Essentials of AML Compliance For Banking as a Service (BaaS) Model?

AML Compliance

April 23, 2025

Is Revolut’s €3.5 Million Fine a Clear Warning for BaaS Providers?

In April 2025, Lithuania’s central bank fined Revolut €3.5 million for deficiencies in its anti-money laundering (AML) controls. While no confirmed instances of money laundering were found, the central bank noted that Revolut occasionally failed to identify suspicious monetary operations effectively.

Revolut has since cooperated with authorities and taken steps to address the identified procedural issues.

Imagine the Fintech growing exponentially, but faces financial penalties due to inadequate AML checks. That’s why every party to a BaaS partnership must implement a detailed AML compliance program, which should be defined in each contract.

But the key question arises here: How can institutions circumvent becoming the next cautionary tale in the world of Banking as a Service (BaaS)?

In the BaaS framework, implementing effective anti-money laundering measures is the need of the hour to prevent fines and penalties.

As per the Office of the Comptroller of the Currency (OCC) guidelines, banking service providers in the USA must adhere to the BSA’s anti-money laundering compliance programs and screen the entities against government lists to counter money laundering offenses.

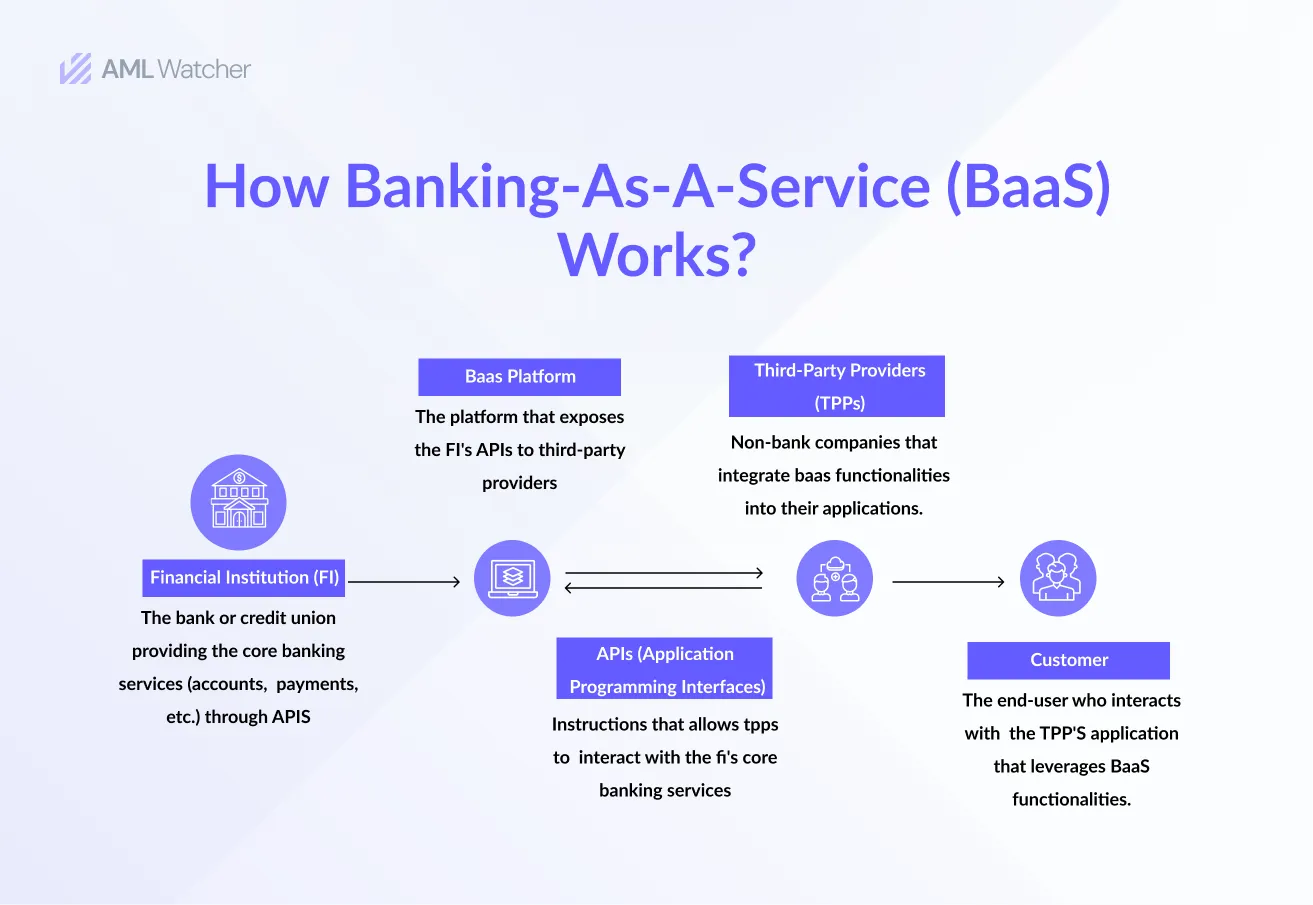

Interested in understanding how banking as a service fintech operates and how the significance of AML in banking is ensured? Let’s examine the banking-as-a-service definition in the next section to get a hands-on understanding of the subject.

What is Banking as a Service (BaaS) Model?

Banking as a service (BaaS) has emerged as a prominent partnership practice in the financial framework, allowing non-banking institutions to offer digital banking services through strong collaboration utilizing the Application Programming Interface (APIs).

The BaaS model allows non-bank institutions, such as fintechs, to offer financial products by utilizing existing banks’ infrastructure, which includes account opening, payment processing, and lending, without the need for additional infrastructure or costly banking licenses.

For Sponsor Banks

Sponsor banks that provide a BaaS solution open up new markets, acquire access to previously unreachable consumers, and generate money through deposits and service charges for fintech partners.

AML Compliance Essentials in the BaaS Model

The regulatory assessment of this partnership is pivotal to ensuring risk-free banking services and efficient third-party risk management since the sector can be targeted for potential money laundering risks.

This includes adhering to required regulatory and AML compliance guidelines across the BaaS platforms while managing risk-free operations.

BaaS, driven by its capacity to streamline the provision of financial services to non-banking institutions, is anticipated to acquire a $64.7 billion market value by 2032.

In the constantly changing regulatory environment, failing to meet the bank AML standards can pose several challenges for all parties involved.

Some of the emerging regulatory challenges that come along the way are:

- Managing and ensuring compliance with third-party service providers, especially when they play a critical role in the BaaS ecosystem, is a growing challenge.

- Maintaining transparency and ensuring accurate and timely regulatory reporting can be resource-intensive, especially when dealing with complex data.

- Different regions and jurisdictions have varying regulatory standards, making it challenging for BaaS providers to maintain consistent compliance across borders.

- Ensuring Know Your Customer (KYC) and Anti-Money Laundering (AML) regulations are effectively integrated into the BaaS platform without compromising speed or customer experience.

- Need to ensure compliance with global sanctions and watchlists and conducting thorough screening for cross-border transactions adds another layer of complexity for BaaS providers.

Due to these regulatory challenges, BaaS providers are required to ensure compliance with stringent AML guidelines. Some of these regulatory frameworks are overviewed below:

Comprehend the Regulatory Framework of BaaS Solutions

The understanding of the AML regulations in BaaS is about examining the risk profiles of third parties offering fintech solutions to combat money laundering offenses.

As per FinCEN’s AML/CFT program amendments, “If a bank considers expanding into a BaaS relation and offers products or services to new customers through fintech partners, the institution is expected to refresh its risk assessment measures as per AML guidelines.”

BaaS providers are expected to oversee the banking regulations proposed by major regulatory bodies to counter suspicious financial operations.

Any fintech firm that directly or indirectly operates with a bank is subject to the same regulators who oversee the Financial Service Compliance requirements of the banking institutions.

“Amid recent scrutiny and enforcement activity in the banking-as-a-service (BaaS) space, federal regulators have issued a joint statement reiterating the importance of banks’ oversight of certain third-party relationships through effective risk management practices.”

Thereby, it is necessary to stay informed of certain regulatory actions involving:

- AML compliance in BaaS mandates the fintech to follow stringent compliance with the sanctions imposed by the concerned authorities, such as OFAC in the United States. This is to ensure the prohibition of illegal transactional activities conducted by sanctioned entities or customers through the BaaS servers.

- In USA, the Consumer Financial Protection Bureau (CFPB) is required to oversee the BaaS operations, ensuring that consumers are being treated fairly by the entities offering financial products. CFPB aims to stimulate consumer protection across all banking and Fintech sectors.

- Baking-as-a-service providers are required to address the threats through a proactive approach, including the involvement of thorough risk assessment and effective due diligence checks to counter sanctions and residual risks.

Wondering how does banking as a service work? This infographic highlights its exact mechanism:

Check the Examples of Banking as a Service Failures

Over the recent banking timeframe, several BaaS examples have emerged that are linked to compliance failures and non-regulated banking operations. Below is an overview of a major BaaS failure that emerged due to non-regulated operations:

Collapse of Synapse BaaS Model

Synapse Financial Technologies, founded in 2014, was an American BaaS provider that went bankrupt in 2024 due to its non-regulated service provision. Over the course of its operations, the provider has supported more than 18 million end users through its fintech services.

According to a report, several internal technical deficiencies and compliance concerns led to the operational challenges. Additionally, Synapse struggled to ensure compliance with the banking regulations, leading to a financial shortfall of $85 million in customer funds.

As a result of these shortfalls, thousands of users lost access to their funds, which ultimately forced them to acquire alternative BaaS solutions.

In response to these gaps, the Federal Deposit Insurance Corporation (FDIC) mandated the BaaS provider to strengthen its recordkeeping requirements for fintech partnerships to ensure credible consumer access to funds and mitigate regulatory shortfalls, which is crucial to mitigating money laundering and terrorist financing activities.

Let’s now examine the BaaS failures that have emerged due to non-regulated activities in the next section:

Best Practices for AML Screening in BaaS

Money laundering and financing of terrorist activities have been the major obstacles that make the BaaS models vulnerable to regulatory loss. Therefore, any licensed fintech provider seeking to implement compliance-ready BaaS solutions must understand some components.

Following these best practices may help BaaS providers and their fintech partners efficiently handle compliance risks, protecting the security and integrity of their financial services.

For BaaS Providers

-

Conduct Comprehensive Risk Assessments

Conduct company-wide assessments to determine and evaluate compliance risks related to BaaS partnerships and end users.

-

Implement Robust AML checks

Detect customer risks, conduct background checks, monitor criminal history, and apply enhanced due diligence for high-risk individuals or entities.

-

Perform Regular Rescreening

Continuously monitor transactions and customers against sanctions lists, watchlists, PEP data, and adverse media sources to detect changes in risk profiles.

-

Maintain Vigilant Transaction Monitoring:

Screen all transactions against sanctions lists and watchlists, utilizing automated tools to enhance accuracy and efficiency.

For Fintech Partners

-

Establish Compliance Readiness

Implement AML and KYC screening processes to ensure alignment with regulatory requirements.

-

Maintain Open Communication

Collaborate with BaaS providers on compliance matters to address potential risks and ensure adherence to legal standards.

BaaS models provide a handful of financial growth opportunities for the non-banking sector through their global financial offerings.

When it comes to maintaining streamlined regulatory compliance, BaaS and fintech service providers must outsource KYC/AML screening services from trustworthy compliance partners.

How AML Watcher Supports Effective BaaS Compliance?

Accuracy, global coverage, and streamlined anti-money laundering controls are the value propositions that create a competitive advantage for BaaS in this continuously evolving environment.

AML Watcher’s enhanced risk screening approach allows BaaS providers or all entities involved to stay ahead of potential money laundering scams in real-time.

How?

- Performs real-time risk assessments of clients and entities, identifying potential money laundering and fraud risks.

- Seamlessly integrates AML screening into the BaaS systems, comparing customer profiles against 230+ global sanctions lists, 2.6m PEP data, 3500+ watchlists, and 50,000+ adverse media sources.

- Offers comprehensive proprietary data which is easy to customize in line with the risk appetite and risk exposure of Baas Provider.

- Supports screening in 80+ languages with data covering 235+ countries, helping BaaS providers maintain compliance across diverse jurisdictions.

- Offers customized compliance solutions tailored to meet the global AML regulatory requirements of BaaS providers and fintech partnerships.

- Customizes risk parameters based on customer profiles and geographic regions for more precise screening.

- Automates alerts to notify stakeholders of potential high-risk activities, enhancing response times to compliance issues.

- Minimize false positives by leveraging advanced algorithms and diverse data sources, improving risk detection accuracy.

- Provides real-time customer data access through optimized API integration, streamlining workflows without manual data transfers.

- Generates detailed, easy-to-read reports, simplifying audits and ensuring compliance documentation remains up to date.

- No commitment needed

- Complete AML Database at your service

- Access our all-in-one dashboard

Tier-2 PSPs in ... must demonstrate automated monitoring, layered CDD, &...

See the Full Regulatory Expectation70–80% less manual work, 95% less fatigue, TruRisk Agent makes compliance effortless.

Experience Agentic AMLMove Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries