AML in Insurance: A Fight Against Money Laundering

Money Laundering

July 9, 2025

- What is Money Laundering in Insurance?

- What are the Ways to Launder Money in the Insurance Sector?

- Top Factors Contributing to Insurance Vulnerability

- Influence of Regulatory Enforcements on the Insurance Sector

- AML in Insurance – Know the Rising Regulatory Scrutiny

- How Insurers Can Respond to Emerging Money Laundering Risks?

- How AML Regulations are Applied to the Insurance Sector?

- Enhance AML Compliance for Insurance with AML Watcher

What if the seemingly low-risk insurance sector is quietly enabling high-risk money laundering schemes?

Criminals are exploiting the insurance sector to legitimize their ill-gotten gains by making premium payments for insurance and annuity contracts.

While legitimate payout typically occurs through maturity, death benefits, or a scheduled series of payments, imposters rarely wait; instead, they often withdraw the amount during the cooling-off period or by surrendering the policies early.

So, what are the red flags of early withdrawal and policy surrender that an insurance business should be looking out for, and how does continuous monitoring help in identifying these complex money laundering patterns?

Let’s get into this article to understand the solid reasons behind money laundering in the insurance sector.

What is Money Laundering in Insurance?

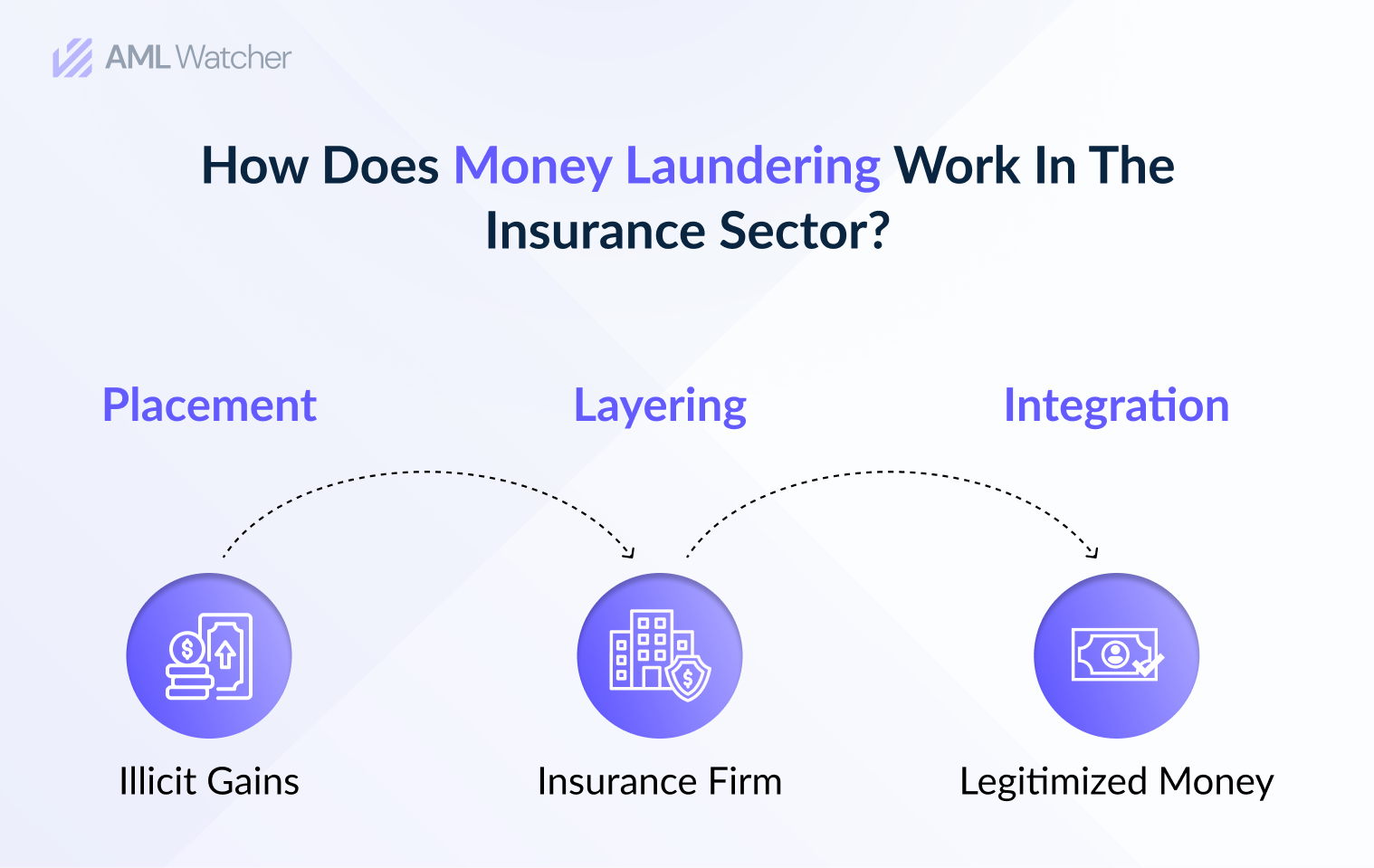

Money laundering in insurance is actually a process in which the origins of illicit gains are concealed by channeling them through insurance products and transactions.

The major objective behind this is to make illegal money appear legitimate by finding out vulnerabilities in the insurance sector.

Policies that hold redeemable cash values are more exposed to money laundering. For instance, illegal money can be utilized to purchase a policy.

Where the dirty money stays within the AML insurance company systems, and when the policyholder receives the payment, it appears to originate from an authentic source.

This complex layering process makes it difficult for the authorities to trace back the original crime, posing a massive challenge for the AML efforts.

Why Do Criminals Mostly Select the Insurance Sector for Money Laundering?

Criminals mostly choose the insurance sector for the following reasons:

- The insurance sector includes large sums of payments, which makes it attractive to launder huge illegal funds for criminals.

- Some of the products in the insurance sector are complex; they enable layers of transactions that mostly hide the origins of funds.

- Life insurance policies are mostly sold with the help of brokers and agents who are unaware of effective AML controls and are likely to be involved with criminals.

What are the Ways to Launder Money in the Insurance Sector?

Money launderers use several ways to legitimize their illicit gains; some of the most commonly used methods are:

Single-Premium Insurance Policy

Single-premium insurance policy is a tactic in which money launderers channel huge sums into a single transaction to conceal the money’s unlawful origin, and later on, they ask for a refund.

The refund that they receive from the companies is now clean because it came from an authentic business.

Third-Party Involvement

Money launderers add a third party within the payment-related processes, such as for paying the insurance premiums or receiving the payouts from the policies.

This automatically adds a complex layer that makes it difficult for the authorities to trace the illicit funds.

Policy Loans

The criminals use their illicit gains to pay for an insurance policy that builds up a high cash value with the passage of time. They then borrow money directly from the insurance company, against the cash value built within the policy.

Although the money that the criminals get is technically a loan, it looks to be from a legitimate source, successfully “cleaning” the illegal funds.

Fraudulent Claims

Criminals fake an injury or prolong their injuries to claim an insurance payout. The payment they receive from that claim is now legitimate income, even though it came from a fraudulent act.

Top Factors Contributing to Insurance Vulnerability

As per Financial Action Task Force (FATF) recommendations, the core money laundering vulnerability in the insurance sector originates from policies that:

- Allow cash holding for a long time (for instance, life policies or annuities)

- Enable early withdrawals

- Transferable to third parties

Criminals can easily exploit these features by:

- Using illegal cash payments to purchase policies

- Precanceling of policies to obtain “clean” refunds

- Disguising ownership using third parties and nominees.

When the customer receives payments, it completes the layering and integration stages of the money laundering process. Normally, these payments came at a scheduled payout or after the policyholder’s death, as a legal asset.

Influence of Regulatory Enforcements on the Insurance Sector

Globally, regulatory bodies recognize the risks related to anti-money laundering in the insurance sector, particularly for products associated with life and investment. To address this,

- FATF recommends that the insurance sector must implement a risk-based approach.

- FinCEN in the US mandates AML programs for certain insurers and has issued advisories on suspicious activity reporting (SAR).

- The European Insurance and Occupational Pensions Authority (EIOPA) publishes regular AML risk reports for insurers.

- The Financial Conduct Authority (FCA) addresses insurance AML risks, and it fined JLT Specialty Limited (JSTSL), an insurance intermediary, over £1.8 million for an unacceptable approach to bribery and corruption when making payments to overseas third parties.

- The Office of Foreign Assets Control penalized Chubb Limited and AXA Equitable for underwriting insurance policies that violated the Cuban Assets Control Regulations (CACR).

These examples show how enforcement actions are imposed on the insurance sector and demonstrate that insurers must comply with AML and sanctions regulations to protect their business and sustain growth.

AML in Insurance – Know the Rising Regulatory Scrutiny

The insurance sector is facing heightened regulatory scrutiny globally regarding anti-money laundering compliance due to the inherent AML risks in its complex financial products.

Here is a list of regulatory bodies that have the same focus:

How Insurers Can Respond to Emerging Money Laundering Risks?

With the constant growth of risks, insurers must respond to emerging threats in a certain way:

Implement Adverse Media Monitoring

Geopolitical risks, cyberthreats, and AML regulatory complexities for insurers are rising with the passage of time.

To achieve measurable success in these matters, insurance firms are advised to integrate systems with early warning signals through ongoing adverse media monitoring on their partners, customers, and shareholders.

Insurers can protect their capital reserves before any financial or regulatory impact by taking such initiatives.

PEP and Sanctions Screening for Third-Parties

Third-party visibility can be a beneficial factor in terms of creating trusted B2B and B2C bonds. Insurers must screen third parties against global sanctions and political exposure.

These anti-money laundering insurance strategies can assist the insurers in gaining instant visibility into third-party reputational threats, ensuring adherence to global regulatory standards and board-level reporting requirements.

Ongoing Monitoring

To take the element of effective AML in the insurance sector, insurers must conduct ongoing monitoring, which offers timely alerts on partners or customer risk profiles. Insurance businesses can automatically get the latest updates on whether their client is sanctioned or hit by a headline.

How AML Regulations are Applied to the Insurance Sector?

Life and annuity insurance companies are designated as obliged entities as per global AML regulations.

The life insurance sector with investment components or cash surrender values carries higher risk as compared to other general ones, such as car and home insurance, which usually pose lower risk.

To adhere to the evolved regulations, insurance firms must fulfill the following requirements:

Enhance AML Compliance for Insurance with AML Watcher

For those who want to join the ranks of forward-thinking insurers! AML Watcher is here to support you.

Its unmatched data coverage against 2.6 million+ PEP profiles, 215+ sanction regimes, and 3500+ global watchlists updated every 15 minutes assists your insurance firms in spotting risks related to customers and partners early.

Therefore, businesses can take proactive measures and minimize the false positives by 44%.

So, what are you waiting for? Take action now! Strengthen your defenses and ensure regulatory compliance.

Frequently Asked Questions

Companies working in the insurance industry must integrate risk-based programs, trace transactions, report suspicious activities, and conduct customer due diligence.

Money launderers mostly employ the following strategies to legitimize their illegal payments through the insurance sector.

- Premium overpayments

- Complex ownership and beneficiary structures

- Early policy surrender

- Third-party transactions

- Use of shell or fake companies

Move Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries