A Guide to FinCEN AML Risk Scoring Model for Investment Advisors

Risk Assessment & Management

December 19, 2025

- What are the AML/CFT Program and SAR Filing Requirements for RIAs & ERAs?

- What is AML Client Risk Scoring

- AML Risk Model for Registered Investment Advisers

- Four principles of an RIA AML risk model

- The AML risk model structure RIAs should adopt

- Why Ongoing Monitoring is Necessary

- Why Registered Investment Advisors (RIAs) Should Turn to Technology

- How AML Watcher Supports the AML Risk Model for RIAs

Investment Advisors serve a wide mix of clients. Some relationships involve high-net-worth individuals with offshore holdings, layered ownership, while others involve domestic clients, clear ownership with a documented source of funds. This leads to a critical question: which of these clients requires what level of due diligence that meets regulatory expectations?

AML client risk scoring provides a systematic way to answer that question. It helps advisory firms apply a risk-based approach, allocate resources where exposure is highest, and document decisions in a way that stands up to regulatory expectations.

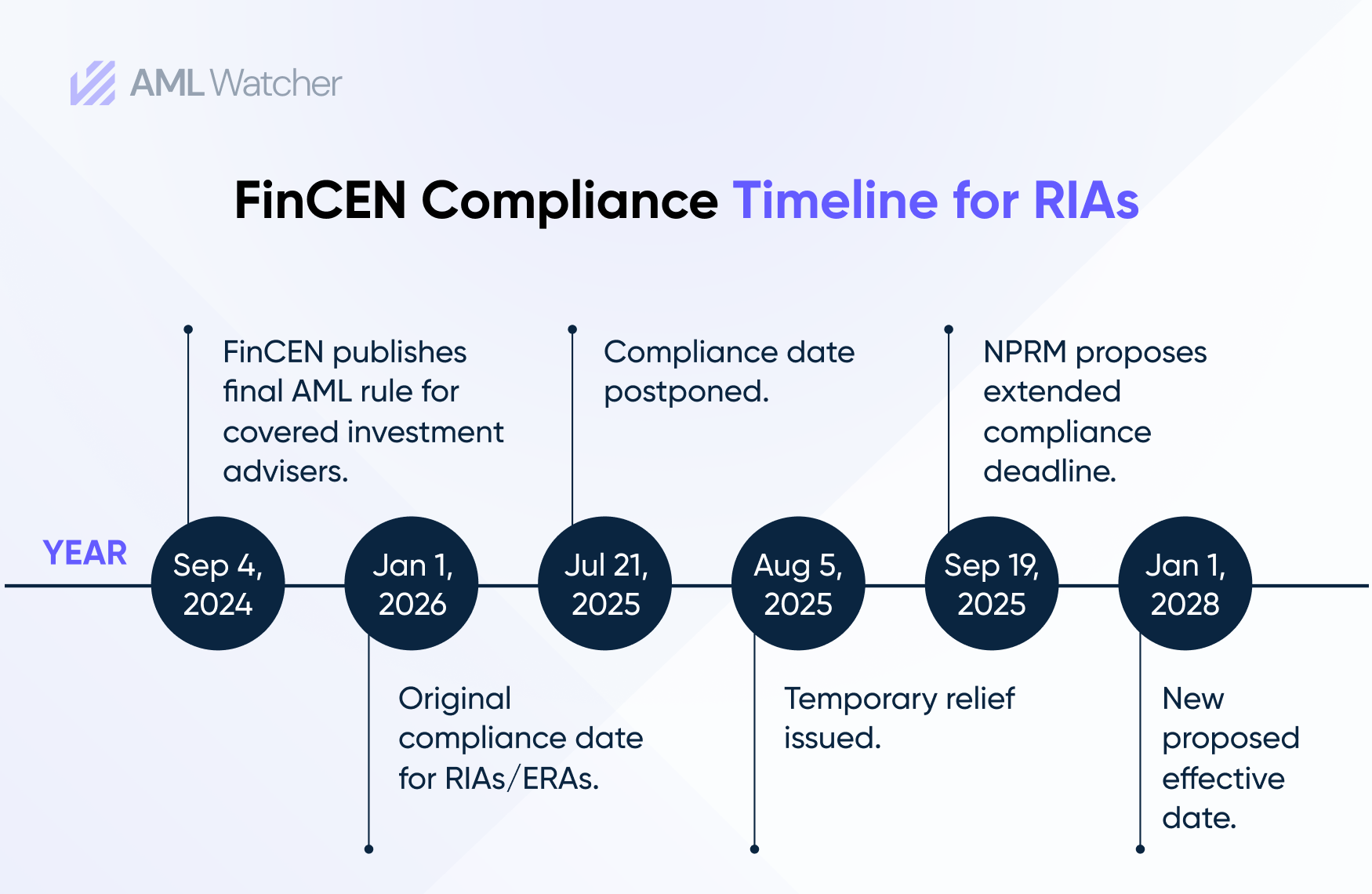

FinCEN’s Investment Adviser AML Rule was scheduled to be enforced on January 1, 2026; however, it has been delayed until January 1, 2028, via an exemptive relief order and ongoing rulemaking. Even with the delayed date, the direction of travel is clear. Risk-based customer due diligence and ongoing monitoring are now central expectations for the AML program of advisory businesses, not optional enhancements.

Let’s discover what AML client risk scoring actually is and how RIAs can apply it effectively within their compliance programs that reflect how advisory relationships actually work.

What are the AML/CFT Program and SAR Filing Requirements for RIAs & ERAs?

Under FinCEN’s final rule, registered investment advisers (RIAs), the individuals or firms that offer financial advice and manage investments for clients, and exempted registered advisors (ERAs) are considered financial institutions under the BSA in terms of AML compliance obligations. By January 1, 2026, these “Covered IAs” must implement a full risk‑based AML/CFT program.

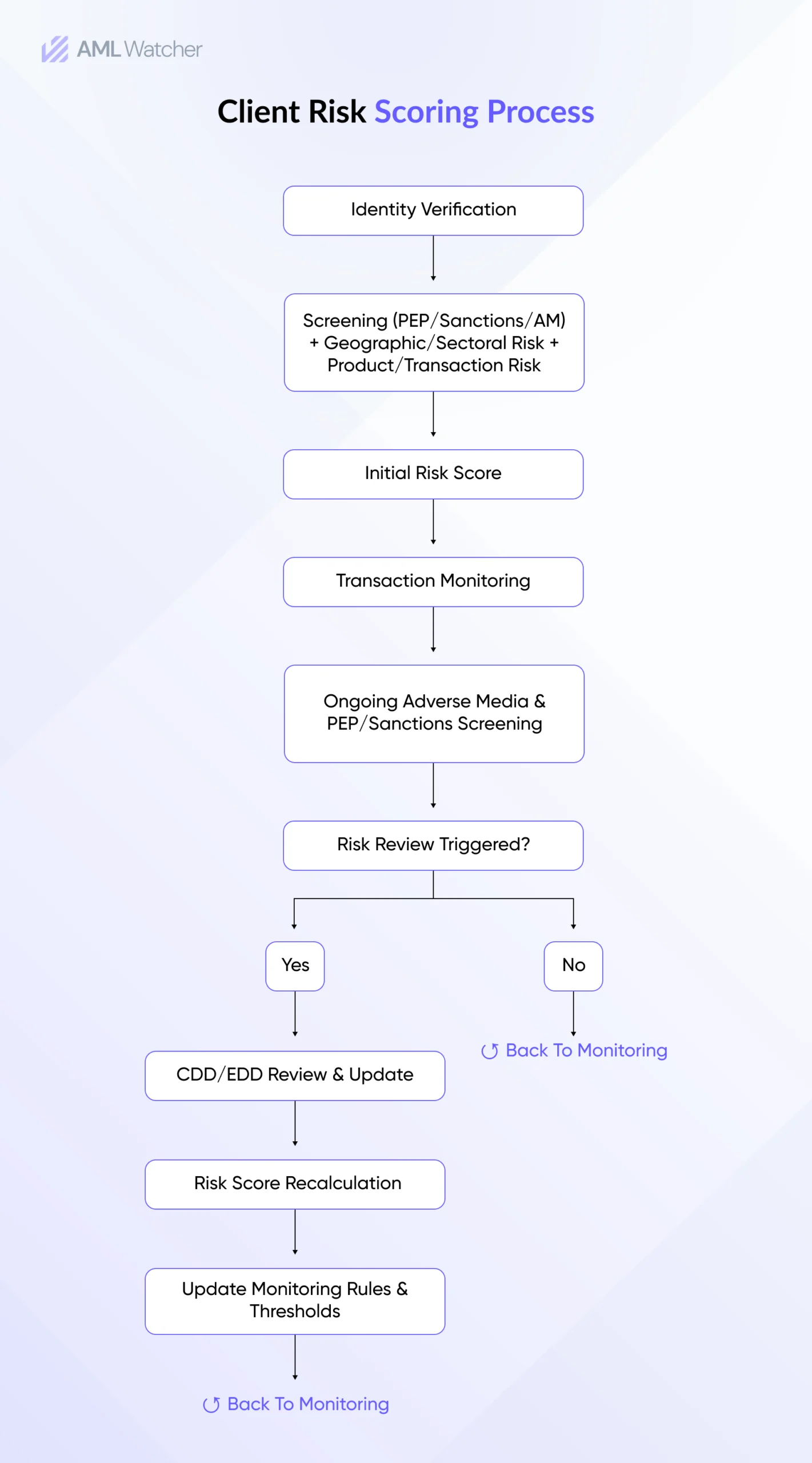

Key requirements in the FinCEN rule for RIAs revolve around having designated AML officers, clear written policies, and strong control measures. Organizations are required to offer regular training for staff, conduct independent testing, and maintain ongoing customer due diligence (CDD) with risk profiling. This actually means assigning a risk rating (such as Low, Medium, or High) to each client based on factors like their country, source of wealth, industry, and irregular behavioral patterns.

FinCEN specifically mandates risk‑based CDD procedures to “understand the nature and purpose of customer relationships” and to conduct “ongoing monitoring to identify and report suspicious transactions”. RIAs are required to:

- Implement a risk-based approach

- File SARs with FinCEN

- Recordkeeping, such as that relating to the transmittal of funds.

- RIAs must do more than basic reporting and have to follow additional regulatory standards.

Regulators have emphasized that RIAs often handle complex structures and international investors, making them targets for illicit finance. Even without an immediate compliance deadline, risk‑focused due diligence is already expected as a best practice.

For this, a robust risk‑scoring framework is no longer optional for RIAs. It is central to meeting the new rule and defending the firm against enforcement.

What is AML Client Risk Scoring

AML client risk scoring is the process of evaluating the client’s potential money laundering or financial crime risk. It assigns a risk score, i.e, high, medium, or low, to clients depending on some defined factors. This helps financial institutions perform appropriate due diligence, reduce false alerts, focus on genuine threats, and streamline the AML program.

AML Risk Model for Registered Investment Advisers

Why RIAs need a tailored AML risk model

Investment advisers operate very differently from banks and broker-dealers. This is because RIAs relationships with their clients are long-term, transactions are episodic, asset flows are often indirect, and ownership structures are frequently layered through funds, trusts, and offshore vehicles.

Therefore, a risk model borrowed from retail banking or payments firms fails to capture where true money laundering and terrorist financing risks emerge in the advisory context. A defensible AML program for RIAs must reflect how advisory services are delivered, how assets enter and exit the ecosystem, and how control is exercised over client relationships.

FinCEN’s rule reinforces a risk-based approach, not a checklist. Hence, the risk model becomes the foundation that supports every other AML obligation. This not only meets FinCEN’s expectations but also speeds up onboarding and reduces false alarms.

Four principles of an RIA AML risk model

AML risk model that meets regulatory requirements should be based on following four principles:

- Client-centric, not transaction-centric

Risk is primarily driven by who the client is, who controls the assets, and why the advisory relationship exists. - Inherent risk separated from residual risk

Regulators expect firms to distinguish raw exposure from risk after controls are applied. - Event-driven and lifecycle-based

Risk ratings must evolve as facts change, not only during periodic reviews. - Explainable and auditable

Every score, tier, and escalation must be traceable to documented logic.

The AML risk model structure RIAs should adopt

1. Inherent client risk assessment

Inherent risk is the risk RIAs are exposed to before any mitigation or controls are applied. Some industries and clientele types pose higher risks than others, therefore, controls should be proportionate to the level of risk a business faces. For RIAs, the following categories are essential.

a. Client type and legal structure risk

Some client profiles are inherently opaque, unclear or distance them from their underlying beneficial owner.

Examples of higher-risk profiles could include:

- Private funds and feeder funds

- Offshore entities and foreign trusts

- Special purpose vehicles (SPVs)

- Family offices with multi-jurisdictional footprints

- Nominee arrangements or layered holding companies

Whereas some examples of lower-risk profiles could be:

- U.S. individuals with transparent wealth profiles

- Domestic operating companies with simple ownership

This category establishes the starting point of the risk score. On a scale of 1 to 5, the lowest risk is represented by 1 whereas the highest by 5.

b. Beneficial ownership and control risk

In an investment advisory context who controls the funds matters more than ownership percentages. In this regard the inherent risk depends on the following points

- Complexity and depth of ownership chains

- Use of trustees, protectors, or managing members

- Presence of unidentified or unverifiable natural persons

- Reliance on third-party administrators for ownership information

Incomplete or delayed beneficial ownership data should materially increase inherent risk.

c. Geographic exposure risk

In risk assessment geographical linkages can seriously impact whether an RIA can deal with a client or not. RIAs must assess geography beyond just client residence. Key considerations in this regard could include:

- Jurisdictions of incorporation

- Source of wealth and source of funds locations

- Custodian and intermediary jurisdictions

- Countries subject to sanctions, FATF grey or black lists, or secrecy concerns

If more than one jurisdiction poses medium or high risks, in that case risk should be compounded not averaged.

d. Source of wealth (SoW) and source of funds (SoF) risk

Collection of SoF or SoW is a central AML obligation for RIAs. Determining where wealth was generated or originated from is as important as knowing the client itself. Higher risk indicators related to SoF/SoW include:

- Wealth derived from high-cash industries

- Significant liquidity events with limited documentation

- Wealth generated in jurisdictions with weak AML controls

- Complex asset liquidation paths prior to onboarding

Clear, well-documented wealth generation trails reduce risk, while ambiguity increases it.

e. Politically exposed person and influence risk

Politically exposed person (PEP) exposure remains a regulatory focus in AML compliance. While regulators now emphasize that simply being a PEP doesn’t mean the person is high risk, however, each client must be evaluated on a case-by-case basis. The factors that can determine risk in this regard include:

- Role and level of influence

- Proximity of associates and family members

- Jurisdictional corruption risk

- Time elapsed since holding public office

Domestic PEPs may present different risk profiles than foreign PEPs, but neither should be treated as inherently low risk and other factors must be considered when reaching a conclusion.

f. Reputation and adverse information risk

Negative media must be evaluated qualitatively, not mechanically. This means only existing in a news story isn’t an adverse media. The significance of the adverse media should be considered on the following factors:

- Credibility of sources

- Allegation severity and recency

- Financial crime, corruption, or sanctions relevance

- Patterns rather than isolated mentions

This category often acts as a risk multiplier rather than a standalone trigger.

2. Expected activity and relationship risk

RIAs do not have one off transactional relationships with their clients, but assessing the expected activity still matters a lot from risk context. RIAs should assess anticipated asset inflows and outflows, how often capital will be moved, and involvement of any third-party payments, custodial arrangements or intermediaries.

Assessing these points at boarding is critical, because it helps RIAs in determining what would be the normal client behaviour and when it should be considered a meaningful deviation.

3. Control effectiveness assessment

Once the inherent risk is identified, controls come into play. Strength and appropriateness of controls determine whether inherent risk is mitigated or amplified. Typical control factors include:

- Depth of customer due diligence performed

- Quality of identity and ownership verification

- Screening coverage and refresh frequency

- Ongoing monitoring mechanisms

- Review frequency that meets the risk tier

Even if the inherent risk in a business relationship is moderate, weak, or manual controls can result in higher residual risks. Therefore, controls must be tailor-made for each risk tier.

4. Residual risk calculation and tiering

Eliminating all the risk isn’t practically possible; however, it should be mitigated with suitable controls, precautions, and strategies. The leftover risk after it is mitigated with controls is known as residual risk. RIAs should document what’s the acceptable level of residual risk for their business, which is also known as risk appetite for that business.

A practical RIA model should translate scores into clear tiers such as low, medium, and high, without making it numerically complex. It should also have a clearly documented policy for specific actions that must be taken for clients falling in each of the defined categories.

Residual risk is also critical to determine the following:

- How often review will be conduct

- Requirements for Enhanced due diligence

- Escalation thresholds

- Senior management involvement

Why Ongoing Monitoring is Necessary

Regulators demand that the risk of a client should change when the underlying factor that determined the risk in the first place changes. Ongoing monitoring is required to keep risk ratings relevant and to ensure controls remain proportionate. For example, risk ratings should be updated when:

- PEP status changes

- New adverse media emerges

- Ownership structures change

- Changes to sanctions lists occur

- Source of wealth narratives evolve

- Activity deviates from expectations

- Periodic reviews fail to refresh the required data

This is where many RIA programs fail by relying solely on calendar-based reviews. This also demands a continuous AML screening mechanism that scans for sanctions, PEPs, or adverse media updates.

Why Registered Investment Advisors (RIAs) Should Turn to Technology

Building and maintaining a risk scoring program is operationally difficult, especially for smaller advisers. Manual models often lead to inconsistent results, delayed updates, and gaps in documentation.

Automated AML solutions can streamline risk scoring and CDD by ingesting client data, assigning points, and adjusting scores without manual effort. In fact, one analysis notes that trying to do this manually “in-house” often takes months and leaves firms unable to keep up with changing risks. A purpose‑built platform can incorporate global watchlists, adverse media, transaction feeds, and built-in risk logic in one single workflow. Therefore, compliance teams can spend less time on repetitive checks and more time on true risk review.

Modern platforms also support the shift toward continuous monitoring approaches often referred to as perpetual KYC. When a system can update risk profiles based on new screening outcomes or meaningful activity change, ongoing CDD becomes more achievable and less dependent on manual cycles.

Whether using a commercial AML system or an advanced analytics tool, the key is that technology must support adaptive, data‑driven scoring. For example, an AI‑powered system might automatically recalibrate a client’s risk profile as new transactions occur or as new PEP/sanctions hits appear. This also meets regulatory push for ongoing CDD, also known as “perpetual KYC”. In short, a modern compliance solution helps you implement the FinCEN program: it lets you customize risk factors (“Build Custom Risk Scoring Models”), assign dynamic weightings, and embed those risk levels into screening and monitoring. This ultimately means fewer missed risks and lower false‑positive rates.

How AML Watcher Supports the AML Risk Model for RIAs

Risk scoring frameworks usually struggle when it comes to execution due to fragmented data, manual reviews and inconsistency in scoring logic across different teams.

AML Watcher helps RIAs operationalize risk-based AML programs with structured scoring, event-driven updates, and audit-ready logic. Firms evaluating their FinCEN readiness can request a demo to see how this framework applies in practice.

- No commitment needed

- Complete AML Database at your service

- Access our all-in-one dashboard

Tier-2 PSPs in ... must demonstrate automated monitoring, layered CDD, &...

See the Full Regulatory Expectation70–80% less manual work, 95% less fatigue, TruRisk Agent makes compliance effortless.

Experience Agentic AMLMove Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries