Types of Financial Fraud Every Business Should Know

Fraud Prevention

December 9, 2025

The number of losses businesses incur from illegal activities is increasing significantly with each passing year. However, this damage is not only fiscal, it severely affects a business’s brand image, official standing, and trust. According to ACFE’s 2024 study, most organizations lost nearly 5% of their annual revenue to fraud. In that research, an assessment of 1921 actual cases discovered that organizations incurred a median loss of $145,000, and in 22% cases, the loss exceeded $1 million.

This is similar to waking up and finding out that the bank has no money left in its account or that an accredited employee commits a scam. These scenarios are no longer hypothetical; they have become a bleak fact in modern society that every business must be aware of, whether it’s a bank or any other finance-based institution.

To get clarity on this, let’s first understand what are the common fraud types that businesses experience in their everyday lives and comprehend how they can save themselves from the legal consequences in response to these fraud cases.

What Is Financial Fraud?

Financial fraud is the deliberate practice of manipulation or trickery, especially for monetary gain. From phishing attacks to payment or tax fraud and card fraud to crypto investment scams, there are several methods of committing fraud.

The consequences of these frauds are more than just direct financial losses; they can also break the trust of clients, result in severe repercussions, and easily tarnish a brand’s reputation.

Let’s understand what these frauds are.

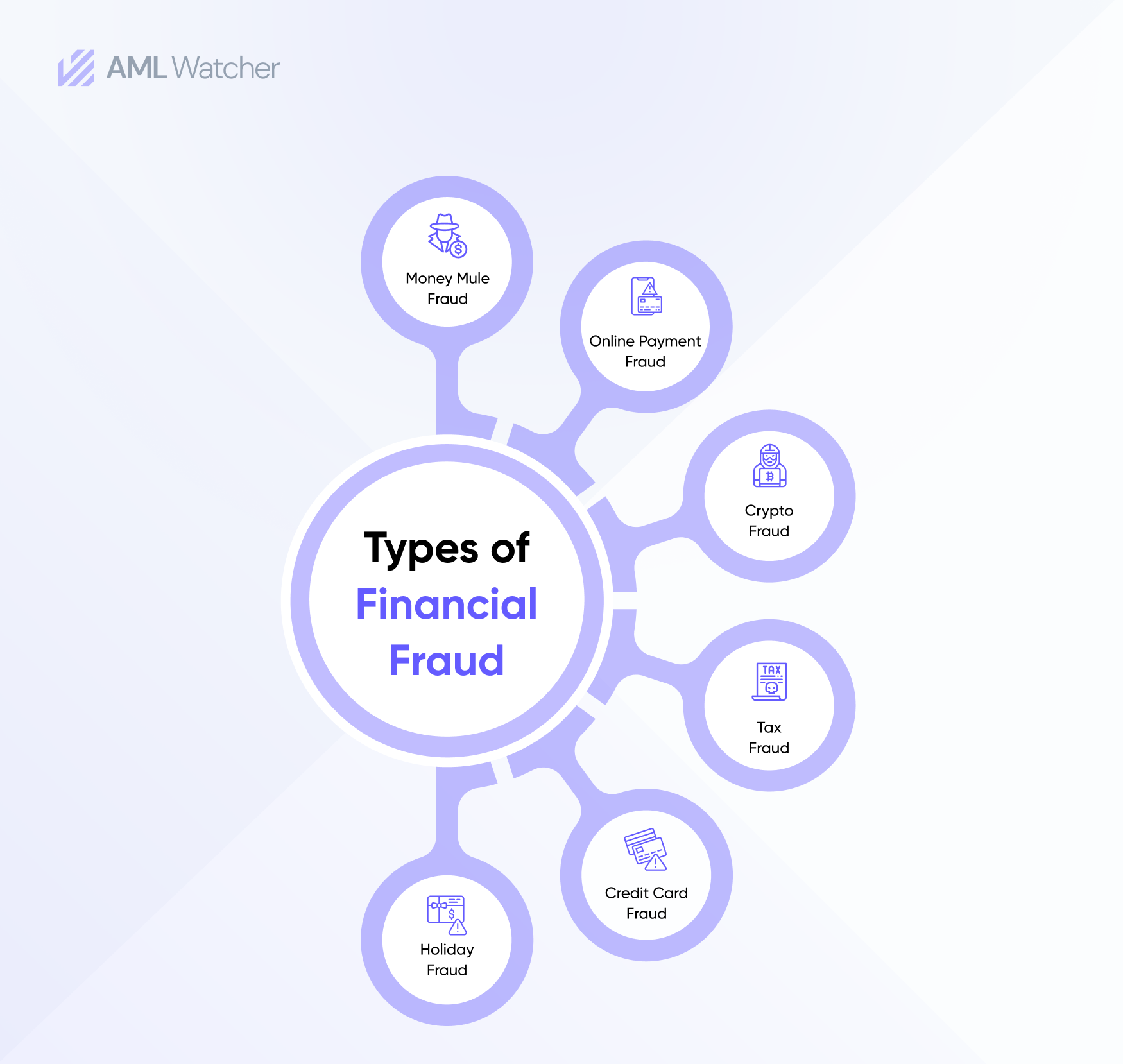

Types of Fraud

1. Identity Theft

Identity theft occurs when criminals steal personal information to open or take over accounts, access funds, or move illicit money, making it a major risk area for AML teams. It often begins with stolen data from phishing attempts, physical document theft, or large-scale breaches targeting financial details. Once the information is obtained, fraudsters can impersonate customers to bypass onboarding or account controls.

Businesses can stop such threats by using effective identity verifiers, performing ongoing monitoring, and checking the customers properly against sanctions or other high-risk entity lists. Furthermore, device intelligence and other risk signals can effectively prevent account takeover and phishing attacks.

2. Online Payment Fraud

The growth of digital commerce has made online payment fraud a serious threat to businesses. In this type of fraud, criminals make unauthorized payments or withdrawals from victims’ accounts using stolen credit information, account takeovers, and phishing attacks. The convenience for criminals to make fake online transactions has made it necessary for businesses to make preliminary changes to their monetary activities.

Such fraud can be easily mitigated when a company adopts advanced detectors that assess anomalous patterns in financial activities. They should also integrate Multi-factor authentication at all payment processing steps to ensure that only authentic clients can proceed with their transactions. Furthermore, tokenization and encryption methods can be used to protect payment data and minimize data breaches.

3. Crypto Fraud

With Virtual currencies gaining prominence, the fraud targeting crypto investors and businesses is also increasing. In this type of financial fraud, fake funding schemes, pump and dump techniques, and Ponzi schemes are included. Additionally, the decentralized nature of the cryptocurrency sector, where there are no intermediaries, makes it highly complex to trace fake transactions. As a result, businesses operating in crypto become more vulnerable to legal penalties, including heavy fines and damage to brand image.

Therefore, crypto businesses must employ advanced monitoring systems to monitor blockchain transactions effectively. The purpose behind implementing these tools is to ensure real-time flagging of illicit transactions and compliance with anti-money laundering (AML) standards.

4. Tax Fraud

Another example of a financial scam that affects businesses globally is tax fraud. It ranges from underreporting income to falsifying deductions. In some cases, businesses intentionally hide their income and funds to avoid taxes. This is known as tax evasion. This continuous practice makes businesses more vulnerable to credibility loss, serious repercussions, and massive fines.

Financial institutions can assist in reducing tax fraud with proper due diligence, continuous monitoring, beneficial ownership identification, and source of funds tracking for anomalous transactions.

5. Credit Card Fraud

Credit card fraud is one of the most pervasive types of fraud. This occurs when a criminal steals someone’s card and uses it to make unauthorized purchases. It can also include the manipulation of payment systems along with the integration of social engineering strategies to gain insights into clients’ credit card credentials.

Businesses can reduce credit card fraud by ensuring secure payment gateways and staying informed with the latest security standards, such as the Payment Card Industry Data Security Standard (PCI-DSS). They can also integrate systems that can effectively monitor anomalies in payment transactions, for instance, if a payment exceeds the set limit, it can flag that in real-time. By doing so, it enables businesses to identify fraud before it actually happens.

How Money Mules Help Move Fraud Money

Criminals usually hire other individuals (mostly young students) to move funds generated from fraud and other illicit activities. These individuals, known as money mules, unknowingly and sometimes for small benefits, assist criminals in transferring funds between jurisdictions and accounts. This activity makes it harder to associate criminal proceeds with their actual beneficiaries and the illegal activity that generated them.

Proper risk assessment and risk profiling can help detect suspicious behaviour that signals mule activity and help track any funds generated from illegal activities. Transaction volume and amounts that do not match the economic status of the account holder are strong indicators of potential money mule fraud.

Fraud During Holidays

Every year, the holiday season comes with an increased risk of fraud for businesses because of the excessive number of customers on e-commerce platforms for shopping and travel bookings. Criminals exploit this surge to engage in illegal activities such as identity theft, fake purchases, charity fraud, and e-commerce money laundering. With consumers and businesses operating at speed, suspicious activities often go unnoticed and remain unflagged.

To minimize holiday fraud, businesses should integrate effective identity checks when they have a long list of clients to deal with. Instant detection of irregular purchasing patterns can help identify fraud beforehand.

How Financial Fraud Impacts Beyond Monetary Losses

Some consequences of financial fraud appear at the moment, but there are some long-term impacts on businesses that are way more damaging. They include:

Reputational damage that can ultimately erode client trust, minimize proceeds, and tarnish brand image. For instance, if a business goes through data breaches due to fraud, it could experience loss of client trust, which is quite complex to rebuild, if not impossible.

Repercussions for financial fraud are massive. There are a lot of countries that implement rigorous standards and regulations that are made to hold any business that fails to report fraud accountable for it.

Non-adherence to AML and KYC regulations leads to huge financial penalties, regulatory scrutiny, and lawsuits that are quite costly.

To prevent these long-term consequences, businesses must take proactive fraud detection strategies that will reduce the risk of reputational damage and other legal repercussions. These approaches include staying informed about relevant regulatory standards, the integration of effective fraud detection systems, and reviewing the internal processes regularly.

Combat Financial Fraud With AML Watcher

Are rising fraud schemes making it harder for your business to stay protected?

From money mule fraud and online payment scams to crypto, tax, and card fraud, each threat demands faster detection and stronger controls. AML Watcher helps businesses combat these risks through:

- Real-time fraud detection to flag suspicious transactions and patterns related to fraudulent schemes, such as phishing attacks, unusual payments, and account takeovers.

- Adverse media screening to spot potential criminals proactively, while gaining insights into whether the potential individual is involved in any financial scandals or has negative news in the media.

- AI-powered risk scoring that automatically evaluates customer and transaction risk levels, generating an accurate fraud score that helps teams prioritise high-risk cases faster while reducing false alerts.

- Sanctions, watchlists, and PEP screening to identify high-risk individuals and apply the appropriate level of due diligence before establishing or maintaining business relationships.

AML Watcher empowers businesses by making them alert, protected, and one step ahead of emerging risks.

- No commitment needed

- Complete AML Database at your service

- Access our all-in-one dashboard

Tier-2 PSPs in ... must demonstrate automated monitoring, layered CDD, &...

See the Full Regulatory Expectation70–80% less manual work, 95% less fatigue, TruRisk Agent makes compliance effortless.

Experience Agentic AMLMove Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries