Why Payment Service Providers Must Conduct Real-Time Sanction Screening?

Sanctions

May 15, 2025

- EU Sanction Compliance for Payment Service Providers

- SEPA Streamlines the Cross-Border Transactions

- Sanctions Screening Requirements as Per EU Instant Payments Regulations

- Why Sanctions Screening is Challenging for PSPs

- Future Approach of PSPs

- AML Watcher Strengthens AML Compliance with Real-Time Sanction Screening

“Digital payments are projected to exceed $33.5 trillion by 2030.”

Worldpay Global Payments Report 2025

As digital payments continue to surge, transcending borders and reaching even the most distant regions, this raises a key question: What is a Payment Service Provider (PSP)? What AML protocols do they follow to transfer funds and handle payments?

Payment-related services such as transferring funds, facilitating card payments, handling transactions through an electronic wallet, and processing direct debits are performed by Payment Service Providers (PSPs).

PSPs have significantly improved the efficiency of cross-border payments, but they face the ongoing challenge of ensuring compliance with evolving sanctions regulations.

With the increasing volume of transactions, managing sanctions compliance becomes more complex, especially due to false positive results, manual reviews, and frequently updated sanctions lists.

The FATF’s Cross-Border Payments Survey highlights that 5% of cross-border transactions require additional sanctions checks. Yet, over 99.9% of these checks result in false positives, causing delays and increased costs for financial institutions.

Manual reviews of paper-based trade documents further slow down the efficiency, while ongoing changes to sanctions lists during the transaction cycle add more complexity. This indicates the critical need for more efficient, automated sanctions screening solutions.

Payment Service Providers (PSPs) are, similar to traditional financial institutions, required to ensure timely sanctions compliance in accordance with the regulatory requirements of their respective jurisdictions.

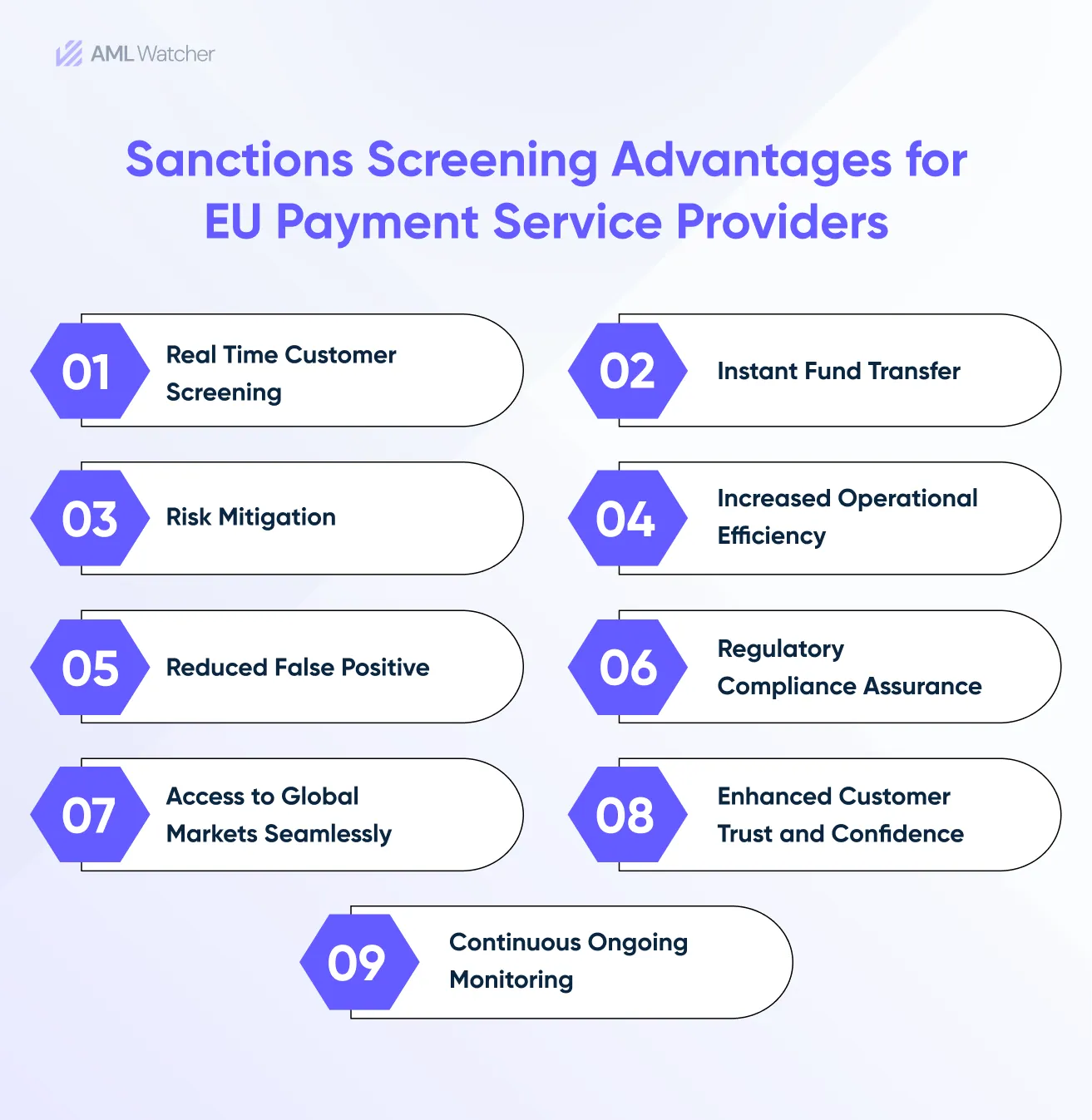

Selecting reliable, secure, and trustworthy AML compliance solutions improves the ability of Payment Service Providers (PSPs) to operate and ensures adherence to relevant AML laws and regulations.

Since PSPs face the challenge of balancing payment speed with accurate sanctions compliance, it is crucial for them to choose a sanctions screening tool that provides precise risk assessment without compromising efficiency.

Integrating a robust sanctions compliance solution enables PSPs to mitigate the risk of violating sanctions and protect their reputation and operational integrity by ensuring compliance with relevant laws and regulations.

To fully understand how PSPs can maintain AML compliance, it’s essential to look at the specific regulatory framework within the EU.

EU Sanction Compliance for Payment Service Providers

According to the EU Payment Services Directive 2 (PSD2), payment service providers must obtain official authorization or registration from their country’s financial regulator before they can legally offer payment services.

In the European Union, sanction screening is a must-have compliance requirement for payment service providers. It is included in their due diligence process to ensure compliance with EU regulations and prevent financial crimes such as money laundering and terrorist financing.

Sanctions screening requires an appropriate balance between speed, efficiency, and meeting legal requirements to ensure PSPs do not unintentionally engage in illicit transactions.

Instant payments, which are conducted in seconds, are increasing in Europe. PSPs must comply with new requirements to screen clients and transactions without missing AML checks, such as sanction screening of clients under the latest EU regulations.

Interesting read yet?

Let’s move forward and learn why sanction screening for PSPs is challenging, given the need to balance speed, convenience, and risk.

According to the New regulations, what rules must be complied with to provide effective services?

SEPA Streamlines the Cross-Border Transactions

The Single Euro Payments Area (SEPA) was introduced to harmonise the payment system, making cashless European payments easy and efficient across borders, just like domestic payments.

Before SEPA, euro payments were slow, as many days were usually required to settle the fees, and high charges across borders, sometimes amounting to 20-30 € per transaction.

Due to variations in rules per country, the efficacy of payment services providers is compromised, which creates confusion, leading to delays and promoting uncertainty in transferring funds across borders.

After introducing SEPA, these issues have been resolved; SEPA makes it uniform, speeds up the process by cutting costs, and promotes clarity; it makes payments across borders efficient, just like domestic euro transfers.

Sanctions Screening Requirements as Per EU Instant Payments Regulations

The European Union officially published Regulation (EU) 2024/886 (the Instant Payments Regulation) in the journal on 19 March 2024. It received legal approval in February 2024 and became effective on 8 April 2024.

As per Article 5d(1) of Regulation (EU) No 260/2012 (as amended by Regulation (EU) 2024/886), PSPs that offer services of SEPA Instant Payment must perform screening of their clients against the EU’s sanctions lists.

Additionally, the regulation requires that whenever sanction lists are updated, Payments Service Providers must re-screen their clients immediately to ensure they are not outdated or missed newly updated sanctions lists.

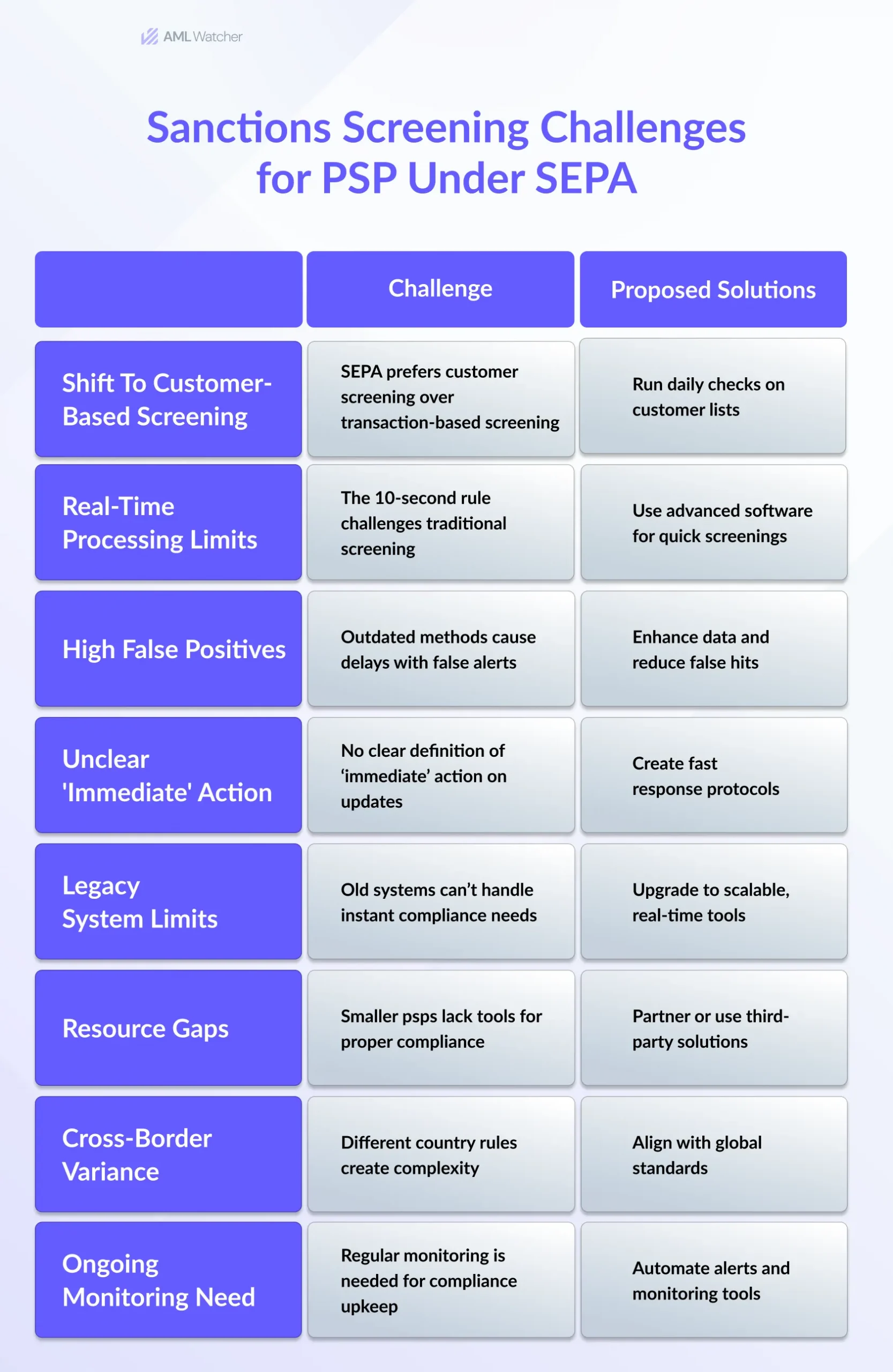

Article 5d(2) encourages customer-level screening instead of transaction-based sanction screening. Before starting or receiving payments, screen clients by checking their names against EU sanctions lists.

There are some key points: screen clients daily against EU sanctions lists and adopt a risk-based approach, rather than focusing solely on transaction screening. This will help prevent transaction delays and speed up cross-border secure payments.

While these regulations set clear standards, implementing effective sanctions screening presents several challenges for Payment Service Providers.

Why Sanctions Screening is Challenging for PSPs

Balancing Speed and Financial Risks

Instant payments are usually settled within 10 seconds, making it quite challenging to prioritize transaction speed while managing compliance risks. There is no time to complete lengthy screening steps or manual checks.

Suspicious transaction activities, such as links to sanctioned entities, must be reported to the relevant regulatory authorities, such as the EU’s Financial Intelligence Units (FIU), through a Suspicious Transaction Report (STR).

AML failure in reporting suspicious transactions results in significant AML fines and reputational damage

So,

Payment service providers must balance speed and risk management while complying with laws, ensuring transactions are fast and not associated with any illegal activity.

Management Complexity and Multiple Types of Sanctions

The Sanction screening process is often quite comprehensive, encompassing more than just comparing client names to sanctions lists.

Sanctions screening is complex due to the varying scope of sanctions across different jurisdictions. The mere appearance of a name on a sanctions list doesn’t necessarily indicate a risk.

Depending on each country’s specific regulations, entities may be subject to various measures, such as asset freezing, travel bans, arms embargoes, and secondary sanctions.

AML Solutions Struggling with Evolving Regulations

Traditional sanction screening solutions typically rely on regulatory updates to sanctions lists, issued by official regulatory authorities such as the EU, UN, and OFAC. New sanctions are not initially displayed in the official database after the update and announcement of sanctions.

PSPs might miss potential financial risks relying solely on the sanctions list data, such as interactions with sanctioned entities or temporary restrictions.

Even a few minutes’ delay can cause AML compliance failures. In the world of instant payments, real-time updates, and AML screening solutions, these tools help ensure robust sanctions compliance.

Future Approach of PSPs

Payment service providers must prioritize the screening of clients daily as mandated by Article 5d(1) of the IPR.

Therefore, they must have an advanced and robust AML screening solution that promptly responds to new sanctions and screens against the latest sanction lists to ensure compliance with the EU’s Article 5d(1) of the IPR.

AML software facilitates automated sanctions monitoring, allowing Payment Service Providers to respond instantly to newly listed individuals or entities.

PSPs earn the trust of clients and avoid penalties by complying with the latest regulations and backing challenging situations without slowing down the customer experience.

AML Watcher Strengthens AML Compliance with Real-Time Sanction Screening

AML Watcher empowers the payments service providers to facilitate cross-border transactions by offering a sanctions screening solution and addressing the challenges that payment service providers (PSPs) face in complying with a recent update by the EU, specifically the Instant Payments Regulation (Regulation (EU) 2024/886). It offers:

Context Driven Approach to Sanctions Screening

Its context-driven approach ensures that each customer’s risk is evaluated on different levels of risk and types of sanctions. Some clients may face embargoes or sanctions, while others are under travel bans or have assets frozen.

Regular Data Updates

With frequent updates, the solution automatically integrates the latest changes in sanctions lists, keeping your compliance efforts current and your business aligned with constantly changing sanctions regulations.

It prevents compliance breaches by reducing false positives due to outdated data.

Batch Search Feature

AML Watcher’s batch search feature empowers businesses to efficiently screen large volumes of customers daily against the most up-to-date sanctions lists.

This tool allows Payment Service Providers (PSPs) to make firm decisions and streamline their compliance processes by automating the screening of multiple clients simultaneously against EU sanctions lists.

It reduces manual workload and enhances operational efficiency.

Secondary Sanctions

Secondary sanctions are mentioned to avoid legal consequences by preventing indirect dealings with sanctioned entities.

It clearly labels secondary sanctions and reduces the review time for PSPs, optimising the compliance process and minimizing exposure to financial and reputational risks.

Reduction in Review Time

Real-time sanction screening updates sanctions lists after 15 minutes and ensures PSPs use the most recent data, validating sanction compliance gaps and enhancing the speed of transactions across borders.

Adverse Media Screening

Traditional AML software ensures PSPs keep up with sanction updates, but struggles to

balance speed and risk mitigation.

AML watcher addresses this concern effectively by offering adverse media screening, accelerating PSPs’ ability to capture sanctions before they appear on legally updated sanctions lists, and ensuring no sanctions are missed during rapid cross-vendor transactions.

Reducing False Positives in Sanctions Screening

A major challenge in payment sanctions screening is minimizing false positives while ensuring accurate detection of sanctioned entities in real time.

AML Watcher enables PSPs to quickly identify entities on sanction lists, reducing false positives, while maintaining an efficient workflow that does not compromise compliance.

Contact us today to streamline your sanctions screening while maintaining the speed and compliance requirements of cross-border transactions.

Frequently Asked Questions

Sanctions in payments are legal restrictions that prevent transactions with specific individuals, entities, or jurisdictions to combat financial crime such as money laundering, terrorist financing, fraud, and corruption.

- No commitment needed

- Complete AML Database at your service

- Access our all-in-one dashboard

Tier-2 PSPs in ... must demonstrate automated monitoring, layered CDD, &...

See the Full Regulatory Expectation70–80% less manual work, 95% less fatigue, TruRisk Agent makes compliance effortless.

Experience Agentic AMLMove Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries