AML Data Freshness That Protects Against Hidden Cost of Delayed Risk Intelligence

AML Compliance

February 19, 2026

At 9:00 AM, the Office of Foreign Assets Control issues a new sanctions designation.

At 1:00 PM, a cross-border transaction is carried out.

At midnight, the internal watchlist refresh occurs.

None of the screening engines ever failed, nor was an alert ever overlooked. The system worked as per the setup, yet money to a sanctioned entity was processed across the border.

The weakness was data freshness

Sanctions compliance works under rigid time-frames. When the watchlist update lags behind regulatory publications, there is a silent exposure window to the financial institutions. Compliance risk is not the only risk that the window generates. It introduces long-term revenue drag, financial risk, and long-term Revenue drag.

Here, data freshness is no longer a technical issue, but it becomes a board-level issue.

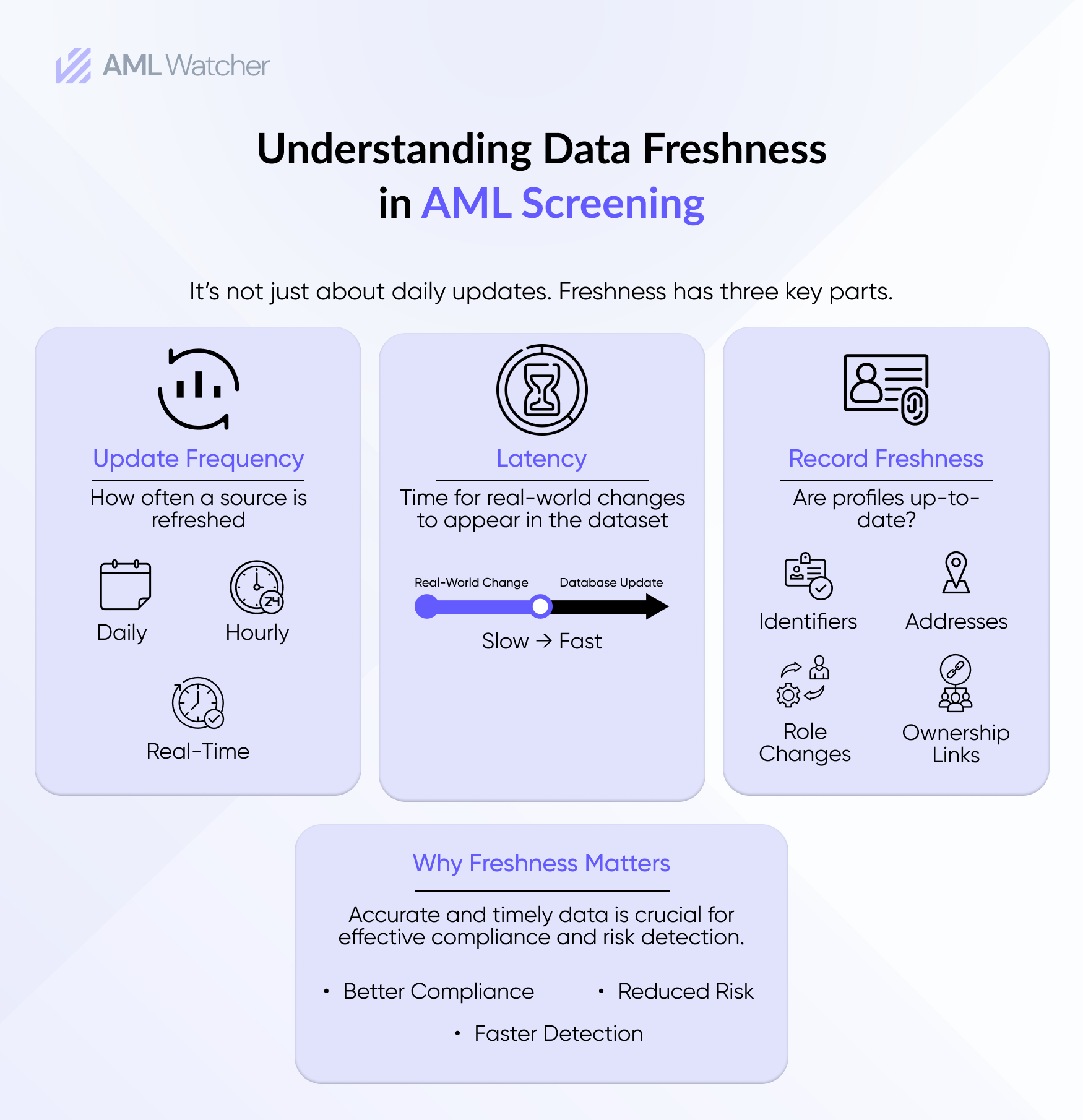

What is Data Freshness?

AML data freshness refers to the timeliness and synchronization of all external risk intelligence used for screening and monitoring.

This includes:

- Sanctions lists from authorities such as OFAC and HM Treasury

- PEP databases reflecting changes in political exposure

- Adverse media feeds identifying emerging reputational risks

- Regulatory enforcement notices and criminal investigations

Though sanctions are usually given most of the focus, PEP and negative media updates are equally dynamic. Political appointments are altered in the middle of the night, new inquires are brought to the centre stage, and court decisions modify risk profiles. AML Data Freshness is a time measure between the external publication and the internal screening synchronization. That timing gap defines institutional exposure.

Why is AML Data Freshness Now a Control Requirement?

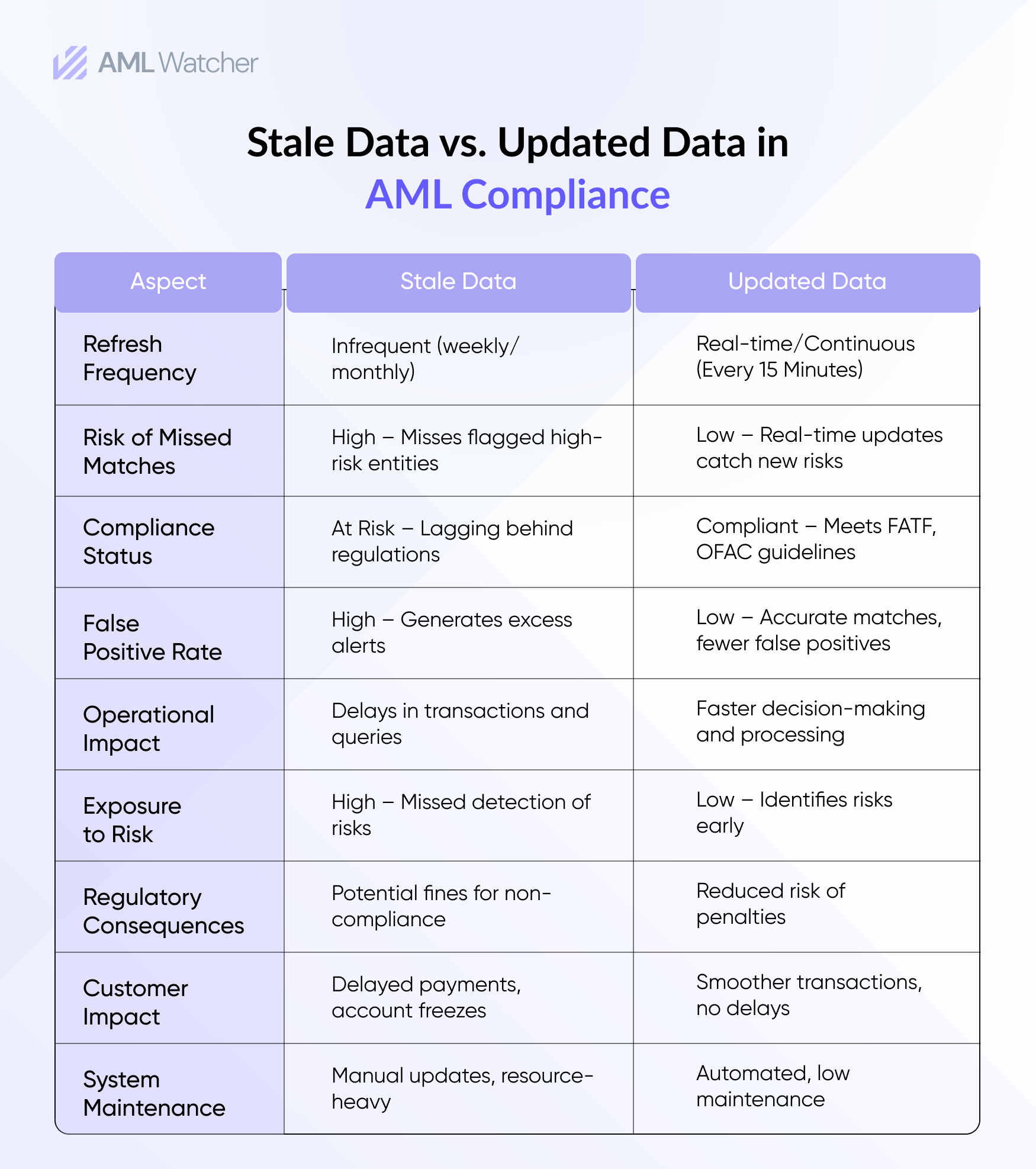

A back-office check that was done every year has been substituted by an always-on requirement. FinTechs and neobanks give approvals to accounts in a brief period. The payment service providers tend to be operating on near real-time expectations, leaving little room for delayed screening. International banks serve customers of various jurisdictions and regimes.

In such settings, stale screening data produces two issues simultaneously. It heightens the risk of missing fast-moving changes in risk, and it increases friction when controls need to retroactively rectify the situation. This is why teams focus on faster ingestion of list changes, particularly where volumes make it difficult to catch-up manually.

The regulators created an expectation for speed. FATF anticipates that targeted financial sanctions should be undertaken “without delay”. When applied to UN designation regimes, it typically denotes idealistically, within a few hours. This puts AML data freshness as not only a system preference but also a compliance requirement in practice

Why Faster Updates Matter for PEP and Watchlist Screening?

Sanctions are only one part of the story. PEP exposure shifts with elections, cabinet reshuffles, senior appointments, state-owned enterprise leadership changes, and new close-associate links. A profile can be “present” in a dataset but still be stale if it lacks updated role, seniority, or contextual links that change risk classification.

That is why many institutions push for an AML system with real-time PEP updates, especially where rapid onboarding and instant payments leave little room for delayed escalation. FinTech firms and neobanks, in particular, face a tight cause-and-effect loop. High operational speed increases the impact of any data delay, which can lead to unrecognised risks and process deviations.

Freshness helps only when updates arrive with stronger identifiers, clearer context, and de-duplicated records that improve match quality rather than increasing noise.

Why AML Data Freshness is Also a Revenue Issue

1. Incorrect Risk Ratings and Mispriced Risk

In case a customer turns to PEP and internal records are not updated with this information, there will be no enhanced due diligence.

This results in:

- Underestimated risk exposure

- Low-quality transaction surveillance

- Delayed escalation

In case of wrong risk classification, the compliance systems are based on false premises.

Incorrect risk pricing ultimately results in monetary and reputational costs.

2. Correspondent Banking Risk and Market Access Risk.

Global institutions rely on correspondent banking relationships for trade finance and cross-border transactions. A sanctions screening lapse may lead to heightened questioning by the correspondent banks. In case of increased risks, relationships can be re-examined or terminated.

Loss of correspondent access impacts:

- International payment outflows

- Dollar clearing capabilities

- Trade finance revenue

The commercial impacts are usually greater than the original enforcement penalty. Perceived compliance reliability is a key element to market access. That confidence is usually undermined by weak data freshness.

3. Operation interruption and Margin Erosion.

Reactive remediation is often caused by delayed watchlist updates.

Upon bulk updates that are made after a period of delay, institutions might have to:

- Re-screen a high number of customers

- Conduct transaction lookbacks

- Explore the historical exposures

Such a reactive cycle increases the workload unpredictably. Analysts are not monitoring the regular activities but resorting to large-scale reviews. Overtime costs rise. Backlogs accumulate in other compliance areas.

Erosion of income becomes slow due to increased operational costs and decreased onboarding cycles.

On the contrary, timely data freshness stabilizes the workload and avoids expensive retrospective measures.

How can Businesses Verify their AML Data is Current?

Data freshness becomes defensible when it is measured.

A practical beginning point is the list update latency, which is the time elapsed between the publication of a change by a regulator and the way it actually occurs in production screening.

Latency-style KPIs are comprehensible to the boards and auditors as they transform freshness into a quantifiable control performance.

The second control is the coverage drift that is the percentage of customers whose last screening date is older than internal policy limits in the risk tier.

The third is the back-testing, which involves re-screening samples of previously cleared customers using the more recent data to gauge what would have been missed at the time. Back-testing is no substitute for live updates, but an effective governance tool for tuning and evidence.

A combination of these controls gives a clear image of whether the program is fresh enough regarding the firm’s product, jurisdictions, and customer base..

Enhance AML Data Freshness with AML Watcher

Financial institutions are continually exposed to changes in sanctions regimes, adverse media development, and political exposure data. Delayed synchronization and manual updates compromise the screening integrity and subject firms to unnecessary financial and regulatory implications.

AML Watcher supports institutions with regularly updated global sanctions,PEP, and adverse media datasets, backed by automated ingestion and audit-ready synchronization controls. This will enhance AML Data Freshness in the screening settings and minimize the risk of intelligence latency.

To improve the AML Data Freshness and safeguard long-term revenue stability, organizations can request a demo to learn about how the AML Watcher assists in implementing real-time risk intelligence governance.

- No commitment needed

- Complete AML Database at your service

- Access our all-in-one dashboard

Tier-2 PSPs in ... must demonstrate automated monitoring, layered CDD, &...

See the Full Regulatory Expectation70–80% less manual work, 95% less fatigue, TruRisk Agent makes compliance effortless.

Experience Agentic AMLMove Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries