives.

- Get AML data enriched with DOBs, Nationalities, RCAs, and more for more precise results.

- Get access to 6M+ PEP Profiles which is 20% more coverage than legacy AML data providers.

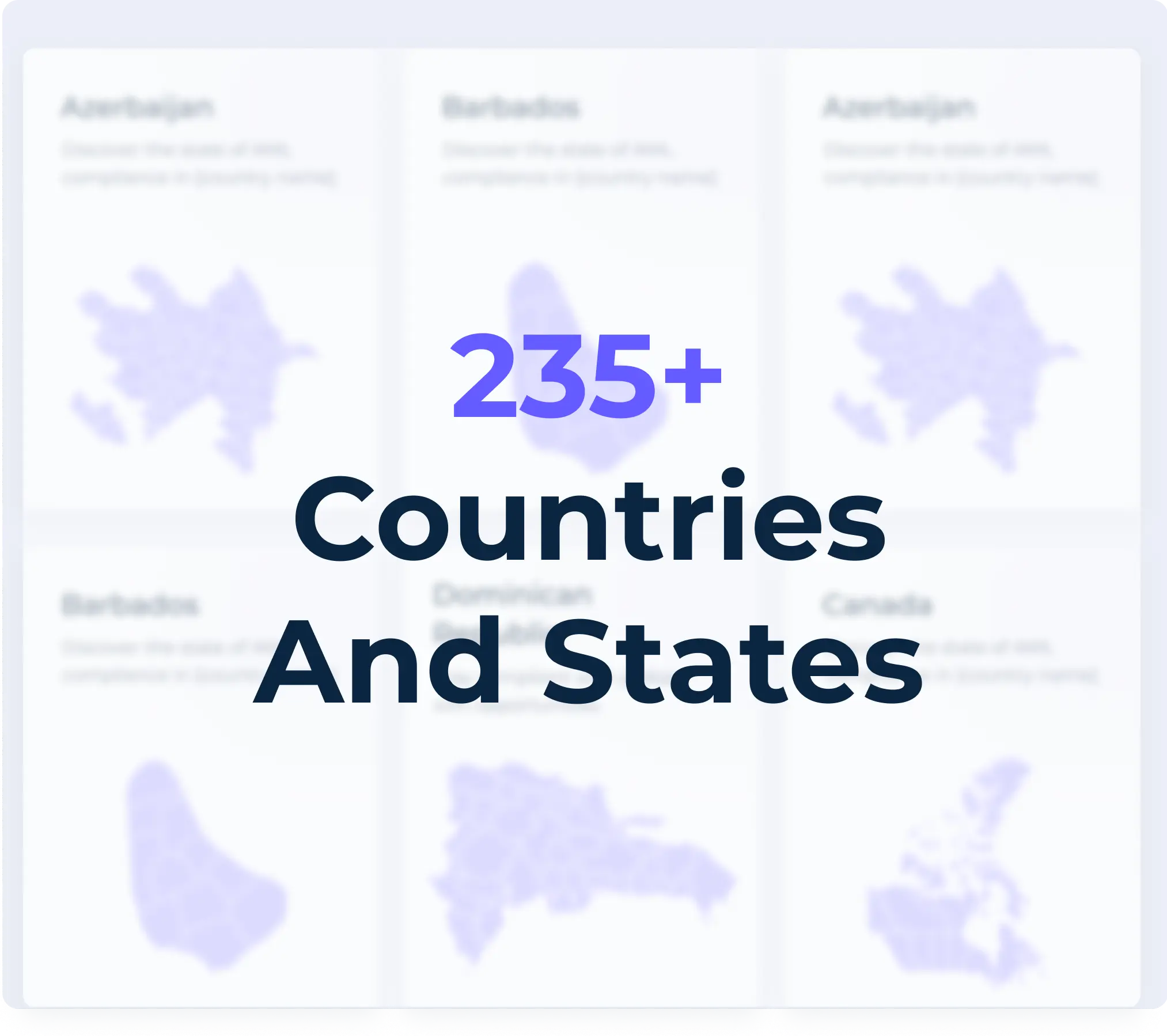

- Reduce your false negatives by 15% by utilizing a definition unification approach to apply across 235 countries and states.

Why AML Watcher

Why AML Watcher's PEP Screening Solutions Are the Perfect Fit

-

You get access to data for local and domestic level PEPs with Level 4 screening.

-

You get access to all close associates and relatives of the PEPs with all their current or past aliases.

-

You get real-time notifications and updates about changes in PEP levels.

-

You get automated detailed reporting saving your documentation costs.

-

You can screen PEPs using unique identifiers.

Where We Help?

Risk Based Approach made easy with AML Watcher’s PEP List Screening

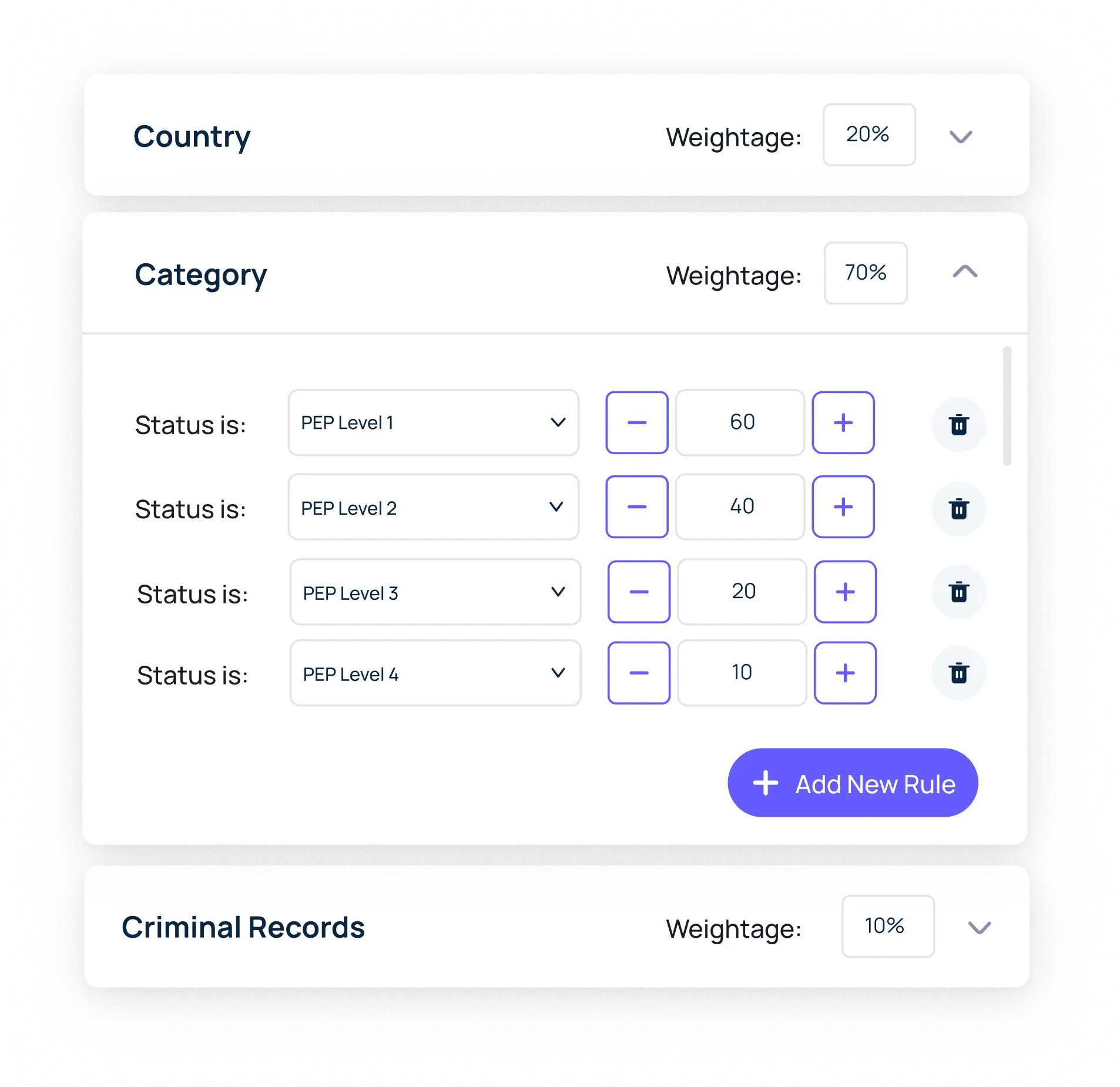

Custom Risk Scoring

Impactful risk assessment to efficiently manage a vast portfolio of PEP profiles.

Learn more

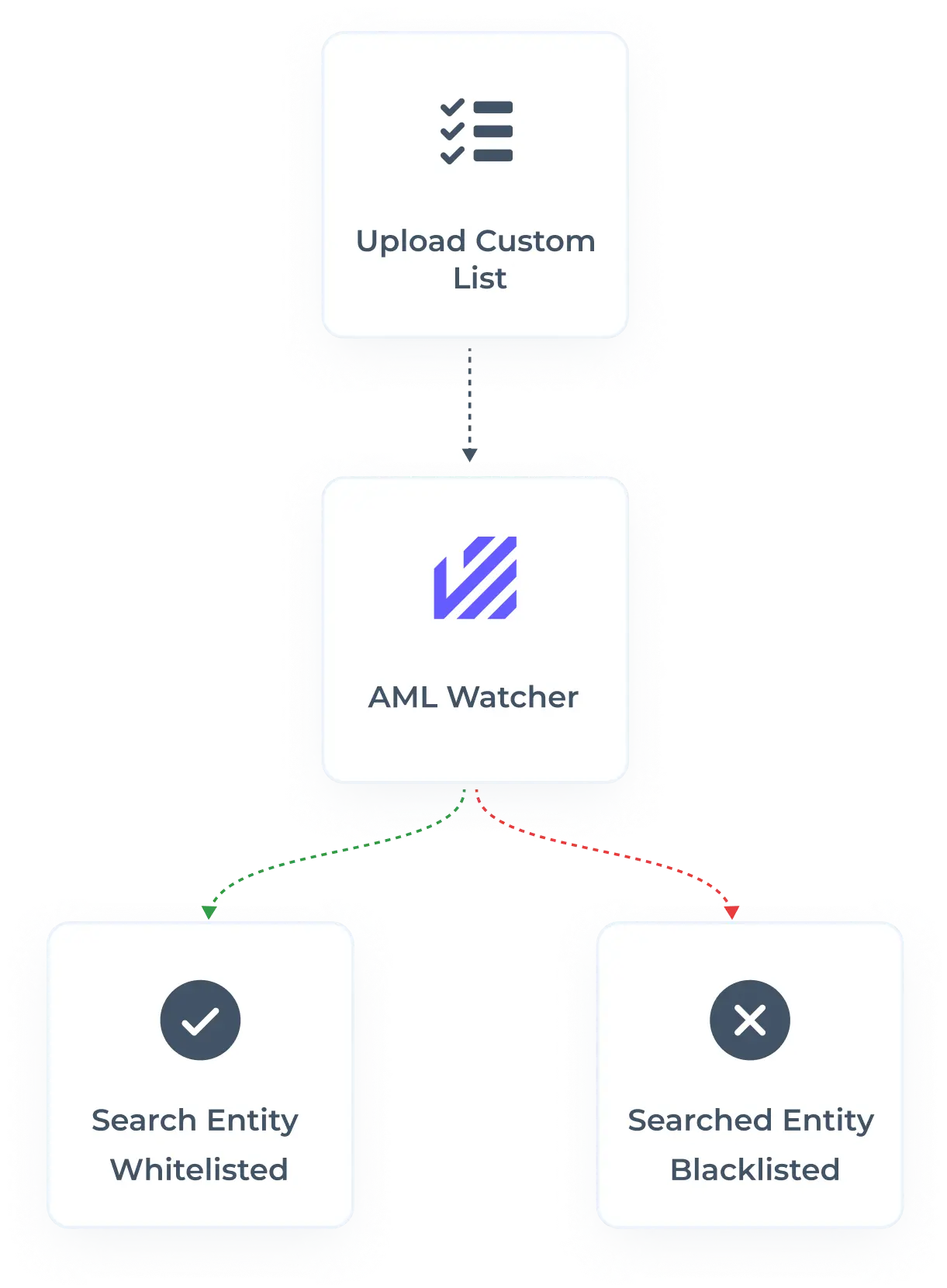

Custom Whitelisting/Blacklisting

Pick and choose the people that you want to do business

with.

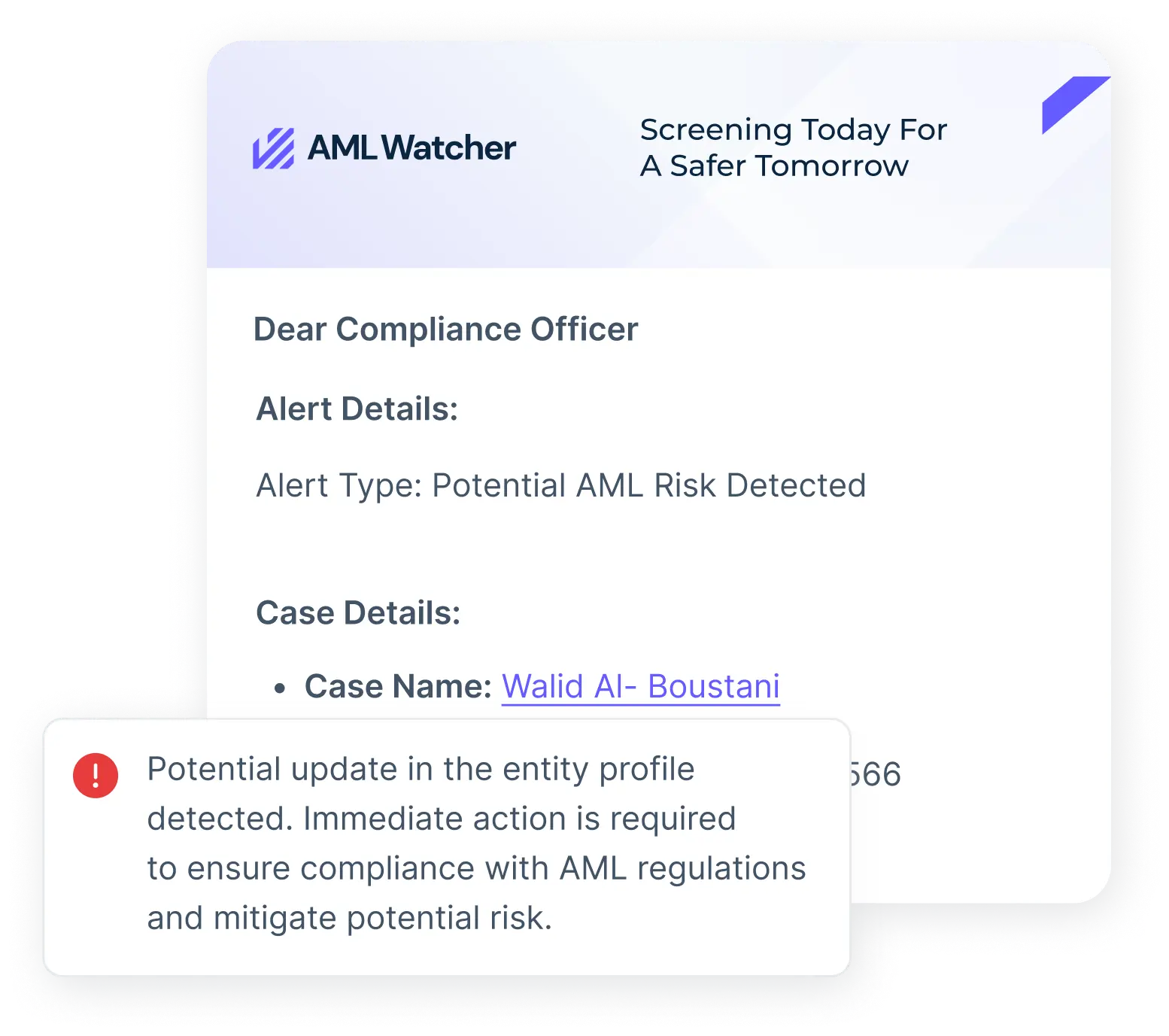

Ongoing Monitoring

Ensure real-time detection of changes in PEP levels with every major event.

Learn more

How we make politically exposed person screening Precise

We have the biggest PEP directory

We have 100,000+ data sources of not only PEPs but their relatives and close associates as well

We keep an eye on everything

Every major event, any elections, or power shift, we cover it all.

We monitor your cases closely

We know you’re busy. That is why we monitor and alert you on the slightest of changes in case PEP status.

We provide custom-fit solutions.

We understand that your needs are unique, so we give solutions that are unique to you.

When someone is designated as a PEP, the classification depends on their immunity. As long as they hold privileges such as immunity at checkpoints, they remain classified as a PEP. Once those privileges are removed, the classification no longer applies.

Learn More About PEP Screening

One stop guide to PEP checks

What does “Good AML Data” mean for AML Watcher?

Your AML screening solution is as promising as the weakest link in your data chain.

Download

Publications

While working with PEPs is often a necessary part of doing business, why is it crucial to screen them? How do you navigate the complexities of PEP screening? And how you overcome the notorious “false positives” challenge?

Learn More

Blogs

What role does PEP screening play in strengthening your AML defences? How can businesses strike the right balance between thoroughness and efficiency? And what new tools are reshaping how we handle this critical task? Find out in our latest blogs.