AML Watcher Face Biometric AML: Revolutionizing the Fight Against Financial Crime with Face matching

Others

November 15, 2023

The pace at which biometric scanning and verification is evolving is commendable. As per the Fortune Business Insights, the global biometric system market is projected to grow at a CAGR of 13.9% in forecast period 2022-2029, from $30.77 billion in 2022 to $76.70 billion by 2029. This is also indicative of how technological expansion has further caused a change in the framework of how AML/CFT systems work. Facial scanning, facial screening, iris scanning and fingerprint scanning all fall underneath the world of biometric verification and scanning. However, in the case of biometric AML, it can be essentially described as a facial screening tool. These enhancements have made the sanctions screening less difficult, less expensive, free from persistent errors along with false positives and negatives, and more efficient. According to a research conducted by Cornell University, the use of biometrics can reduce false positives in AML systems by 80% while detecting over 90% of true positives. Consequently, this has in addition endorsed financial institutions and regulators to select biometric solutions of their AML approaches. While this tool gives its very own challenges, a door stays open for insurance agencies, banks and investment companies to discover its viability and the way it could be integrated or included into their systems. This tool has certainly demonstrated to be an exquisite paradigm shifter in saving financial structures and contributors from monetary fraud and crimes.

Biometric technology isn’t simply restricted to compliance. Various industries, which majorly pertain to everyday life have integrated biometric verification systems to make sure ease and comfort for the customers. Moreover, all the industries require safety in their underlying tactics, consequently the adoption of the biometric verification tools. Let’s read through its applications in such sectors.

Current Biometric Applications

- In digital devices, it’s visible how biometric technology has taken a crucial position in improving safety. It enables verification and unlocking of the devices through face recognition and fingerprint. Take as an example Apple’s Face ID and Touch ID which aren’t only handiest used for authenticating and unlocking gadgets but for the verification of payments too.

- In healthcare, biometric statistics assists in affected person identification and personalized treatment plans. For example, palm vein recognition is utilized in a few hospitals for patient registration.

- In an attempt to substantially reduce wait times, airports make use of biometric verification by making the boarding process and safety checks easy and accurate. For instance, Biometric passports, which consist of a chip with the holder’s biometric statistics, presently are famous in many nations.

- Additionally, inside the realm of private security and domestic structures, biometrics like voice and facial recognition have turned out to be really beneficial.

As evident by the practices above, biometric verification tools have been able to make the technological panorama fairly efficient in terms of customer experience, security and operational productivity. This suggests that biometrics go beyond the mere applications of compliance and regulation.

Now let’s discuss the role of biometric technology in the KYB and KYC industry.

Face Biometric Technology in KYC and KYB

For a very long time there have been inevitable inefficiencies and lack of good security in traditional Know Your Customer (KYC) and Know Your Business (KYB) practices. With the introduction of biometric technology involving image processing or facial recognition systems, both of the aforementioned industries have been revamped in a sense that the procedure of customer onboarding has been made more efficient, smooth, and more secure. This is backed up by a report published by McKinsey & Company which suggests that there has been a surge in the trend of financial institutions integrating face scanners into their systems solely for the purpose of customer onboarding.

Furthermore, in order to alleviate the resources and time spent on manual checks, biometrics have enabled verification through face analysis which has further led to a better and augmented approach towards due diligence. As opposed to the traditional ways of KYC and KYB in the financial sector which heavily rely on physical documentation, face analyzers like biometric scanners have made the processes fraud and risk free and have reliably minimized the threats of identity theft.

Next let’s have a look at how current Anti-Money Laundering (AML) practices face several demanding situations and obstacles, which particularly stem from their dependence on conventional, and mostly out of date strategies.

Current Industry Practices and Limitations in AML

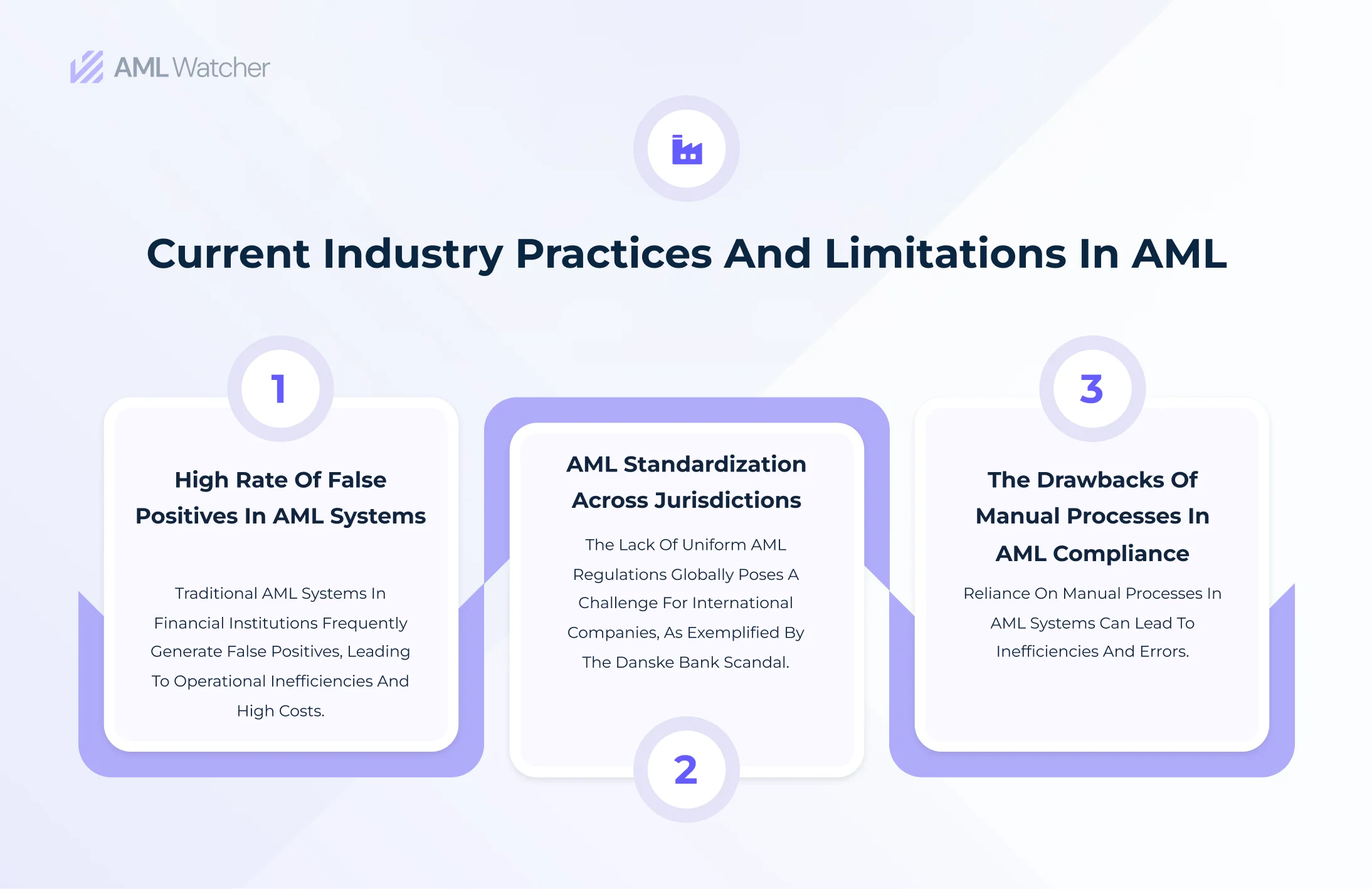

High Rate of False Positives

One biggest challenge which banks and other financial institutions face repeatedly with traditional AML systems is the occurrence of false positives which not only lead to operational inefficiencies through skewed resource allocation but also incur heavy costs for the firms. This is evident by the fact that in order to counter false alerts, large banks annually spend $500 million on average. Although this sum is spent on adhering to regulatory requirements and compliance procedures, most of it goes to mollifying the effects of false alerts. This is better explained by a study by Thomson Reuters which explains that 95% of the false alerts prompted in AML systems are all false positives. This conundrum is further aggravated by the invention of advanced and complex technologies in the finance industry, like the use of cryptocurrencies, which makes it challenging for the AML systems to keep up with the evolving trends.

Lack of Standardization

Adhering with AML regulations across various jurisdictions is no less than an austere task for companies which are operating internationally. This is primarily because the AML regulations are not uniform in all the regions around the world. To top it up, GDPR clearly disallows sharing of sensitive and confidential financial information because of the prevailing privacy concerns. Such laws do not allow freedom of sharing information, specially across multiple jurisdictions and add to the challenges of global businesses. This is highlighted by The Danske Bank scandal in which around €200 billion of transactions could not be traced which originated from the Estonian branch of the bank. This inability to trace this huge amount was attributed to the varying AML rules and regulations in both Estonia and Denmark resulting in an oversight.

Reliance on Manual Processes

Any process or practice involving manual care is prone to inefficiency and human error. Speaking from the perspective of an AML system where updating information plays a key role, manually reporting suspicious activity can not only slow down the overall process but also lead to larger errors, causing massive harm to those involved. The problem with manual processes surfaced in the case of Commonwealth Bank of Australia where due to a coding error caused by a manual lapse in its transaction monitoring system, 53,000 transactions went unreported timely. This made the bank pay a whopping fine of AUD $700 million signifying how crucial it is for the banking sector to adopt more advanced AML systems which are fully automated with minimum human intrusions.

We just studied the limitations in the AML practices. It’s imperative to understand how these gaps in the AML industry can be filled with the adoption of biometric technology which specifically involves face matching.

Bridging the AML Gap with Biometric Face Matching

- With financial crimes becoming more sophisticated and hard to detect, integration of biometric tools in AML systems is becoming all the more imperative. Currently, there is a gap in the adoption of technologies pertaining to face analysis in the AML industry which has led to many critical fraudulent and suspicious entities slipping away. The European Union’s Fifth Anti-Money Laundering Directive (5AMLD), which came into effect in January 2020, opened the door to more digital solutions, including biometrics, in proper consumer vetting.

- As suggested by the limitations above, businesses loathe spending huge sums on operational costs and fines resulting from errors like false alerts. Hence, accuracy, faster onboarding, and detection of frauds timely in the AML industry becomes all the more crucial. This need prompts the adoption of face matching technology to not just detect but to alleviate financial fraud greatly.

- In the conventional AML procedures, specially in the sanctions screening process, the use of names and other unique identifiers is a common practice. This leads to a persistent problem of false positives or negatives because of common names, different spellings, or aliases. With the adoption of face matching technology, the chances of false negatives and positives are eliminated to a great degree because the the faces of the clients are directly being matched with the faces of fraudulent or sanctioned individuals in the database.

Discussing the future changes in the industry related to biometric Anti-Money Laundering (AML) technology involves several aspects. Let’s talk about them.

Future of Bio AML in AML/KYC

Market Growth and Technological Advancements:

The global AML software solution market, encompassing technologies like transaction monitoring systems and customer identity management systems, is projected to reach $3.5 billion by 2027, growing at a compound annual growth rate of 16% from a 2018 baseline. This growth is fueled by technological enhancements, including biometrics customer sign-ups and e-signing partnerships, as evidenced by companies like DocuSign expanding partnerships with digital identity providers.

Effective Fraud Prevention:

Biometric AML technologies have shown effectiveness in fraud prevention. For instance, Shufti Pro’s identity verification software, using an advanced neural network, prevented $1.3 billion in fraud attacks against businesses in the first quarter of 2023 alone. This demonstrates the potential of biometrics in enhancing AML systems’ accuracy and security.

Application in Banking:

Banks are increasingly adopting biometric technologies for AML and fraud protection. Facia’s facial biometric verification technology, for example, helps banks verify online users against trusted photo IDs, offering protection against presentation attacks and digitally injected attacks. This technology not only reduces the risk of fraud but also streamlines customer onboarding, thereby increasing efficiency.

AI and Machine Learning Integration:

The integration of AI and machine learning is crucial in enhancing AML programs. These technologies assist in customer onboarding by verifying identities in real-time and detecting fraudulent documents. AI improves ongoing transaction monitoring by scanning large data sets, thereby enhancing the recognition of customer risks and reducing the time and costs involved in compliance processes.

While technology advancements offer numerous benefits, challenges persist, particularly in infrastructure and compliance.

Challenges and Compliance:

The existing AML systems, mostly developed in the 2000s, struggle to handle the current scale of data and demand. Therefore, balancing technological innovation with privacy, ethical considerations, and legal compliance remains a critical aspect.

Concluding Thoughts

The AML/CFT systems have greatly been improved with time with the integration of biometric verification systems which have brought features like face matching, face analysis, face scanning, iris scanning etc. These features have not only minimized operational costs for the businesses but have also greatly enhanced the accuracy in fraud detection of the entire AML system which is representative in the expansion of the biometric system market. The market is expected to grow from $30.77 billion in 2022 to $76.70 billion by 2029. The adoption of biometric technology is further accentuated by the study conducted by Cornell University which suggests that face similarity tests can detect 90% true positives and can also reduce false positives by 80%. This is a huge breakthrough for the stakeholders of financial institutions which majorly include banks. This tool is also revolutionizing customer onboarding in the KYB and KYC industry. However, AML practices face challenges related to high false positive rates, manual processes, and lack of juridical standardization in AML laws. This makes integrating facial biometrics into AML essential, as the EU’s 5AMLD promotes digital solutions for customer efforts. The face matching feature provided by AML Watcher specially makes the sanctions screening process more efficient and foolproof. The inevitable challenges which result because of name scanning can be eliminated greatly with the face matching technology AML Watcher offers.

Contact us to modernize AML practices and enhance financial security while balancing innovation and privacy.

- No commitment needed

- Complete AML Database at your service

- Access our all-in-one dashboard

Tier-2 PSPs in ... must demonstrate automated monitoring, layered CDD, &...

See the Full Regulatory Expectation70–80% less manual work, 95% less fatigue, TruRisk Agent makes compliance effortless.

Experience Agentic AMLMove Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries