What Is Transaction Fraud and How Can Businesses Detect It

Transaction Monitoring

January 30, 2026

Transaction fraud is emerging as a significant threat to companies in the online economy. With the growth of online payments and international business, the number of fraud attacks is increasing. These attacks range from chargebacks to account takeovers and scams that target both merchants and consumers. According to Juniper, online payment fraud was expected to cost global e-commerce merchants an estimated $44.3 billion in 2024, rising to $107 billion by 2029. This figure highlights the severity of the issues that businesses have to deal with in the contemporary era.

Outdated detection systems mostly fall short when dealing with advanced fraud schemes. Businesses require advanced data-driven strategies to stay one step ahead.

The article will focus on the significance of transaction fraud detection, the challenges businesses face, and the technology used to curb this menace.

What is Transaction Fraud?

Transaction fraud is committed when a fraudster obtains access to a financial account or payment illegally (in many cases, online platforms or digital payment methods are involved). It may be in various forms, such as the fraudulent transactions done using stolen credit card information or complicated strategies involving card-not-present transaction fraud.

Both businesses and consumers are highly concerned with such fraudulent activities that destroy trust in online transactions and result in huge losses of money.

Why Transaction Fraud is Hard to Detect at Scale

The emergence of online payment systems and the transition to the cashless economy have exposed businesses to more chances of transaction fraud. Fraud methods are evolving at an alarming pace, and businesses are finding it challenging to fight such advanced fraudsters.

Here are a few reasons why transaction fraud is hard to detect at scale:

Fraud Techniques Evolve Rapidly

Traditional detection systems are increasingly being outsmarted as fraudsters evolve their methods, employing innovative techniques such as social engineering, authorized push payment (APP) scams, mule networks, synthetic identities, and credential stuffing.

Legitimate-Looking Transactions

Most of the contemporary fraud can be characterized by authorized or seemingly regular transactions, thus being hard to differentiate from legitimate customer activity.

Limitations of Rule-Based Systems

Static detection systems are based on fixed rules and thresholds, which are not able to detect complex, coordinated, and low-value fraud patterns at scale.

Large Transaction Volume in Digital Payments

During the processing of millions of transactions in real time by businesses, it is harder to detect subtle signals of fraud without creating delays.

Lack of Transparency in the Fraud Cycles

Multiple accounts, devices, or institutions often involve fraud, but the detection systems usually work on individual data, minimizing contextual awareness.

Trade-off Between Customer Experience and Fraud Prevention

Stricter controls have the benefit of reducing fraud, but more false positives, which causes businesses to apply less restrictive rules, letting more fraud go to scale.

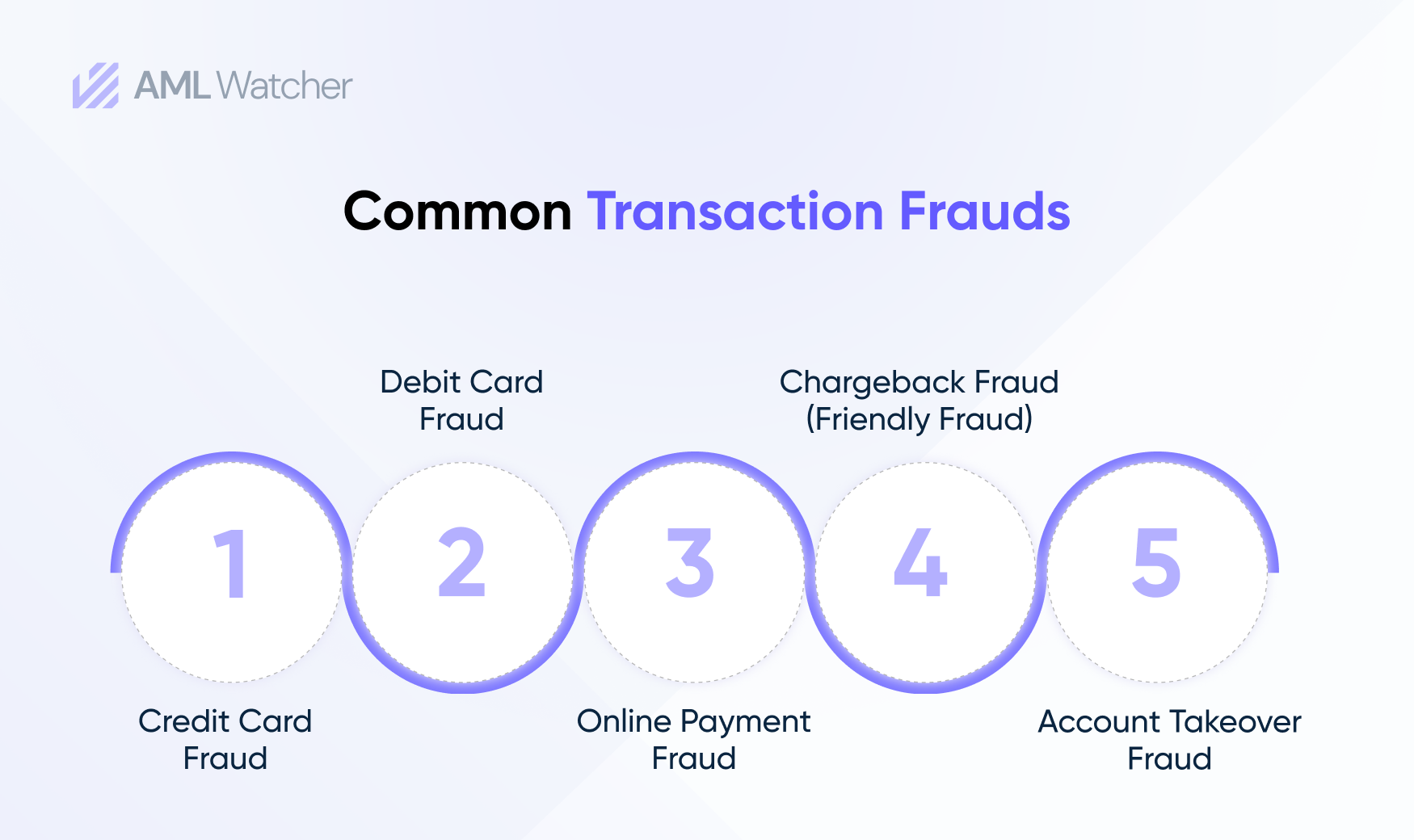

Common Transaction Fraud Schemes in Online Payments

Businesses should know about various forms of transaction fraud:

- Credit Card Fraud: Credit card fraud usually happens when criminals steal the credit card details and use them to make false purchases.

- Debit Card Fraud: Fraudsters steal the information on a debit card and execute unwarranted transactions, usually depleting the financial accounts of the victim.

- Online Payment Fraud: Fraudsters apply the stolen payment credentials to commit fraud on e-commerce websites. To gain access to credentials, criminals usually use data breaches, fake websites, malware, phishing emails, and social engineering schemes.

- Chargeback Fraud: A client uses a valid purchase through their credit card issuer, falsely claiming that they have been cheated out of a purchase, and the merchants incur losses.

- Account Takeover Fraud: Fraudsters illegally access the account of a person or a business (bank, e-commerce, etc.) and explore it to accomplish fraud.

Scale and Projection of Business Losses from Transaction Fraud

Transaction fraud is not only a financial issue but also a reputational risk for businesses.

A single fraud incident can trigger security breaches, legal infractions, and loss of customer trust that is complex to rebuild.

Beyond reputational damage, the financial impact of transaction fraud is rising each year. Businesses confront not only immediate losses of transactions, but chargebacks due to fraud are also an increasing financial liability. According to research, fraudulent chargebacks are going to increase 24% to 324 million transactions a year by 2028, of which 45% of all disputes will be fraud-related. The total number of chargebacks worldwide is projected to grow to 33.79 billion in 2025 and 41.69 billion in 2028, which is a sign of the rising danger to merchants and financial institutions.

With a growing volume of transactions and more advanced fraud methods, businesses are faced with a greater risk exposure and have to balance customer experience, compliance requirements, and operational efficiency, which makes transaction fraud a perennial and challenging problem to address.

Transaction Monitoring Vs Fraud Detection

| Transaction Monitoring | Feature | Fraud Detection |

| Suspicious patterns across multiple transactions | Focus | Immediate fraudulent activity |

| Regulatory compliance (AML, sanctions, KYC) | Purpose | Prevent financial loss and protect customers |

| Analyzes trends, thresholds, and behavior deviations | Approach | Real-time alerts, AI scoring, anomaly detection |

| Real-time or retrospective | Timing | Predominantly real-time |

| Multiple small cross-border transfers below reporting thresholds | Example | Stolen credit card used online; sudden, unusual login triggering account takeover |

How AML Watcher is Helping in Combating Transaction Fraud

Transaction fraud investigations often fail when fraud signals sit in one tool, and AML risk sits in another, which slows decisions and increases disputes.

AML Watcher supports screening and transaction monitoring in one place, helping compliance and risk teams spot unusual patterns earlier and document decisions for audit readiness.

The distinctive characteristics of AML Watcher that empower institutions are:

- Real-time Fraud Detection: AML Watcher leverages advanced algorithms and machine learning to detect fraud instantly.

- Comprehensive Monitoring Tools: The platform monitors financial transactions, such as card-not-present, payment, and online transactions, to protect businesses from different categories of fraud.

- AI-Powered Analytics: With automation, AML Watcher detects the emerging fraudulent patterns, which will allow businesses to take immediate action and prevent fraudsters from inflicting a lot of damage.

- Scalable solutions: The platform provides scalable solutions that can be adjusted to the requirements of any organization, be it a small online shopping platform or a huge financial service.

With AML Watcher, businesses can easily minimize the risk of transaction fraud and secure a seamless customer experience.

- No commitment needed

- Complete AML Database at your service

- Access our all-in-one dashboard

Tier-2 PSPs in ... must demonstrate automated monitoring, layered CDD, &...

See the Full Regulatory Expectation70–80% less manual work, 95% less fatigue, TruRisk Agent makes compliance effortless.

Experience Agentic AMLMove Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries