Why is AML in FinTech Crucial For the Sector’s Growth?

Sanctions

March 21, 2025

“FinTech’s rapid expansion is significantly outpacing conventional banking sectors. Between 2023 and 2028, fintech revenues are expected to grow almost three times faster than those of traditional banks.”

Fintech is an umbrella term because it involves a wide range of technological and financial services, including but not limited to

- Lending

- Banking

- Wealth Management

- Payments

- Insurance

It caters to all businesses that use technologies and automated services to provide digital finance-based services to their clients. To implement AML Compliance strategies and strengthen AML in FinTech, financial businesses must consider several factors, which can include:

- Typologies of services being offered

- Jurisdiction of Operations

- Nature of technology

- Size of Customer Base

AML Compliance for FinTech- What Are Challenges?

According to the Financial Action Task Force FATF Guidance “Opportunities and challenges of new technologies for AML/CFT”, financial technologies can pose certain risks related to money laundering and terrorist financing.

Despite their inventiveness, FinTech businesses still need to adhere to stringent AML or sanctions compliance guidelines. Meanwhile, they are expected to maintain operational effectiveness and enhance user experience. Some of the crucial challenges include:

Varied FinTech Ecosystem

-

Buy Now, Pay Later (BNPL)

Within BNPL, people can purchase things and pay later. Unlike traditional lending, BNPL providers do not directly lend money to clients but rather facilitate structured payment plans.

However, due to minimal upfront verification and lax identity checks, criminals and money launderers can exploit these platforms to layer and hide their illegal money. Therefore, strengthening AML measures is crucial for mitigating these risks.

-

Crypto Wallets

Crypto wallets, especially self-managed ones, face numerous challenges because they don’t always verify client identities. Even when they do, they do not perform extra checks and balances on them.

Additionally, the client has complete authority; with no third-party involvement. This makes it difficult for the regulators to track suspicious transactions.

-

Neobanks and Digital-Only Banks

Neobanks and Digital-Only Banks perform all the actions digitally, which means they do not have a physical presence. While their digital-first approach enhances convenience, it also introduces risks related to involvement with illicit entities and fraud. Additionally, fewer checks make the sector more vulnerable to imposters.

However, many of these institutions are subject to the same AML regulations as traditional banks, requiring compliance with KYC (Know Your Customer) and transaction monitoring standards.

Despite these regulatory measures, the rapid onboarding processes and lack of in-person verifications increase their vulnerability to imposters and illicit entities. Strengthening AML frameworks and implementing AI-driven compliance solutions are crucial for mitigating these risks.

-

Credit and Peer-to-Peer Lending

Compared to conventional payment providers, P2P lending platforms offer alternative ways of getting loans. However, these transactions are done in real time, often neglecting the verification of clients. These lending platforms mostly end up getting massive penalties in terms of getting involved with illegal entities.

High Cost of Compliance Failures

FinTech businesses experience huge penalties for not implementing the advanced AML measures and adhering to the evolved standards. Some of the major fine examples are:

Payoneer

Payoneer was penalized by OFAC for failing to prevent transactions linked to sanctioned countries and individuals. The company’s weak screening system allowed over 2,200 restricted payments, violating U.S. sanctions. As a result, Payoneer agreed to pay $1.39 million to settle the case.

Klarna Bank

Klarna Bank has been hit with a hefty fine of $46 million for breaches in FinTech compliance regulations. These imposed fines highlight the significance of FinTech AML compliance.

Binance

In November 2023, Binance, the world’s leading cryptocurrency exchange, violated the AML laws because it got involved with unlicensed money transfers along with sanctions violations in the US. As a result of these violations, they had to pay $4 billion as a penalty.

Revolut Bank

The Bank of Lithuania imposed a fine of €200,000 on Revolut Bank because it violated the FinTech AML standards. The bank took the incident seriously, investigated internal issues, adhered to legal standards, and integrated AI-driven solutions.

The case of Revolut is a testament to how AML in FinTech is crucial for the further growth prospects of the business.

Starling Bank

In October 2024, the United Kingdom’s Financial Conduct Authority imposed a £29 million fine on Starling Bank for insufficient fincrime controls. The bank has to pay a double penalty, one financial and the other reputational.

The bank’s failure stemmed from prioritizing transaction speed while overlooking proper AML screening measures, leading to gaps in monitoring suspicious activity. Consequently, Starling Bank suffered both financially and reputationally, highlighting the importance of robust compliance measures alongside operational efficiency.

Balancing Transaction Speed with Compliance

Balancing transaction speed while adhering to AML Compliance in FinTech is one of the most challenging things a financial business experiences in the status quo. One of the major examples of failure to balance transaction speed with compliance is the penalty imposed on Starling Bank.

The case of Starling Bank mentioned above underscores how FinTech businesses must integrate AI-driven AML solutions to ensure real-time risk assessments without compromising transaction speed.

FinTech firms can prevent regulatory fines, safeguard reputations, and enhance trust within the financial ecosystem, by implementing advanced compliance frameworks.

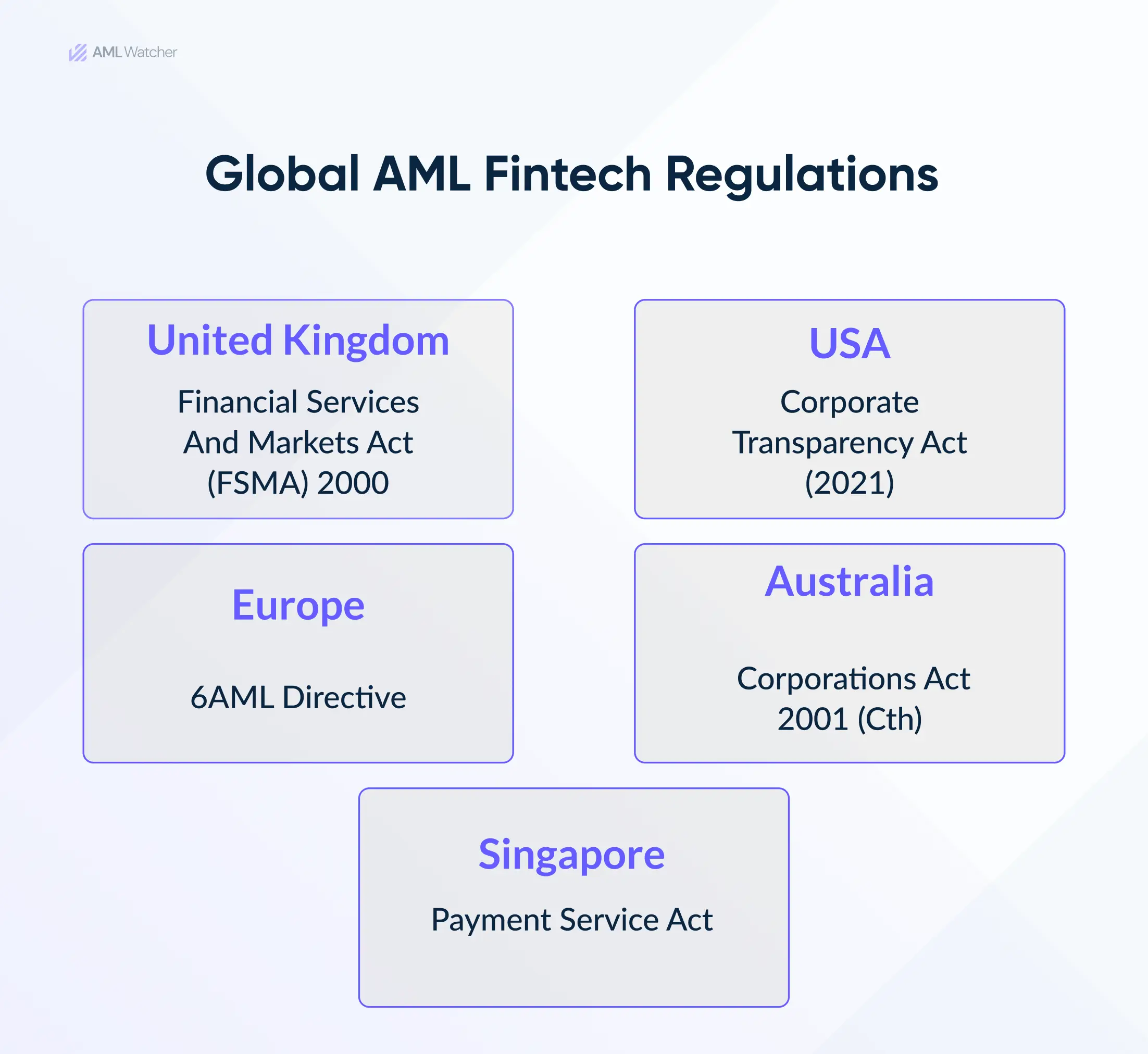

Regulations Governing AML Compliance in the FinTech Sector

AML for FinTech is a regulatory requirement, and as new financial technologies emerge, it faces more scrutiny from regulatory bodies and financial watchdogs. For example, FATF 15 Recommendations offers a comprehensive framework to fight terrorist financing and money laundering.

AML Compliance- A Necessity for Growth of the FinTech Sector

FinTechs seeking further growth opportunities such as filing for IPO or obtaining a Banking License or IPOs, must demonstrate strict compliance with global and jurisdiction-specific AML regulations.

Revolut faced regulatory scrutiny while expanding its banking services, addressing accounting issues, EU regulatory breaches, and reputational concerns, including an aggressive corporate culture.

The UK’s Financial Conduct Authority investigated its AML checks in 2016, closing the case in 2017. Now, Revolut continues to expand its financial services, from mobile payments to cryptocurrency trading.

Similarly, Klarna, which already holds a Swedish banking license, has filed for an IPO. As it expands its global “Buy Now, Pay Later” services, it must ensure compliance with AML laws across multiple jurisdictions, including the EU, UK, and US. Strengthening its AML procedures is crucial for regulatory approval, investor confidence, and long-term growth.

Customer Risk Assessment for FinTechs

FinTechs should ensure that they have adequate resources available at their disposal to conduct due diligence, ensuring compliance with AML regulations. After setting the clear AML and Sanctions compliance program, they should evaluate their Anti Money Laundering screening tools on the basis of their scope of operations, risk exposure, and jurisdictions in which they operate.

Global Coverage

To comply with the risk-based approach to anti-money laundering, the obligated sector must ensure accurate initial risk assessments. For this purpose, FinTechs should ensure that the AML screening solution they use has AML screening data that is relevant to the scope of operations and must offer data of high-risk entities in line with global and jurisdiction-specific AML regulations.

Adverse Media Screening

FinTech businesses must implement adverse media screening to ascertain the risk of the customer being associated with any predicate offense and high-risk criminal activity such as human trafficking, child abuse, murder, and terrorism, to name a few. This will save them from non-compliance risks that may arise for not being able to flag suspicious activity.

Sanctions and Watchlist Screening

Like banks, FinTechs are also obliged to conduct sanctions and watchlist screenings in line with FATF recommendations and according to the regulatory authority’s jurisdiction in which they operate. e.g, OFAC in the United States, DFAT in Australia, OFSI in the UK.

PEP Screening

FinTech businesses mostly deal with international clients; therefore, there is a higher chance of being exposed to politically exposed persons (PEPs). Those operating globally must have access to the PEP screening database with global coverage

Immediate Risk Mitigation

Real-time alerts indicating the updated risk status of their clients enable FinTech companies to take instant action, such as freezing accounts, stopping transactions, or flagging suspicious activity. This prevents unauthorized financial dealings with sanctioned and other high-risk entities.

Stay Compliant with AML Watcher

The rapid expansion of the FinTech sector and its diverse services demands that the industry enhance its AML compliance. Stay ahead of the curve by proactively preventing FinTech financial crime and avoiding hefty penalties. With AML Watcher, FinTech businesses can get:

- AML Watcher has 415+ risk categories.

- AML Watcher has more than 3500 criminal watchlists.

- Data of sanctions for more than 215 jurisdictions.

- Global coverage of PEPs in line with laws of jurisdiction.

- Real-time monitoring for continuous compliance.

Move Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries