Best Practices For Corporate Screening in AML

Anti Money Laundering

December 17, 2024

On November 29, 2024, Swiss private bank Lombard Odier and a former employee were charged with aggravated money laundering for allegedly helping “The Office,” to hide illegal funds between 2005 and 2012.

The Swiss authorities claim the bank and its employees played a key role in concealing the criminal proceeds of The Office, a criminal group led by Gulnara Karimova that was involved in money laundering.

How does a criminal group utilize bank services, why did this happen, how much does the group launder money through this bank, and why the bank’s higher authorities didn’t notice it earlier?

These questions may remain a mystery but one thing this case highlights is the importance of corporate screening in AML processes.

Why financial institutions and other businesses should conduct corporate screening regularly and thoroughly to prevent such money laundering risks associated with either internal stakeholders or external parties.

How to preserve the integrity of the global financial spaces. Why not give a complete read to this article to get detailed insights about corporate screening?

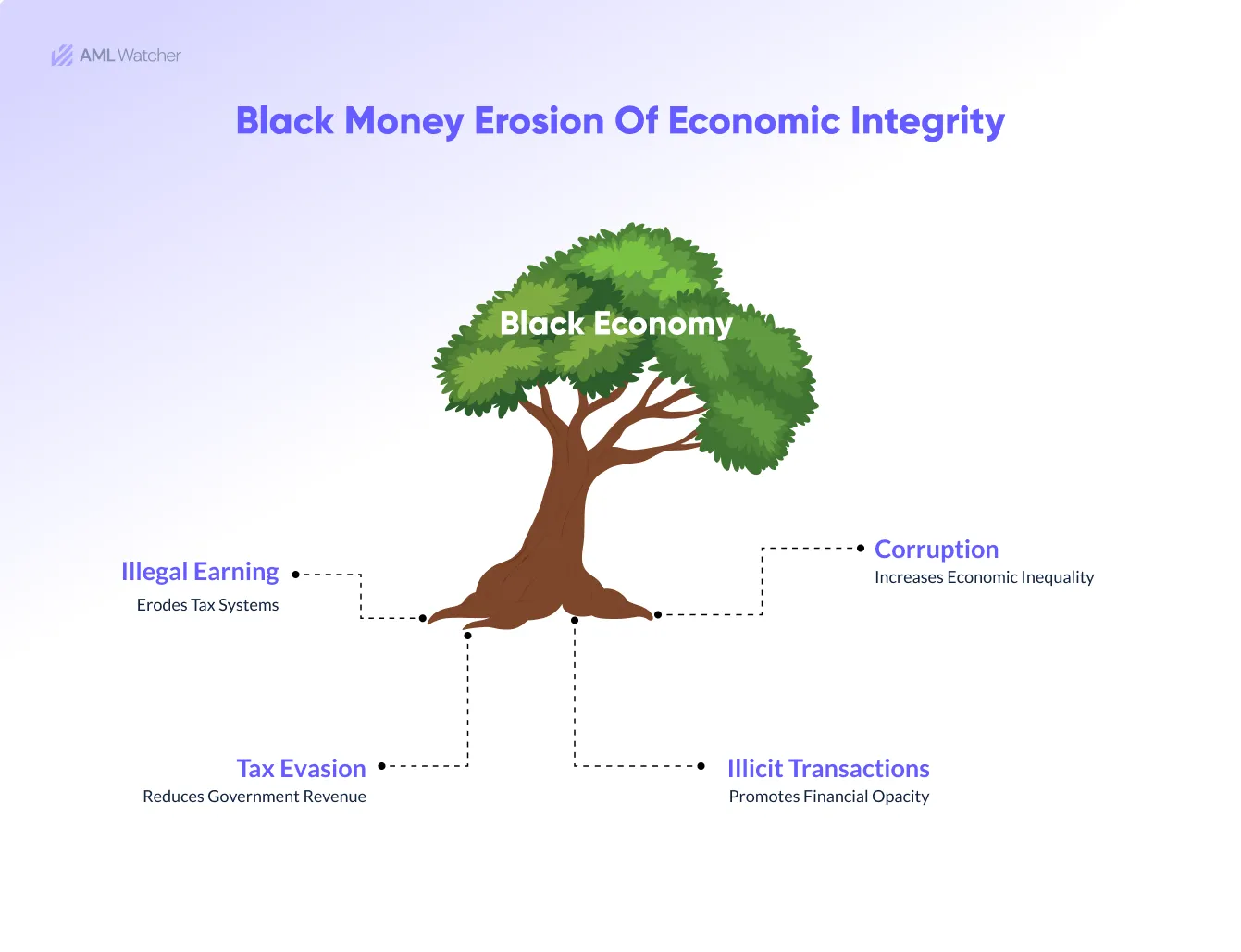

What is Corporate Screening?

Evaluating and verifying the authenticity of corporate entities and businesses to ensure they are not linked with financial crimes such as “money laundering, fraud, and terrorist financing” is known as Corporate Screening in AML compliance.

Financial institutions must follow this AML obligation as it is part of their Know Your Customer (KYC) and Anti-Money Laundering (AML) procedures and policies while starting any business relationship with another company/ business.

The screening covers almost every entity linked with business, such as “employees, partners, and ultimate beneficial owners (UBOs).” Corporate screening protects financial institutions (FI) and other DNFBPs like “real estate, legal services, investment, and payment providers” from various financial, economic, and reputational risks.

Criminals use evolved techniques for their illegal purposes. For example, some launder the money and hide the source of their proceeds of crimes. Many are involved in fraud by faking businesses, and some invest funds in their terrorist activities.

How Long Does Corporate Screening Take?

The duration of corporation screening varies from business to business as it depends on several factors, such as “the complexity of the business structure, the jurisdiction, and the depth of checks required.” It may take a “few hours to several days for normal clients.”

Dealing with high-risk entities requires “complex verification and enhanced due diligence, along with detailed AML screening measures,” which may take longer.

Data-driven AML solutions speed up the process and minimize the risks and delays while ensuring better performance.

What are Global AML legislations For Corporate Screening?

Key AML laws and regulations, including corporate screening requirements, are mandated to be implemented in various countries to combat financial crimes such as money laundering, fraud, and terrorist financing.

The most prominent AML obligations are;

U.S. Corporate Screening Regulations & Legislations

In 1970, the Bank Secrecy Act (BSA) was introduced as an AML law in the US to stop drug traffickers and criminal groups from engaging in money laundering and promote financial security.

The law proposed KYC/AML requirements for organizations, such as “Enhanced Due Diligence (EDD) and Suspicious activity reports (SARs),” for individuals who pose higher risks and who evaluate beneficial owners of businesses.

The Role of OFAC

Additionally, with the passage of time, OFAC, as a significant part of the “U.S. Department of the Treasury,” enforced sanctioned lists against entities involved in illegal activities such as drug trafficking, money laundering, and other crimes.

Businesses must screen their company clients against “OFAC sanctions lists, the Sectoral Sanctions Identifications List (SSI), and other reluctant lists” in corporate sanctions screening to confirm that they don’t deal with entities linked to illegal activities.

The PATRIOT Act 2001

“Providing Appropriate Tools Required to Intercept and Obstruct Terrorism (PATRIOT Act) of 2001” was established in the US by expanding BSA and requiring businesses to check clients’ identities by introducing “Customer Identification Programs (CIP)” and keeping records of all information.

This Act protects businesses from financial crimes by improving their efforts for national security.

FinCEN further added AML regulation in 2016 in their current CDD policies by adding the point of verifying the identity of “ultimate beneficial owners (UBO)” in CDD requirements.

UK Corporate Screening Regulations & Legislations

Challenges of financial crimes, such as “money laundering, fraud, and illegal selling or purchasing of properties” in the UK, have been observed for ages.

AML Regulations in the UK have evolved to fight these challenges.

Proceeds of Crime Act 2002 (POCA)

“Proceeds of the Crime Act 2002” is imposed in the UK to combat money laundering and illegal transfer of gains obtained from money laundering.

The act aims to seize the proceeds of crimes and mandate law enforcement agencies to recover the assets to prevent the growth of financial crimes.

It sets penalties for making money laundering a regular business activity, such as transferring assets or illegal property, hiding the source of funds, and using illegal gains to fund further illicit activities.

Corporate screening ensures the detection of the association of business with any proceeds of crimes.

The Terrorism Act 2000

It was implemented in the UK to prevent terrorist-related activities and provide a legal framework to make “investigation, prosecution, and prevention of terrorist activities” easy and make financing of funds difficult.

It Mandates corporate screening by defining terrorism and legally making terrorism or financing of terrorism an offense.

According to this, seizing the assets of suspected terrorist entities is mandatory, as is taking strict actions against them and reporting suspicious activities related to terrorist financing.

Terrorist Asset Freezing Act 2010

“Terrorist Asset Freezing Act 2010” requires countries to incorporate corporate screening to prevent dealings with businesses that are linked with terrorist financing or the “use or transfer of frozen assets of entities that are lined with terrorism.”

EU Corporate Screening & Regulations & Legislations

Corporate screening measures in the European Union (EU) have been implemented through AML directives, which are given below :

Money Laundering Regulations 2003

Money laundering regulations were introduced to comply with AML obligations of the EU, followed by the “First Money Laundering Directive (Directive 91/308/EEC) of European Union,” which was later modified to “Second Money Laundering Directive.”

These regulations were proposed in the parliament in 2003 and implemented officially in 2004, and these laws were modified in 2007, 2012, and 2017 to establish robust AML compliance.

Money Laundering Regulation 2003 implements the “3rd Money Laundering Directive” of the EU. Businesses are mandated to apply CDD measures to verify customers’ identity and the associated risks.

A risk-based approach is implemented to evaluate the risks of financial crimes, maintain a record of mandatory information related to entities, such as records of transactions and identity, and report unusual or suspicious transactions to relative authorities.

Fourth Anti-Money Laundering Directive (4AMLD)

“The Money Laundering, Terrorist Financing and Transfer of Funds Regulations 2017” was implemented on 26 June 2017 to implement the “4th EU Anti-Money Laundering Directive (AMLD4)” in United Kingdom Law Enforcement.

Businesses must conduct corporate screening background checks by verifying the company’s identities and ultimate beneficial owners (UBO) and understanding the reason behind the business relationship.

Countries must apply Enhanced due diligence (EDD) and Ongoing monitoring to detect risks in transactions and for high-risk individual countries and entities.

Collaborate with other law enforcement authorities to combat financial crimes and maintain financial security across the globe.

Fifth Anti-Money Laundering Directive (5AMLD)

5AMLD is an amendment to already existing AML legislation, and companies, by following this law in corporate screening, can enhance transparency in the financial system and mitigate the risks associated with “virtual currencies and prepaid cards.”

As the directive mandates on virtual currency, “Exchanges and wallet providers” must follow the AML obligations. Its AML obligation for financial institutions and trusts is that ownership registers are publicly accessible and that prepaid card-related AML obligations must be followed.

In addition, a risk-based approach for high customers, such as PEPs and collaboration with related authorities to combat money laundering, must be established.

Sixth Anti-Money Laundering Directive (6AMLD)

6AMLD borders the definition of predicate offence, such as making money laundering “an offense for legal entities” and imposing stricter penalties for individuals or entities who are linked with financial crimes.

It enhances collaboration across borders and between relative authorities like Financial Intelligence Units (FIU). It mandated companies to conduct EDD and STR measures to combat money laundering.

Who Should Conduct Corporate Screening?

Businesses use AML solutions for corporate screening across industries to verify that their clients comply with AML legislation and ensure AML compliance. It is used in financial institutions and industries dealing with large amounts of transactions or data, such as:

Financial Institutions and banks

Financial institutions such as “banks, investment firms, and insurance companies” imply CDD checks to comply with AML regulations as part of their AML/KYC obligations. Corporate screening allows them to identify the entities with higher risks by implying AML screening through robust AML solutions.

These institutions evaluate the legitimacy of the companies they will start business with or are already dealing with. Legitimacy is checked in different phases, whether “opening accounts, taking out loans or making investments.”

Invest firms, banks, and insurance companies asses higher-risk entities not to get involved with entities that are linked with illegal activities.

Corporate Service Providers

Providers of different services, such as “company formation, legal and compliance consulting, and accounting,” must benefit from corporate screening services.

They must verify the companies they engage with or advise to prevent association with companies linked to illegal activities and avoid assisting and promoting financial crimes like “money laundering or fraud.”

Law Firms and Legal Advisors

Law firms must verify the credibility of the companies they “serve or collaborate with” by corporate screening. Law firms that are exceptionally complicated in “ mergers, acquisitions, or corporate transactions”

Corporate screening aims to detect whether the business they are dealing with involves illegal activities such as “money laundering or terrorist financing.”

Real Estate Companies

Real Estate agencies deal with large transactions while selling or purchasing properties; corporate screening is a must AML obligation to ensure “buyers or sellers entity ” are not involved in illicit financial activities and their transactions are legitimate.

Audits and Compliance Firms

External AML audits verify that the companies under their audits comply with AML regulations and AML laws by conducting corporate screening. Another crucial factor in corporate screening is hiring Compliance firms, which companies usually use to ensure regulatory compliance.

Trade and Customs Businesses

Corporate screening in businesses engaged in international trading must establish corporate screening to ensure companies they are transactions with or involving are not on sanctioned lists or FATF’s grey lists.

Thus, it prevents any potential breach of AML laws related to import and export.

Payment Service Providers (PSPs) and Money Transfer Operators (MTOs)

Payment service providers such as “remittances and money transfer operators (MTOs)” must screen their “corporate clients” to comply with AML legislation and regulations. It ensures that transactions are not linked to illicit activities and will not facilitate any illegal activities.

How AML Watcher Simplify Corporate Screening and AML Compliance?

AML Watcher offers best-in-class corporate screening by leveraging advanced technology and comprehensive data to support institutions in conducting effective due diligence and compliance. Here’s how it stands out:

Global Watchlist & Sanction Screening

AML Watcher provides access to over 1,300 global and regional watchlists and 200+ sanction regimes allowing businesses to check corporate entities and their stakeholders (directors, shareholders, etc.) against sanctions lists, enforcement lists, and high-risk individual databases.

Use Case: If a company or its key executives are flagged on a sanctions list (e.g., OFAC, EU, UN), AML Watcher instantly identifies this, helping institutions avoid engaging with risky or blacklisted entities.

Adverse Media Screening

The tool uses Natural Language Processing (NLP) and machine learning to scan news, blogs, and other media sources for mentions of a company or its stakeholders. It categorizes information as positive, neutral, or negative.

Use Case: Adverse media checks could uncover past allegations of fraud or environmental violations against a corporation, alerting institutions to reputational risks before establishing partnerships.

Politically Exposed Persons (PEP) Screening

AML Watcher detects whether any of the company’s key figures (e.g., directors or significant shareholders) are politically exposed persons (PEPs) or have connections to such individuals.

Use Case: A company owned by a family member of a senior politician might pose a corruption or bribery risk. The platform enables institutions to flag these connections and take necessary precautions, such as enhanced due diligence.

International Leaks Database

This feature provides insights into offshore entities and potential money laundering schemes by referencing leaks like the Panama Papers or Paradise Papers.

Use Case: AML Watcher could reveal that a corporate client is linked to an offshore shell company, raising red flags about the legitimacy of their operations and prompting further investigation.

Custom Risk Scoring and Batch Search

Institutions can define custom risk thresholds (e.g., high-risk industries, countries, or individuals) and screen large volumes of corporate entities at once. Our system allows to score companies based on their risk profile, prioritizing those that require enhanced due diligence.

Use Case: A bank onboarding multiple corporate clients can use batch screening to identify high-risk companies based on their operations in sanctioned countries or ownership structures tied to high-risk individuals.

Ongoing Corporate Monitoring

The platform provides continuous monitoring of clients and associated entities, ensuring that any changes in risk status, such as new sanctions or adverse media reports, are promptly detected. This proactive approach helps institutions maintain up-to-date compliance.

Use Case: If a corporate client becomes subject to new regulatory sanctions, AML Watcher will immediately alert the institution, enabling swift action to mitigate potential compliance breaches.

Whitelisting & Blacklisting

The platform enables institutions to maintain and manage customized whitelists and blacklists of corporate entities or individuals based on prior interactions, risk evaluations, or regulatory compliance needs.

Use Case: A company flagged for previous suspicious activities can be blacklisted to prevent future engagement, while trusted long-term partners can be whitelisted to streamline transactions and minimize unnecessary screening.

- No commitment needed

- Complete AML Database at your service

- Access our all-in-one dashboard

Tier-2 PSPs in ... must demonstrate automated monitoring, layered CDD, &...

See the Full Regulatory Expectation70–80% less manual work, 95% less fatigue, TruRisk Agent makes compliance effortless.

Experience Agentic AMLMove Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries