6 Best Practices For Efficient PEP Screening

PEP

October 1, 2024

- How HSBC Significantly Breaches Supervisory Laws?

- What AML Measures Are Enforced By FINMA?

- The Concept of Politically Exposed Persons

- PEP Screening and Categorization

- Managing High-Risk PEPs Under Global Regulatory Guidance

- Why Do Traditional PEP Screening Solutions Fall Short?

- 6 Best PEP Screening Practices That You Can Trust: AML Watcher

Knowing your customers means knowing their risks, and continuous PEP checks are crucial for understanding your customers and their associated threats.

Recall a time when Switzerland’s financial regulatory authorities banned HSBC Private Bank (Suisse) SA because of banking ties to two politically exposed individuals.

In December 2021, FINMA imposed a variety of sanctions on the subsidiary of HSBC involving the transfer of multiple transactions of over $300 million between Switzerland and Lebanon between 2002 and 2015.

The regulator discovered that the institution’s actions had breached serious anti-money laundering laws.

This wasn’t just an ordinary regulation—it was a clear warning sign for financial institutions everywhere to follow updated AML regulations by regulatory bodies and report suspicious profiles on time.

This case brings to light how such cases offer valuable insights into the complexities financial institutions face today and also highlight the necessity to implement effective PEP screening solutions.

How HSBC Significantly Breaches Supervisory Laws?

HSBC Private Bank (Suisse) SA deliberately breached supervisory law by neglecting to appropriately investigate the sources, purpose, or background of assets in two high-risk business partnerships that were PEPs, totaling more than $300 million in transactions between 2002 and 2015.

Originating from a government entity, the funds were transferred from Switzerland to Lebanon and swiftly moved back to accounts in Lebanon, all without the bank explaining the usage of a transitory account.

HSBC failed to uncover money laundering indicators, didn’t comply with due diligence standards for politically exposed persons (PEPs), and failed to submit suspicious actions to the Money Laundering Reporting Office until 2020, despite agreeing to terminate the accounts in 2016 owing to known risks.

This shows a major violation of both the anti-money laundering regulations and suspicious profile reporting duties.

What AML Measures Are Enforced By FINMA?

The Switzerland financial regulator, FINMA, has mandated that HSBC Private Bank (Suisse) SA:

- Examine all of its existing business dealings with politically exposed persons (PEPs) and high-risk clients, and confirm the risk classification of all other clients.

- Not allowed to form new PEP partnerships until an audit agent certifies the completion of these reviews.

- Must also provide FINMA with a detailed report on the responsibilities within its board and executive management.

This highlights that financial institutions must stay vigilant about their PEP clients and to comply with the latest AML regulations must adopt efficient PEP screening solutions to detect the associated risks with them.

With this emphasis on PEP complexities and screening, why not review the basic idea of PEP, PEP screening, and associated PEP risk categories?

The Concept of Politically Exposed Persons

The Financial Action Task Force (FATF) defines PEPs as those individuals who are or have been trusted with public function.

In light of Article 52 of the United Nations Convention against Corruption (UNCAC), PEPs are defined as “ subjects who are or have been titled with prominent public positions in past or present, including their family members and close associates”

Taking a PEP as a customer, financial institutions (FIs) are required to conduct detailed evaluations to assess the risks associated with them.

PEP Screening and Categorization

FATF in its Recommendations 12 and 22 states that the FIs such as banks and other designated non-financial businesses and professions (DNBPs) under AML compliance are encouraged to employ a PEP compliance program to fight money laundering and potential financial crimes.

When conducting PEP screening, it is essential to pinpoint politically exposed individuals, as well as their relatives and close associates (RCAs). Additionally, it’s important to note that not all PEPs carry the same level of risk, as there are distinctions within the PEP category itself.

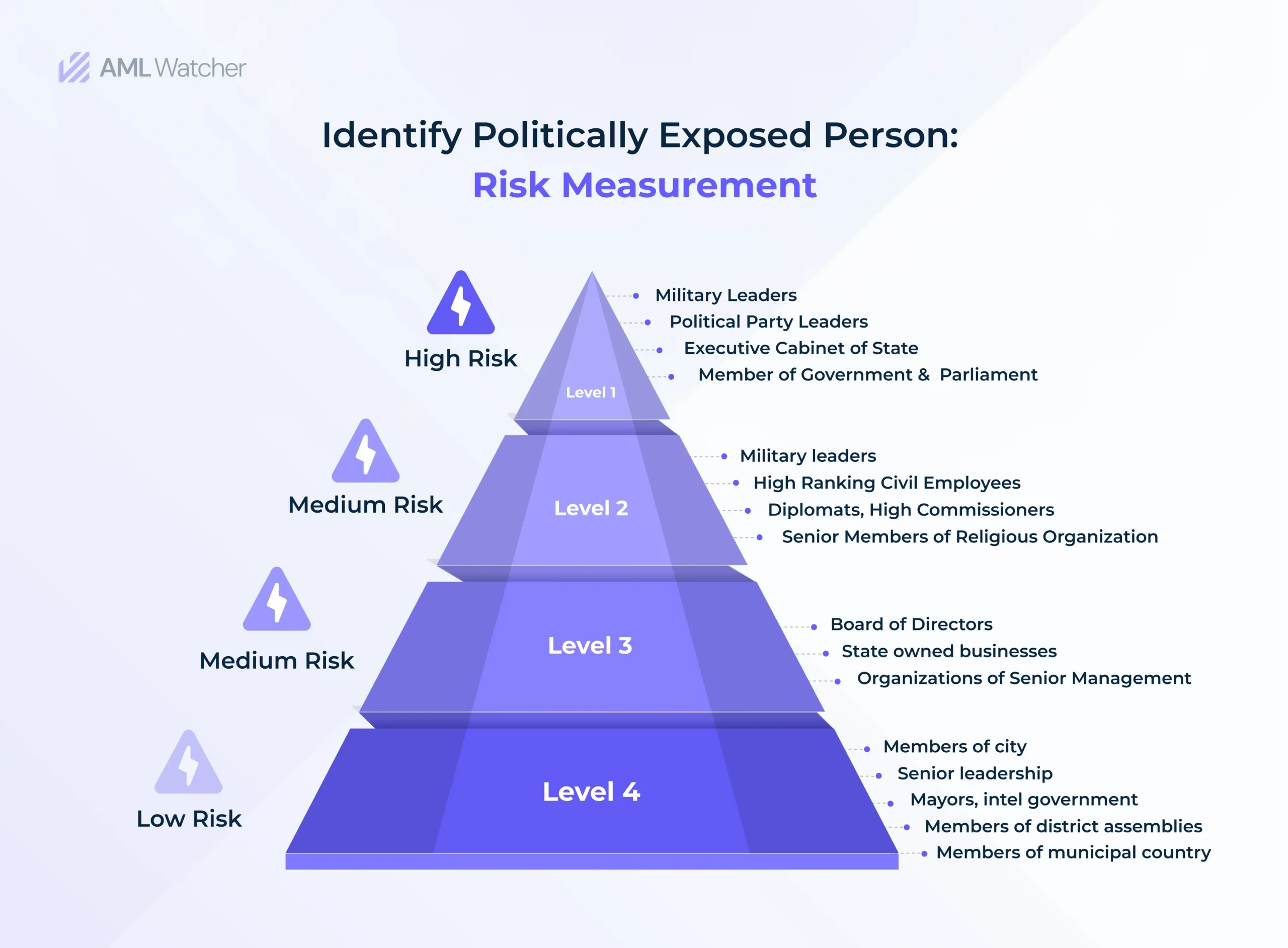

Categorization Based On 4 Levels of Risk

Different PEPs present different levels of AML/CFT risk. In light of this, it is possible to categorize the PEP risk levels into the following 4 risk levels:

Managing High-Risk PEPs Under Global Regulatory Guidance

After a detailed analysis of the PEP cases, international authorities like the FCA, FinCEN, and FATF have stressed that banks can manage high-risk PEPs without automatically excluding them.

- FATF: FATF recommendations 12 and 22 have established special measures that set the rules for improved due diligence, which enables banks to reduce the risks and at the same time, provide equality in access to banking services.

This approach complies with the regulations of various countries for example United States Bank Secrecy Act and the United Kingdom Proceeds of Crime Act.

- United States: PEP regulations under the Bank Secrecy Act (BSA) and Patriot Act require risk-based AML/CFT programs with customer due diligence (CDD) and enhanced due diligence (EDD) for high-risk PEPs. Firms must report suspicious activities to FinCEN.

- United Kingdom: FCA mandates PEP screening MLR 2017 & ATCSA 2001 similar to EU standards; ongoing review of PEP treatment by banks and financial firms, with findings expected in 2024.

- Canada: Under the Proceeds of Crime (Money Laundering) and Terrorist Financing Act (PCMLTFA), PEP screening is mandatory, with foreign PEPs always considered high-risk. The Financial Transactions and Reports Analysis Centre of Canada (FINTRAC) enforces these PEP regulations.

- European Union: Uniform PEP screening policy under AML Directives especially the 6AMLDs, following a risk-based approach aligned with FATF standards.

- Australia: The Australian Transaction Reports and Analysis Centre – AUSTRAC oversees AML/CTF compliance, requiring financial institutions to conduct PEP screening and adhere to CDD guidelines.

All these AML regulatory bodies emphasize one key point in the case of efficient PEP screening; adopt a risk-based screening solution.

Curious to explore how the legacy solution providers ignored this key aspect with multiple lacks in their screening solutions.

Why Do Traditional PEP Screening Solutions Fall Short?

Global businesses especially financial institutions often fail to identify, categorize, and highlight low to high-risk PEPs due to their screening solution lacks and failures. These are:

Lack of a Single Universal PEP Definition

Different countries have varying criteria for what constitutes a PEP, which complicates the implementation of a unified screening process.

For instance, FATF has broader criteria to consider any person as PEP whereas the US, UK, Canada, and other countries have different explanations of PEPs.

Thus multiple screening solutions offer PEP screening solutions with limited scope or consider PEP which falls under specific country definition, which limits the screening outcomes.

Limited Jurisdictional PEP Coverage

For thorough risk management, PEPs from occupied or less-recognized territories must be included in the Politically Exposed Person database.

For example, a financial institution operating in Eastern Europe utilizes a smart PEP solution to keep an eye on each PEP client from occupied regions such as Crimea or Northern Cyprus.

Including local PEPs from various districts and administrative regions within Crimea or Northern Cyprus, the organization efficiently recognizes and reduces risks linked with individuals involved in local governance and political activities that could otherwise go unnoticed.

However, multiple screening solutions do not sufficiently address these areas and their PEPs, which could leave screening procedures with blind spots.

Inefficiency With Different Languages

PEP data is released in a variety of languages and formats, which makes it challenging to coordinate data across international jurisdictions and raises the possibility of errors and false positives or negatives.

Multiple leading solution providers in the market are focused on specific countries or areas, therefore they only cover those languages and ignore the others, which results in a larger percentage of missing data with higher false positives.

Inefficient AML Data update & Flexibility

The inability to regularly update and modify screening algorithms in response to shifting definitions, PEP status, and regulatory changes can put a burden on system capacity and cause errors and delays.

Multiple screening solutions failed to update their solutions immediately for any change in PEP status, sanctioned list, or delisting which can cost millions of dollars to an institution for screening clients with outdated data.

Focused On High-Risk Jurisdiction

Certain vendors limit their focus to big international sanction lists that encompass densely populated countries while ignoring lists of less populated or localized places.

Institutions are exposed to inaccurate and ineffective outcomes that raise local regulatory concerns due to this narrow PEP data scope.

Operational Burden and False Positives

Broader definitions like those explained by FATF & EU can lead to higher false positive outcomes, while narrower definitions utilized by the U.S. or Canada may miss certain high-risk individuals.

These high false positive rates create the need for more resources for AML compliance teams to review and verify each dataset.

On the other side narrow definitions might create a smooth process but can leave gaps in screening, failing to identify some high-risk individuals.

Mostly screening solutions failed to create a balance or thus produced unauthentic and wrong data.

Now being a compliance officer you must be in search to get reliable and detailed PEP data coverage for accurate outcomes when the major AML compliance solution providers lack these features.

The answer to your search lies here; AML Watcher is the leading screening solution provider with global PEP data that not only covers the market gap in PEP coverage but also offers unique features for the future.

6 Best PEP Screening Practices That You Can Trust: AML Watcher

AML Watcher stands out in the market by ensuring thorough coverage of PEPs from all regions, including those often overlooked by legacy vendors.

AML Watcher’s comprehensive approach covers risk classification from levels 1- 4, including real-time updates and local PEP identification, ensuring thorough risk management and AML compliance.

Our PEP screening solution features include:

Broader Jurisdiction Coverage

AML Watcher offers a unique feature to cover PEP data from less recognized, controversial, occupied regions, or small islands.

Our in-house data team extracts, analyzes, and maintains all PEP information from regions like Abkhazia, Crimea, Northern Cyprus, Nagorno-Karabakh, Kashmir, Kuril Islands, and many more.

This will ensure that no high-risk individuals from these regions are overlooked, or no profile is wrongly sanctioned thus providing a detailed risk assessment for organizations.

Real-Time PEP Data Updates

AML Watcher updates its PEP database every fifteen minutes, incorporating the latest information from all regions and global regulatory sources.

These timely updates reduce the risk of undetected changes in PEP status, enhancing AML compliance and security.

This dynamic integration lowers the chances of AML compliance violations and allows financial institutions to take quick, well-informed actions without blocking client accounts.

Local PEP Data Coverage

AML Watcher successfully covers data for PEP level 4 & their associated risks that offer a quick screening of national as well as local PEPs, including regional officials and local politicians.

Detailed screening with granular data captures all relevant political figures, ensuring thorough due diligence.

Tailoring PEP Risk Levels

AML Watcher allows institutions to screen PEPs with different risk levels, based on their position, influence, and other risk criteria.

This adaptability lowers false positives and negatives and ensures that screening procedures meet the particular risk appetite of the organization.

Fit For the Smallest Jurisdictions

With its scalable screening capabilities, AML Watcher offers the PEP data to screen customers from regions with populations of any size, even smaller than 100,000 people.

Smaller financial institutions and those operating in less populous areas like Gibraltar, South Ossetia, and Transnistria will especially benefit from this functionality.

Customizable PEP Screening Parameters

With AML Watcher, institutions may customize their screening criteria to match their unique risk profiles and regulatory landscapes.

Institutions may choose their definitions from a range of regional and international standards definitions, such as the legislation of the EU and the UK, the FATF, or particular national recommendations.

- No commitment needed

- Complete AML Database at your service

- Access our all-in-one dashboard

Tier-2 PSPs in ... must demonstrate automated monitoring, layered CDD, &...

See the Full Regulatory Expectation70–80% less manual work, 95% less fatigue, TruRisk Agent makes compliance effortless.

Experience Agentic AMLMove Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries