Why is a Quality AML database the backbone of Modern Compliance?

AML Compliance

August 18, 2025

- What is an AML Database?

- Five Traits of High-Quality AML data

- Completeness of AML Data Coverage

- Accuracy in AML Risk Screening

- Consistent Across Jurisdictions

- Relevance of AML Data Sources

- Timeliness of AML Database Updates

- How Poor Data Inflates Compliance Costs?

- Future-Proof Compliance and Reduce Costs with AML Watcher

Sanctions can shift in hours, and politics can change overnight. If your Anti Money Laundering (AML) database cannot keep pace, your controls cannot either. Speed and accuracy at the data layer decide outcomes, from screening sanctions and Politically Exposed Person (PEP) profiles to monitoring adverse media and Know Your Customer (KYC) changes.

This article explains what an AML database is, the traits that define data quality, and how a modern, frequently updated dataset strengthens detection while lowering AML compliance costs.

What is an AML Database?

Central to any AML compliance operation is the database. This database stores data related to international and domestic sanction lists, watchlists, Politically Exposed Person (PEP) lists, adverse media screening, know your customer (KYC) data, and so much more – allowing compliance teams to screen, monitor, and investigate financial crimes.

This central database provides compliance officers with a unified, structured, and searchable system that allows for ease of use and efficient screening.

But not all AML databases are created equal. Most legacy AML vendors supply compliance officers with static, limited, and outdated databases that leave financial institutions vulnerable to

- Regulatory penalties and scrutiny by financial watchdogs.

- Reputational harm and loss of clients

- Inefficiency and increased operational costs

In the following sections, we break down the five key characteristics of high-quality core AML data and how the right AML compliance solution can give you a decisive victory over competitors still stuck with legacy AML systems.

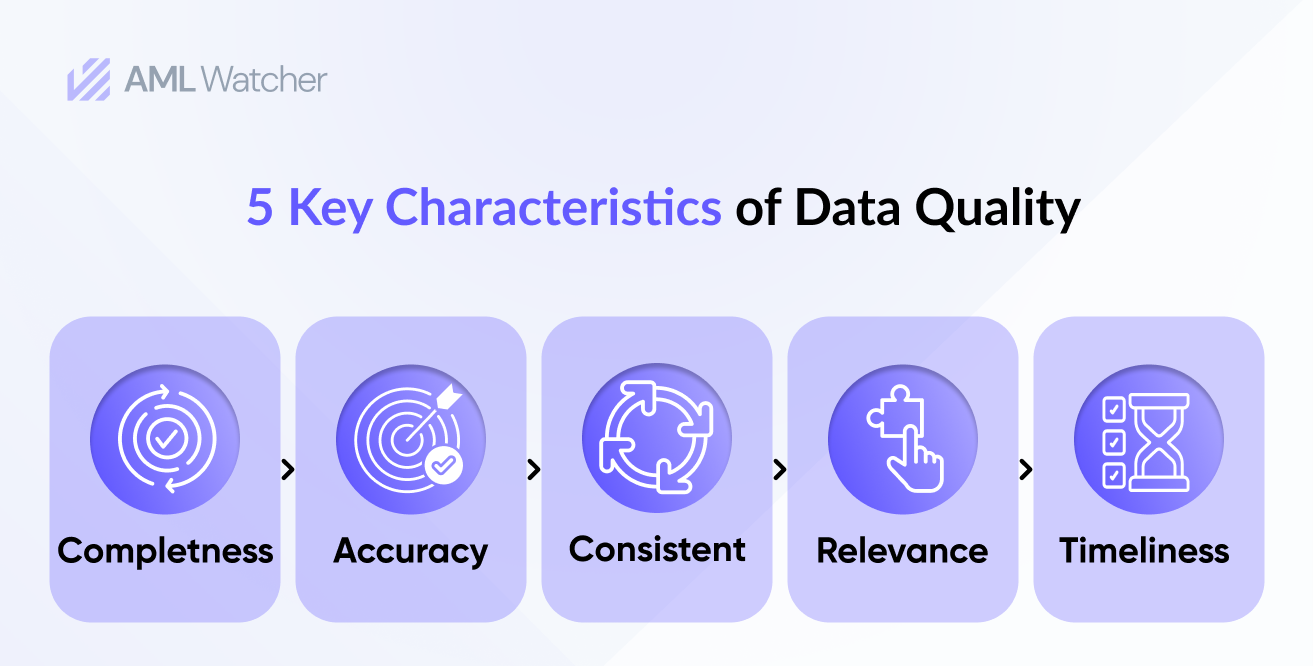

Five Traits of High-Quality AML data

The quality of data, both quantitative and qualitative, is determined by certain critical characteristics. Here are 5 key characteristics of high-quality AML data:

Completeness of AML Data Coverage

Where customer data is incomplete, financial transactions that may otherwise be flagged could go unnoticed – thereby exposing the financial institutions to penalties from relevant financial regulatory bodies.

For instance, if the AML database has incomplete information on a global sanction list, AML systems may fail to identify suspicious patterns that do not fit the customer’s usual behaviour, resulting in false negatives.

The Financial Action Task Force (FATF) Recommendation 10 on Customer due diligence sheds light on the importance of obtaining complete customer data for financial transactions.

But due diligence is a two-way street. Financial institutions must also ensure that their AML screening database is complete and up-to-date – for only when both the customer data and the AML database are complete, will there be effective AML compliance in the modern world.

Accuracy in AML Risk Screening

The accuracy of data is determined by the degree to which the data describes real-world information.

For example, the information about a customer may be inaccurate if their names or addresses are not correct. Further, said data must also accurately reflect the relevant regulatory requirements of its jurisdiction. Discrepancies in data can include mismatched customer names, which may lead the AML compliance system to flag transactions for suspicious activity incorrectly.

Consistent Across Jurisdictions

Given the global scale of financial transactions, data must also be consistent across multiple jurisdictions and systems.

For example, in a multi-national financial institution, data from sanction lists and watchlists in Central Asia needs to be appropriately formatted, identified, and translated into English for the financial institution’s central AML database in Europe. Any discrepancy or inconsistency in this process could result in poor missed suspicious activity reports and regulatory fines.

The FATF Recommendation 18 (Internal controls and foreign branches and subsidiaries) directs financial institutions to implement group-wide programs against money laundering and thorough internal controls that monitor the accuracy of the data, to avoid mistakes in risk profiling.

Relevance of AML Data Sources

For AML compliance, data will only be useful if it is relevant. Financial institutions need data related to economic activity in high-risk jurisdictions and unusual transactions. Particularly, the relevance of data isn’t only about removing the noise, but also about ensuring that it reflects the high-risk entities according to the laws of jurisdiction.

What is relevant in one jurisdiction may be entirely irrelevant in another. Sanction lists, for instance, vary from territory to territory. A sanctioned entity in one territory may not be a sanctioned entity as per the sanction list of another territory.

Many legacy AML solution databases lack comprehensive coverage for PEP lists in jurisdictions with fewer than 100,000 people, allowing bad actors to exploit this limited coverage.

Lower-level public officials, including mayors and members of the local council, may not be considered high-risk PEPs in one jurisdiction. Still, they may be high-risk PEPs in other jurisdictions.

The failure of legacy AML databases to cover such sparsely populated jurisdictions opens the way for sanctioned entities to engage in illicit financial activities without getting caught.

Timeliness of AML Database Updates

One thing common to every AML database is the fact that data is subject to change. With shifting global events and regulatory changes, it is crucial that AML data is dynamic. If customer profiles or sanction lists are not timely updated, suspicious activity may go undetected, leaving institutions exposed to financial crime.

In 2024 alone, 74 national elections reshaped PEP populations as new administrations formed—databases that are not refreshed quickly will miss status changes.

Many legacy AML solution providers have static datasets that are not timely updated, leaving compliance officers with outdated and incorrect data on PEP status.

Similarly, this is also true for the sanctions list data. The recent Israel-Iran conflict illustrates how quickly designations can change. Iranian military personnel were added to multiple sanction lists as new updates emerged in the conflict. The promptness of an AML compliance system is determined by how swiftly it can update its AML database.

How Poor Data Inflates Compliance Costs?

Regulators impose legal obligations on financial institutions to apply a risk-based approach to AML compliance. As such, financial institutions are mandated to tailor their AML compliance efforts according to the risk they face.

To comply with the regulatory requirement of a risk-based approach, it is essential that financial institutions rely on high-quality data. The effectiveness of a risk-based approach is almost entirely dependent on the quality of data feeding it. Inaccurate and outdated information is poor at identifying risk and undermines the legal obligation imposed on financial institutions by regulators.

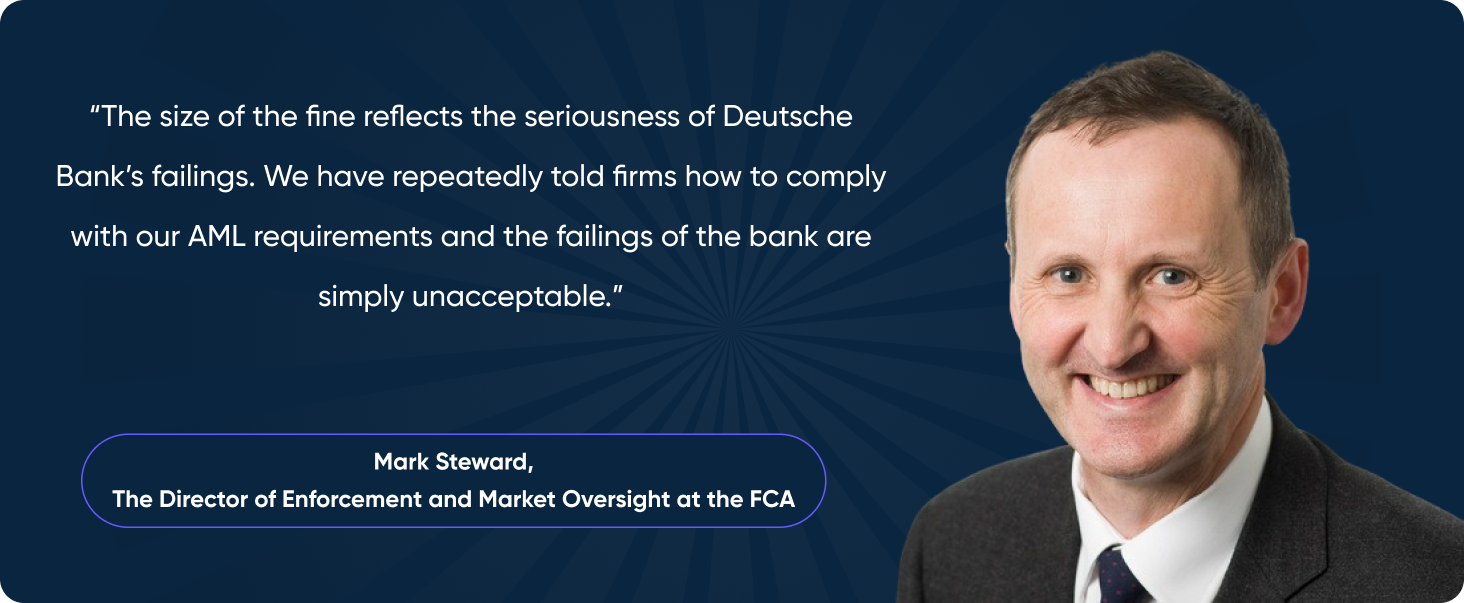

The consequences of poor data-quality can be severe for financial institutions. The FCA fined a multi-national German bank £163 million for inadequate AML controls that allowed unidentified customers to transfer billions of pounds from Russia to offshore bank accounts.

It’s important to mention two critical regulatory findings of this case: first, the bank’s flawed customer and country risk-rating methodology, which resulted in assigning incorrect risks to clients; and second, a fragmented AML database resulting in missing critical risks.

This demonstrates how poor AML databases and rigid AML systems that cannot be customized according to the risks can directly translate to regulatory penalties and reputational damage.

Other key ways poor-quality data directly impacts AML systems include:

- Without comprehensive and accurate data available at their disposal, financial institutions will struggle to assess and mitigate risk. For example, inaccurate and incomplete data may lead the AML compliance system to treat low-risk customers as high-risk individuals, resulting in compliance teams spending precious resources scrutinizing low-risk customers for little to no benefit.

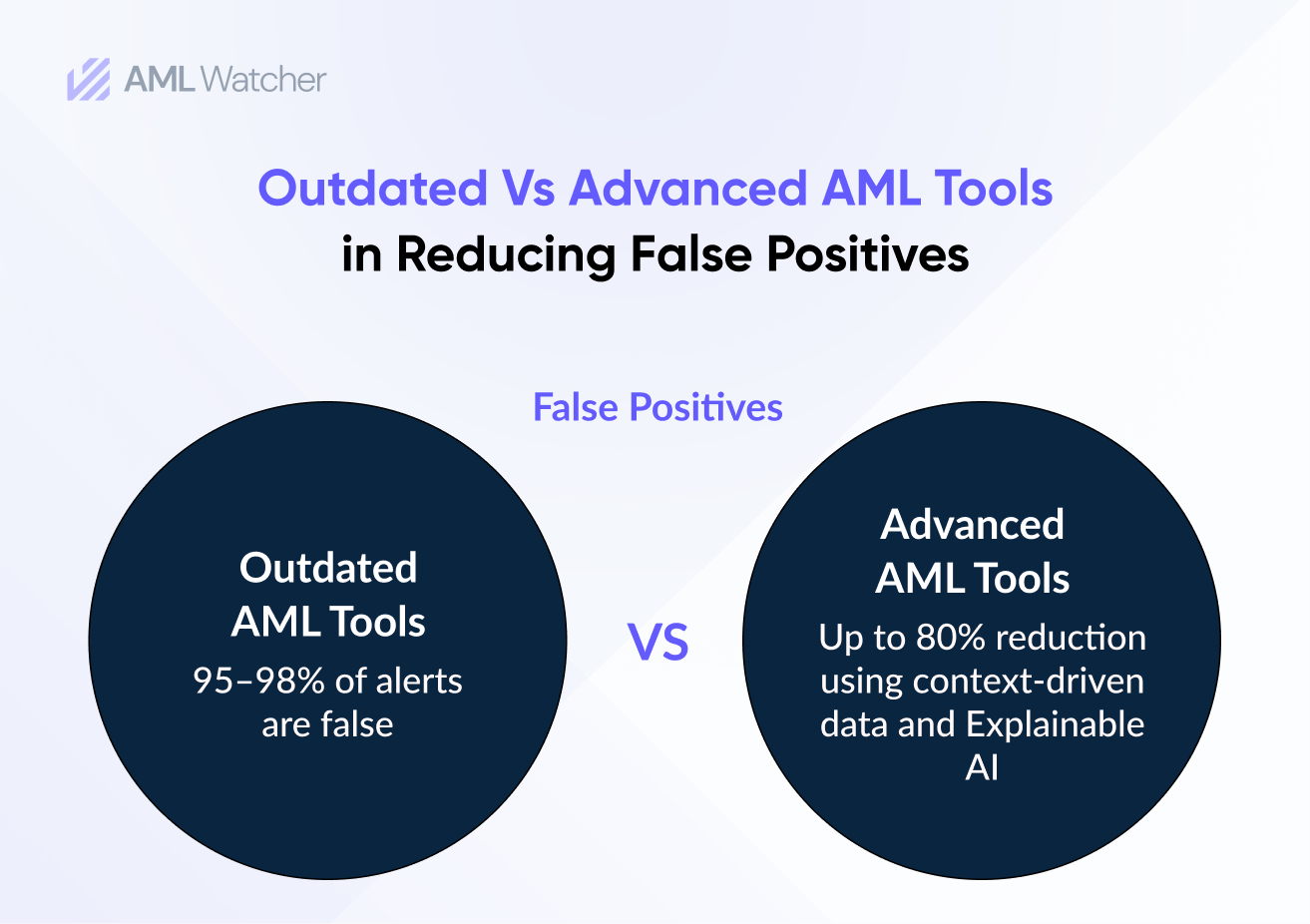

- Inaccurate data also increases the likelihood of false positives. Incomplete customer information may result in the AML system sending unnecessary alerts to compliance officers, who will then need to individually resolve the alert, which increases business costs and reduces the effectiveness of the AML system.

- Similarly, incomplete and inconsistent customer data can severely slow down the KYC process, which in turn causes unnecessary delays in the customer onboarding and increases operational expenses. Friction in the onboarding process can also drive away potential customers.

Future-Proof Compliance and Reduce Costs with AML Watcher

From missed alerts, hefty regulatory fines, reputational damage and loss of clients, you’ve seen the consequences of poor-quality data in AML systems. At AML Watcher, we understand the need for high-quality data for modern AML compliance systems. Our comprehensive and accurate solutions enable financial institutions to increase their efficiency, improve effectiveness, and avoid regulatory penalties. Here’s how our proprietary database can help you:

- Global AML Coverage – At AML Watcher, we deliver accurate and up-to-date data from around the globe, including disputed and remote territories in multiple languages – eliminating blind spots and providing you with a solution that is consistent across multiple jurisdictions. Unlike legacy AML solution providers, our proprietary database covers over 235+ countries, including disputed regions and jurisdictions in more than 80+ languages.

- Screening Accuracy – Through our advanced name-matching algorithms that use a multi-faceted approach, AML Watcher reduces false positives up to 44% and false negatives by 15% in contrast to other AML solution providers.

- Context-driven Insights- Our solutions go beyond traditional screening methods to provide you with content-rich profiles, including data from multiple global sources. Our proprietary database integrates data from over 215 sanction regimes, 3500+ watchlists, 50,000+ adverse media sources, and hundreds of risk categories. At AML Watcher, we strive for precise risk detection, highlighting emerging threats and allowing you to make informed decisions.

- Always ready – Our proprietary database refreshes data every 15 minutes, keeping you instantly synced with any changes in sanctions, PEPs, and adverse media, ensuring we always keep you up-to-date in shifting conditions. Our rich PEP database from across the world is unified and includes public officials of all levels.

- Adaptable Risk Scoring Engine – Our robust, data-driven risk intelligence allows you to implement tailored AML solutions according to your business’s risk appetite and exposure. As financial crime risks keep evolving, you can customize and dynamically assign risks and categories to each customer with the help of AML Watcher’s adaptable risk engine.

Move Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries