7 Key Components of Successful Customer Screening Process in AML

Anti Money Laundering

December 30, 2024

- What is Customer Screening in AML?

- Why Customer Screening Programs are Crucial?

- Seven Components for Real-time AML Customer Screening

- Global AML Regulatory Guidelines Related to Customer Screening Checks

- The Danske Bank Case: A Failure of Customer Screening and AML Compliance

- How Does AML Watcher Improve Customer Screening Processes?

Behind the allure of high-risk customers lies a darker truth: an open invitation for money laundering to flourish.

It is observed that business relations with high-risk customers are very threatening for the institutions due to their indirect or direct involvement in financial crimes, including corruption and money laundering.

Therefore, it is necessary to incorporate an effective and AML-compliant customer screening solution to counter crimes and illegal operations in real-time.

Concerning the failures in the company’s customer screening operations, a fine of approximately £29 million was imposed on Starling Bank in 2024 by the Financial Conduct Authority.

Since this bank monitored the customers against only a limited array of criminal lists, these screening insufficiencies led to the onboarding of high-risk customers.

The inadequate sanction screening database and outdated compliance policies facilitated the account registration of more than 54,000 accounts for 49,000 high-risk customers between September 2021 and November 2023.

Therefore, understanding the significance of credible customer screening is critical for financial and non-financial institutions.

This article elaborates on What is Customer Screening and its role in assessing the potential threats and risk levels of different institutions and customers.

What is Customer Screening in AML?

Customer screening, an essential component of anti-money laundering regulations, is the practice of assessing and identifying the legitimacy and risk profiles of potential customers. As this process greatly aligns with the global AML/CFT guidelines, the main aim of screening the customers is to minimize the risks of money being laundered illegally.

Why Customer Screening Programs are Crucial?

AML customer screening offers a layer of defense when it comes to protecting firms from the harms of money launderers and terrorist financiers.

The ultimate objective of the customer screening process is to assess the client’s risk profiles and ensure that the customers meet global regulatory guidelines.

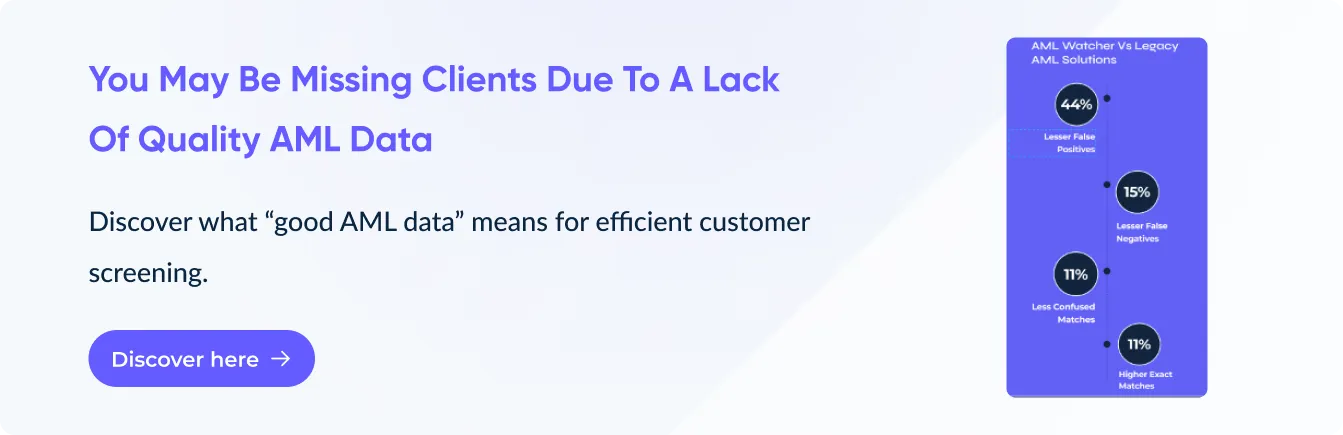

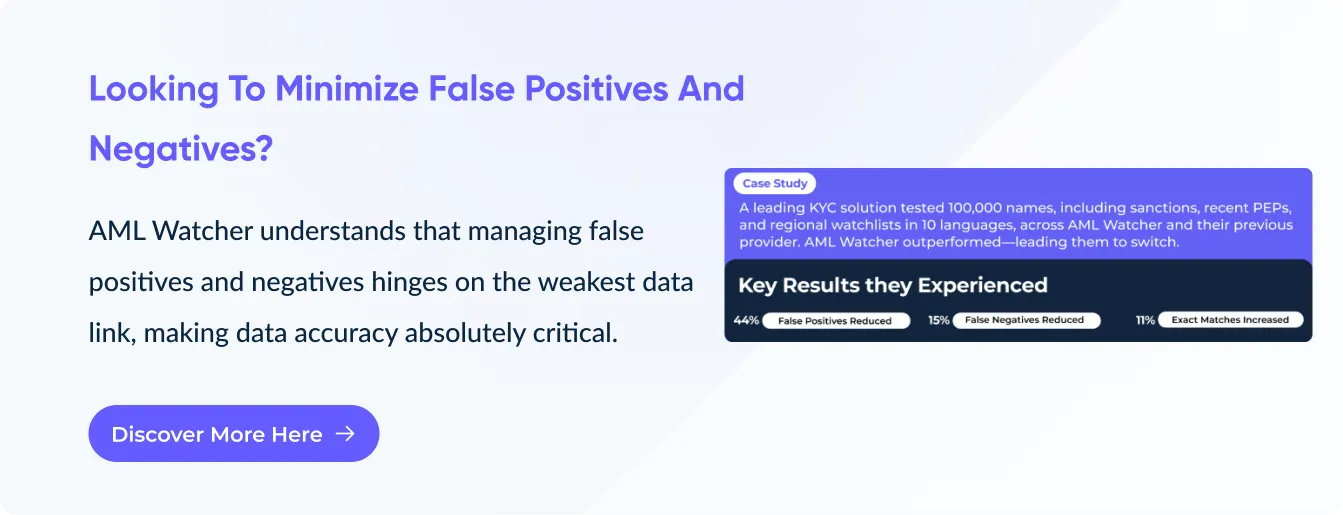

The effective screening of customers’ risk profiles requires institutions to access reliable data sources to get accurate and credible outcomes. Obliged entities can significantly reduce the instances of false positives and negatives by ensuring data extraction from credible sources.

Furthermore, some of the best practices of the customer screening process revolve around the following factors:

- The AML customer screening process must proceed through a risk-based approach. This entails the categorization of customers according to their risk levels, ensuring enhanced due diligence for customers with higher risks and simplified due diligence for clients with lower risk levels.

- Quick checks that are backed by reliable data sets must be utilized during the customer screening process. This ensures that the updated customer data is assessed to enhance the credibility of the risk profiling.

- The assurance of continuous screening audits is essential to ensure that the screening checks comply with the latest regulatory benchmarks. Therefore, routine audits help businesses assess the customer’s suspicious activities, which are crucial to mitigating money laundering and corruption activities.

Curious about the critical customer screening components? Continue reading this article to get all your required information regarding AML customer screening.

Seven Components for Real-time AML Customer Screening

Monitoring, tracking, and proactively screening individuals and organizations is essential for assessing consumer risk profiles and possible involvement in illegal financial activities.

Assessing a client’s financial risk patterns and their presence on multiple watchlists or sanction lists gives compliance officials an accurate understanding. This helps establish if maintaining long-term partnerships with such customers is consistent with predefined corporate risk management principles.

As per the Financial Action Task Force in its 12th recommendation, businesses must emphasize the detailed screening of all the PEPs and their relatives through EDD measures.

A quick glimpse of the essential components of AML screening is provided below:

1. Ongoing customer due diligence (CDD)

After onboarding, organizations must continue to review and update client information to maintain accuracy and compliance.

This includes tracking changes in their preset risks and possible criminal activity status. Regular customer due diligence guarantees that the client remains in compliance with rules and detects any growing hazards.

2. Enhanced Due Diligence (EDD)

If differences are discovered in updated information or if new risks emerge throughout the engagement, Enhanced Due Diligence must be performed.

This procedure entails a thorough investigation of the customer’s assessment, business relationships, and transaction history. EDD is critical for managing high-risk consumers and staying compliant with changing regulatory regulations.

3. Sanction Screening

Customer names are checked against worldwide sanctions lists as part of the screening process. These lists cover persons, corporations, and governments that have been sanctioned internationally.

If a consumer is directly or indirectly related to a sanctions list, they must go through EDD to determine their risk rating and compliance status.

4. Global PEP Screening

Businesses must assess whether a consumer is a politically exposed person (PEP). This classification might emerge from a political function, title, or intimate affiliation with someone in a political position.

As global political situations change, organizations must frequently update their tests to reflect changes in PEP status.

5. Watchlist Screening

Customer information is cross-referenced through watchlist screening, including global and FBI Watch list, against databases of persons, corporations, and entities labeled for criminal activity, sanctions violations, or other high-risk behaviors.

Regularly updating and screening against these lists ensures that organizations discover and manage risks connected with prohibited or suspect entities while remaining compliant with regulations.

6. Adverse Media Screening

Besides sanctions and PEP lists, firms must continually watch the local and international media for bad news about their clients.

Adverse media screening may reveal links to criminal activities or high-risk conduct. Effective screening requires tracking news in multiple languages and staying up to date on changing global events to guarantee accurate assessments.

7. Ongoing Monitoring

Customer screening is an ongoing procedure. Businesses must constantly monitor their clients throughout the relationship to discover any changes in their situation, developing threats, or updates to worldwide sanctions and watchlists.

Ongoing monitoring helps to maintain compliance and efficiently handle any risk.

Global AML Regulatory Guidelines Related to Customer Screening Checks

The global AML regulatory guidelines ensure that the institution’s customer screening checks perfectly line up with the country’s AML regulations. Considering these rules, a few of the major recommendations and their importance are discussed below:

- According to the 6th and 7th recommendations, the organizations are required to comply with the screening laws established by the United Nations Security Council Resolutions (UNSCRs).

As per this regulation, businesses are required to screen the customers thoroughly against the international and domestic sanction databases. Moreover, the 12th recommendation emphasizes the significance of PEP screening during customer risk management.

- Under the 5th AML Directives and 6th AML Directives formulated by the European Union, institutions must prioritize customer due diligence and PEP screening.

The primary goal of the CDD process is to screen the entities against the global sanctions and PEP lists. The continuous monitoring of the customer’s financial operations is highlighted under client screening.

- In light of Section 326 of the USA Patriot Act, customer screening is mandated to combat money laundering operations. Businesses are required to streamline the screening of customers against the OFAC sanction lists and identify the risk levels.

- As per the AML guidelines proposed by the FinCEN, institutions are required to ensure compliance with the Bank Secrecy Act while screening the customers against the sanction lists maintained by the Office of Foreign Assets Control (OFAC).

The compliance officers are prompted to examine the financial uncertainty levels of all the entities during the customer screening procedures to counter critical money laundering instances.

Are you looking forward to understanding the complexities of ignoring the AML customer screening protocols? Continue reading the article to get a further overview.

The Danske Bank Case: A Failure of Customer Screening and AML Compliance

Danske Bank, Denmark’s largest financial institution, declared guilty to bank fraud conspiracy and agreed to pay a $2 billion fine in 2022 after misleading US banks about its anti-money laundering (AML) controls.

Between 2008 and 2016, Danske Bank’s Estonian office handled $160 billion in suspicious transactions for non-resident customers, especially Russian clients, by misrepresenting AML compliance and hiding transaction details.

AML Compliance failure

The fraud was based on poor transaction monitoring, fake client risk profiles, and the use of shell organizations.

Despite internal audits and whistleblower reports identifying these flaws, Danske Bank tricked US institutions into maintaining access to US currency deposits.

The settlement includes $850 million to cover simultaneous investigations by the SEC and Danish authorities, stressing worldwide enforcement cooperation.

Remediation and Monitoring

Danske Bank will revise its AML compliance procedures as part of the plea agreement, cooperate with continuing investigations, and undergo evaluation by an independent expert.

This case emphasizes the necessity of thorough customer screening, strong AML measures, and adherence to US financial system legislation.

Notably, compliance with the customer screening modules results in the identification of risky financial activities in the real-time frame.

How Does AML Watcher Improve Customer Screening Processes?

AML Watcher’s comprehensive features are intended to meet every aspect of customer screening while also ensuring continuous monitoring with worldwide regulatory compliance and effective risk management.

Explore how each feature directly helps AML Customer Screening;

Comprehensive Watchlist & Sanction Screening

- Checks customer information against worldwide databases of sanctions, watchlists, and politically exposed individuals (PEPs).

- Identifies high-risk businesses and persons based on real-time updates from over 1,300 global watchlists and 200+ sanction regimes.

Reduces false positives and minimizes regulatory exposure, improving customer screening efficiency.

Simplified PEP Screening

- Categorizes and screens PEPs across risk levels 1 to 4, with a focus on high-risk individuals linked to corruption or financial crimes.

- Screens Politically Exposed Persons (PEPs) and their close relationships from conflicted and disputed regions, addressing risks tied to political instability and money laundering.

- Access Data for jurisdictions with populations under 100,000, ensuring comprehensive compliance even in overlooked areas.

- Provides real-time monitoring and alerts, notifying compliance teams of PEP status changes for quick action.

Adverse Media Screening

- AML Watcher scans global media sources, including local and regional outlets, to detect negative news that might implicate customers in financial crime or unethical activities.

- Conducts sentiment analysis and categorization for easy risk assessment.

- Supports multilingual media monitoring to capture news across diverse geographies.

- Alert compliance teams about emerging threats in real time.

Continuous Monitoring

- Continuous monitoring ensures that client profiles are up to date with the most recent risk information, such as updates to sanction lists, unfavorable publicity, or PEP status.

- Re-screens consumer data at predetermined intervals.

- Sends real-time warnings for any status changes, allowing institutions to respond quickly to emerging threats.

Advanced Name Matching

- AML Watcher uses powerful name-matching algorithms to detect sanctioned persons and entities, even if their names contain variants, aliases, or transliterations.

- Reduces false positives while ensuring that no high-risk persons or businesses are overlooked.

- Improves AML customer screening accuracy, allowing for speedier decision-making.

Custom Fuzzy Logic for Accurate Detection

- The platform utilizes customized fuzzy logic matching to find partial or approximate matches in customer data.

- Detects risks that typical exact-match algorithms may overlook.

- Customizable parameters allow firms to fine-tune the system to meet their specific compliance requirements.

Customized Risk Scoring

- AML Watcher enables institutions to establish risk thresholds depending on their industry’s specific compliance needs and risk appetite.

- Prioritizes notifications and evaluations of high-risk instances.

- Ensures compliance workflows are in line with industry-specific requirements.

- The customized “Add List” option allows institutions to add proprietary or industry-specific watchlists into the Customer Screening system.

- No commitment needed

- Complete AML Database at your service

- Access our all-in-one dashboard

Tier-2 PSPs in ... must demonstrate automated monitoring, layered CDD, &...

See the Full Regulatory Expectation70–80% less manual work, 95% less fatigue, TruRisk Agent makes compliance effortless.

Experience Agentic AMLMove Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries