The MLRO’s Guide to FATF 40 Recommendations

Others

December 11, 2024

- What Does the FATF Actually Do?

- FATF Black or Greylisting

- Forty Recommendations on Money Laundering

- Domains of FATF 40 Recommendations

- Nine Special Recommendations on Counter-Terrorism Financing

- FATF Key Recommendations for AML Compliance

- FATF’s Role in Cryptocurrency Regulation

- How AML Watcher Empowers Your Compliance Journey With FATF-Aligned Screening?

In the summer of 1989, when the G7 summit welcomed world leaders in Paris to exchange ideas to tackle the growing threats of rising financial crimes, France took the lead and presented an unprecedented proposal that would reshape international efforts against financial crimes for decades to come.

It proposed the establishment of a powerful international financial watchdog: the Financial Action Task Force (FATF).

With the backing of the United States and the United Kingdom, who were already battling money laundering in their own jurisdictions, the idea gained momentum, and it set the stage for a global crackdown on organized crime, corruption, and terrorism.

This was the beginning of an international initiative to develop and enforce policies to dismantle money laundering networks and counter the financing of terrorism.

What Does the FATF Actually Do?

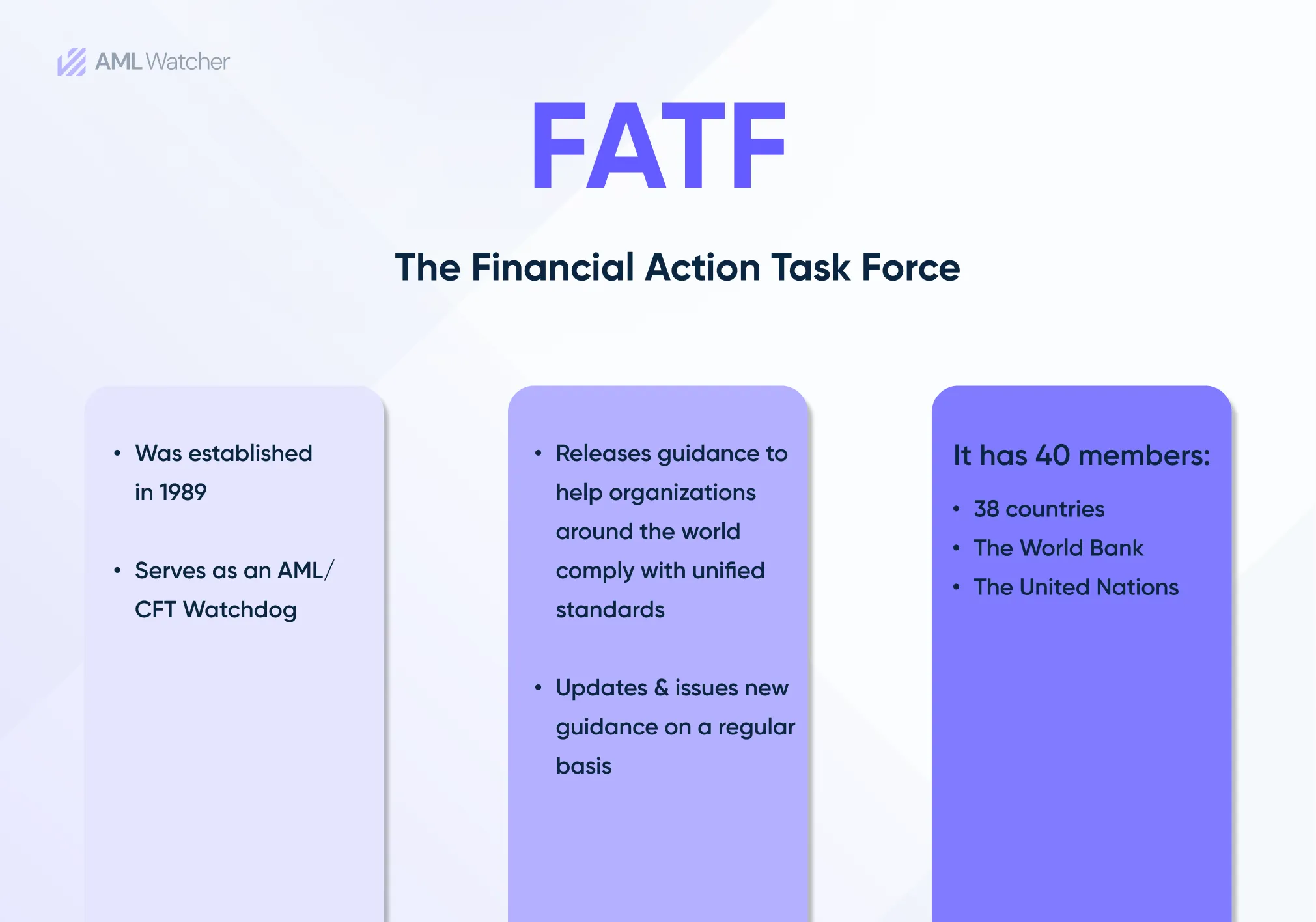

Financial Action Task Force (FATF), is an intergovernmental organization, comprising 40 member states; the United Nations, the World Bank, and 38 nations. It advises global and state governments on how to fight financial crimes, including the financing of terrorism, and money laundering.

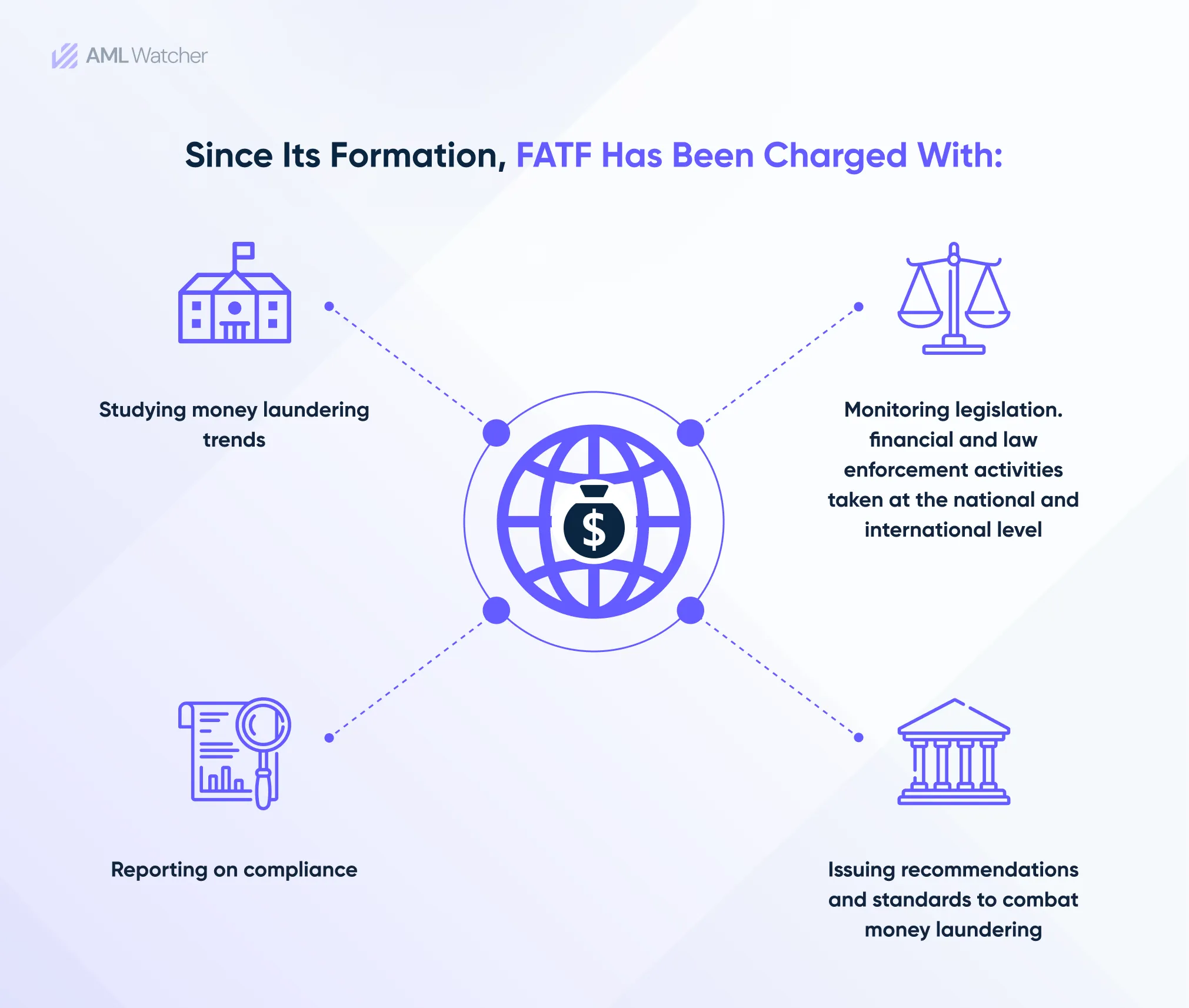

FATF is a policy-making body that builds the global political commitment necessary to drive national legislative and regulatory reforms in the AML and CFT domains.

Setting standards and encouraging the efficient application of legislative, regulatory, and operational measures to counteract money laundering, terrorist financing, corruption mitigation, and other associated challenges to the integrity of the global financial system are the primary objectives of the Financial Action Task Force.

Following the September 11 terror attacks on the Twin Towers of New York, FATF included terrorist financing in its primary focus area.

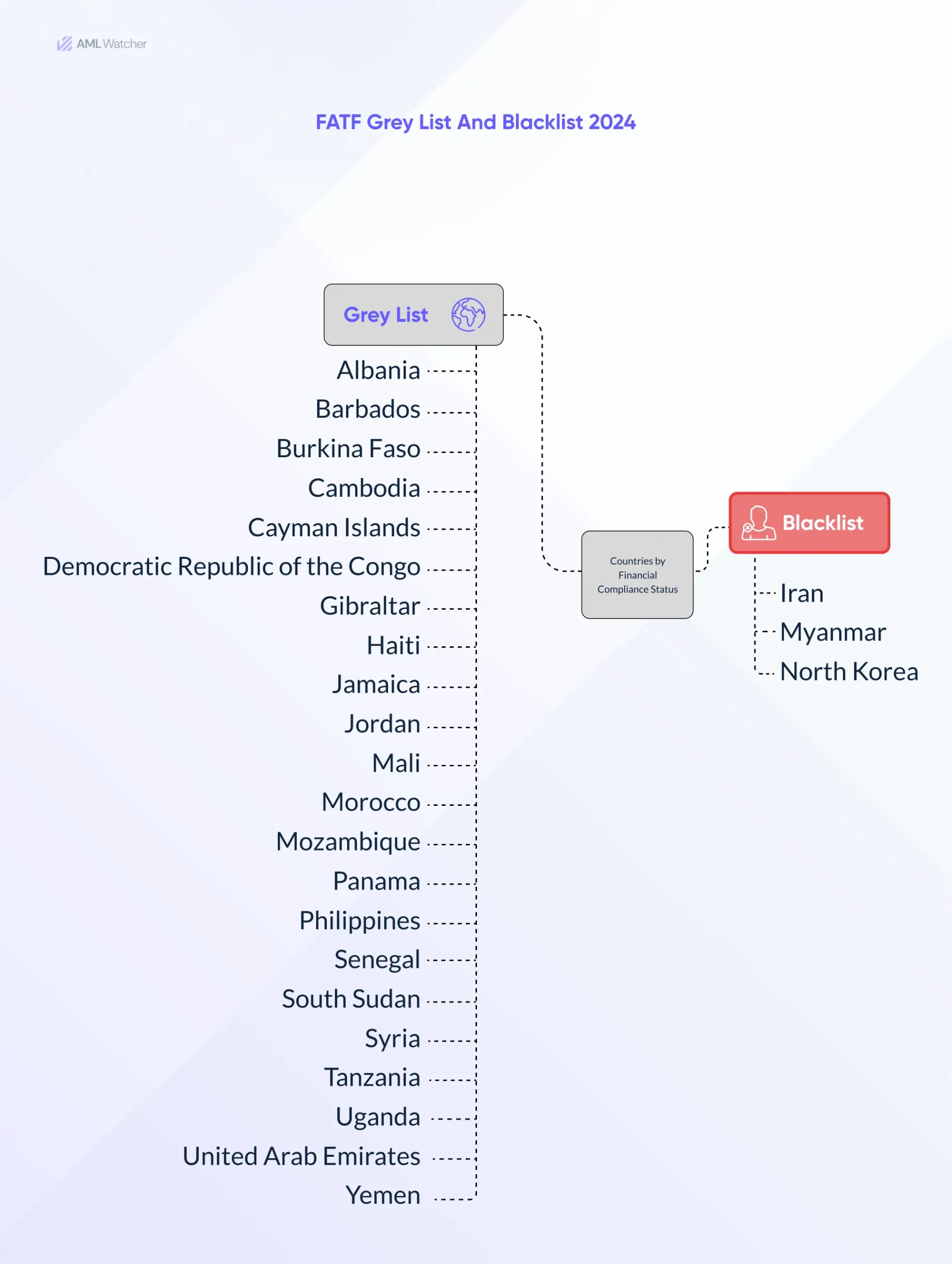

FATF Black or Greylisting

FATF’s Greylisting and Blacklisting assess countries under FATF’s mutual evaluation system for weak AML/CFT frameworks.

FATF Blacklisting and Greylisting Process

1: Mutual Evaluation

FATF regularly monitors countries’ adherence to AML/CFT standards, evaluating their laws, regulations, and enforcement effectiveness.

2: Identification of Non-Compliant Countries

Countries that fail to meet FATF’s standards are flagged, with greylisting or blacklisting used to prompt improvements.

3: Greylisting

Countries with strategic deficiencies are placed under increased monitoring and must submit an action plan to address AML/CFT weaknesses. Consequences include reputational damage and loss of investment, but no immediate sanctions.

4: Blacklisting

Countries that fail to demonstrate a commitment to change face harsh financial sanctions and worldwide avoidance owing to high risks. Blacklisted countries risk losing access to international financial markets and experiencing trade disruptions.

FATF’s decisions often influence other international bodies, such as the World Bank and IMF, in enforcing financial sanctions or help.

As of June 2024, countries in the FATF’s greylist and blacklist are:

Forty Recommendations on Money Laundering

Since their introduction in 1990, the FATF’s Forty Recommendations on Money Laundering have been the gold standard for combating financial crimes worldwide.

The Nine Special Recommendations on Terrorism Financing and these recommendations have established the standard for many nations trying to improve their anti-money laundering frameworks.

The Recommendations address everything from international collaboration and financial regulations to criminal justice and law enforcement.

The 1996 update, for instance, stretched its application beyond drug, and money laundering techniques, and the regulations were further strengthened by 2003.

Under the revised criteria, nations are expected to do the following:

- Implement record-keeping, client checks, and the reporting of suspicious conduct in the financial and some non-financial industries.

- Financial intelligence units (FIUs) should be established to manage and disseminate reports of irregular transactions.

- Compliance with international financial crime conventions

- Cooperate internationally to look into and bring charges against offenders

These recommendations are more than simply guidelines; they represent a global commitment to staying one step ahead of financial scammers.

Domains of FATF 40 Recommendations

The 40 Recommendations are divided into seven different domains:

- Recommendation 1-2: AML/CFT Policies and Coordination

- Recommendation 3-4: Money laundering and confiscation

- Recommendation 5-8: Terrorist financing and financing of proliferation

- Recommendation 9-23: Preventive measures

- Recommendation 24-25: Transparency and beneficial ownership of legal persons and arrangements

- Recommendation 26-35: Powers and responsibilities of competent authorities and other institutional measures

- Recommendation 36-30: International cooperation

Nine Special Recommendations on Counter-Terrorism Financing

Following the tragic events of September 11, 2001, the FATF took immediate measures to fight terrorist financing. In October of that year, it issued eight Special Recommendations aimed at reducing the flow of financing to terrorist organizations.

Special Recommendation VIII (SR VIII) was a useful policy that aimed at improving control of non-profit organizations and recognizing their potential for sponsoring terrorism.

Later, a ninth Special Recommendation was added, substantially broadening the framework. To remain effective in the face of changing dangers, the Special Recommendations and the original Recommendations were both updated in 2003.

The FATF’s determination to remain at the forefront of the battle against terrorist financing while adjusting to new obstacles can be seen in this changing set of actions.

FATF Key Recommendations for AML Compliance

The FATF’s recommendations offer a framework for international AML/CFT compliance, with an emphasis on risk-based strategies and improved due diligence.

To provide effective measures to prevent financial crimes and sanctions evasion, financial institutions and nations must remain vigilant in adjusting to emerging risks.

The essential AML/CFT compliance recommendations include:

Risk-Based Approach (Recommendation 1)

Countries should adopt a risk-based strategy for AML/CFT, modifying compliance protocols in response to identified risks. Higher-risk jurisdictions require more stringent controls, while lower-risk jurisdictions allow simplified measures.

Sanctions (Recommendations 6/7/35)

FATF recommends targeted financial sanctions to comply with UN Security Council resolutions against the funding of terrorism and the proliferation of weapons by freezing the assets and money of designated entities.

Customer Due Diligence (Recommendation 10)

Financial institutions are required to implement Customer Due Diligence to confirm customer identities, monitor accounts, and identify beneficial owners—particularly in cases where money laundering or terrorism funding is suspected.

Politically Exposed Persons (PEPs) (Recommendation 12)

For PEPs, financial institutions are required to perform more thorough due diligence, which includes tracking down the source of funds, and wealth, keeping an eye on transactions, and getting top management’s consent for commercial partnerships. Family members and close associates of PEPs must also undergo detailed screening.

Virtual Assets (Recommendation 15)

Countries are required to regulate Virtual Asset Service Providers (VASPs), monitor virtual currencies, stablecoins, and cryptocurrency transactions, and ensure AML compliance, including CDD.

Wire Transfers (Recommendation 16)

According to the Travel Rule, financial institutions must gather identifying information about the originators and recipients of wire transfers, including cryptocurrency to properly maintain an AML audit trail.

High-Risk Countries (Recommendation 19)

When working with high-risk nations, such as those on the FATF’s grey or black lists, Enhanced due diligence is mandatory. This includes steps like limiting new business partnerships and requiring more thorough reporting.

Reporting Suspicious Transactions (Recommendation 20)

Suspicious transactions connected to money laundering or terrorism financing must be reported to financial intelligence units (FIUs), regardless of the size of the transaction.

Beneficial Ownership (Recommendation 24)

Financial institutions need to determine who the beneficial owners of businesses are to stop money laundering. With an emphasis on DNFBPs like casinos and real estate, FATF advocates for public registries to increase transparency.

FATF’s Role in Cryptocurrency Regulation

As cryptocurrencies and digital assets gained popularity, FATF recognized the growing risk that they may be exploited for illicit reasons.

In response, FATF issued regulations ensuring that Bitcoin platforms operate inside the same AML/CFT standards as traditional financial institutions.

It focused on traceability, increased compliance, and transparency for VASPs and aligned cryptocurrencies with the global AML/CFT regulatory framework.

How AML Watcher Empowers Your Compliance Journey With FATF-Aligned Screening?

AML Watcher is an all-inclusive AML compliance solution that helps institutions adhere to the FATF’s 40 Recommendations, and facilitate compliance with the anti-money laundering (AML) and counter-financing of terrorism (CFT) guidelines, specifically about Politically Exposed Persons (PEPs) and other high-risk individuals and entities.

AML Watcher directly or indirectly complies with nearly all 40 FATF recommendations, ensuring real-time monitoring, risk-based approaches, and continuous updates for effective AML screening.

AML Watcher helps organizations adhere to FATF’s requirements:

Global Coverage & Regulatory Alignment

- AML Watcher aggregates data from over 100,000+ global sources, including sanctions lists, watchlists, PEP data, and adverse media.

- This enables a comprehensive view of risks from all jurisdictions, helping to comply with international FATF requirements.

- The system automatically integrates updates from key regulatory bodies like the EU, OFAC, FATF, and other organizations, ensuring real-time regulatory compliance and reducing the risk of missing updates.

Sanctions & Watchlist Screening

- AML Watcher screens clients against over 1,300+ global sanctions lists, including lists from OFAC, the UN, EU, DFAT, OFSI, UNSC, CAATSA, JMOF, and other regulatory bodies, flags high-risk associations and ensures businesses avoid indirect engagements that may breach AML Laws requirements.

- AML Watcher enhances compliance by conducting secondary screening to detect entities indirectly linked to sanctioned individuals or organizations.

Comprehensive PEP & RCA Coverage

- AML Watcher’s solution consolidates PEP definitions from various regulatory bodies (e.g., FATF, FinCEN, EU, and national authorities), to ensure that all types of PEPs including foreign, domestic, and their family members and close associates (RCAs)are appropriately recorded.

Enhanced Due Diligence (EDD)

- AML Watcher enhances screening by cross-referencing individuals’ profiles with global news sources, public reports, and legal databases, providing in-depth due diligence on their associations with controversial activities.

Risk-Based Screening

- AML Watcher allows compliance teams to customize risk thresholds based on an institution’s jurisdiction and risk appetite.

- Institutions can set up AML screening rules to flag higher-risk individuals or high-value transactions that require further investigation.

- AML Watcher uses a dynamic risk assessment model that allows you to set risk levels based on your specific needs, flagging high-risk individuals or transactions for additional review to focus on real threats.

Real-Time Monitoring & Alerts

- AML Watcher’s databases are updated every 15 minutes, ensuring institutions receive up-to-the-minute information on PEP status, sanctions lists, and adverse media reports.

- The system generates real-time alerts when individuals are being added to or removed from sanction lists or linked to negative news, ensuring immediate compliance checks.

Transaction Monitoring

- AML Watcher monitors transactions by continuously screening them against FATF-aligned global data, identifying high-risk entities, and ensuring ongoing compliance through risk-based analysis and enhanced monitoring.

- The system screens and flags potential risks based on FATF’s risk-based approach, focusing on unusual patterns or associations with sanctioned entities.

- No commitment needed

- Complete AML Database at your service

- Access our all-in-one dashboard

Tier-2 PSPs in ... must demonstrate automated monitoring, layered CDD, &...

See the Full Regulatory Expectation70–80% less manual work, 95% less fatigue, TruRisk Agent makes compliance effortless.

Experience Agentic AMLMove Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries