AML Screening: Fighting The War Against Money Laundering

Anti Money Laundering

May, 27 2025

January 23, 2024

In March 2025, HM Treasury issued its annual “Anti-Money Laundering and Counter-Terrorist Financing (AML/CTF) Supervision Report,” with a major focus on two primary goals: enhancing compliance monitoring effectiveness and AML/CTF legislation.

In May 2025, the Central Bank of Cyprus (CBC) introduces a risk-based AML/CFT directive, effective on June 2, 2025, allowing financial institutions to update customer information based on risk profiles and customize due diligence to individual risks, therefore expediting operations for low-risk clients.

In April 2025, the Monetary Authority of Singapore (MAS) recommended changes to AML/CFT notifications, highlighting the need for AML Screening using relevant search engines from countries linked with the person and conducting screening in their native language.

This seeks to reduce false positives and maximize the efficiency of AML compliance solutions, particularly those that offer multilingual screening.

In the same month, OFSI’s penalty notice emphasizes critical AML compliance standards for all firms incorporated under UK legislation.

OFSI recommends that businesses thoroughly understand and handle sanctions risks, seek expert assistance, and adhere to its guidelines.

It also underlines the significance of thoroughly evaluating and implementing sanction screening methods for each business.

Now, the interesting point is, all these regulatory bodies are focused on one goal: enhancing AML/CFT regulations with the integration of strong AML screening processes.

This increased focus and amount of regulatory rule issuances also underscore an important fact:

- Traditional anti-money laundering screening processes are no longer sufficient.

- Financial institutions require updated and efficient AML Screening and Monitoring solutions aligned with their risk appetite.

This article will look at the essentials of AML screening and why efficient, real-time Screening in AML is no longer simply a legal requirement but a critical tool for protecting your organization, reputation, and financial integrity.

What is AML Screening?

Anti-money laundering screening is the process of cross-checking potential clients against public databases such as sanctions lists, PEP lists, watchlists, criminal lists, and adverse media to identify individuals or business entities who may be involved in money laundering or terrorism financing.

While AML screening is essential for identifying financial crime threats, it is part of a larger compliance framework that includes customer background checks, due diligence, continuing risk assessments, and transaction monitoring.

In brief, financial institutions and other obliged entities must conduct AML Screening and Monitoring to:

Evaluate the risk level of their consumers.

Avoid conducting business with high-risk people and organizations, such as sanctioned parties and PEPs.

What are the Types Of AML screening?

Anti money laundering screening has become essential for recognizing financial crime threats and complying with the latest legislation.

There are multiple forms of AML screening: sanctions screening, PEP screening, Watchlist screening, SIP/SIE screening, and adverse media screening.

Each kind focuses on a unique area of risk and serves an important role in protecting financial institutions.

1. Sanctions Screening

Sanctions screening includes cross-referencing client data to sanctions lists issued by institutions such as OFAC (Office of Foreign Assets Control), OFSI (Office of Financial Sanctions Implementation), Global Affairs Canada, and the UN Security Council.

These lists include persons, corporations, and territories prohibited from engaging in crimes such as financing terrorism, money laundering, or corruption.

There are two main types of sanctions:

- Primary sanctions are those that directly target persons or organizations.

- Secondary sanctions impact people who conduct business with sanctioned parties.

Financial institutions must avoid doing business with sanctioned parties, as violating sanctions can result in legal penalties and reputational harm.

The screening should be performed in real time during the customer onboarding phase and for each transaction, as well as continuing monitoring to keep up with changes in sanction statuses.

Compliance Tip:

- Choose a screening solution with global sanctions list coverage

- Ensure it handles conflicting sanction regimes accurately

- Choose platforms that update sanctions promptly

- Prioritize real-time sanction screening

- Align screening with your organization’s risk appetite

2. PEP Screening

PEP screening seeks to identify Politically Exposed Persons (PEPs), who hold prominent public positions or have strong relationships with government officials.

PEPs have been classified as high-risk for money laundering and other financial crimes since they have access to considerable financial resources and are vulnerable to corruption.

PEP screening entails cross-referencing customers with PEP lists and doing enhanced due diligence (EDD) for increased assessment.

This involves determining the source of wealth and keeping track of ongoing transactions for suspicious activities. Individuals’ positions or associations change over time, therefore, politically exposed persons‘ lists must be updated on a regular basis.

Compliance Tip:

Choose a solution that

- Offers unified PEP data aligned with global frameworks

- Categorizes PEP risk levels from 1 to 4, covering both high-profile and local PEPs

- Includes PEP data from conflicted and controversial territories

- Provides coverage of regions with populations under 100,000

3. Watchlist and Criminal List Screening

Watchlist and Criminal List Screening is the practice of checking an individual’s information against databases holding the names of known or suspected criminals.

These checks are a vital aspect of AML compliance and serve a variety of objectives.

Criminal screening aims to detect those who have committed financial crimes such as money laundering, whereas watchlist screening focuses on individuals associated with higher-risk activities, such as terrorist funding.

Given that these lists are regularly updated, sustaining successful AML due diligence necessitates access to current databases and, ideally, real-time screening to assure accuracy and compliance.

Compliance Tip:

- Choose a screening solution that offers separate watchlist screening

- Incorporates regulatory enforcement and warning data

- Shares data from the Fugitive and Debarment lists

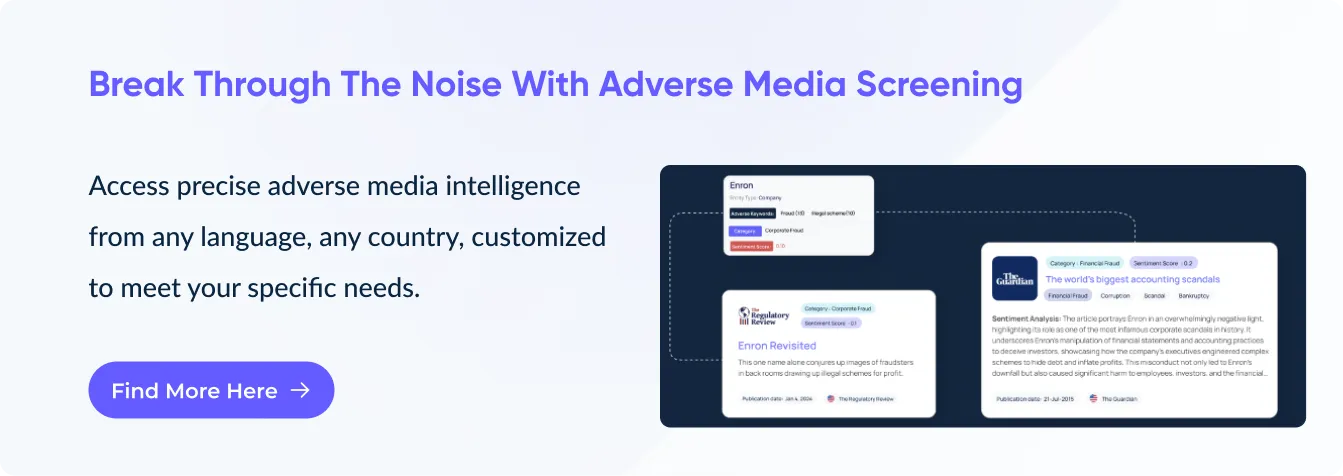

4. Adverse Media Screening

Adverse media screening is a method of scanning news stories, reports, and online publications for unfavorable information about an individual.

These mentions may suggest potential involvement in financial crimes such as fraud, corruption, or money laundering.

Unlike other methods of screening, adverse media screening does not use predefined lists. Instead, it employs complex algorithms to search media sources for unfavorable offering critical information about a customer’s risk profile.

Compliance Tip:

Choose a solution where Adverse Media Screening covers:

- FATF-designated offenses.

- Support trusted global media sources.

- Identifies risks in both pre- and post-conviction scenarios.

- Tailor media searches to your unique risk appetite.

- Advanced LLMs with risk categories to flag Correct Contexts

5. SIP/SIE Screening

Individuals and organizations classified as SIPs (Special Interest Persons) or SIEs (Special Interest Entities) are subject to greater investigation due to their suspected participation in illegal activities such as money laundering, fraud, or terrorism.

They may not be politically exposed, but their actions or connections put them at risk.

SIP/SIE screening entails cross-referencing client information with criminal watchlists or databases, such as Interpol’s Wanted Persons list.

This form of screening helps organizations avoid unintentionally associating with high-risk persons or entities associated with illegal activity, hence reducing possible legal exposure.

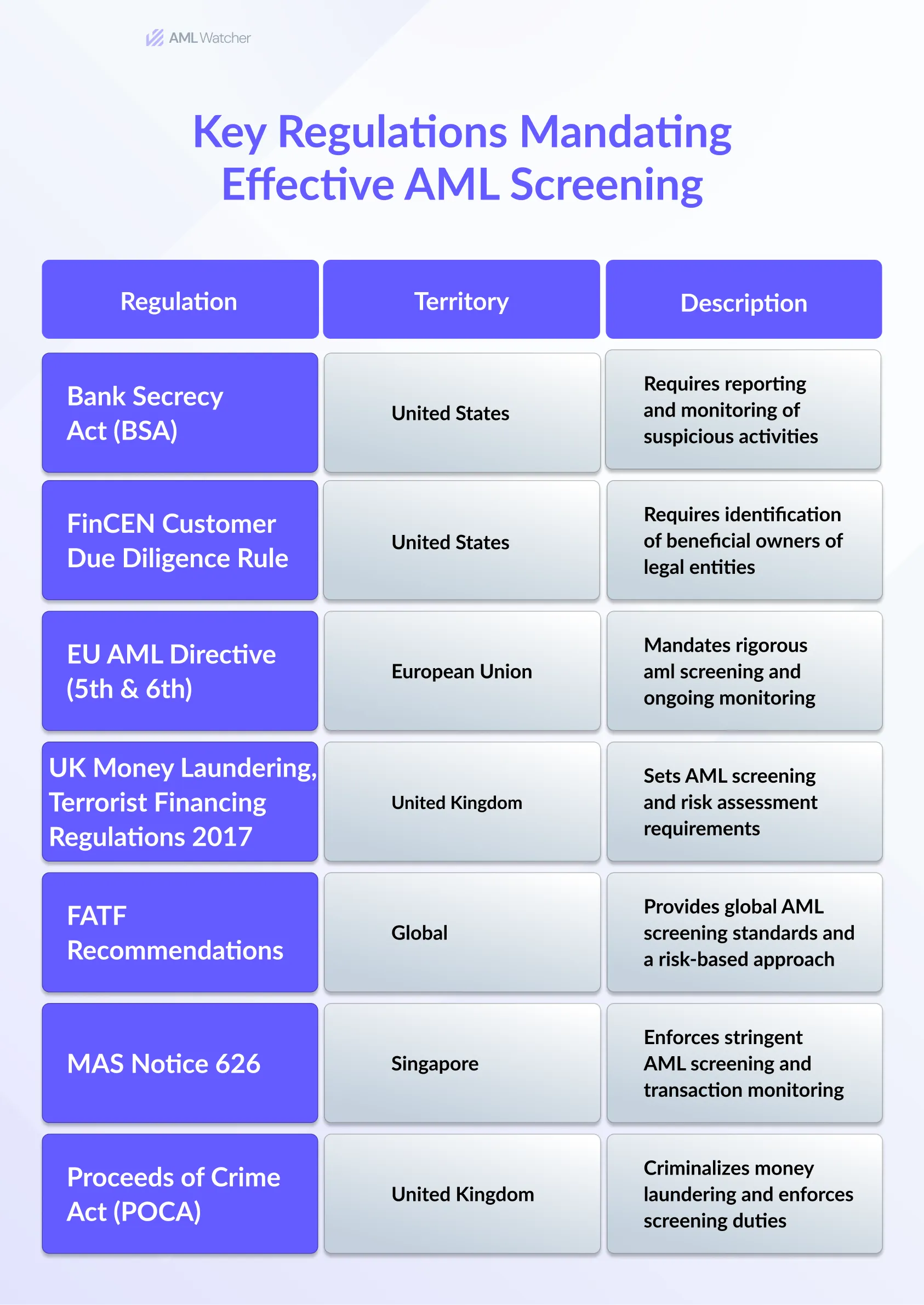

Key Regulations Mandating Effective AML Screening

Global AML regulations highlight thorough screening methods as important for detecting and reducing financial crime threats.

These regulations require institutions to conduct extensive client and transaction screening to ensure compliance and defend against illegal activity.

The key regulatory bodies are:

- Financial Action Task Force FATF Recommendations

- EU Anti-Money Laundering Directive (AMLD) – 5th & 6th Directive

- Bank Secrecy Act (BSA) – United States

- Financial Crimes Enforcement Network (FinCEN) Customer Due Diligence Rule – United States

- Money Laundering, Terrorist Financing and Transfer of Funds Regulations 2017- United Kingdom

- MAS Notice 626 on Prevention of Money Laundering and Countering the Financing of Terrorism – Singapore

The Proceeds of Crime Act (POCA) – United Kingdom

What is The Purpose Of AML screening?

The primary purpose of AML screening is to detect and prevent fraudulent activities, including money laundering, illicit transactions, and terrorist financing.

This goal can be divided into these main objectives:

Risk Assessment

The screening process assesses the risks associated with customers and their transactions, assisting in detecting suspicious activity and identifying high-risk persons or businesses.

Ongoing monitoring

This entails routinely checking consumers against sanctions lists, PEP databases, and other watchlists over time. This monitors changes in client risk levels, allowing firms to keep on top of emerging risks and changing consumer profiles.

Preventing Regulatory Penalties

Strong AML screening policies assist companies and financial institutions in avoiding fines and penalties that might result from noncompliance with AML rules and regulations.

Supporting Global collaboration

AML screening is essential not just at the local level, but also as part of worldwide collaboration in the fight against financial crime.

Countries work together through international organizations such as the Financial Action Task Force (FATF) to ensure that enterprises follow AML Screening Requirements and fight money laundering on a global scale.

How Does the AML Screening Process Work?

The AML screening procedure ensures the authenticity of the customer information and determines whether their conduct indicates any suspicious activities. Essentially, it contributes to determining a customer’s risk profile.

The screening process includes;

- Checks essential client information (name, DOB, ID, etc.)

- Screens customers against numerous essential databases, including sanctions, PEP, watchlists, and criminal records.

- Incorporates adverse media monitoring to detect negative news influencing risk profiles.

- Assesses a customer’s risk level using contextual insights and detailed data matching.

Focuses on continuous, real-time screening and monitoring aligned with regulatory requirements, enabling timely risk identification.

Looking for top AML screening providers with comprehensive features? AML Watcher has you covered.

Why AML Watcher Stands Out as the Premier AML Screening Solution?

AML Watcher employs a huge proprietary database and innovative algorithms to give unparalleled accuracy and efficiency in AML screening.

Our suite of tools provides compliance teams with the depth, speed, and context they need to remain ahead of changing risks and regulatory requirements.

It offers:

- Screening from 100,000 + data sources that incorporate 230+ sanctions regimes, and 2.6 million+ PEP profiles to discover comprehensive AML/CTF risks.

- Access to 3,500+ specialized watchlists, including debarment, fitness & probity, and sex offender lists, providing a comprehensive view of high-risk entities.

- Over 50,000 global media sources with 400+ risk categories identifying negative mentions and news related to customers.

- Customizes screening criteria depending on each organization’s risk appetite, allowing for targeted risk management via its risk-based screening methodology.

- Incorporates jurisdiction-specific profiling and constantly updated risk classifications to prioritize high-risk consumers and transactions.

- Harmonized PEP definitions aligned with FATF and Wolfsberg Regulations, categorized into PEP Levels 1 to 4 for tiered risk assessment.

- Coverage extends to local PEPs, including county mayors and administrators, and PEPs from jurisdictions with populations under 100,000.

- Secondary sanctions risk labels highlight conflicts between regimes like EU Blocking Statutes, avoid false positives, and increase compliance accuracy.

Frequently Asked Questions

- No commitment needed

- Complete AML Database at your service

- Access our all-in-one dashboard

Tier-2 PSPs in ... must demonstrate automated monitoring, layered CDD, &...

See the Full Regulatory Expectation70–80% less manual work, 95% less fatigue, TruRisk Agent makes compliance effortless.

Experience Agentic AMLMove Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries