AML Compliance For Neobanks – Balance Speed with Security in the Fintech Sector

AML Compliance

April 30, 2025

- Rise of Neobanks and the Associated AML Screening Challenges

- Speed Vs. Security – The Need to Balance Fundamental Trade-Off

- How to Balance Speed with AML Compliance?

- Challenges Faced by Neobanks due to AML Non-Compliance

- Restrictions on Robinhood Crypto by the New York State Department of Financial Services (NYDFS)

- Using Ongoing Monitoring to Get Accurate Changes in Customer Risk Profiles

- Speed and AML Compliance- A Framework for Neobanks

- Partner AML Watcher For Better Compliance

Adhering to the worldwide guidelines of the Financial Action Task Force (FATF), assisting neobanks to enhance their compliance while offering instant and online banking services.

According to Statista, Neobanks are expected to experience market growth from approximately $4.96 trillion in 2023 to around $10.44 trillion by 2028, with a CAGR of 13.15%.

These statistics demonstrate the growing demand for instant and more streamlined banking solutions. Just like other financial institutions, Neobanks are also obligated to follow Anti-Money Laundering regulations.

However, AML Compliance in neobanks is a bit challenging because of the digital nature of the services offered by them.

In pursuit of quickly offering financial services to their clients, Neobanks often face the challenge of servicing a higher volume of customers while ensuring compliance.

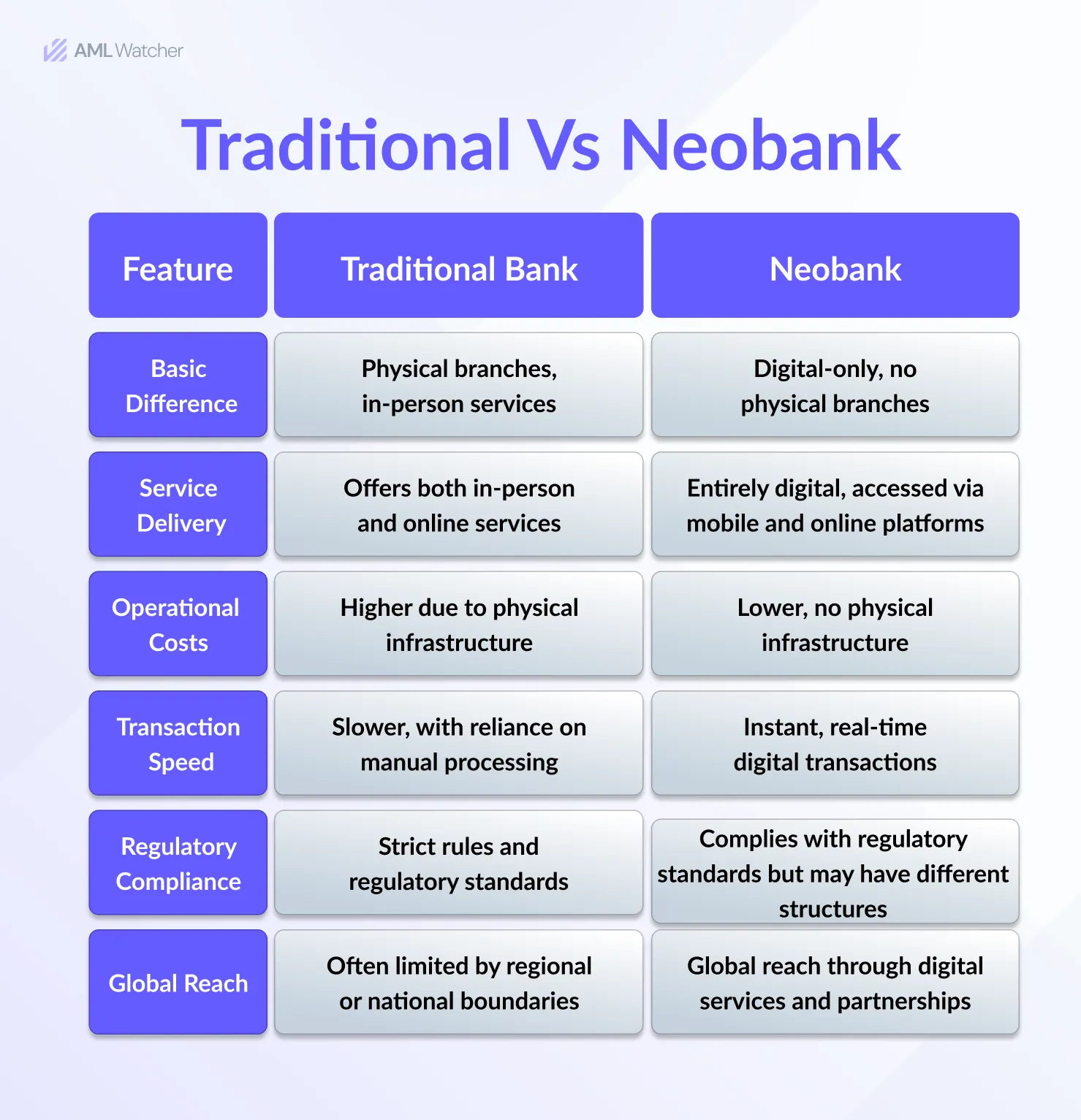

Rise of Neobanks and the Associated AML Screening Challenges

The true scale of AML Compliance challenges in Neobanks is evident from the answer to What is a neobank?

Neobanks are digital-only banks that have changed the banking industry to a large extent by offering streamlined user experiences and instant payments.

However, this instant service also brings diverse challenges, with susceptibility to fraud being the foremost concern. The scale and speed of account opening or transactions create a conflict due to the constant need to stay ahead of evolving financial crime strategies while maintaining effective AML processes.

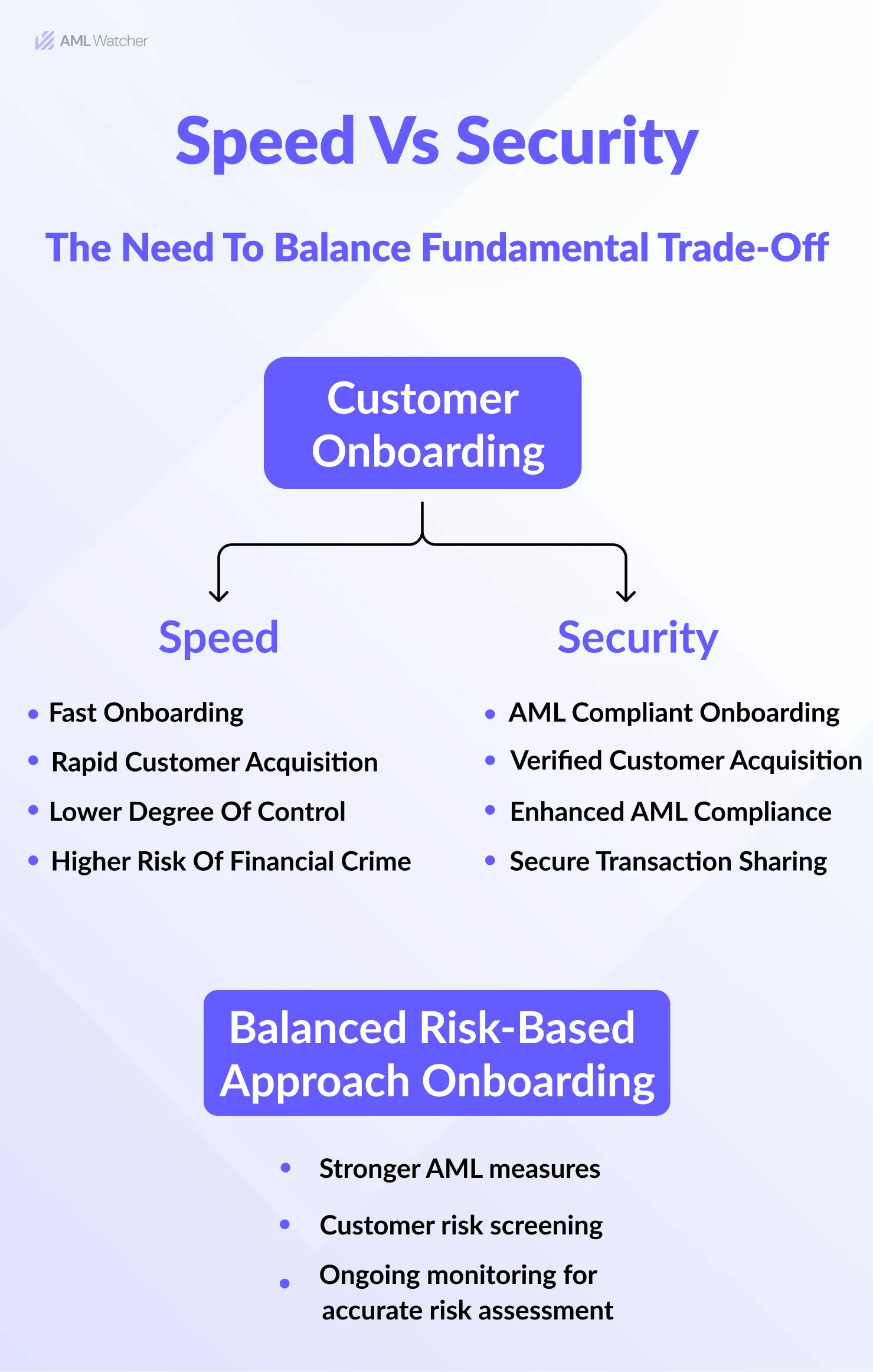

Speed Vs. Security – The Need to Balance Fundamental Trade-Off

Neobanks are famous for taking a few seconds to complete the onboarding process or share payments. This assists digital-only banks in scaling their customer base. However, prioritizing speed comes at a cost, which often poses compliance challenges for these banks.

According to the Swedish national risk assessment, neobanks’ digital identification of customers mostly includes a lower degree of control, making them more vulnerable to identity theft and financial crimes.

While seamless customer onboarding experiences increase customer acquisition, weak security measures make Neobanks more vulnerable to FinCrime.

Compliance officers implementing AML regulations for Neobanks must ensure to perform accurate customer risk assessment, and this can be done by implementing an advanced risk-based approach to AML compliance through the assistance of a screening solution with comprehensive data coverage.

How to Balance Speed with AML Compliance?

A balanced approach ensures compliance and growth for businesses. Therefore, the neobanks that want to accelerate their growth must balance the provision of instant financial services with the latest AML regulations.

It may include:

Automation Backed by Comprehensive Customer Data

The scale and scope of operations by Neobanks require them to utilize advanced AML screening solutions that not only automate customer risk screening but also ensure accuracy, allowing risks to be filtered and valuable customers to be identified.

Overreliance on automation without sufficient quality data and manual review processes leads to inadequate AML risk assessments of high-risk clients. This weakens the effectiveness of screening for customers against Politically Exposed Persons (PEPs), watchlists, and sanctions lists.

The €4.25 million fine in October 2021 imposed on German FinTech company N26 by the Federal Financial Supervisory Authority (BaFin) due to shortcomings in its AML monitoring measures serves as a pertinent example of how an imbalance between speed and security ends up in huge penalties.

Instant Transactions and Structuring Risk

This is particularly critical in the context of SEPA Instant Payments in the European Union, where transactions are processed in real-time, increasing the pressure to meet compliance obligations on time.

Some of the Neobanks that operate on real-time payment systems such as SEPA instant payments in the European Union, which facilitate Instant and Faster Payments, pose different compliance challenges, particularly in adhering to sanctions regulations.

As per EU instant payments regulations, Payment Service Providers (PSPs) are required to monitor transactions and screen customers against sanctions lists on a daily basis.

This poses a significant challenge for neobanks in both preventing financial crime and ensuring AML compliance with evolving regulations, especially within the European Union’s context for SEPA Instant Payments.

The US Department of the Treasury’s Financial Crimes Enforcement Network (FinCen) highlights how instant transfers in neobanks result in heightened risk for money laundering.

Challenges Faced by Neobanks due to AML Non-Compliance

Restrictions on N26 by The Bank of Italy

In March 2022, the Bank of Italy imposed restrictions on N26 due to AML deficiencies, including fast onboarding that prioritized speed over compliance. This led to inadequate customer risk assessments and gaps in detecting fraudulent accounts, increasing exposure to financial crime.

N26’s failure to integrate AML systems with customer risk assessments allowed high-risk clients to slip through. Their transaction monitoring systems were also ineffective at flagging suspicious activities.

The case highlights the need for a balanced approach to onboarding, ensuring both speed and thorough customer risk assessment to prevent compliance failures and financial crime exposure.

A strong AML framework, with continuous transaction monitoring and enhanced due diligence for high-risk clients, is essential.

FATF has reported that the new payment methods, such as online payments, have been misused for money laundering and terrorist financing purposes.

Restrictions on Robinhood Crypto by the New York State Department of Financial Services (NYDFS)

New York State Department of Financial Services (NYDFS) imposed a penalty of $30 million on Robinhood Crypto for significant violations of the Bank Secrecy Act (BSA) and anti-money laundering requirements.

During this inspection, Robinhood was found to be inadequately staffed to comply with the evolving AML regulations. These gaps in compliance demonstrate the need for robust compliance programs and sufficient allocation of resources to maintain regulatory adherence.

Using Ongoing Monitoring to Get Accurate Changes in Customer Risk Profiles

Neo-banks often use multiple tools, such as device location, customer behavior, transaction monitoring, and other digital footprints, to analyze customers’ dynamic risk.

However, accurate customer risk assessment in line with the regulations of a particular jurisdiction requires access to dynamic data on changing customer profiles, such as changes in PEP Status, or their name being subject to sanctions entities, or warnings and regulatory enforcement.

Here, using automated tools that assist with ongoing monitoring of the customers by updating about changes in risk profiles plays a crucial role. These systems track dynamic changes in AML data, ensuring that any updates to client risk profiles are immediately recognized.

For instance, a client who is not sanctioned during onboarding could later be added to sanctions lists, or a previously sanctioned individual may get delisted.

Additionally, clients who were initially deemed low-risk might later be subjected to regulatory warnings or appear in adverse media reports linked to illicit activities.

Organizations can proactively manage and mitigate emerging risks by continuously monitoring these developments.

Speed and AML Compliance- A Framework for Neobanks

Neobanks must expertly balance transaction speed with strict regulatory compliance. In this balancing, a risk-based strategy is involved that categorizes the clients into different tiers based on their risk profiles. These risk tiers are:

-

Low-risk

Instant and AI-powered verification for smooth onboarding.

-

Medium-Risk

Enhanced tracking with quick decision-making.

-

High-Risk

Manual feedback and limitations on transactions to hinder scams.

Partner AML Watcher For Better Compliance

Every neobank faces the challenge of balancing speed with compliance, often hindered by unreliable service providers with fragmented solutions.

To navigate the delicate balance between speed and compliance, partnering with a platform like AML Watcher is necessary.

AML Watcher empowers Neobanks to ensure seamless compliance with AML regulations:

- Accurate Risk Assessment: Gain access to 3500+ official watchlists, covering 215+ sanction regimes, and 2.6 million PEP profiles.

- Due Diligence: Robust screening of adverse media across 415+ risk categories in 80 languages.

- Ongoing Monitoring: Continuous updates to clients’ risk profiles in response to changes in regulations or their status in PEP and sanctions lists.

- Regulatory Enforcement Warnings: Timely alerts and compliance enforcement to mitigate potential risks.

- False Positive Reduction: Advanced machine learning minimizes false positives by improving detection accuracy.

- Real-Time Screening: Conducts immediate checks against watchlists and sanctions lists, ensuring the prompt identification of illicit activity.

- Unified Solutions: A consolidated approach to AML monitoring and risk assessments, streamlining compliance tasks, ensuring data accuracy, and improving operational efficiency. This integrated strategy helps neobanks scale while maintaining robust security and compliance standards.

Our team helps neobanks establish and maintain robust AML compliance frameworks, ensuring sustainable success in the competitive digital banking landscape.

- No commitment needed

- Complete AML Database at your service

- Access our all-in-one dashboard

Tier-2 PSPs in ... must demonstrate automated monitoring, layered CDD, &...

See the Full Regulatory Expectation70–80% less manual work, 95% less fatigue, TruRisk Agent makes compliance effortless.

Experience Agentic AMLMove Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries