FinCEN Beneficial Ownership Rule: CTA Compliance & Screening

AML Compliance

March 27, 2026

- What the FinCEN BOI Rule Actually Requires

- The March 2025 Pivot: What Changed and Who Is Still Covered

- BOI Deadline and Filing Requirements for Foreign Entities

- CTA Compliance Requirements: Financial Institutions Cannot Ignore

- How Beneficial Ownership Data Reshapes Screening Operations

- How AML Watcher Supports Beneficial Ownership Screening

Compliance teams spent years gearing up for the Corporate Transparency Act (CTA), anticipating comprehensive reporting of beneficial ownership across U.S. entities. However, in March 2025, FinCEN changed that outlook significantly.

The agency relieved any entity that was set up in the United States from having to report information of beneficial ownership (BOI) and instead turned to non-U.S. companies. This change will have impacts on the Chief Compliance Officer and AML analysts regarding both the way financial institutions screen their legal entity customers as well as their customer due diligence (CDD). It will also influence their handling of the risks of ultimate beneficial ownership (UBO).

What the FinCEN BOI Rule Actually Requires

The CTA was drafted as part of the Anti-Money Laundering Act of 2020, which attempted to fix the shell company loophole. The dense corporate form through LLCs, nominee directors, cross-border holding companies, and the like has long been utilized by criminal organizations to launder money via the U.S financial system without disclosing who the real owner is.

The beneficial owners should also be disclosed in the FinCEN BOI rule in the reporting organization. The beneficial owners are those who directly or indirectly own more than 25 percent of the company or have controlling power over the company. The beneficial ownership information that must be disclosed is the full legal name of each owner, birthday date, residential or business address, and a government-issued identification document such as a passport or driver’s license. This information is reported electronically using the BOI E-Filing system of FinCEN at no charge.

There is no difference in the definition of beneficial owner under the 2025 interim final rule. What has been altered is the parties that are required to report. These positive ownership reporting requirements are the basis of BOI filing requirements under the CTA system.

The March 2025 Pivot: What Changed and Who Is Still Covered

On March 26, 2025, FinCEN released an interim final rule that notably narrowed the range of beneficial ownership information (BOI) reporting obligations. The exemption has been granted to all institutions created in the United States, including those that were once considered to be domestic reporting companies. The rule modifies the definition of a reporting company. It now incorporates only businesses established under foreign law that have registered to conduct business in any state or tribal area in the U.S.

This change reduces regulatory reporting requirements, but increases the risk of concentration of foreign-owned companies in the U.S. This is exempted for beneficial owners who are U.S. persons. It is no longer necessary to disclose U.S persons as beneficial owners of foreign reporting companies and the information of U.S residents to any foreign reporting company in which they have an ownership interest.

Therefore, the foreign-formed entities requirement remains the same as long as they do business in the U.S. So, such companies are to make reports according to BOI requirements, and updated deadlines. FinCEN will complete the rule by further modification upon the conclusion of the 60-day public comment period. This should be checked by compliance teams that have cross-border client bases.

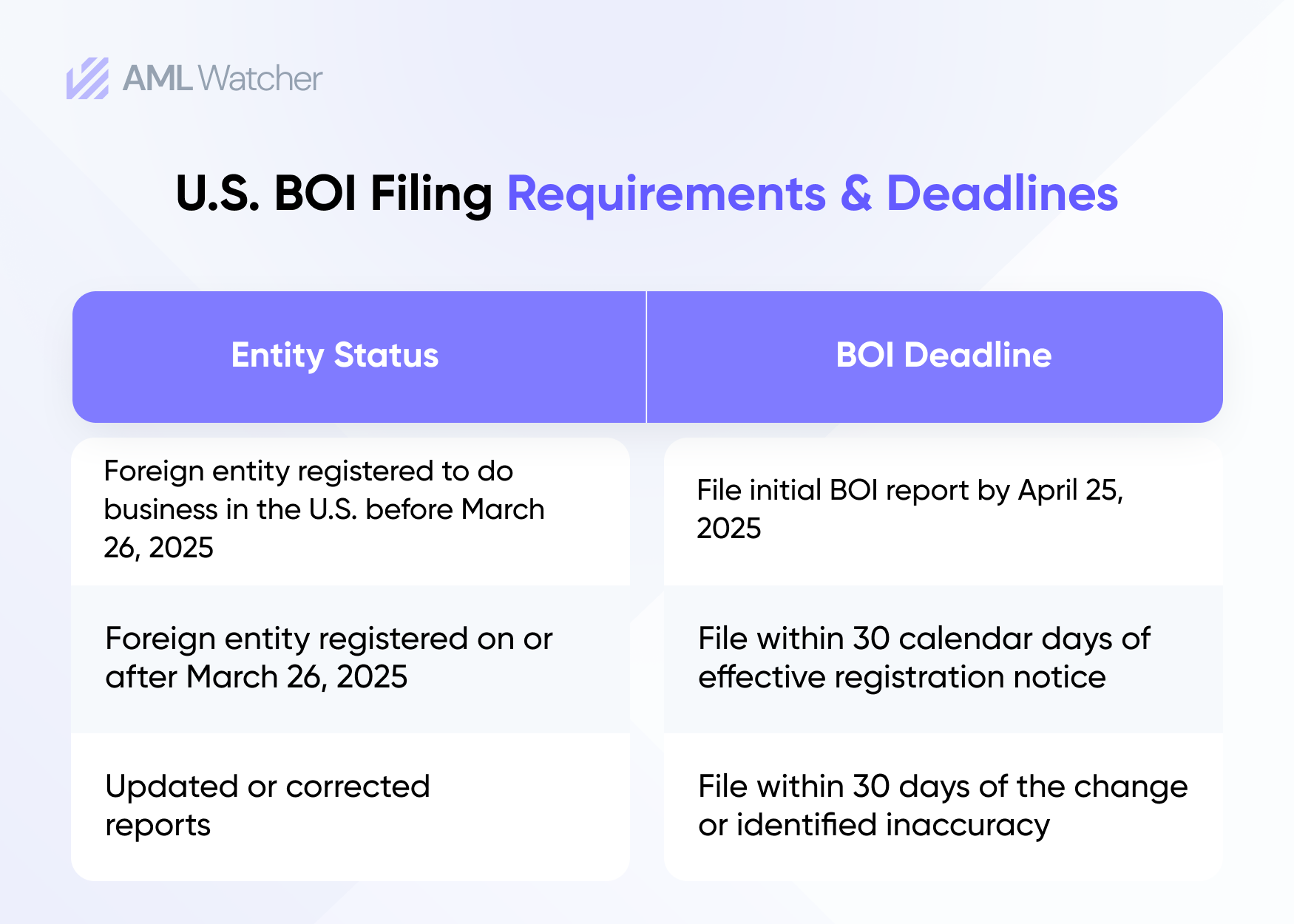

BOI Deadline and Filing Requirements for Foreign Entities

The interim final rule provided two filing tracks depending on the date of registration.

The deadline of the BOI for most current foreign reporting companies was April 25, 2025, 30 days after the publication date of the interim final rule. The 30 days within which new registrants can act commence on the date of registration effectiveness. No fee is required, and it is filed via the secure online portal of FinCEN.

The foreign reporting companies continue to face penalties in cases of willful non-compliance: $500 per day of continued violation, criminal penalties of $10,000 or higher, and a maximum jail term of 2 years.

CTA Compliance Requirements: Financial Institutions Cannot Ignore

The change in scope does not lessen the compliance requirements for financial institutions, it just simply shifts them. The FinCEN Customer Due Diligence (CDD) rule requires financial institutions to identify and verify the beneficial owners of customers that are legal entities when they open accounts. This rule is part of the Bank Secrecy Act (BSA) and was established before the Corporate Transparency Act (CTA). That requirement has not changed. Therefore, financial institutions need to continue to rely on internal CDD frameworks, no matter if the external BOI data becomes available.

What the CTA and its access rule add is a new data resource. Financial institutions are among the six categories of authorized recipients permitted to access the FinCEN BOI registry. Banks and other covered institutions may request BOI data from FinCEN for CDD, sanctions screening, enhanced due diligence (EDD), and suspicious activity report (SAR) investigations, provided the relevant reporting company has consented to that disclosure.

For compliance teams, CTA compliance requirements now mean operating two parallel obligations: maintaining your own internal beneficial ownership verification process at onboarding, and building the capacity to cross-reference FinCEN registry data when your legal entity clients are foreign reporting companies. The registry does not replace internal CDD. It supplements it.

This creates a clear operational gap for compliance teams managing large volumes of legal entity customers. Manually pulling registry data, matching names across jurisdictions, and managing update workflows across thousands of legal entity customers is not scalable without a structured screening infrastructure.

How Beneficial Ownership Data Reshapes Screening Operations

Foreign reporting companies often present the highest UBO complexity. Layered ownership structures, nominee arrangements, cross-border holding companies, and opaque equity stakes are precisely the mechanisms bad actors exploit, and precisely what the FinCEN BOI rule was designed to surface. This makes beneficial ownership screening a central component of modern AML risk assessment.

For AML teams, identifying the disclosed beneficial owner is only the first step. Screening that individual against sanctions lists, Politically Exposed Person (PEP) databases, adverse media sources, and global watchlists is where real risk exposure is determined. A disclosed owner with clean documentation who appears on OFAC’s Specially Designated Nationals (SDN) list, on a debarment register, or in the FinCEN Files dataset represents an entirely different risk profile than the paperwork alone would suggest.

The screening challenge compounds when foreign entities have multiple beneficial owners across multiple jurisdictions, with names requiring phonetic matching, transliteration, or script conversion. A name-matching system that has been tuned to English-language inputs will not detect any attempts at sanctions evasion performed using Arabic, Cyrillic, or Chinese name forms. Crimea, Abkhazia, Taiwan, and Northern Cyprus are jurisdictions with problematic sovereignty, which standard watchlist vendors often fail to cover.

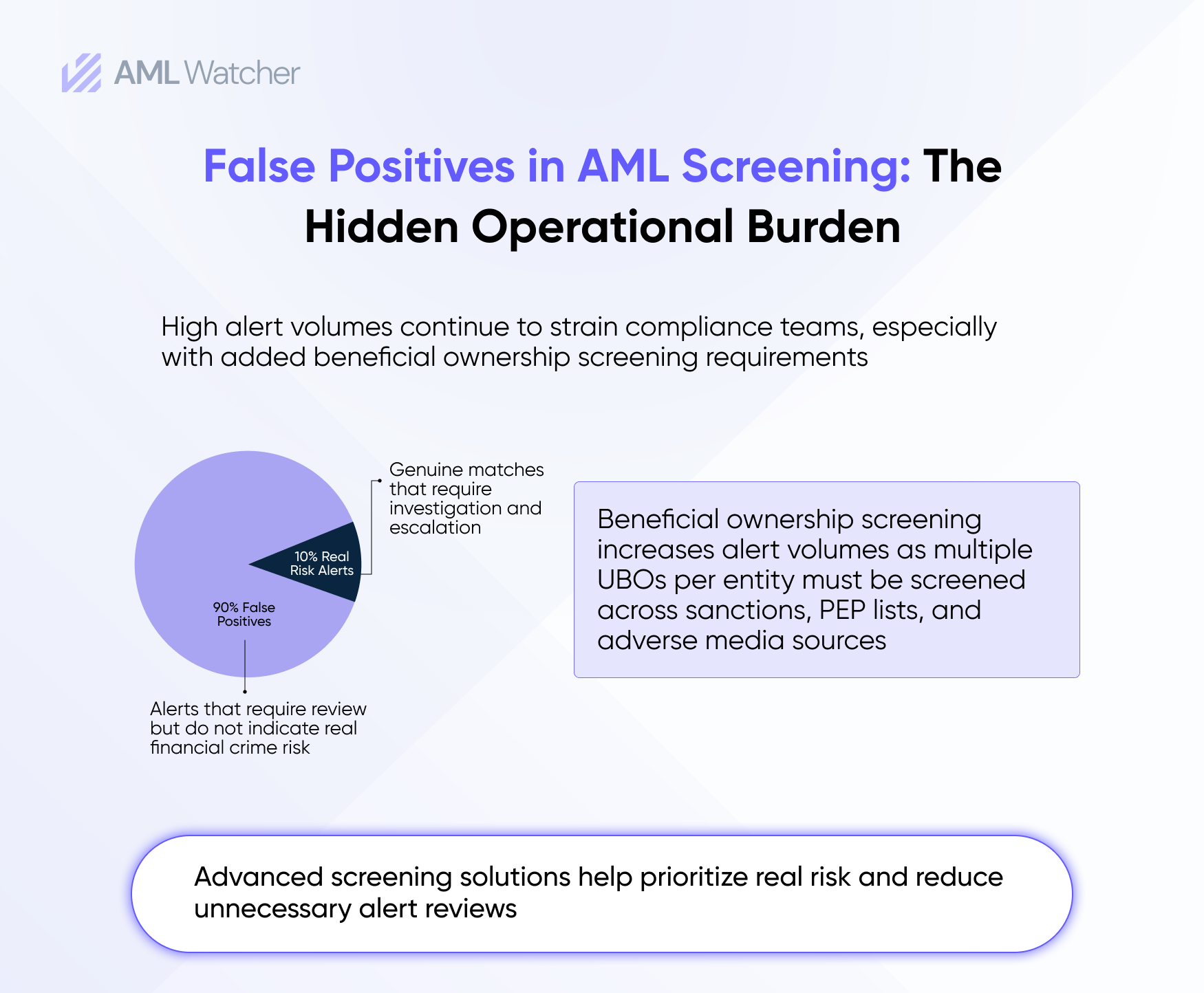

Industry statistics demonstrate the magnitude of the problem of false positives that lies behind all of this: approximately 90% of AML compliance notifications are false positives, i.e., noise, instead of actual risk that is occupying the capacity of analysts. When beneficial ownership screening adds another layer of entity and individual matches to the alert queue, teams without intelligent triage tooling will struggle to maintain both throughput and accuracy.

How AML Watcher Supports Beneficial Ownership Screening

Translating BOI data into actionable risk insights requires more than basic screening tools. BOI disclosures provide visibility into ownership, but compliance teams still face the challenge of validating risk across complex, cross-border UBO structures. Screening beneficial owners against fragmented global data while managing high false-positive volumes remains a persistent industry problem.

AML Watcher fills this gap by providing an extensive global watchlist and sanctions screening, assisted by sophisticated name-matching technology that identifies transliteration and jurisdictional differences. Its combined PEP and unfavorable media reporting enable a more comprehensive risk evaluation than superficial assessments, whereas AI-prioritized alerts reduce false threats and human workload. This enables compliance teams to focus on genuine UBO risk and ensure effectiveness as screening requirements increase.

- No commitment needed

- Complete AML Database at your service

- Access our all-in-one dashboard

Tier-2 PSPs in ... must demonstrate automated monitoring, layered CDD, &...

See the Full Regulatory Expectation70–80% less manual work, 95% less fatigue, TruRisk Agent makes compliance effortless.

Experience Agentic AMLMove Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries