AML Checks Trends for 2026

AML/CFT

December 18, 2025

The tightening of regulations across different jurisdictions, such as the US, UK, and EU, has made Anti-money laundering checks a core requirement for everyday operations.

Weak or inadequate AML checks are no longer an option because the consequences can result in irreversible monetary, business, and reputational losses. These regulatory actions signal that manual and outdated AML processes fail to protect institutions from supervisory scrutiny or customers from fraud.

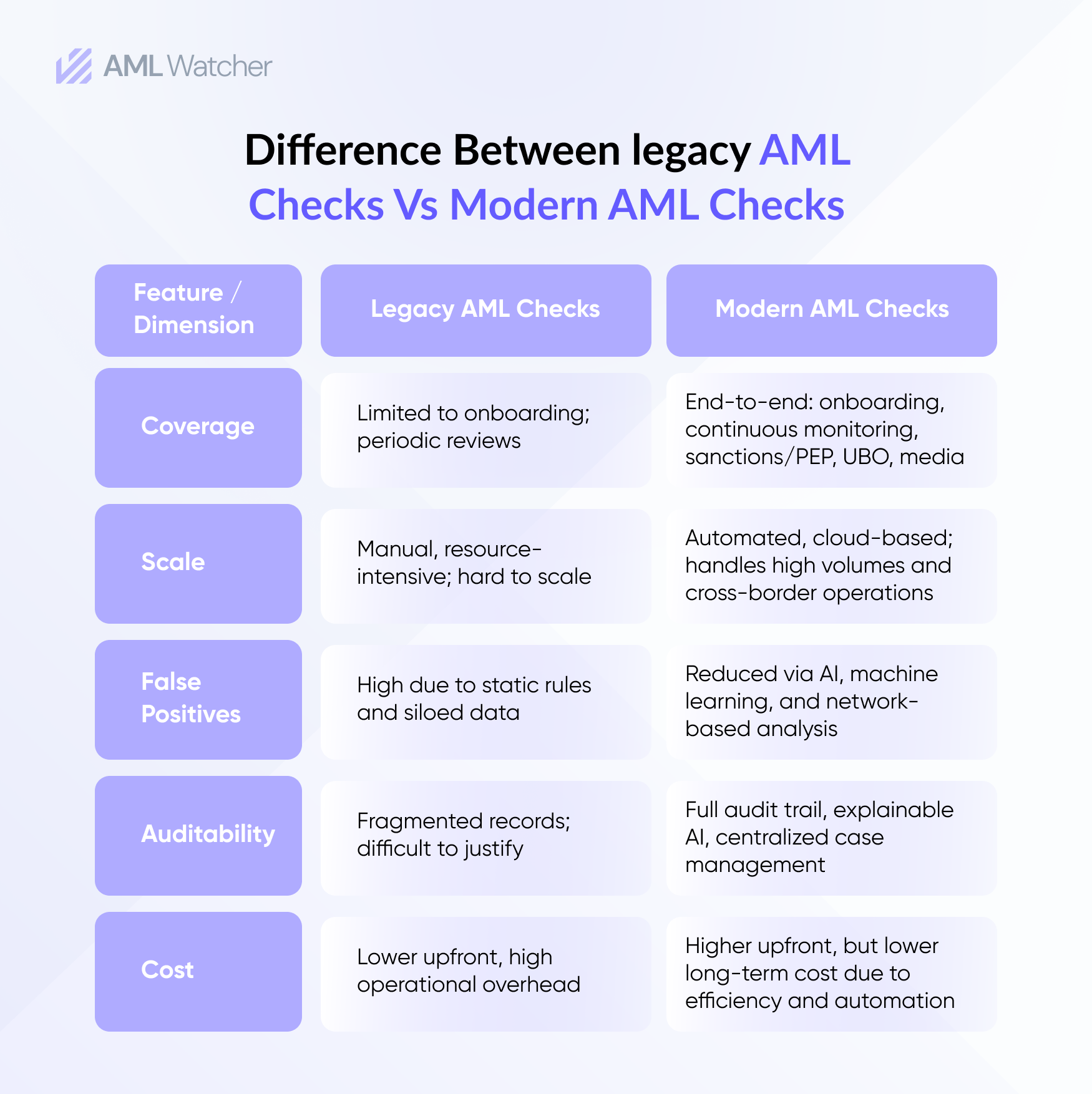

By 2026, regulatory expectations will require institutions to operate with fragmented customer data, varying regulatory standards across jurisdictions, and a growing volume of false alerts. To comply effectively, institutions must replace manual AML processes with automated, intelligence-driven systems that centralize data, ensure audit-ready transparency, and give a unified view of ownership structures with red flags.

What AML Checks are Necessary in 2026?

To meet the growing demands of 2026’s regulatory landscape, online AML checks must be more comprehensive. Here are the key components institutions should expect in AML systems by 2026:

Identity Verification & Risk Profiling

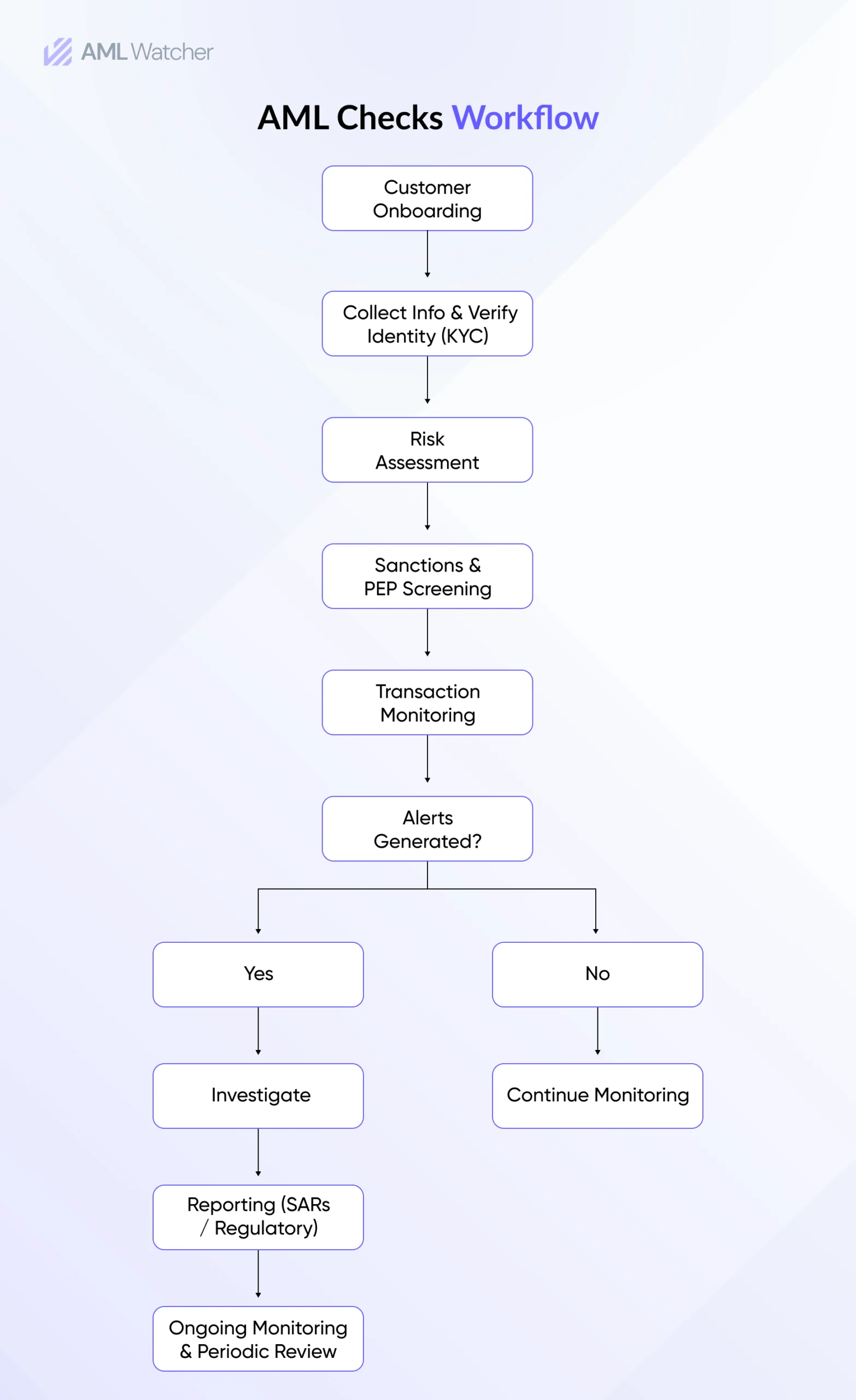

Automated AML checks must extend beyond basic identity verification. Institutions need to assess customer risk based on financial behavior, geography, product, and delivery channels, and historical data. AI-enhanced risk profiling should offer transparent, explainable risk scores, so auditors and model risk teams can trace why a customer is rated high, medium, or low. Profiles should auto-recalculate in real time when any attribute changes, with periodic review frequency tied to the dynamic score rather than fixed calendars.

Customer Due Diligence (CDD) and Enhanced Due Diligence (EDD)

Enhanced due diligence (EDD) must include deeper scrutiny for high-risk customers, such as PEPs, adverse media with negative sentiment, higher-risk corridors, and complex corporate structures. AML systems should be capable of providing a comprehensive risk review of an entity across areas like sanctions, PEP, and adverse media to determine the right level of due diligence, like EDD or CDD. Decision tests include: categorizing PEPs by seniority and jurisdiction, triaging adverse media by category, language, sentiment, and recency to reduce noise, and linking findings clearly for reviewers and regulators.

Beneficial Ownership Validation

With tightening requirements for beneficial ownership (UBO) validation, AML systems must cross-check UBOs against international registries and continually validate ownership structures beyond what is available in basic registry data. Systems should visualize ownership networks, flag opacity, bearer shares, nominee roles, fast-flipping ownership, and automatically alert when a UBO becomes sanctioned or appears in high-risk media.

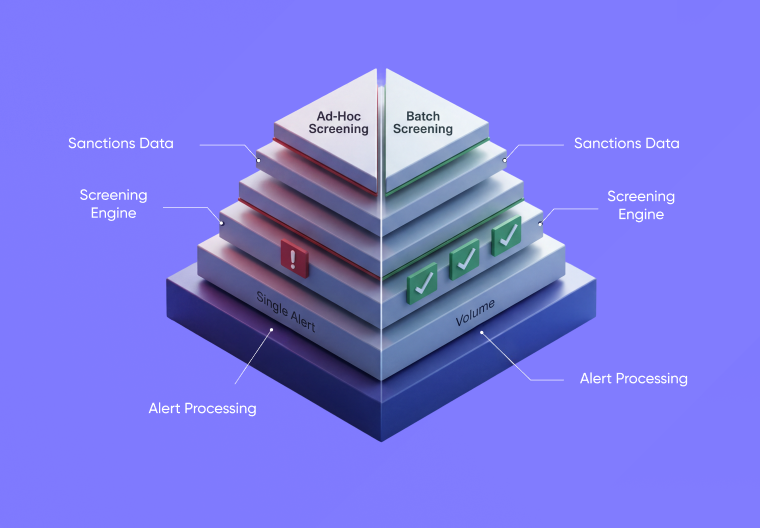

Real-Time Sanctions, PEP & Watchlist Screening

Screening against global sanctions lists, PEP databases, and watchlists must run at onboarding and continuously thereafter. Systems should use structured identifiers and ISO 20022 fields to raise match quality, maintain robust audit trails, and reflect updates quickly when designations change.

AI-Assisted Monitoring & Continuous Screening

Pair rule-based scenarios with explainable AI, graph analytics, and outlier detection. Focus on first-line review with reason codes analysts can trust, monitoring network effects like shared devices, IPs, or counterparties that suggest mule activity or nested relationships. Alerts should provide all necessary information on a single screen, and false positives should be tracked by scenario and outcome to guide tuning.

Key Regulatory Changes Shaping AML Checks in 2026

Regulatory changes impact on how institutions perform their anti-money laundering (AML) checks. Key regulatory updates that are reshaping the AML requirements are:

EU AML Regulation (AML-Reg) & AML Authority (AMLA)

Published in June 2024, the EU AML package introduces a single rulebook that applies from July 10, 2027. Complementing this framework, the Anti-Money Laundering Authority (AMLA), established in 2024 and becoming operational in 2025, will directly supervise high-risk financial institutions and coordinate enforcement across national regulators. AMLA’s mandate signals a shift from fragmented oversight to centralised supervision, raising expectations for consistent, intelligence-driven customer screening across the EU.

US FinCEN Modernization

On June 28, 2024, FinCEN issued a proposed rule to strengthen and modernize anti-money laundering and counter-terrorist financing (AML/CFT) programs under the Bank Secrecy Act (as amended by the Anti-Money Laundering Act of 2020), which would require financial institutions to adopt effective, risk-based compliance frameworks that can use advanced analytics and technology to improve risk assessment. As a result, institutions will need to do comprehensive customer checks. Meeting these standards will help them detect fraud more effectively.

Australia’s AML/CTF Reform 2026

From July 1, 2026, lawyers, accountants, real estate agents, and other specified professionals will be required to comply with AML/CTF obligations under Australia’s Tranche 2 reforms. The rules will also modernize how reports are made and support financial institutions in tracing transactions continuously. For banks and fintech companies, these regulations come with the need to strengthen their transaction monitoring systems and use automation to meet stricter regulatory requirements.

Expansion of the Travel Rule

A 2025 FATF survey found that 85 of 117 jurisdictions (73%) have passed legislation implementing the travel rule, with a further 14 jurisdictions in the process of doing so. Across the wider FATF global network, 99 of 164 jurisdictions (approximately 60%) have either enacted or are actively implementing Travel Rule measures. As these requirements increasingly shape cross-border cryptocurrency transfers, banks and crypto service providers operating across jurisdictions must rely on accurate, real-time tracking systems to manage uneven enforcement and supervisory expectations.

ISO 20022 Standardization

As ISO 20022 provides structured, standardized fields across all payment messages, AML systems can screen with greater accuracy, improving name matching, reducing false positives, and surfacing risks that were previously hidden in unstructured SWIFT MT messages. AML systems will need to effectively process and analyze the structured data to find emerging risks. Anti-money laundering (AML) systems will need to effectively process and analyze the structured data to find emerging risks.

Why 2026 is the Year of Automation for AML Checks

As technology is advancing, new risks and fraud typologies are emerging everyday, acting as a catalyst for governments to introduce new laws and regulations to counter these threats. Financial institutions and regulated sectors are feeling the pressure from regulators to demonstrate effectiveness of AML checks whereas false positives are overwhelming compliance teams.

In such an environment, automated and explainable AML checks can solve this issue, meeting regulatory expectations as well as letting compliance teams focus on actual risks.

In 2026, KYC and AML checks will transition from static reviews to intelligence-driven monitoring. This shift will push AML systems to adopt automated workflows and contextual data to identify the emerging risks.

AML programs will continue to make progress through a risk-based approach (RBA), which means that firms will invest more energy into managing high-risk entities like complex corporate structures or PEPs with adverse media. Automation enables this transformation by speeding up the due diligence and transaction monitoring procedures, offering real-time investigations, reduced false positives, and smarter alerts.

New technologies such as machine learning, graph analytics, and natural language processors will reinforce automation by encouraging customized risk scoring and ongoing monitoring of client anomalous behavioural patterns.

As a result of changing regulatory expectations, financial institutions will be required to adopt a more scalable and intelligence-driven approach to AML checks.

Stay Ahead in AML Checks with AML Watcher

Businesses in 2026 face rising pressure from regulators to demonstrate the effectiveness of their controls, at a time when limited resources already feel strained by false positives. AML Watcher empowers institutions with automated and explainable AML checks, which not only minimize false positives but also create audit trails that satisfy regulatory demands. It helps financial institutions with:

- Ongoing Monitoring: continuous screening that ensures systems remain updated and CROs can detect proactively if any illegal activity occurs.

- Customized Risk Scoring: Precise and tailored risk scoring that reduces the rate of false positives and speeds up the investigation process.

- Cross-border Compliance: Smooth integration with international standards such as FATF, AMLA, and FinCEN for cross-border compliance.

- Irregular Pattern Detection: Expose hidden risks by checking the anomalous patterns in the client behaviour.

- All-in-one Dashboard: Gain a combination of integrated risk profiles, sanctions, watchlists, PEPs, ownership, and behavioural insights in one dashboard.

AML Watcher empowers your team to meet the regulatory demands of 2026 with fewer obstacles and less risk.

- No commitment needed

- Complete AML Database at your service

- Access our all-in-one dashboard

Tier-2 PSPs in ... must demonstrate automated monitoring, layered CDD, &...

See the Full Regulatory Expectation70–80% less manual work, 95% less fatigue, TruRisk Agent makes compliance effortless.

Experience Agentic AMLMove Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries