How Does Quality Data Drive Efficient AML Risk Assessment?

Risk Assessment & Management

January 15, 2025

- What is AML Risk Assessment?

- Why Is AML Risk Assessment Important?

- Who Writes The Rules and Establishes AML Regulations?

- How Institutions Held Responsible for Where Legacy System Fell Short

- Do Institutions Face Challenges In Implementing An AML Risk Program?

- Can Any Vendor Elevate Risk Assessment Across All Businesses?

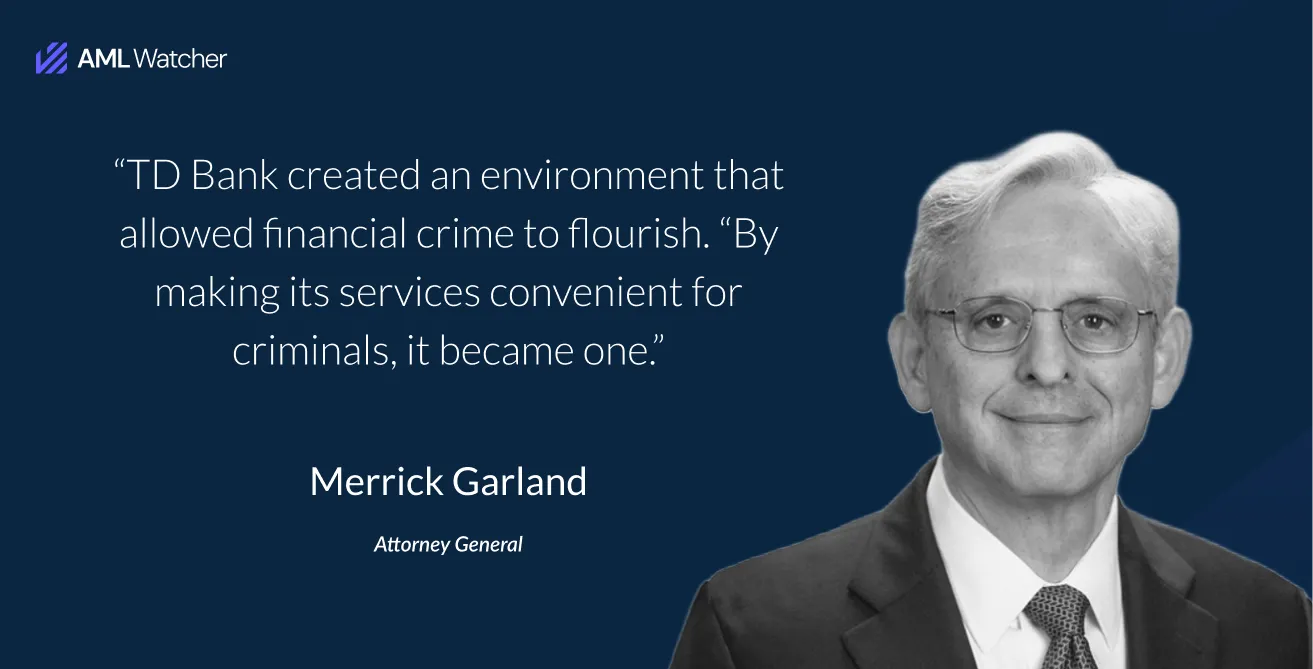

Choosing a high-risk client over AML compliance checks can cost billions of dollars to financial institutions.

That is the case with TD Bank, the United States of America’s 10th-largest bank, which faced a 3 billion dollar fine due to violation of the BSA AML Regulations Act and weakened AML risk assessment measures.

Therefore, multiple key money laundering techniques such as structuring and smurfing have become more valuable for criminals to launder funds through institutions with weaker AML risk assessment programs.

That is why global AML regulations oblige every business in the jurisdiction to follow stronger AML compliance programs with a risk-based approach to combat these rising financial crimes.

Financial institutions are not the only ones needed to comply with these AML Regulations, however, under the Financial Action Task Force recommendation number 26, DNFBs are also required to conduct AML risk assessment based on customer profile, geographical location, and transaction pattern.

Despite knowing the importance of AML risk assessment, institutions often avoid implementing robust AML screening solutions to follow required AML regulations within their organizations.

The HSBC, Metro Bank, and TD Bank are prime examples of violating AML regulations and focusing on dealing with high-risk clients without any proper risk checks.

Points to consider here are; why do institutions still avoid obeying AML regulations? Does the AML risk assessment make the customer dealing process difficult? Do AML risk assessments create operational delays or add value?

There could be one of many reasons for not complying with AML regulations, however, mitigating the money laundering and terror financing risks within your organization is bound no excuse or reason.

Read this article to get in-depth knowledge on:

- What is AML risk assessment and why AML risk assessment is important?

- What does it actually mean for a business to deal with and reduce any risks?

- How does it help to detect high-risk clients even after onboarding?

- What do corporate and individual clients need for AML risk assessments?

- What sort of due diligence procedures must be followed during this process?

What is AML Risk Assessment?

An AML risk assessment is a procedure used to evaluate the potential risk posed by each customer, to reduce the likelihood of involvement in illicit activities such as money laundering, terrorism funding, and tax evasion.

It is a well-documented part of AML regulations where organizations follow the process to detect, evaluate, and interpret the chances of money laundering and other financial crimes that could affect business activities.

That is to say, these measures are taken to evaluate the entire organization’s exposure to financial crimes and put in place effective AML compliance measures to prevent them.

There is no one-size-fits-all method for managing risk, so risk variables vary depending on the industry of the firm. Common risks must be evaluated: transaction risk, product risk, geographic risk, customer risk, and service risk.

However, finding each customer’s risk based on its risk assessment matrix is what makes the AML program strong and reliable.

Crime Alert!

The Financial Action Task Force (FATF) identifies weak AML risk assessments in financial institutions as a major driver of financial crime.

Why Is AML Risk Assessment Important?

Evaluating financial risks within an organization goes beyond simply assessing the money laundering risk tied to specific individuals or entities.

While detecting potential criminals or those at a higher risk of involvement in financial crimes is essential, but it alone cannot prevent money laundering or terrorist financing from infiltrating the financial system.

Given that money laundering tactics are constantly evolving and criminals are always seeking new ways to exploit vulnerabilities, organizations must establish clear policies and procedures that emphasize the importance of a comprehensive and effective AML risk assessment program.

AML Risk Factors to Consider

The following are some common risk factors that may be very useful while conducting AML risk assessment.

Customer Profile

Different types of customers pose different levels of risk depending on customer background and the services and products you offer.

Business Size and Complexity

The larger the business, the higher the chances of getting trapped in financial crimes. If your business structure is more complex, combating crimes faces greater challenges.

Transaction Size and Type

High-value or cross-border transactions are often used to evade reporting requirements, raising the risk of illicit activity.

Who Writes The Rules and Establishes AML Regulations?

From FATF recommendations to FinCEN, and FCA, EBA regulations, every organization dealing with financial transactions must conduct robust AML risk assessment to enhance sanction compliance and assure the security of these transactions.

Businesses need to conduct globally recognized standards to provide a unified approach. For instance, the Financial Action Task Force (FATF), a key regulatory body, offers essential guidelines, including its 40 recommendations, which nations can implement within their own regulatory frameworks.

Other global criteria for AML compliance include:

US-The Bank Secrecy Act (BSA)

Bank Secrecy Act (BSA) mandates that financial institutions carry out regular AML risk assessments to identify and reduce risks associated with money laundering and terrorism funds with the FinCEN 2020 CDD Rule strengthening standards for customer screening and risk-based monitoring.

UK-The Proceeds of Crime Act (POCA)

Companies in the UK are required under the Proceeds of Crime Act (POCA) to do AML risk assessments and use a risk-based strategy for client due diligence.

For high-risk clients, the FCA rules (2021) place a strong emphasis on increased monitoring.

EU-Anti-Money Laundering Directives (AMLDs)

Sixth Anti-Money Laundering Directives- AMLD6 (2020) mandates that EU institutions conduct risk-based AML assessments to comply with greater surveillance of high-risk transactions, improved due diligence, and beneficial ownership transparency.

The Proceeds of Crime (Money Laundering) and Terrorist Financing Act

Institutions in Canada are required to do AML risk assessments that take regional, customer, and service concerns into account.

The 2020 revisions to FINTRAC mandate adherence to the risks associated with cross-border transactions and virtual currency.

Do you want to know what happens when institutions fail to follow these regulations?

Let’s explore this;

How Institutions Held Responsible for Where Legacy System Fell Short

Time to revise the concept with real-life cases, where institutions ignored following AML risk programs and got serious penalties from authorities.

Bank of America Failure to comply with AML

Bank of America faced serious regulatory action in December 2024 due to inadequacies in its AML risk assessment methods.

According to the Office of the Comptroller of the Currency (OCC), the bank was in danger of allowing money laundering and terrorism funding because its systems were insufficient to detect suspicious activity.

- Bank of America has not implemented efficient AML risk assessment procedures, particularly when it comes to monitoring foreign transactions.

- The OCC discovered a number of problems with the bank’s transaction monitoring system, limiting its ability to detect suspicious behavior rapidly.

- As a result, the bank had to hire an outside consultant to help tighten its systems, implement more strict monitoring methods, and restructure its AML compliance framework.

Metro Bank and Inadequate AML Risk Assessments

The UK Financial Conduct Authority (FCA) fined Metro Bank £16.7 million in October 2024 for major deficiencies in their AML risk assessment.

The FCA discovered severe flaws in Metro Bank’s automated transaction monitoring system, which allowed considerable amounts of money to go unnoticed.

- Metro Bank’s AML system failed to detect suspicious activity due to a failure to monitor over 60 million transactions worth £51 billion.

- The FCA became aware of the bank’s poor risk-based strategy in its compliance systems and suggested that it enhance its AML risk assessments.

- The settlement required Metro Bank to strengthen its client due diligence, tighten its anti-money laundering procedures, and create efficient transaction monitoring.

Do Institutions Face Challenges In Implementing An AML Risk Program?

Establishing and maintaining an efficient AML risk management program can be impacted by several obstacles.

These challenges require careful analysis and proactive actions for compliance and improved risk management of finances and reputation.

Among the main challenges to successful AML risk management are:

Data Quality Issues

AML risk assessment relies on accurate and thorough transaction and customer data. Risk assessments may not be as effective if the data is insufficient, inconsistent, or erroneous.

Outdated AML DATA

To enable accurate risk assessments and prevent dependence on outdated aml data, it is essential to regularly update client information, including sanctioned, criminal history, and PEP screening, as well as externally derived information, such as from negative publicity.

Risk Scoring Model Limitations

For risk assessments to be comprehensive and successful, risk-scoring models need to be strong, well-designed, thoroughly documented, and routinely evaluated and improved.

Real-time Risk Detection

Dynamic AML risk assessment relies heavily on the capacity to update risk profiles in real-time based on ongoing monitoring operations, such as transaction analysis, watchlist screening, and evaluation of client attribute changes.

Data Integration Difficulties

It can be difficult to integrate data from different internal and external sources, like customer databases and transaction records, because of format and system differences as well as problems with data quality.

Resource Constraints

Access to trustworthy data sources, a strong technology infrastructure, and qualified staff are necessary for thorough risk assessments. Organizations that have access to limited resources may find these standards difficult to meet.

Looking for a solution to handle all the challenges in your AML risk assessment process while ensuring compliance with AML regulations?

We’ve got the perfect solution for you, equipped with top-tier AML screening tools.

Can Any Vendor Elevate Risk Assessment Across All Businesses?

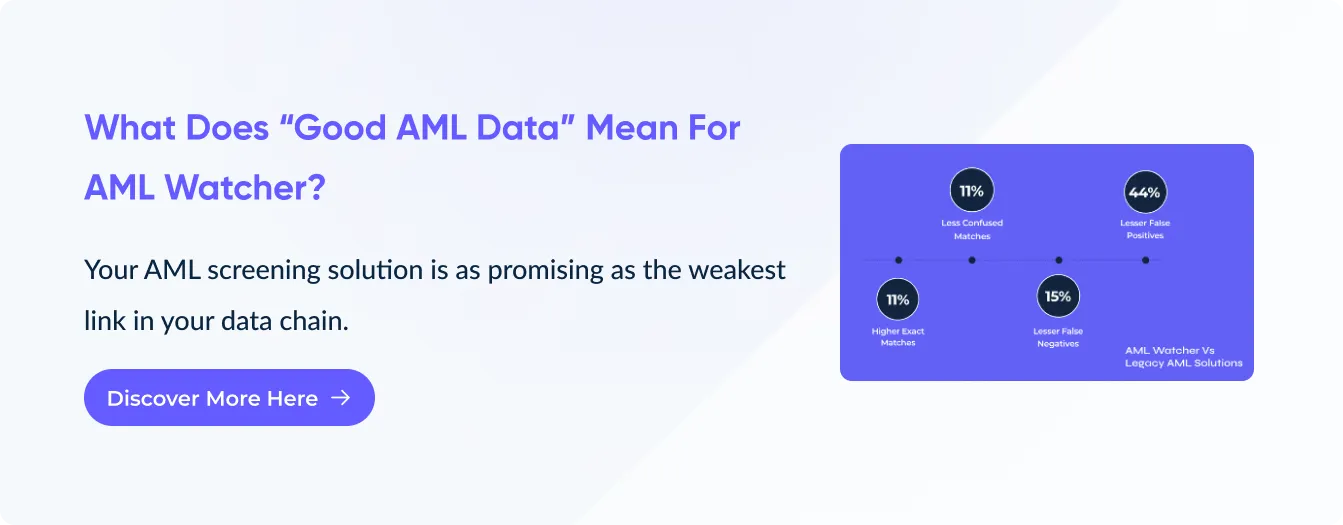

AML Watcher meets the most serious challenges that financial institutions come across when performing efficient AML risk assessments.

From real-time screening to unique risk scoring to accuracy aided by quality data sources and global regulatory compliance, AML Watcher offers great solutions that can help the accuracy of AML risk management with 50% less cost than other vendors.

AML Watcher can help financial institutions and non-financial institutions prevent financial crime, maintain the pulse on regulatory changes, and enhance the effectiveness of an AML compliance program.

How?

With its:

Global Coverage for Cross-Border Compliance

AML Watcher combines watchlists, sanctions lists, and adverse media data from over 100000 databases in over 80 languages to meet various international AML compliance standards.

Financial institutions can efficiently facilitate cross-border transactions, thus meeting numerous international regulations and minimizing jurisdictional risks.

Comprehensive Watchlist Screening

AML Watcher provides access to over 3500 official watchlists, including restricted party lists, fugitive lists, and debarment lists.

- Allows institutions to identify high-risk individuals and entities associated with financial crimes.

- Helps assess the risk level of each individual or entity by cross-referencing clients against these lists.

- If there’s a match, the institution can further investigate the profile or transaction to determine the potential for illicit activities.

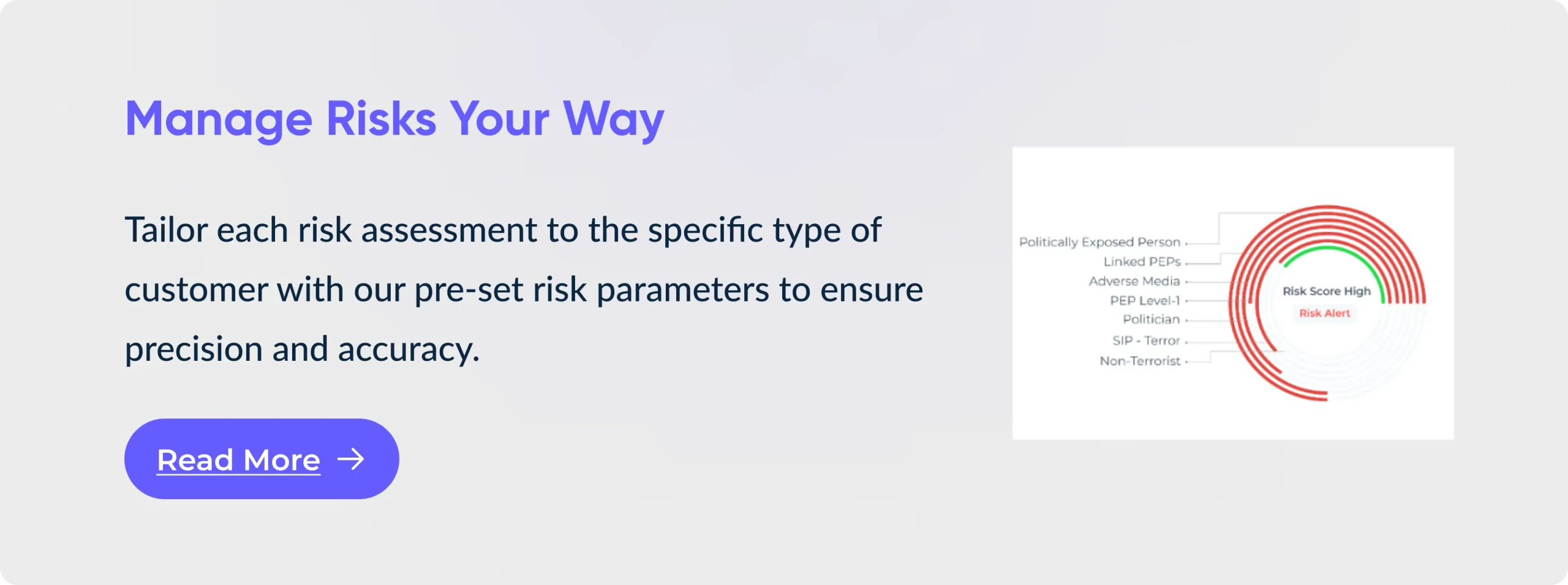

Configurable Risk Scoring

AML Watcher’s configurable risk rating algorithms where institutions may set parameters according to their own risk appetite and regulatory requirements.

- Incorporates scoring based on transaction history, geographical risk, and customer risk profiles.

- Institutions can prioritize high-risk organizations for additional inquiry to give risk ratings to transactions and consumers.

- Ensures an AML risk management procedure that is more focused and effective, directing resources where they are most required.

Politically Exposed Persons Screening

AML Watcher offers a comprehensive and unified PEP database with more than 2.1 million profiles covering more than 235 countries.

- Ensures complete visibility across client portfolios by including both domestic and overseas PEPs.

- Assists organizations in conducting a thorough risk evaluation of the client relationship by flagging PEPs in real time.

- Ensures that any possible conflicts of interest or suspicious activity are promptly found and addressed. Enhanced due diligence (EDD), which adds another level of examination to the AML procedure, is then applied to PEPs.

Adverse Media Screening

AML Watcher leverages Natural Language Processing (NLP) and structured sentiment scoring to review over 50K international and local news sources.

- It helps to identify negative media that can involve risks associated with money laundering, fraud, or financing of terrorism.

- In the case of negative news stories, the risk level for a particular client or transaction is boosted very fast.

- Ensures no adverse media is left unseen to provide institutions with a detailed analysis of the risk of money laundering or other financial crimes that may be associated with the media in its coverage.

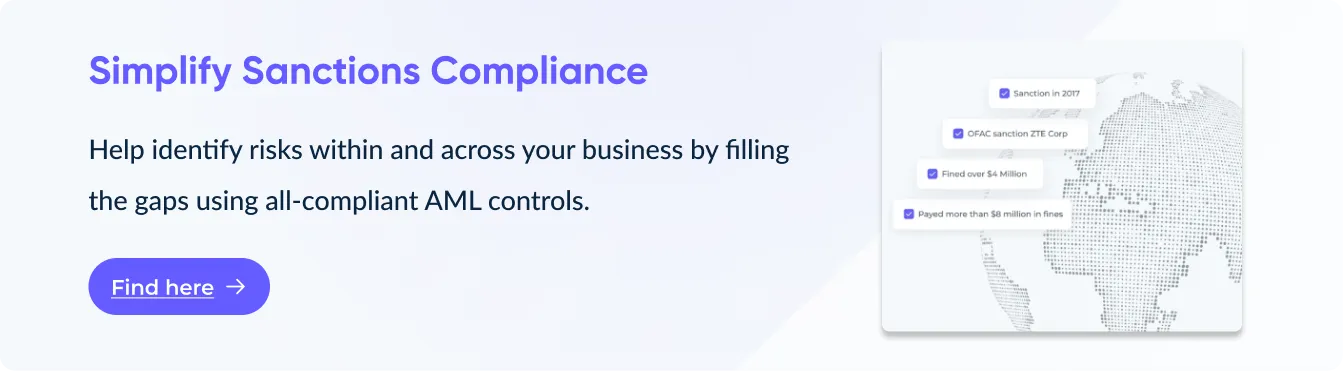

Detailed Sanctions Screening

Get real-time sanction screening against international sanctions lists, such as OFAC, EU, UN, and others.

- Improve correctness, entity connections, and aliases are added to the data.

- Significant legal and financial dangers are associated with sanctioned organizations or persons.

- Financial institutions can improve their AML risk assessment and compliance status by promptly evaluating any possible sanctions concerns.

Ongoing Monitoring and Real-Time Alerts

AML Watcher offers real-time alerts on transactions that match watchlists, adverse media, or sanctions lists.

- Constant supervision of the transactions offers continuous supervision that makes compliance standard.

- With real-time monitoring in place, particular risks can be modified as they evolve, and new risks can be detected while the institution can identify any suspicious activity instantly.

- Assist institutions in meeting lawful requirements and is on the right side in fighting and deterring wrongdoers.

Enhanced Customer Risk Profiling

AML Watcher provides advanced risk profiling by combining information from PEP lists, watchlists, and negative media sources.

- For each customer, institutions can develop a thorough risk profile that helps in deciding if enhanced due diligence (EDD) is necessary.

- This customized profile makes sure that consumers who pose a greater risk are identified and properly tracked.

- Institutions can better deploy resources to high-risk clients by tailoring the risk levels to business demands.

- No commitment needed

- Complete AML Database at your service

- Access our all-in-one dashboard

Tier-2 PSPs in ... must demonstrate automated monitoring, layered CDD, &...

See the Full Regulatory Expectation70–80% less manual work, 95% less fatigue, TruRisk Agent makes compliance effortless.

Experience Agentic AMLMove Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries