Is Your AML Strategy Aligned With UK Anti-Money Laundering Regulations?

AML Regulations

January 2, 2025

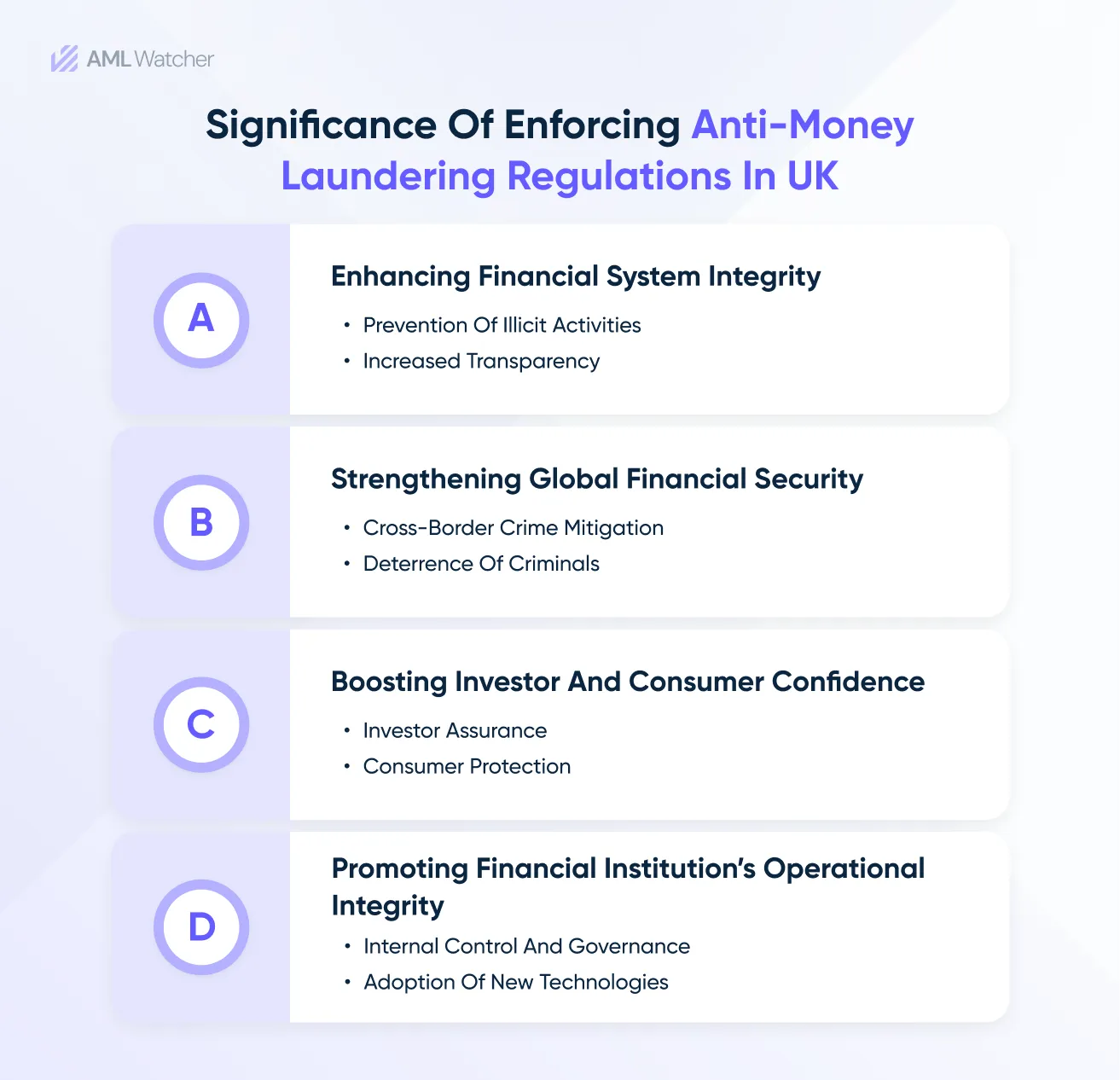

“Stopping money laundering reduces the harm caused to people and society by crime and terrorism, it protects the financial system, attracts investment, promotes economic prosperity, and it enables and safeguards international trade.”

–David Lewis (FATF Executive Secretary)

Behind every illicit transactional practice lies the trail of financial deception that endangers financial stability. During these scenarios, the money laundering regulations serve as the frontline defense through which disruptive financial activities are countered.

Money laundering has been affecting the financial integrity of the United Kingdom for decades. In response to these activities, the UK’s Financial Intelligence Unit (UKFIU) reported approximately 460,000 suspicious activity reports over a year.

The UK’s law enforcement agency is responsible for overseeing the major business spheres that fall under the AML rules.

To assess the financial discrepancies resulting from disguising the fund’s origin, using fake identities, and conducting irregular transactions, it is important to understand what money laundering is and what money laundering regulations are.

Read this article to get professional insights about UK money laundering regulations and their impact on the institutions.

What is Money Laundering?

Money laundering is one of the most prominent financial crimes involving the concealment of the proceeds acquired from criminal activities. The monetary proceeds are usually laundered through several transactional activities across multiple platforms to disguise the origin of the unauthorized funds.

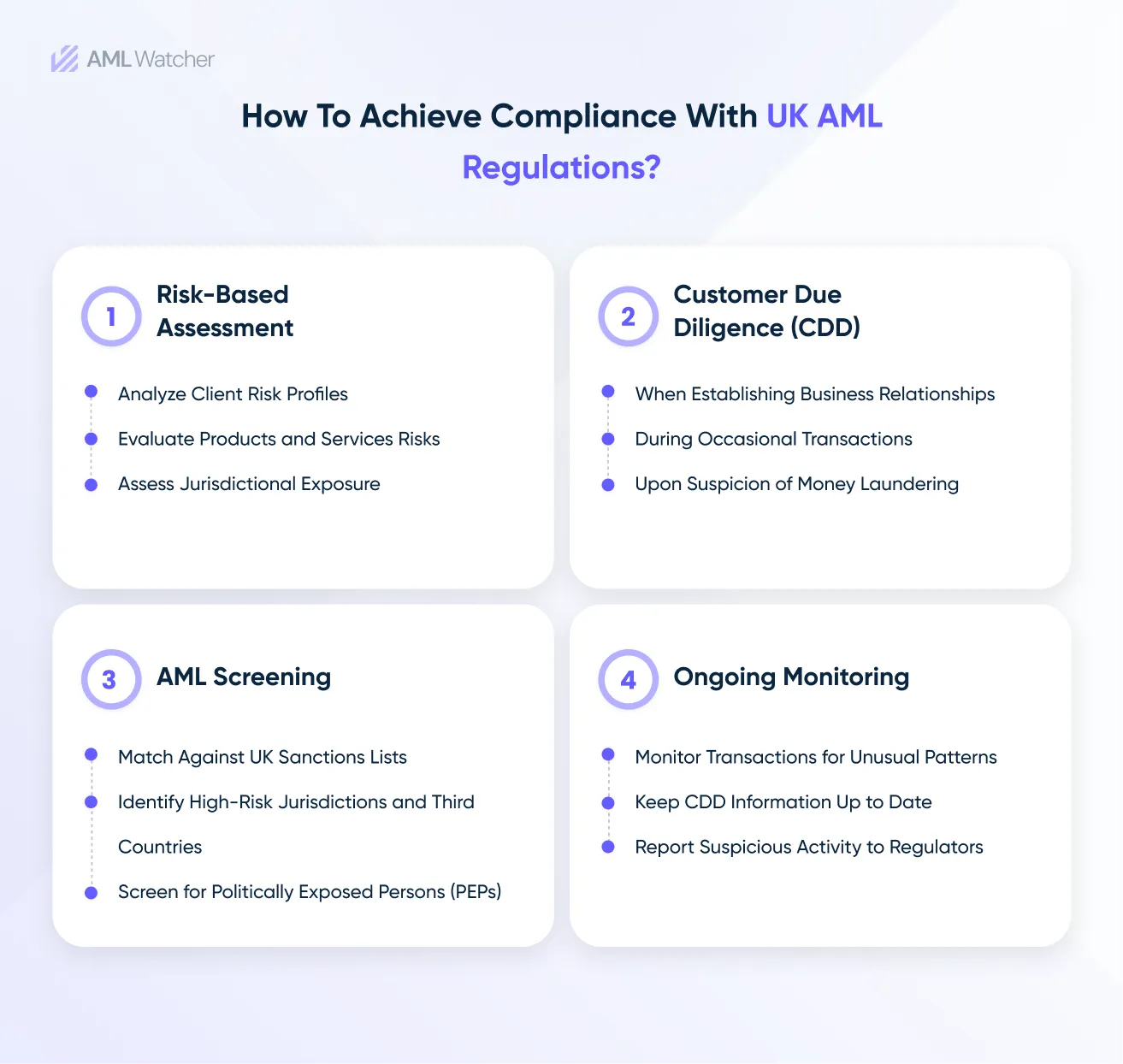

Compliance with the UK money laundering regulations serves a crucial role in this scenario. Interested in understanding the nature of AML legislation in the UK?

Due to its global business operations, the United Kingdom remains the central hub for imposter’s money laundering activities. Over the last few years, the digitization of financial activities has established new avenues for criminals to launder funds through the three typical stages, which are:

Imposters introduce illegal funds into the financial system by deliberately structuring transactions.

These funds are subsequently transferred across many accounts, adding layers of complexity and making it more difficult to trace and identify their unlawful origins.

Key Regulatory Players of the UK’s Money Laundering Act

Being an active member of the Financial Action Task Force (FATF), the UK’s AML authorities are required to align their regulatory guidelines with the FATF recommendations.

More than 100,000 UK-based institutions, including banks, credit unions, money service businesses, and high-value dealers, are mandated to comply with the country’s anti-money laundering regulations.

Some of the most prominent AML regulatory bodies in the UK are:

FCA (Financial Conduct Authority)

The major Money Laundering Act UK revolves around the rules set out by the Financial Conduct Authority (FCA). FCA plays an important role in maintaining the financial integrity of the country’s financial institutions.

These UK AML regulations are responsible for maintaining the country’s anti-money laundering standards. Through its impressive regulatory practice, FCA AML supervises financial institutions in its fight against money laundering activities.

This authority contributes to shaping the country’s AML policies to be in line with global regulatory standards.

FCA AML regulations mandate the implementation of customer due diligence checks to identify potential money laundering risks. These operations are supervised by the Money Laundering Reporting Officer (MLRO), who addresses unusual financial activities in real time.

The Financial Services Act 2021 strengthens the FCA guidelines in terms of regulating firms involved in the facilitation of crypto assets and transaction management. Under this act, all the fintech firms must ensure secure CDD checks and SAR operations to minimize the criminal’s financial ills in real-time.

HMRC (Her Majesty’s Revenue and Customs)

HMRC operates in collaboration with the FCA money laundering rules to streamline Great Britain’s financial operations. As a regulatory authority, HMRC monitors compliance with AML rules, particularly for sectors like money service businesses, and addresses the movement of illicit funds across UK borders.

As per the UK-based AML requirements, HMRC emphasizes strict transaction monitoring checks and requires the FIs to report suspicious financial activities to the FCA.

To counter the money laundering instances, the institutions are required to register their financial proceedings with HMRC for support.

Under the HMRC guidelines, some of the regulated UK sectors include:

- High-value dealers

- Telecommunication and digital payment sector

- Bill payment service providers

The HMRC regulators prevent the scale of money laundering operations by initiating warning letters to the non-compliant entities. These AML legislations UK introduced penalties for businesses that fail to ever abide by the risk assessment and transaction monitoring protocols.

The National Crime Agency (NCA)

NCA leads the management of organized financial crimes by disseminating intelligence on money laundering activities. The compliance officers operating under the NCA prioritize the identification of risky entities.

Moreover, the NCA manages extraterritorial inspection by assessing the financial activities that are related to cross-border money laundering schemes. In 2023, the NCA dismantled £100 million worth of laundered funds that were about to be smuggled from the UK to the UAE.

For this reason, the NCA stays ahead of the imposter’s money laundering tactics through its regulatory reinforcement.

Having discussed the prominence of the money laundering regulations UK, let’s now turn our attention to real-life situations that accentuate their role in identifying financial crimes.

Real-Life Cases of Financial Crime Regulations UK

The UK’s AML regulatory authorities have dismantled various money laundering instances due to their whistleblowing risk assessment mechanism.

Interested in how such risks were identified? The three prominent recent cases related to the regulations of anti-money laundering UK are discussed below:

-

NatWest’s Breaching of AML Laws

NatWest, short for National Westminster, is a banking institution that serves more than 19 million customers annually. In 2021, the bank was fined a penalty of £264 million for breaching the money laundering regulations.

NatWest’s business partnership with Fowler Oldfield, a local jewelry firm, resulted in the cash deposits of unusually large funds and unauthorized assets.

Despite the clear financial pitfalls, NatWest neglected the AML requirements and reporting of suspicious transactional activities.

FCA penalized the bank as NatWest pleaded guilty to failing to comply with the AML regulations UK. The UK’s regulatory authority ordered the bank to pay confiscation costs amounting to £4,297,466.27.

WealthTek LLP Money Laundering Case

Since 2023, the UK’s Financial Conduct Authority has been conducting a criminal investigation against the WealthTek firm due to financial breaches.

In December 2024, WealthTek’s former partner, John Dance, was charged with more than £64 million as he was found guilty of laundering money.

FCA examined that Dance exploited his position to fund personal business and support a lavish lifestyle. Due to such severe regulatory issues, he was placed under special administration by the FCA due to false representation of the financial documents.

Understanding Amendments to the UK’s Money Laundering Regulations

Over the recent years, several amendments in the various UK MLRs have been observed, which are done to enhance the institution’s adherence to the updated regulatory standards. Some of the renowned amendments are:

- In the public Consultation Paper 24/9 (CR24/9) issued in April 2024, several amendments were proposed by the FCA. Following the Russian invasion of Ukraine, this amendment focuses on enhanced sanction screening protocols. The proliferation financing has also been updated, emphasizing the involvement of a comprehensive risk-based screening approach.

Through the recent anti-money laundering amendments, the Financial Conduct Authority proposed enhancements in the PEP screening checks under regulation 48(1) of the Money Laundering, Terrorist Financing, and Transfer of Funds Regulation. The purpose of this update was to boost the involvement of proportionate EDD checks to combat the customer’s de-risking threats.

The updates observed in 2020 mandated strict regulatory operations within the cryptocurrency firms. All the prominent virtual currency service providers were prompted to register with the FCA’s anti-money laundering rules.

How AML Watcher is the Ideal Compliance Partner for MLROs in the UK?

AML Watcher offers a suite of powerful screening tools tailored to help UK institutions excel in meeting Anti-Money Laundering (AML) requirements.

With its innovative solutions, it ensures compliance, efficiency, and proactive risk management.

How? Through its

Comprehensive Sanctions Database

AML Watcher provides access to a unified database of global sanctions lists, including EU, UN, OFAC, OFSI, FCA, and HMT, ensuring compliance with UK-specific and international regulations.

- Covers all sanctioned entities and individuals, including those in high-risk jurisdictions.

- Integrates country-specific requirements for precise alignment with FCA and AML regulatory guidelines.

Separate Watchlist Screening

- Consolidates over 1,300 official watchlists, including enforcement and debarment lists.

- Includes coverage of individuals flagged for financial crime, terrorism, and other illicit activities.

Unified PEP Screening

AML Watcher offers a unified approach, consolidating politically exposed person definitions from global and UK-specific frameworks, including FCA guidelines and Money Laundering Regulations (MLR).

- Covers direct PEPs and their close associates or family members, ensuring no connections are overlooked.

- Optimized to screen focused client bases or regions with populations under 100,000, enabling accurate results without overloading systems or resources.

PEP Risk Level Categorization

- Categorizes PEPs into Risk Levels 1 to 4, enabling institutions to tailor due diligence efforts based on individual risk profiles.

- Facilitates enhanced due diligence (EDD) for high-risk individuals, as mandated by UK regulations

Risk-Based Screening

- Tailors the screening process based on risk profiles, focusing on high-risk jurisdictions and flagged entities.

- Prioritizes enhanced due diligence (EDD) for individuals or transactions linked to sensitive regions.

Real-Time Monitoring and Alerts

- Continuous updates keep institutions ahead of regulatory changes, ensuring no critical updates are missed.

- Automated alerts for sanctions or PEP status changes reduce manual monitoring efforts.

Customized Risk Management

- Customizable risk-scoring models help institutions focus on high-priority clients and transactions, aligning with FATF’s risk-based approach.

- Enhanced due diligence capabilities ensure heightened scrutiny for high-risk profiles and jurisdictions.

Move Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries