Exploring Fraud Triangle Theory & the Wirecard Scandal

Fraud Prevention

March 4, 2025

Ever wonder why even people with good moral compass commit fraud? What turns trustworthy individuals into fraudsters?

Financial fraud alone causes the global economy to suffer a financial loss worth more than $5.38 trillion as per the 2021 report.

This enormous portion of the world economy could have been used to strengthen communities and help the 700 million people (8.5 percent of the world’s population) who, according to the World Bank, live in extreme poverty, earning less than $2.15 a day.

A PwC report states that in only the past two years, economic crime has increased globally, rising 17% in North America, 16% in Asia, and 25% in Latin America. Fraud may take many forms, from minor insurance claims to complex international money laundering schemes.

Given the digitalization of societies around the globe, fraud cases have risen dramatically. Frauds, including internal embezzlement examples, not only affect businesses around the world but also end up destabilizing economies.

30% of the firms have reportedly experienced fraud, and shockingly, 80% of such frauds were committed by internal employees in operations, sales, management, and accounting.

PwC Report

In most of these fraud cases, it’s the lack of internal controls that opens the gates of financial misconduct caused by criminal acts or anomalies through intentional deceit. Scammers take advantage of such weaknesses and commit fraud.

Fraud is classified as a subset of internal threats that consist of corruption, asset misappropriation, and fake declarations, among others.

According to the Association of Certified Fraud Examiners (ACFE), fraud is “the use of one’s occupation for personal enrichment through the misuse or deliberate misapplication of the resources or assets of the employing organization”.

A study shows that 39.1% of fraudulent activities are detected through employee tips, which explains the vital importance of robust whistleblower mechanisms in any organization.

International Journal of Business, Economics and Law

The capacity to engage in this type of behavior is due to the weaknesses in the control mechanisms that institutions and businesses have. In such cases, scammers use these loopholes to conduct fraud.

Fraud is intrinsically linked to human behavior. Thus, understanding the reasons for criminals or their psychological and personality features that cause them to violate ethical boundaries is more than ever essential.

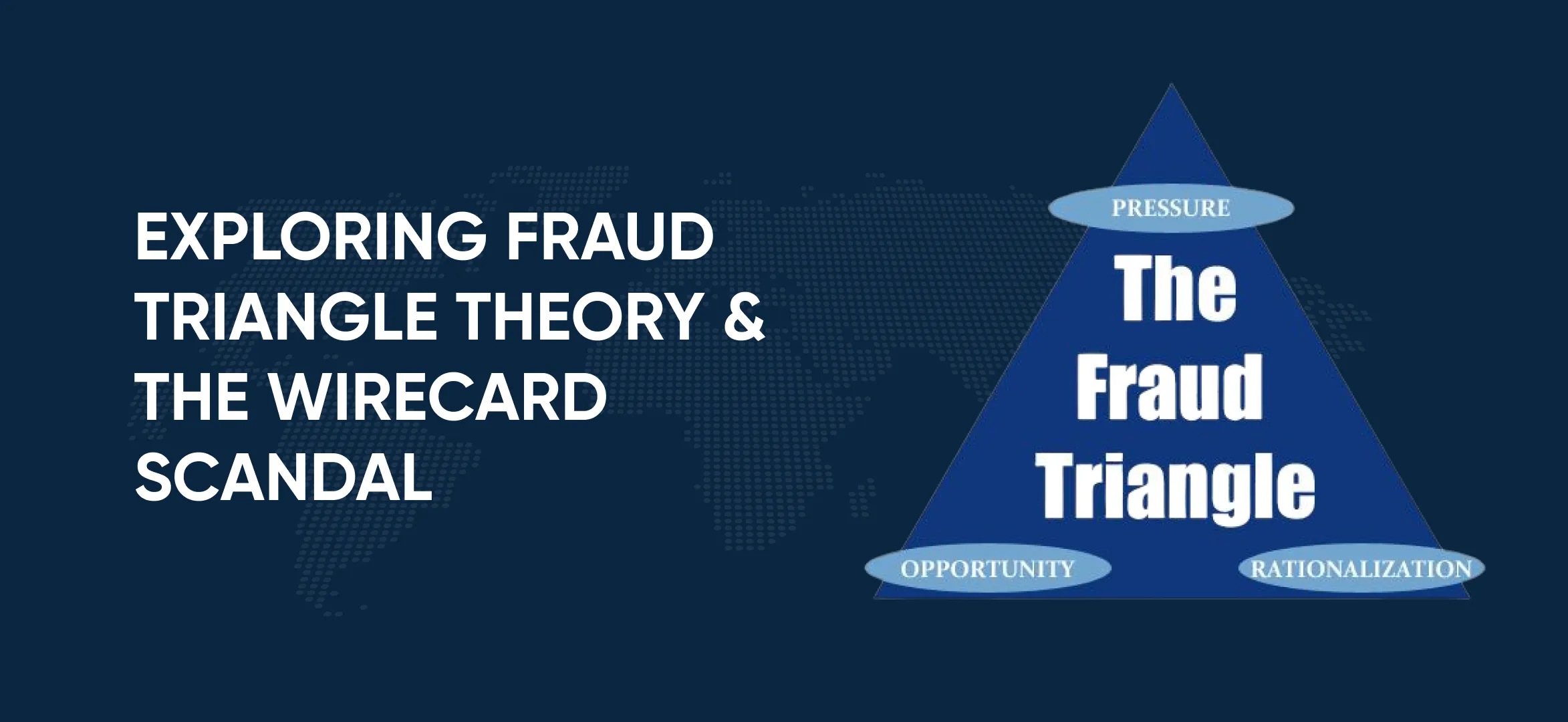

This is where the Fraud Triangle, a theory established by criminologist Donald Cressey, becomes indispensable.

Let’s explore each stage and dimension of this theory with us.

What is the Fraud Triangle Theory?

Donald R. Cressey was an American sociologist, and criminologist who first came up with the concept of the Fraud Triangle by interviewing the 133 imprisoned individuals to understand the psychological and social factors that led them to commit financial fraud.

According to him, there are three key elements which include pressure, opportunity, and rationalization – that must exist for fraud to happen.

He described these ideas in his dissertation, ‘’Other People’s Money: A Study in the Social Psychology of Embezzlement (1953)’’, which became an important work in criminology and corporate governance.

Key Components of Frauds Triangle Theory

The Fraud Triangle transformed our understanding of financial fraud by stressing both environmental and individual elements. The prime components are:

Pressure

It refers to the financial or social factors that drive someone to commit fraud, for example, personal debt or unrealistic performance goals.

Opportunity

It focuses on the systems or procedures that allow fraud to occur without rapid fraud detection, for example, lack of internal oversight.

Rationalization

It suggests the cognitive dissonance that fraudsters feel and their attempts to rationalize unethical activity by portraying it as temporary or necessary.

For example, An employee may feel that they are not paid fairly and believe that committing fraud is a way to get what they deserve.

Cressey’s concept has now become a cornerstone of anti-fraud measures worldwide. It has influenced corporate governance principles, investigating employees, auditing processes, and checking fraud risk management frameworks.

Fraudulent activities usually go unnoticed for about 18 months on average before they’re caught. This shows just how tough it can be for organizations to spot and deal with fraud right away.

International Journal of Business, Economics and Law

To better understand the fraud triangle theory, let’s apply it to Germany’s biggest fintech scandal; the Wirecard Scandal.

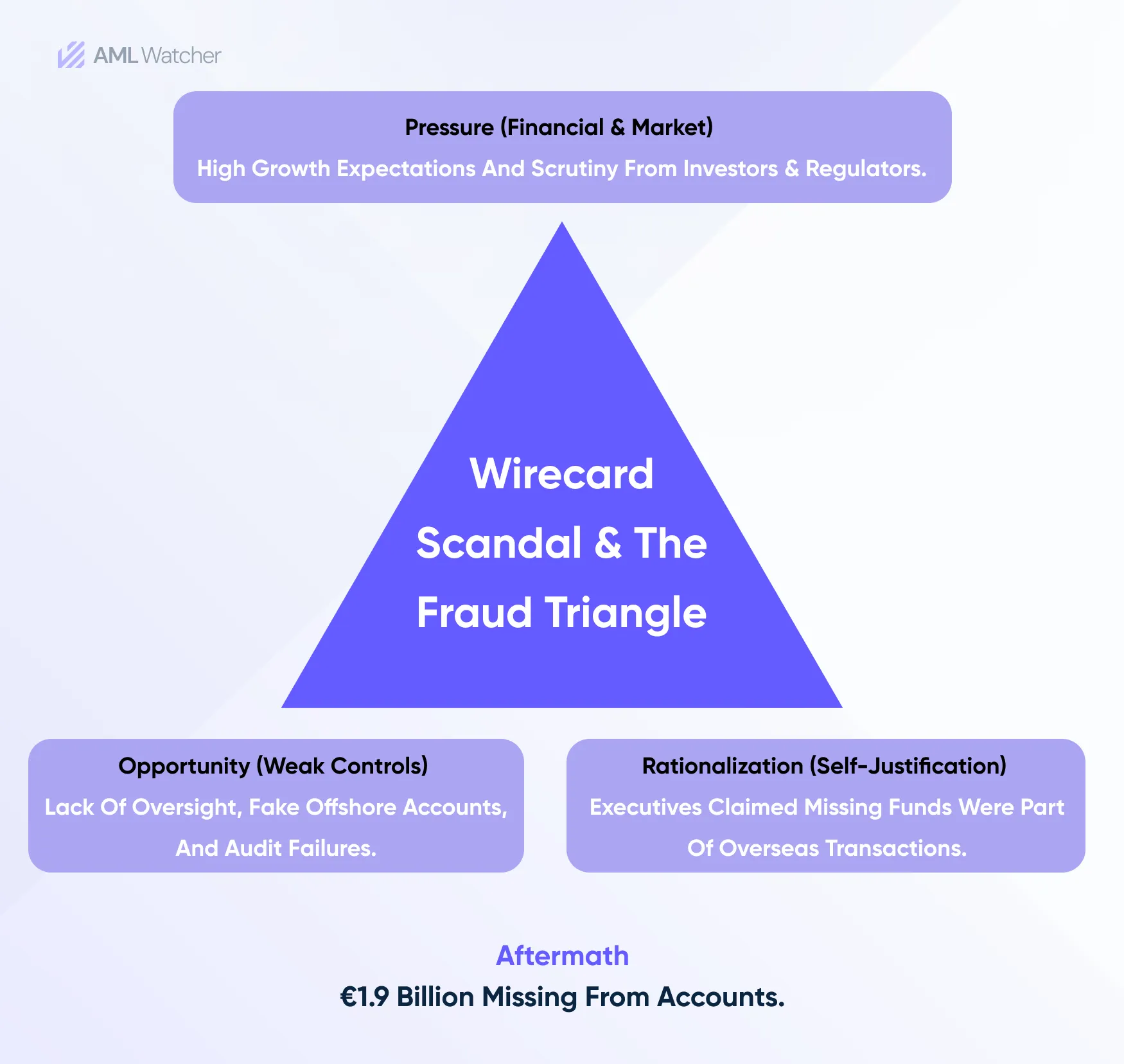

How the Fraud Triangle Theory Maps Wirecard’s Scandal?

On June 25, 2020, Wirecard payment processor, which was previously known as Germany’s fastest-growing fintech company, officially went bankrupt.

Wirecard became involved in a series of fraudulent business activities and fake financial reports. Later investigations revealed that €1.9 billion was actually missing from its accounts.

Markus Braun, the CEO of Wirecard was accused of fraud and other financial offenses and was immediately fired as a result of this revelation. Braun was later arrested.

The German financial industry was rocked by the fall of Wirecard. Surprisingly, it was not regulators or auditors who brought the company down. In fact, it was a journalist and his editors in London working for the Financial Times.

This scandal caused the investors and regulators to focus on the existing shortcomings in corporate governance and devise strategies to proactively deal with serious oversight on such a scale that led to the fall of a corporate giant like Wirecard.

The Fraud Triangle Theory, which talks about factors like Pressure, Opportunity, and Rationalization, is an interesting approach to studying what led to scandals like Wirecard.

Let’s unfold this theory with the Wirecard scandal, to understand the motivations, systemic flaws, and rationalizations that enabled Germany’s most shocking scandal.

Pressure in Wirecard Scandal

In the case of Wirecard Fraud, its executives were under the pressure of faking success even when the company was struggling and not making profits.

The shady financial dealings and money laundering operations by executives Markus Braun (CEO) and Jan Marsalek (COO) were caused by their motivation for power and maintaining deception for as long as they possibly could.

Their illegal activities were simply a way to protect their interests, which makes their shady actions feel understandable, even if it was not the criminal thing to do.

Opportunity in Wirecard Scandal

What opportunity provided the Wirecard executives to bypass government regulations and continue with their crime? Multiple factors.

Firstly, Wircard was able to evade government scrutiny by combining banking (through its subsidiary Wirecard Bank) and non-banking (primarily payment processing) operations.

This resulted in Germany’s Financial Regulator (BaFin) treating Wirecard as a technology business rather than a financial institution. It compelled investors to lean on the company’s own “adjusted version” of its accounts.

Second, Wirecard executives exploited the fact that BaFin only had authority over Wirecard’s bank business subsidiary and lacked the authority to look into the company’s accounting procedures or main operations.

Third, auditors found it difficult to confirm transactions because, by 2015, the majority of Wirecard’s fraudulent earnings were purportedly generated in Asia in its companies in Manila, Singapore, and Dubai, which were bringing in over half a billion euros a year.

These firms were frequently found in remote areas with no overt indications of the volume of business that was documented in Wirecard’s reports.

Given that, Wirecard was able to make it difficult for investigators to follow the paper trail by strategically moving funds and accounts across several jurisdictions.

Rationalization in Wirecard Scandal

Executives at Wirecard used “market rule” as an excuse for their illegal actions. So, to grow and remain competitive in the fintech sector, practices like aggressive bookkeeping, offshore transactions, and profit-inflating were justified as standard procedures.

Being the first fintech company in Germany to compete with Silicon Valley, Wirecard has also been a source of pride for the nation.

Thus, Wirecard rationalized and presented the attack on the business as an assault on Germany’s reputation and the country as a whole.

Key Lessons the Financial Industry Can Take From Wirecard Fraud

The Wirecard scandal consists of all of the typical characteristics of the Fraud Triangle Theory, which makes it one of the most catastrophic financial scandals in recent years.

What distinguished Wirecard was the way it combined accounting fraud with massive money laundering. Wirecard not only falsified the sheets but also laundered money and inflated its profits.

No previous major scandal has pulled off this combination. Enron was well-known for pretending to be a bank using questionable accounting practices, but Wirecard took it to the next level; it was a bank.

This Wirecrad fraud case study is only one of hundreds of money laundering scandals that could be studied to understand how pressure, opportunity, and rationalization combine in real-world circumstances to cause frauds like Wirecard.

In the end, scandals like these can be avoided, and it really comes down to whether corporate leaders want to truly build a culture that values honesty.

They can make a significant impact in combating internal fraud and establishing trustworthy organizational operations by first exercising integrity themselves and then fostering a culture of professional integrity at all levels.

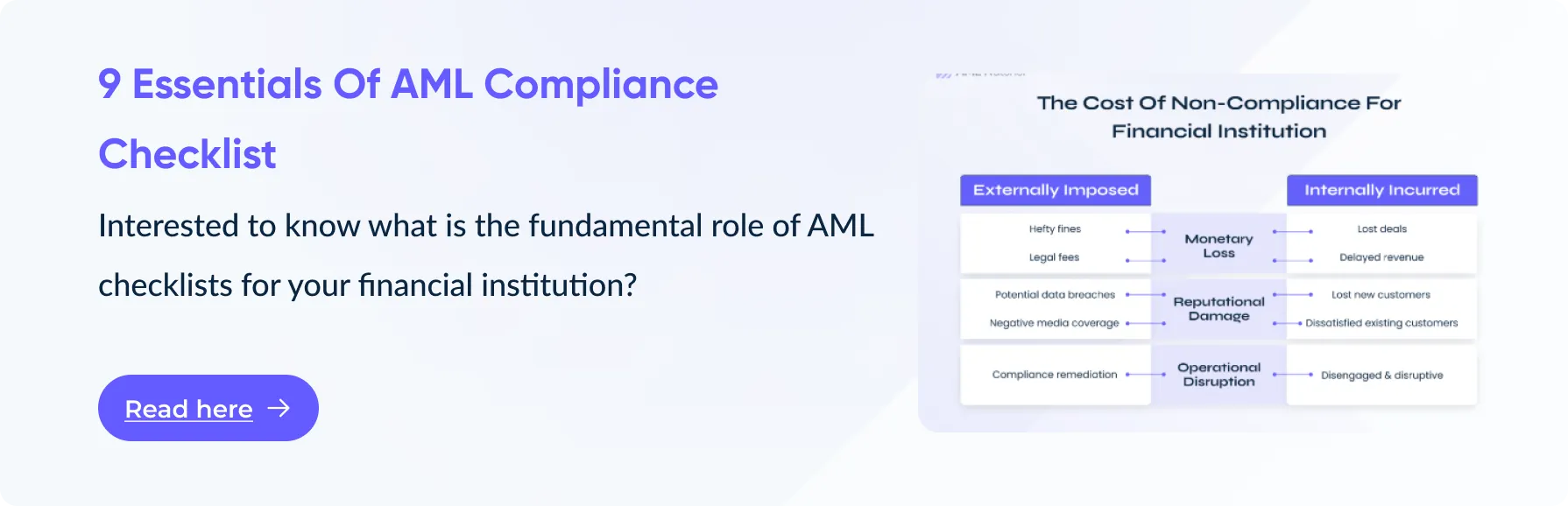

According to the Fraud Triangle Theory (Pressure, Opportunity, Rationalization), people commit fraud for a variety of reasons. Despite its value in comprehending criminal conduct, it does not offer a direct means of detection or prevention.

However, to improve the reduction of fraud detection, AML compliance solutions like sanction screening, transaction monitoring, and risk assessments can be organized around the principles of fraud theory.

How?

How Does AML Watcher Help Detect And Reduce Fraud?

AML Watcher assists institutions in lowering the risk of fraud, money laundering, or terror financing by detecting high-risk people and organizations through its AML screening solution to prevent compliance breaches and ensure continuous fraud monitoring.

It;

Detects High-Risk Individuals & Entities

Screens against 230+ sanctions lists, 3500+ watchlists, and 50,000+ adverse media sources to detect individuals in financial distress or linked to fraud, bribery, or corruption.

Reduces Financial Crime Opportunities

AML Watcher offers ongoing monitoring to track changes in risk profiles, ensuring institutions detect newly sanctioned or flagged entities before conducting business deals or transactions.

Spot Repeat Offenders & Suspicious Patterns

It flags individuals and businesses previously involved in fraud or money laundering activities by screening against more than 60 years of historical criminal records, multiple negative media sources, and local to international regulatory enforcement lists.

Strengthens Risk-Based AML Compliance

It helps institutions stay ahead of potential fraud or money laundering risks by ensuring all customer screenings align with major global AML regulators like FinCEN, UN, EU Directives, OFAC, OFSI, FINTRAC, and many more.

- No commitment needed

- Complete AML Database at your service

- Access our all-in-one dashboard

Tier-2 PSPs in ... must demonstrate automated monitoring, layered CDD, &...

See the Full Regulatory Expectation70–80% less manual work, 95% less fatigue, TruRisk Agent makes compliance effortless.

Experience Agentic AMLMove Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries