Ultimate Guide to AML Risk Assessment in High-Risk B2B Payments

AML Compliance

March 26, 2025

Over the past two decades, technology has revolutionized almost every aspect of our lives, and the payments sector is no exception. It allowed the movement of funds around the globe in seconds, transforming the way we’ve been banking in the past.

This transformation is particularly evident in business-to-business (B2B) payments as companies increasingly adopt digital-first solutions. Once reliant on fax machines and telephone banking for some sort of autonomy, businesses are rapidly embracing advanced digital solutions, driving the B2B payments market size to over $1.1 trillion as of 2023.

However, as technology evolves, so do the moves of criminals.

The United Nations estimated the scale of money laundering to be 2–5% of the global economy, which means a staggering $2 to $5 trillion in estimated illicit funds in 2023—highlighting the growing challenge of financial crime.

We know that B2B transactions often involve the cross-border movement of large sums or large volumes for complex business structures.

These factors make B2B payments inherently vulnerable to risks of money laundering. This vulnerability requires a strong, risk-based Anti-Money Laundering (AML) strategy to effectively mitigate these risks and ensure compliance with ever-changing regulations.

Let’s explore this article to get in-depth knowledge on AML risk assessment in B2B payments, the risk factors to monitor, the challenges to overcome, and some future trends to follow.

Why do B2B payments need AML risk assessment?

B2B transactions are inherently different from consumer payments. In many cases, these transactions involve high-value payments, multiple parties, complex corporate structures, and opaque beneficial owner information.

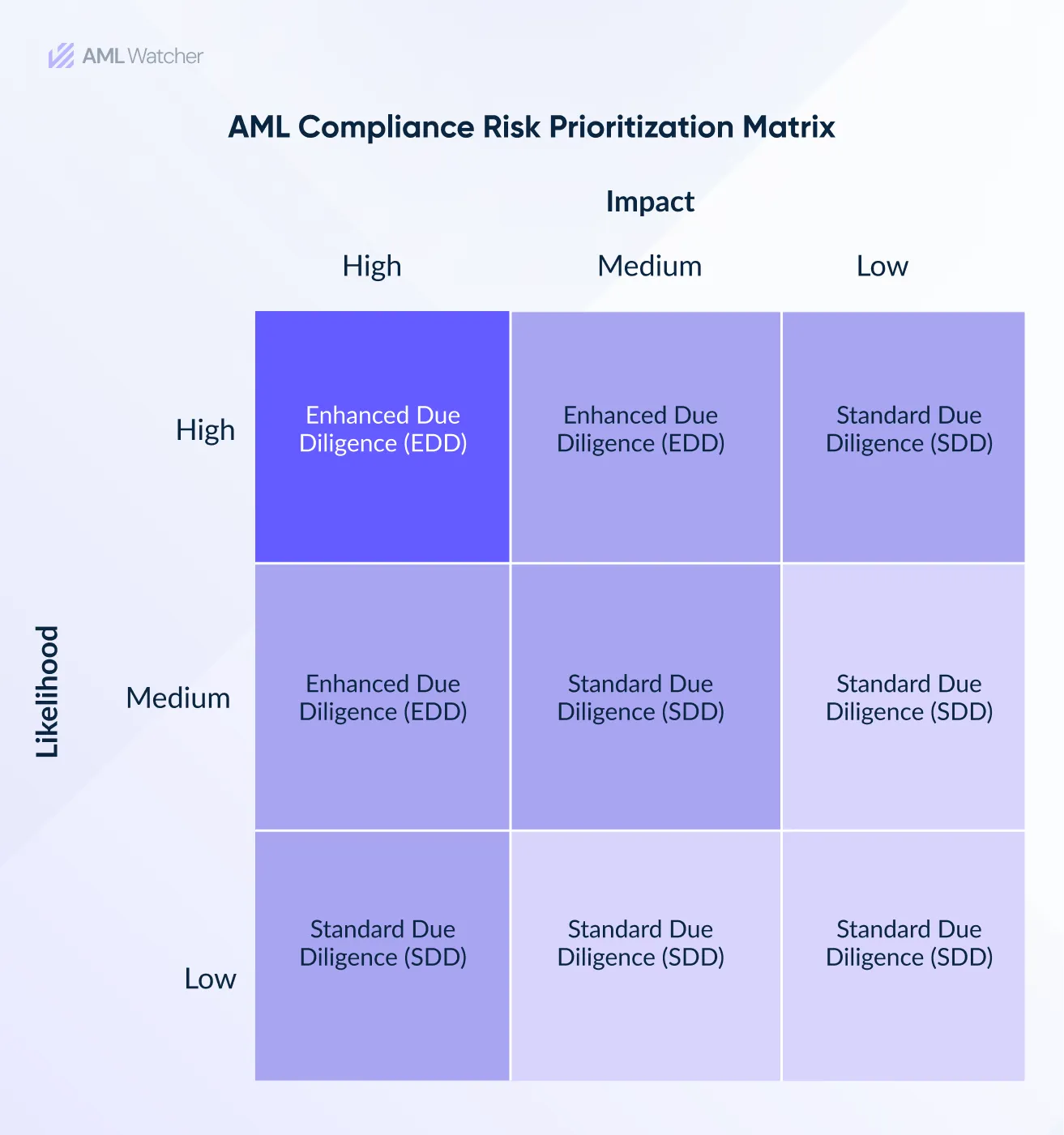

Such complexity makes it challenging to pinpoint illicit activities amid legitimate business flows. Most regulators across the globe mandate a risk-based approach to AML compliance. Failure to do so may result in serious fines or reputational damages.

The goal is to ensure that businesses focus their efforts on segments with the highest risk rather than applying a one-size-fits-all model.

This further entails that a payment processor must be capable of distinguishing between low-risk, routine B2B payments from high-risk transactions.

But how do businesses make this distinction? The answer lies in a comprehensive risk assessment framework.

In a nutshell, an AML risk assessment framework involves identifying and prioritizing risks based on their likelihood and impact and then implementing proportionate controls to mitigate the identified risks.

Consequences of Delayed Risk Assessments

In January 2025, Block Inc., formerly known as Square, the parent company of Cash App, reached a multi-state settlement to pay an $80 million penalty to 48 US state financial regulators for violations of BSA/AML regulations on its Cash App platform.

In another case, in 2015, a global payment processor, PayPal, was fined by the US Treasury Department for $7.7 million for violating sanctions against Iran, Cuba, and Sudan.

Risk Assessment in B2B Payments

In the following section, we’ll discuss some key factors from the perspective of a high-risk B2B payment, which should be, at minimum, part of a risk identification process.

Key Factors in a High-Risk B2B Payment

Geographic Risk

These risks emanate from the locations where a business operates or offers its services and the destination or origin of the funds.

The following are considered to be indicators of a high geographic risk:

- Jurisdictions subject to UN, EU, or other international Sanctions

- Jurisdictions known to have weak AML/CFT controls or supervision, also known as countries on FATF blacklist and grey lists

- Countries or regions known to have support of terrorist activities/funding and regions with known operational terrorist organizations, through independent credible sources

- Countries are known to have high corruption or other crime scores as reported by credible independent sources like the Corruption Perception Index of Transparency International

Customer Risk

These risks emerge from the type or behavior of the customers a business will be dealing with or offering their services to.

The following are some indicators of a high risk if the customer is:

- A company with nominee directors or bearer shareholders

- A politically exposed person (PEP), a family member, or a close associate of PEP, especially when these individuals act as beneficiaries of a business

- A cash-intensive business (e.g., by filling non-existing revenues with illicit funds)

- Reluctant to provide details during the due diligence process

- A person with publicly available negative news or adverse media about their involvement or links to criminal activities.

Product or Service Risk

These risks originate from how these products or services are designed to attract new customers in an effort to gain a competitive advantage.

The following are indicators of high-risk products or services:

- Offer transactions with large or no limits with global reach

- Promote enhanced anonymity like private banking

- Involve new technologies, like virtual currencies

Distribution Channel Risk

The way these products or services reach the customers has its own risks and opportunities.

The following are some indicators of increased risks in delivery channels:

- Dealing with customers without their physical presence, for example, customers using an agent or lawyer to conduct business on their behalf

- Remote and internet-based customer onboarding.

- Products/services offered through the use of intermediaries or agents

AML risks evolve with business growth and regulatory changes. Money laundering risk assessment should be reviewed on a periodic basis or as a business expands into new markets, adopts new technologies, or offers new products.

A comprehensive AML assessment does not merely discharge regulatory duty; it provides a competitive advantage. Firms with comprehensive AML processes protect their reputation, secure potential partnerships driving growth, and avoid regulatory fines.

Furthermore, effective Anti-money laundering risk assessment enables organizations to optimize resource allocation by targeting areas with the highest potential risk.

We’ve explored the key risk factors in B2B payments; now, let’s look at the challenges that can hinder the efficiency of B2B transaction processes.

Unique Challenges in High-Risk B2B Payments

Layered Beneficial Ownership

Complex corporate structures, such as offshore entities or trusts, can obscure true ownership. Compliance teams must dig deeper using public registries and third-party databases.

Evolving Sanctions Landscape

B2B payments are particularly vulnerable to the risk of changing the sanctions landscape due to global geopolitical issues. B2B payments often involve multiple intermediaries across diverse jurisdictions; due to this risk of transacting with restricted entities or individuals is higher than ever.

Cross-Border Transactions

Differing AML standards across jurisdictions complicate compliance. For example, a payment routed through a country with insufficient due diligence regulations may require additional checks.

High Transaction Volumes

Automated monitoring systems are essential to handle large-scale B2B transactions without compromising accuracy.

Balancing Compliance and Convenience

Manual and legacy compliance methods may delay payments and onboarding processes, frustrating clients and resulting in bad customer experiences. AML solutions supporting automation and risk-based solutions can expedite transactions, improve customer experience, and safeguard from regulatory violations.

Future Trends in AML Risk Assessment of B2B Payments

RegTech Solutions

RegTech solutions merge machine learning, real-time databases, and biometrics to create a holistic compliance ecosystem that automates risk assessment, sanctions screening, and transaction monitoring.

Scrutiny of Crypto Transactions

As B2B crypto payments rise, regulators are tightening requirements for virtual currencies, such as crypto travel rule obligations. Businesses are increasingly shifting to crypto wallet screening and risk assessment tools to maintain compliance amidst growing supervision of the crypto industry.

These tools can uncover nexus with sanctioned entities and criminal actors involved in a B2B crypto payment by leveraging screening, blockchain analytics, and adverse media checks.

ESG Integration

Environmental, social, and governance factors are increasingly linked to AML risks, such as corruption in resource-rich regions. To ensure compliance, businesses need access to an AML solution provider with an extensive database of regulatory enforcements and warnings issued for ESG compliance violations in the supply chain.

In high-risk B2B payments, AML risk management is not a one-time exercise but a dynamic process requiring vigilance, adaptability, and technological innovation.

Organizations can protect themselves and contribute to global efforts against financial crime by embedding a risk-based culture and staying ahead of regulatory shifts.

AML Watcher Empowers B2B Payment Processors with Global AML Compliance

Stay ahead of financial crime with AML Watcher. AML Watcher empowers B2B payment processors with a global footprint to manage AML risks.

With key features like advanced sanctions and PEP screening, customizable risk scoring, and transaction monitoring, we help businesses process payments across borders without the risk of non-compliance.

Our tailored risk assessments focus on high-risk transactions, ensuring that compliance is maintained without hindering business growth or operations.

Cut your compliance costs up to 50% and get access to our real-time, updated, proprietary database of:

- 415+ risk categories

- 3500+ criminal watchlists

- 215+ Sanction Regimes

- 2.6 Million PEP Profiles from over 235 jurisdictions

Discover how your business can automate the screening and monitoring of high-risk B2B payments with AML Watcher to simplify AML compliance.

- No commitment needed

- Complete AML Database at your service

- Access our all-in-one dashboard

Tier-2 PSPs in ... must demonstrate automated monitoring, layered CDD, &...

See the Full Regulatory Expectation70–80% less manual work, 95% less fatigue, TruRisk Agent makes compliance effortless.

Experience Agentic AMLMove Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries