PEP Screening – Step to Stop Money laundering

PEP

December 28, 2023

Securing the capital position of money laundering happening globally, with more than £100 billion of laundered money every year, the United Kingdom seems to have a fragile regulatory and compliance control raising the need for robust anti-money laundering (AML) measures. The global financial system being abused by the power holders, particularly people entrusted with public functions and their associates, has created a sense of emergency for the regulatory bodies to unite on standard and effective measures to counter Financial crime threats from politically exposed persons (PEPs). Evaluated on the basis of technical compliance and effectiveness by FATF (Financial Action Task Force), PEP screening is required to be a mandatory part of AML measures for financial and non-financial institutions and other businesses.

In this blog we will take a deeper dive into the intricacies of PEP list screening and how efficiency of PEP screening methods are challenged by various technical and regulatory gaps.

Why Screening against PEPs is the Highlight of AML Control

Swaying the 2-5% of the global GDP annually, the predicate offenses, particularly money laundering, have shattered the economic stability of the global financial system. The politically exposed persons, their relatives and close associates (RCAs) are vulnerable to abuse their public power and resources to commit or facilitate flows of illicit money across the borders. Raising alerts for the institutions, particularly financial institutions, the exposed PEP compliance program and neglected checks on persons not mentioned in their screening books encourages them to abuse their political power and manipulate the financial systems.

Holding millions of euros (€94 million) in the Bank of Valletta, junior Ghaddafi, the son of Muammar Ghaddafi, a Libyan dictator, was found accused of money laundering and keeping the illicit money in several credit card and savings accounts. Leveraging the loopholes of incompetent screening protocols of the Bank of Maltese, Mutassim Ghaddafi trespassed the red alerts which could have been prevented if went through robust PEP screening solutions. With immeasurable amounts of money being laundered through PEPs and RCAs, the globally reported financial crime cases highlight the involvement of PEPs in most of the money laundering scandals.

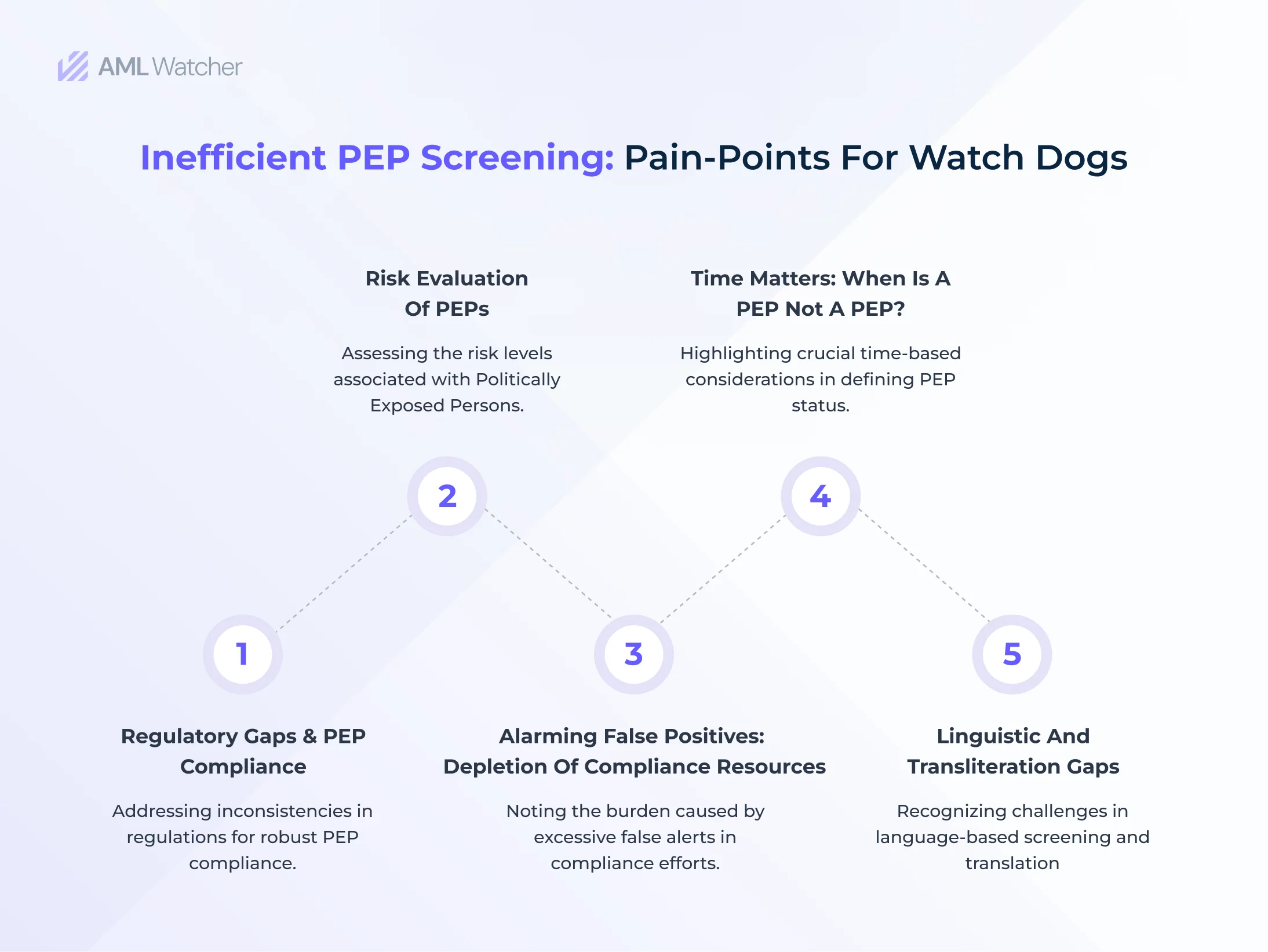

Inefficient PEP Screening Pain-Points for Watchdogs

Ever growing corruption industry costing approximately $2.6 trillion annually not only raises questions on the ineffective preventive and screening measures but the gaps in technical compliance and effectiveness are held responsible for creating a deteriorating financial system security. The regulatory and crime fighters face several challenges while implementing a robust PEP compliance program of which we are going to explore a few significant gaps below.

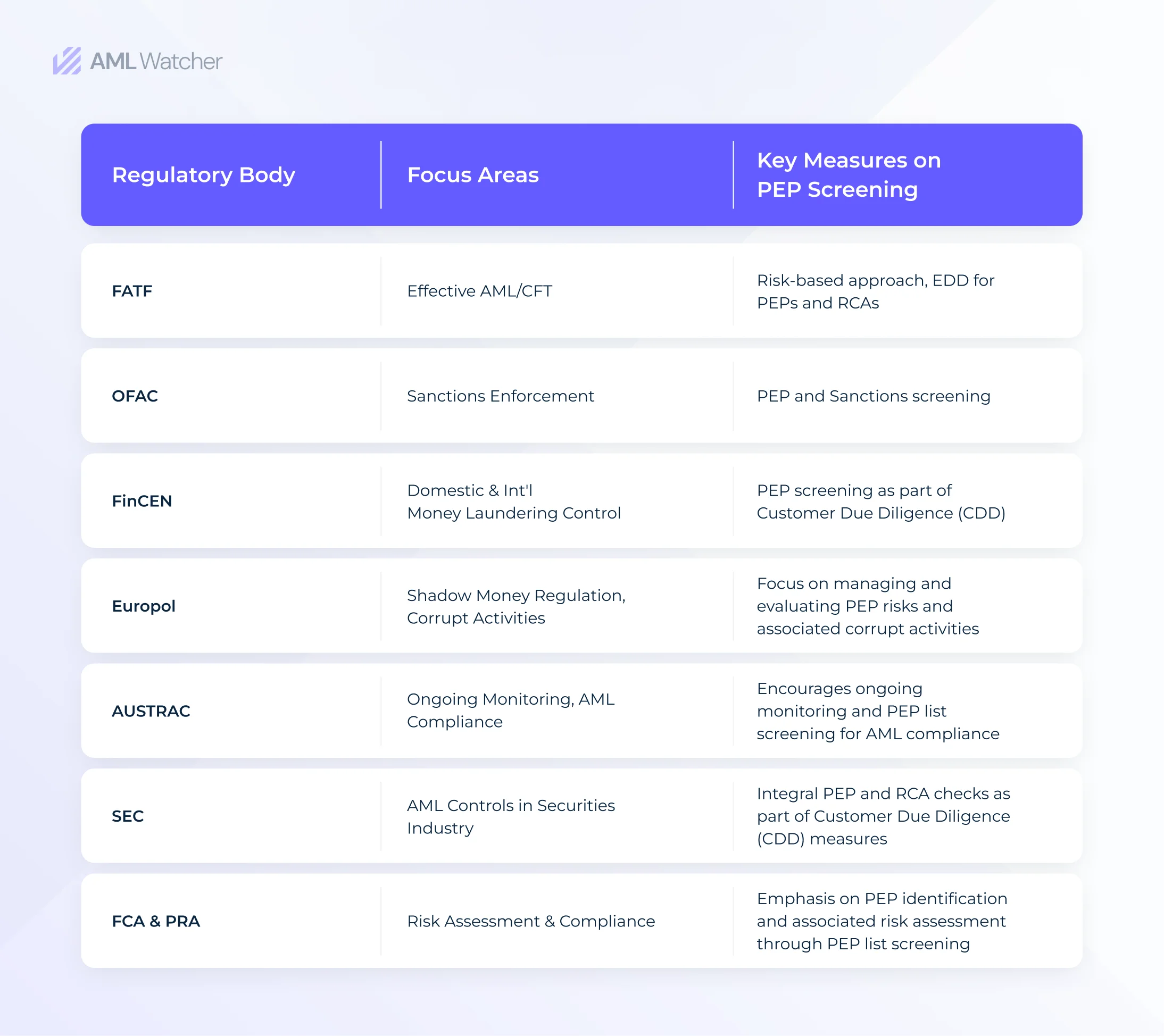

Regulatory Gaps & PEP Compliance

Subjected to call for an action against financial crimes and compliance breach, different jurisdictions and regulatory bodies aiming towards a united cause have set various regulatory measures and compliance programs to be practiced within the institutions and businesses.

The Financial Action Task Force (FATF) underlining the importance of effective AML measures to fight money laundering, terror financing, corruption and bribery, has established its globally recognized recommendations to be followed. Including regional organizations European Commission and the Gulf Cooperation Council, FATF with its 37 member jurisdictions has called attention to implementation of EDD (enhanced due diligence) and a rigorous risk-based approach while dealing with PEPs and RCAs.

The Office of Foreign Assets Control (OFAC) being a part of U.S Department of Treasury majorly regulating the sanctions against specific countries and individuals along with entities present in SDN (Specially Designated Nationals and Blocked Persons) list, enforces the implementation of PEP and sanctions screening to certainly cease the prohibited transactions and business relationship.

The Financial Crimes Enforcement Network (FinCEN) in an effort to fight against domestic and international money laundering activities, with no uniform definition for PEPs, enforces the financial institutions to implement PEP screening as a part of their CDD (customer due diligence).

The Europol (European Union Agency for Law Enforcement Cooperation) with no PEP definition outlined in the books, enforces the member jurisdictions to manage and evaluate the PEP risks and associated corrupt activities while regulating the flow of shadow money.

The AUSTRAC (Australian Transaction Reports and Analysis Centre) encourages the financial institutions to adopt ongoing monitoring and enforces the conduction of CDD along with PEP list screening to stay compliant with AML requirements.

The SEC (Securities and Exchange Commission) administering the AML compliance control against financial security threats associated with securities industry, investment businesses, and broker dealers, imposes the practice of robust checks against PEPs and RCAs as an integral part of CDD.

The FCA (Financial Conduct Authority) and PRA (Prudential Regulation Authority) in the United Kingdom underlines the importance of PEPs identification and associated risk assessment. The jurisdiction coerces the practice of screening against PEP lists as a cornerstone of customer due diligence measures within the institutions.

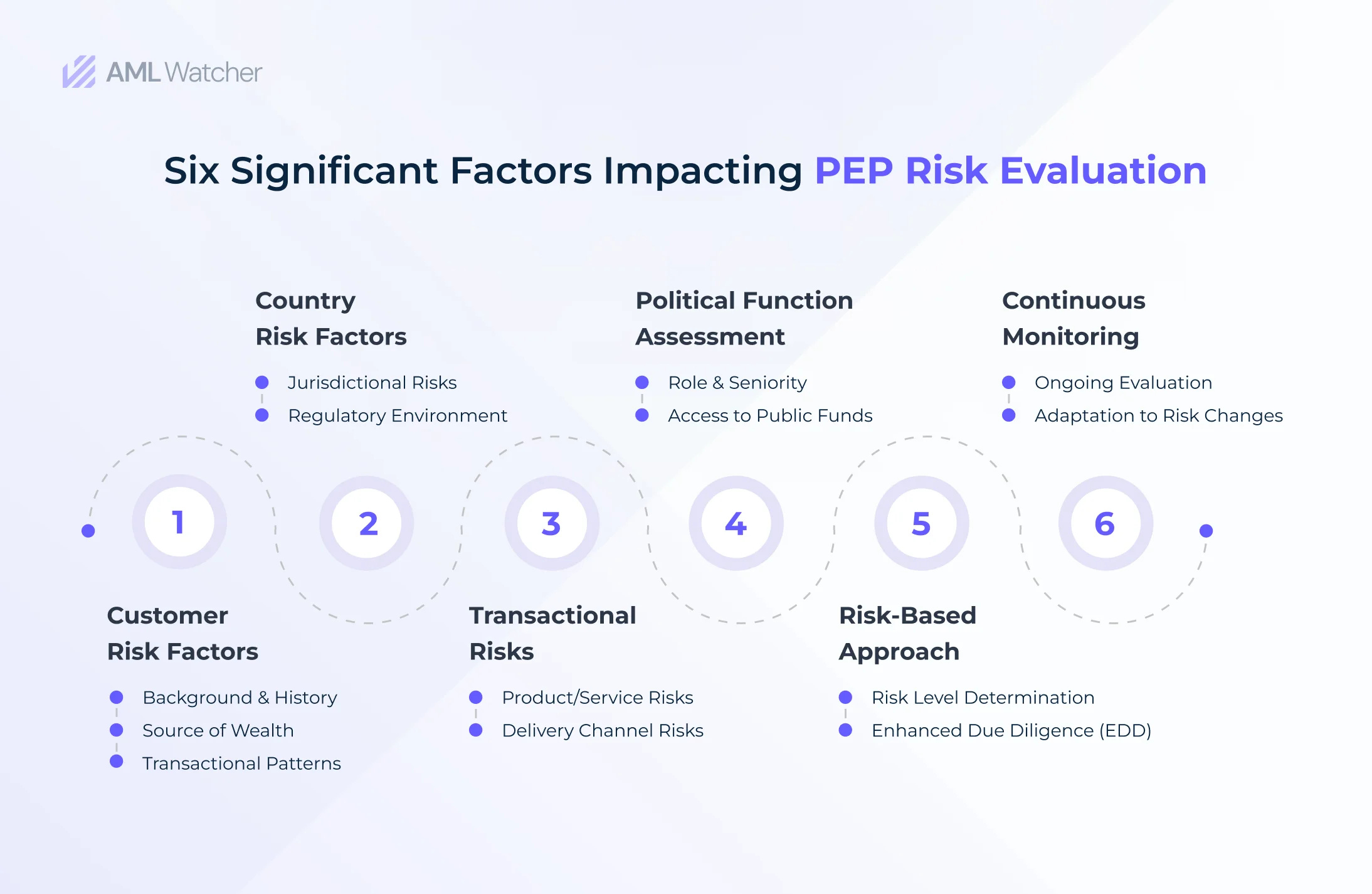

Risk Evaluation of PEPs

Ascending in the severity of risks associated with potential money laundering and corruption threats, politically exposed individuals and their associates are assessed in four different levels ranging from lowest to high risk PEPs. According to FinCEN published guidelines on PEPs and their risk evaluation, the scale and circumstances of threat varies in relevance to the customer relationship. Maintaining a lower risk profile, PEPs and RCAs with acknowledged funds and sources, and ownership of products aligned with AML requirements do not pose an alarming threat to the sanctity of global financial systems. However, not exempted from the scrutiny process on a regular basis, PEPs on an ongoing PEP AML risk are monitored after going through initial due diligence. Posing more threat of money laundering through off-shore accounts, international PEPs are highlighted as high-risk PEPs and their screening against enhanced due diligence is encouraged by the regulatory bodies as a pivotal part of AML/CFT measures.

Relative and Closed Associates (RCAs) in PEP anti money laundering compliance hold a significant concern and risks when the regulatory bodies enforce the implementation of AML/CFT checks. Considering RCAs carrying equal or sometimes even intense risks as other PEPs, the institutions and businesses are required to implement PEP screening solutions coupled with a thorough risk-based approach and management plan. Including business or social association with PEPs, the RCAs are enlisted as close friends, family members (childrens, spouses, parents, uncles, aunts, and cousins, inlaws and family friends), accountants, legal advisors, personal assistants and secretaries.

Additionally, it is imperative for crime detectors and regulators to identify the ventures of RCAs where the involvement of a PEP is possible. Therefore, a robust screening measure through PEP screening software equipped with an extensive database of covering all domestic and international PEPs along with the RCAs while accounting the impactful factors is undoubtedly the need of the hour.

Alarming False Positives: Depletion of Compliance Resources

To screen a client base of approximately one million, it takes 208 to 375 days of eight working hours to run a manual screening of 500k to 900k PEP entries, estimated by de Ruig (2008). Taking into account the cost of compliance and inconvenience the institutions grind through while implementing the AML/CTF measures, the alarming rates of false positives (an alert generation when in fact the target entry does not possess high-risk PEP level) is the focal point of concern to be addressed. Inefficiency of a thorough PEP screening bugged by time and resource consumption to tackle false positives not only leads the businesses and institutions to legal penalties but plays a role in depleting integrity of their financial system by means of facilitating predicate crimes. Along with addressing the loopholes in standard AML guidelines and reducing false positives, an efficient and robust PEP monitoring solution must perform risk evaluation based on geographic and services attributes associated with PEPs and RCAs.

Time Matters: When is a PEP not a PEP?

Does a PEP stop being a PEP when he resigns from his public service? Reflecting the approach set by the FATF “once a PEP, always a PEP” the absence of strict guidelines to determine when a PEP should cease to be monitored poses challenges for the institutions in implementing a thorough compliance measure. However, the regulatory body advises to adopt AML measures based on risks associated with the current and previous positions of the individual. Many jurisdictions believe to follow the 12 months rule continuing robust monitoring of PEPs, however the guidelines for RCAs are exempted from this timeline and need to be monitored in alignment with in-house PEP compliance program.

Linguistic and Transliteration Gaps

Creating a blind spot for effective screening against PEPs and RCAs, the nuances of linguistic and cultural ways to write names offers a big challenge for institutions to implement a robust PEP compliance. For example, a foreign PEP named John can be written in various languages based on the cultural or geographical landscape of the resident, which makes it difficult for the screening process to look for who is the most wanted one. Similarly, the Arabic and Russian notion of writing names in terms of “Bint” poses a healthy challenge for an effective PEP list screening tool to analyze the risks associated with RCAs.

How AML Watcher Implements a Robust Approach to Meet the Gaps

Reflecting the technical and regulatory challenges, AML Watcher has developed a systematic approach to equip your compliance measures while addressing the loopholes that might keep you awake at night. To put a dent in this long standing problem, choosing AML Watcher’s PEP screening service will enable you to,

- Foster a healthy relationship with your customer while implementing a robust risk-based ongoing monitoring and staying updated on the varying status of your client base

- Retrieve an extensive database of PEPs and RCAs with a broad coverage of more than 235 countries and PEP lists updating after every 15 minutes, leaving no place for a blind spot or missing on last minute update.

- Reduce the occurrence of false positives through fuzzy logic automated in the tool while preserving your business resources.

- Overcome linguistic and transliteration gaps through automation of AI/ML algorithms which transform scripts with ease.

- Align with domestic and international regulatory standards against PEPs and RCAs by implementing a rigorous check on foreign and domestic PEPs and their acquaintance.

- Unveil the hidden connections between PEPs and their association with establishing crimes while staying compliant with AML/CFT standards.

With AML Watcher, let your business thrive and evolve with changes in technology and regulations.

- No commitment needed

- Complete AML Database at your service

- Access our all-in-one dashboard

Tier-2 PSPs in ... must demonstrate automated monitoring, layered CDD, &...

See the Full Regulatory Expectation70–80% less manual work, 95% less fatigue, TruRisk Agent makes compliance effortless.

Experience Agentic AMLMove Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries