How Does Open Banking Improve Customer Due Diligence?

Due Diligence

April 11, 2025

Open banking opens doors to data sharing. Is it an opportunity to simplify customer due diligence (CDD) in banking or a threat to complicate it further?

In this blog, we’ll explore how access to financial data can have an impact on AML compliance for both seeking and providing financial services.

What is Open Banking?

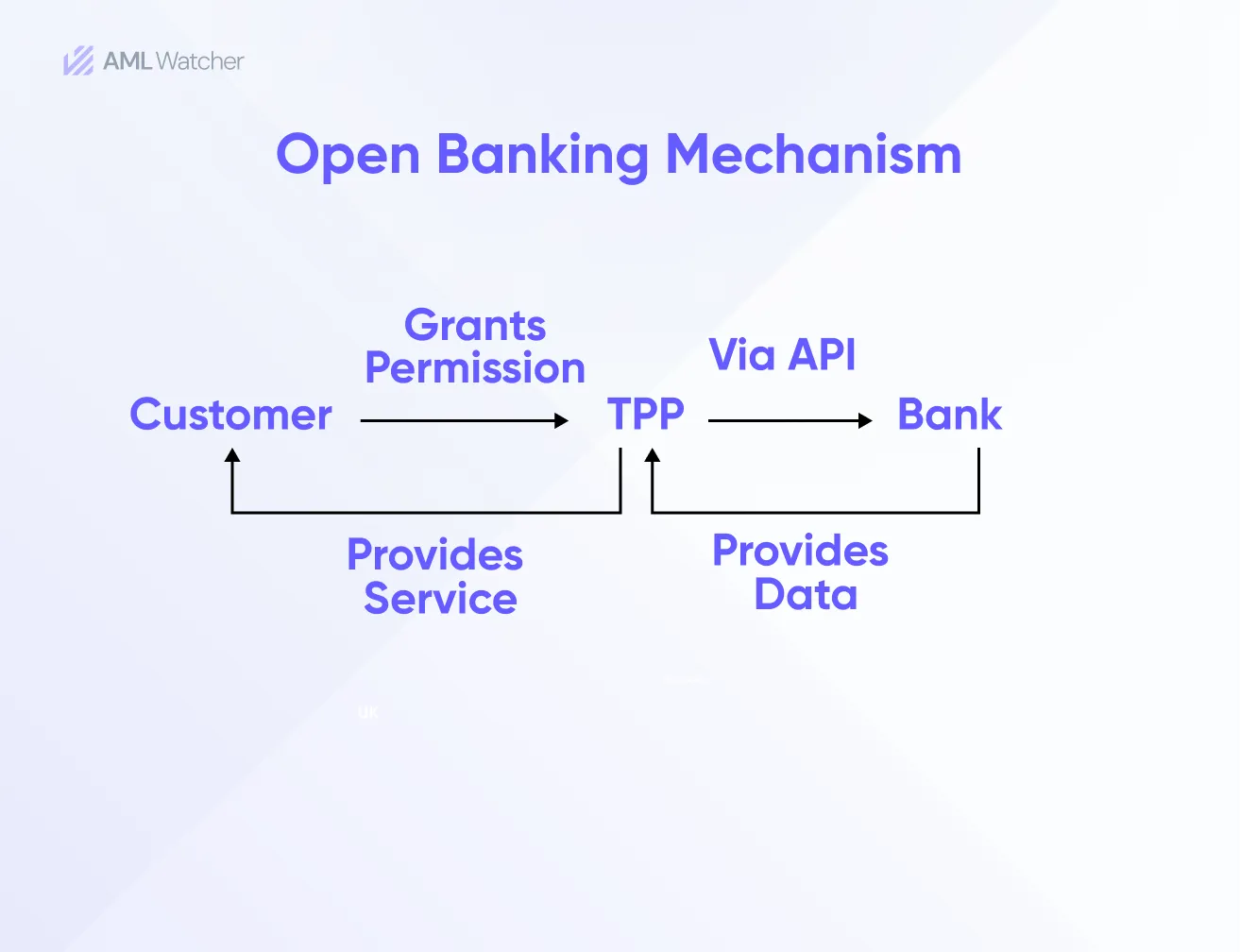

At a fundamental level, Open Banking is a system that allows customers to grant permission to third-party providers (TTPs) to fetch their financial data held by banks and other financial institutions in one place.

Open Banking allows account holders to see a wider picture of all their bank accounts, account balances, payments, and spendings in one place.

On the other hand, TPPs (like FinTechs) can use this information to provide innovative and customized products and services that best suit the circumstances of each customer.

The core element behind developing Open Banking was to promote healthy competition within the financial sector and ultimately allow customers to make more informed decisions about their money.

What are the Trends and Scope of Open Banking?

Open Banking, which started as a regulatory tool in Europe in 2018 (as a result of revised PSD2) to stimulate healthy competition within the financial sector to enhance transparency in financial dealings, ultimately allowing customers to make more informed decisions about their money, quickly became a global phenomenon.

According to a report by Open Banking Ltd, as of January 2025, there were 13 million users of open banking in the United Kingdom alone. It is estimated that the global Open Banking market size exceeded $30.89 billion in 2024.

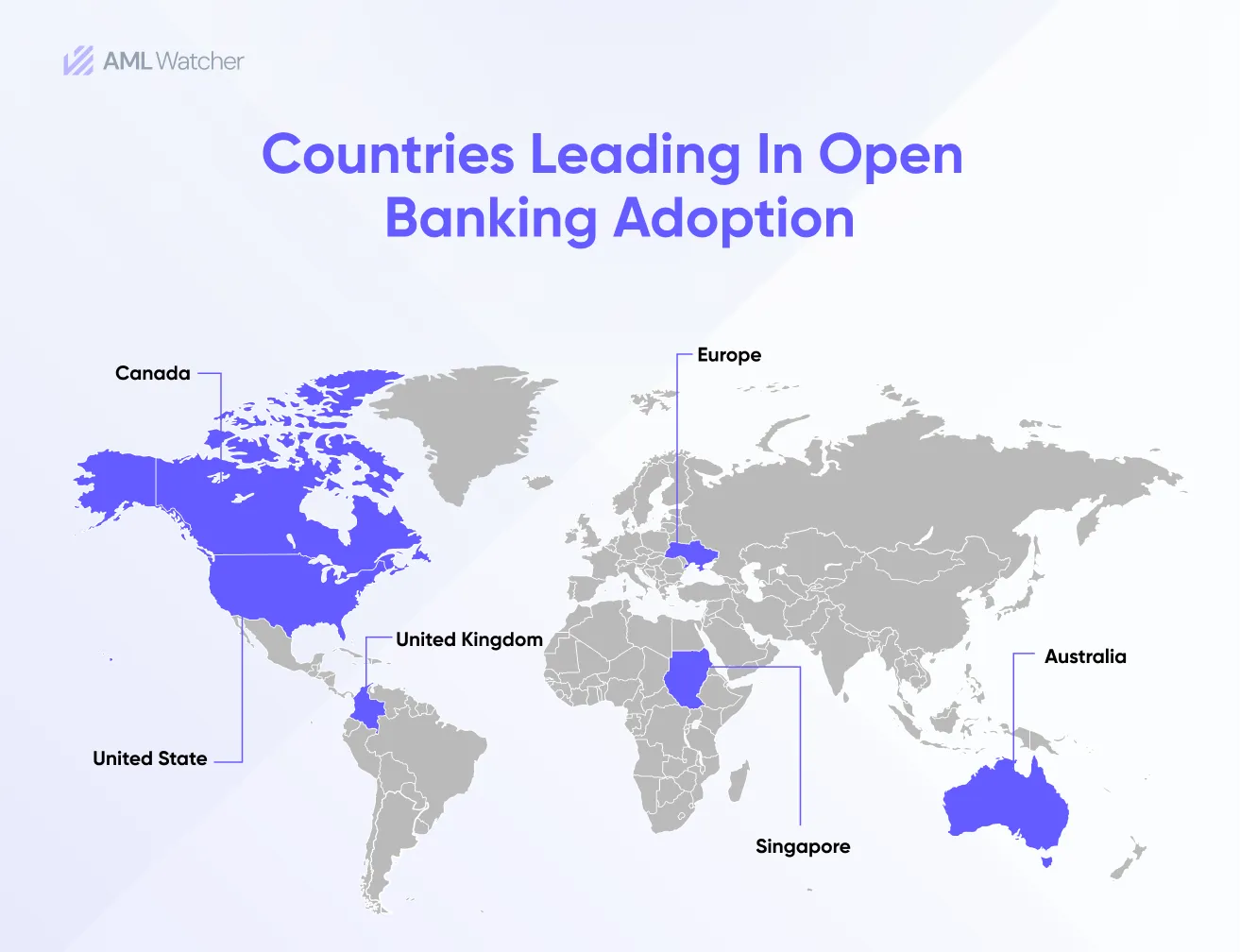

Today, Open Banking is growing at exponential rates across different markets on the globe, including the United Kingdom, Singapore, Australia, Canada, and the United States.

Open Banking and Customer Due Diligence (CDD)

Open banking enables TPPs to get access to client information like account identification and transaction details held by banks and other financial institutions.

CDD in banking is one of the main pillars holding AML compliance. Following are some examples of how open banking can enable improved compliance with the customer due diligence checklist:

Instant Client Onboarding

With access to already verified KYC information, businesses can onboard new customers instantly. This significantly cuts the time consumed in chasing documents, ultimately improving client experience and reducing compliance costs.

Accurate Risk Profiling

Access to wider information like customer spending, transaction patterns, and financial behavior means institutions can now develop more accurate risk profiles of their customers in order to apply risk-based CDD measures.

Enhanced Ongoing Monitoring

Real-time access to transaction data of a customer across different platforms allows businesses to detect any deviation from expected behavior at an early stage. This effectively reduces the risk of financial crimes.

Open Banking Regulations

One of the most important drivers that paved the way for the development of Open Banking was the revised Payment Service Directive (PSD2) of the European Union that mandated banks to share the client’s data with the TPPs.

Other notable OB Regulations include the UK’s Open Banking Initiative CMA9 that started in 2018 and mandated the top 9 larger banks to open their APIs for the authorized TPPs.

The Consumer Data Right (CDR) Law enables customers in Australia to share their banking information with third-party providers.

The Personal Financial Data Rights rule of the Consumer Financial Protection Bureau, finalized in October 2024 under Section 1033 of the Dodd-Frank Act, is a major milestone toward OB Regulations in the US.

Canada has also introduced its Consumer-Driven Banking Framework, outlining core elements for the implementation of Open Banking.

Applications and Use Cases of Open Banking

Open banking is transforming the financial landscape by unlocking the power of smart data for the development of innovative and customer-centric services.

Following is a list of key use cases and Open Banking Examples:

- Payment initiation, direct payments without involving card details

- Quicker Loan approvals, with real-time access to client history

- Account aggregation allowing expense tracking and budgeting

- AML Compliance (faster onboarding and better risk detection) with access to verified identity and transaction data

- Subscription management by helping users to track and cancel unwanted subscriptions

- AI-based insights based on real-time financial behavior

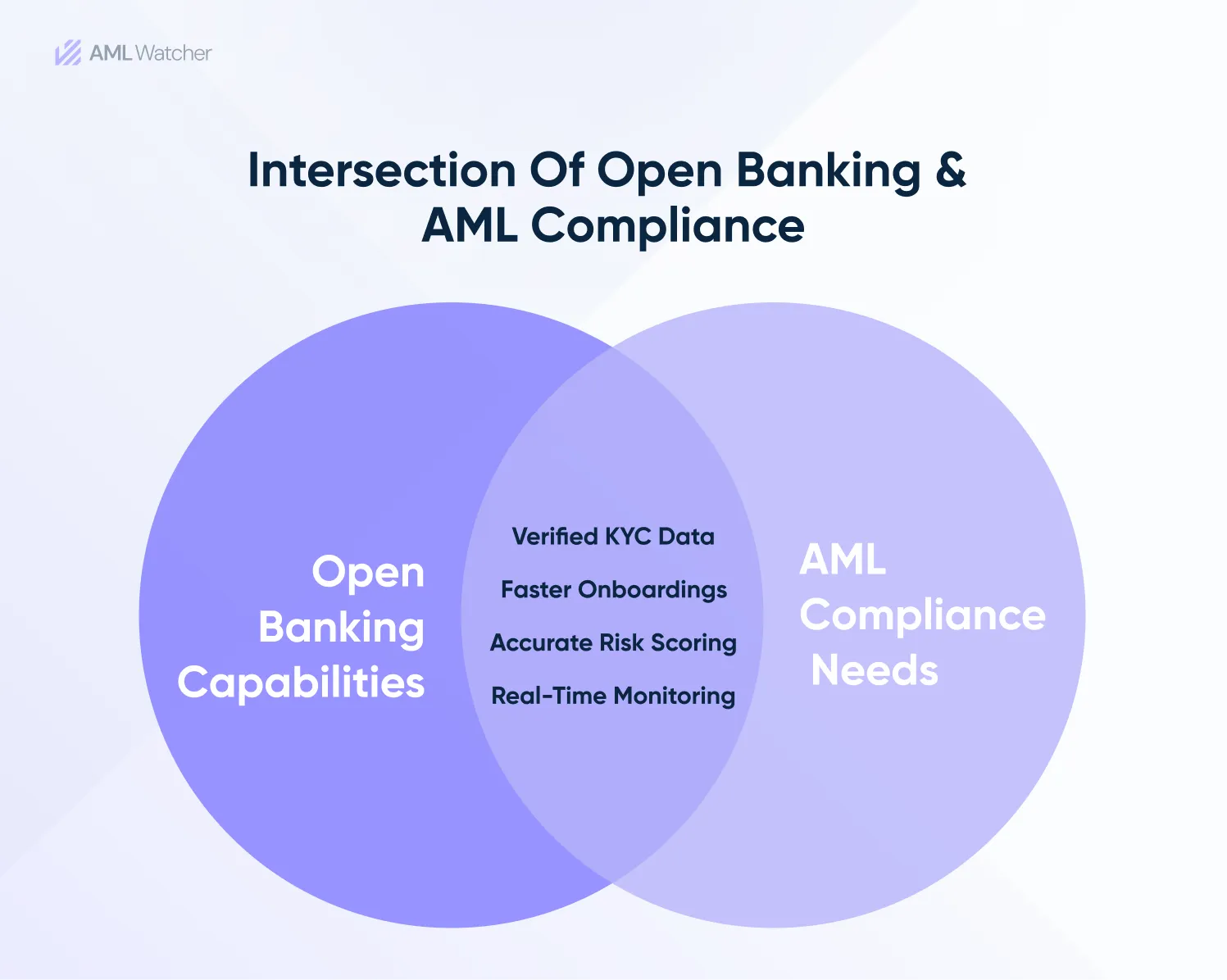

How Open Banking and AML Compliance Intersect?

Open Banking is transforming the way businesses have been onboarding new clients and conducting risk assessments. Open banking KYC allows instant onboarding by retrieving verified account details (done with appropriate authentication and permission of a client).

The availability of wider KYC data (e.g., country of residence, date or place of birth, etc) means fewer false positives when doing customer screening against sanctions lists or PEP lists.

dditionally, real-time access to full transaction history and spending patterns across different platforms allows for accurate risk profiling and early detection of any unusual behavior. This ensures the business stays compliant with AML regulations while cutting on compliance costs and improving client experience.

The connection between Open Banking and AML compliance is accurate, especially in terms of KYC data usage and transaction monitoring.

AML Watcher Empowering AML Compliance with Open Banking

Stay ahead of financial crime with AML Watcher. AML Watcher empowers Open Banking solution providers with a global footprint to manage AML risks.

With key features like advanced sanctions and PEP screening, customizable risk scoring, and transaction monitoring, we help businesses implement open banking solutions without the risk of non-compliance.

Cut your compliance costs up to 50% and get access to our real-time, updated, proprietary database of:

- 415+ risk categories

- 3500+ criminal watchlists

- 215+ Sanction Regimes

- 2.6 Million PEP Profiles from over 235 jurisdictions

Frequently Asked Questions

- No commitment needed

- Complete AML Database at your service

- Access our all-in-one dashboard

Tier-2 PSPs in ... must demonstrate automated monitoring, layered CDD, &...

See the Full Regulatory Expectation70–80% less manual work, 95% less fatigue, TruRisk Agent makes compliance effortless.

Experience Agentic AMLMove Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries