How Fraud Detection Rules Keep Institutions Ahead of Evolving Financial Crime?

Fraud Prevention

October 24, 2025

Financial Institutions are facing a growing challenge as fraud schemes are developing at a faster rate than ever before. With new emerging technology, fraud attempts become increasingly innovative and dynamic. They exploit loopholes in systems and target human mistakes. Contemporary swindlers shift strategy on the fly, making them difficult to identify using conventional means.

Depending on traditional fraud prevention methods is no longer sufficient. Institutions must have systematic controls to detect suspicious activity before it results in significant loss. According to the Federal Trade Commission (FTC):

“Consumers reported losing over $12.5 billion to fraud, marking a 25% increase from the previous year. Additionally, 25% of financial organizations reported direct fraud losses exceeding $1 million.”

Banks and financial firms also need to keep updating their systems and train employees regularly to handle new fraud risks. Banks and financial institutions also have to continuously update their systems as well as train staff periodically to manage new fraud threats. By using technology along with skilled individuals, organizations can establish stronger defenses and stay ahead of fraudsters. This makes institutions one step ahead of fraudsters and guards both their customers and reputation.

What Are Fraud Detection Rules?

Fraud detection rules are predefined situations that help in identifying potential linkage to suspicious activity and flag such behaviors automatically. The rules serve as digital checkpoints, monitoring transactions, logins, and payments for unusual activity. The transfer of large amounts, quick payments, or logins from unknown places can all trigger alerts.

Unlike conventional manual checks, these rules are also integrated into Enterprise Risk Management (ERM) products, which are implemented by financial institutions. By incorporating fraud detection rules, institutions are able to minimize loss, improve compliance, and react to suspicious activity more efficiently.

Below are some of the most prevalent and efficient types of rules:

Transaction-Based Rule:

This is one of the most common rules for fraud detection. These types of rules identify transactions that are significantly different from a customer’s typical behavior.

For example, a $10,000 transfer if the customer usually spends $500 would be abnormal activity and trigger a review.

Geolocation and IP Monitoring:

These regulations screen the device or device behind a login attempt or a transaction. Their aim is to identify cross-border fraud attempts via stolen credentials.

If a user logs in from Italy and, 10 minutes after that, initiates another transaction from a German IP-address-based device. These geo-location or device changes typically signal malicious activity and trigger an investigation alert.

Device Fingerprinting:

Flagging suspicious behavior when the transaction is being received from an unknown or new device. Its function includes spot account takeovers, synthetic identity theft, or impersonation registrations.

For example, if the user normally transacts from one Android device but, for some unknown reason, logs in to the system from another version of the device, it can be flagged for investigation.

Velocity Rules:

The velocity rule of transaction monitoring assesses the speed and frequency of transactions to detect unusual bursts of activity.

If five rapid transactions are made in 10 minutes from the same account or card, the system can mark it as suspicious. These patterns are likely to indicate automated or manipulative activity and need to be investigated immediately.

Behavioral Pattern Rule:

This rule monitors how a customer usually behaves — such as how, when, and where they spend or transfer money — and then flags any unusual changes.

For instance, when a customer spends unexpectedly at 3 a.m. or purchases outside of their usual category, it shows anomalous behavior associated with potential fraud.

Blacklist and Watchlist Rules:

These rules automatically block or flag high-risk individuals, entities, or geographies based on internal or external lists (e.g., OFAC, FATF). It also ensures AML/CTF compliance and the prevention of regulatory breaches.

Duplicate or Mirroring Rules:

One of the fraud detection rules is the duplication rule. Its function is to catch potential system exploitation or mule network testing. This rule also includes identifying repeated transactions with the same values or beneficiaries within short timeframes.

Dormant Account Rules:

This rule triggers warnings when an inactive account suddenly initiates transactions. It identifies reactivation fraud or unauthorized behavior.

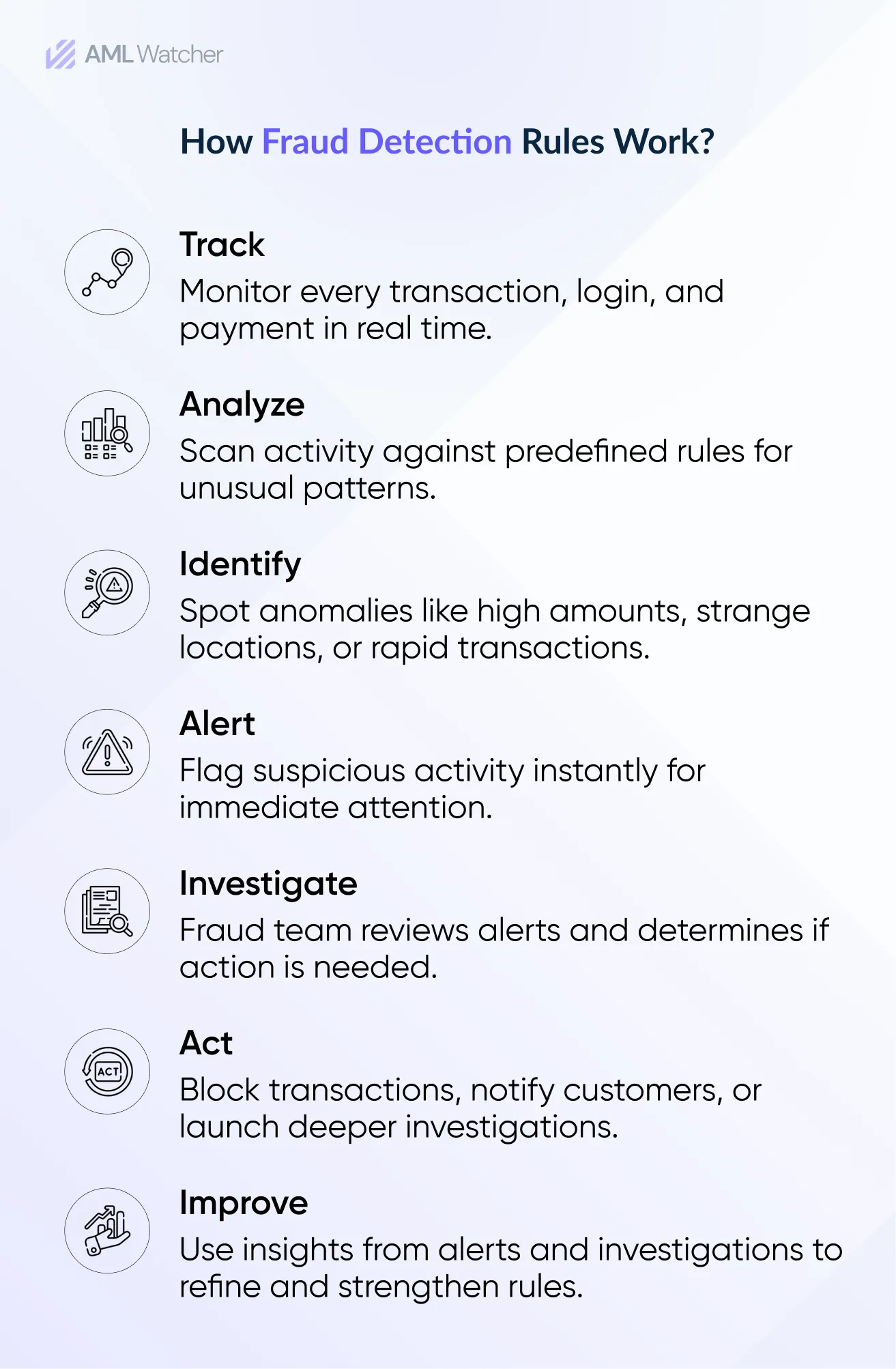

Once these fraud prevention rules are in place, they work together seamlessly to analyze every transaction. The following infographic explains how this process unfolds in practice.

Why Are Rules Central to Modern Fraud Detection Strategies?

After placing fraud detection rules and actively monitoring transactions, it’s important to understand why they’re so central to contemporary fraud prevention. Fraud prevention rules aren’t just used to identify anomalies—they are components of wider policies, procedures, and compliance frameworks that enable institutions to respond promptly, mitigate risk, and comply with regulation.

These days, in the high-speed financial world where SEPA Instant cross-border payments are settled in seconds, fraudsters leverage the same speed to steer funds past controls. Regulations permit institutions to react with the same precision and quickness.

As fraud typologies evolve, especially in the Gen AI era, through schemes like pig-butchering and APP fraud. Detection frameworks have to change with these emerging threats and include newer, quicker payment channels. Rules that are properly documented also assist with audit readiness, strengthening regulatory confidence, and strong internal controls.

How Are Institutions Evolving Their Approach to Fraud Detection Rules?

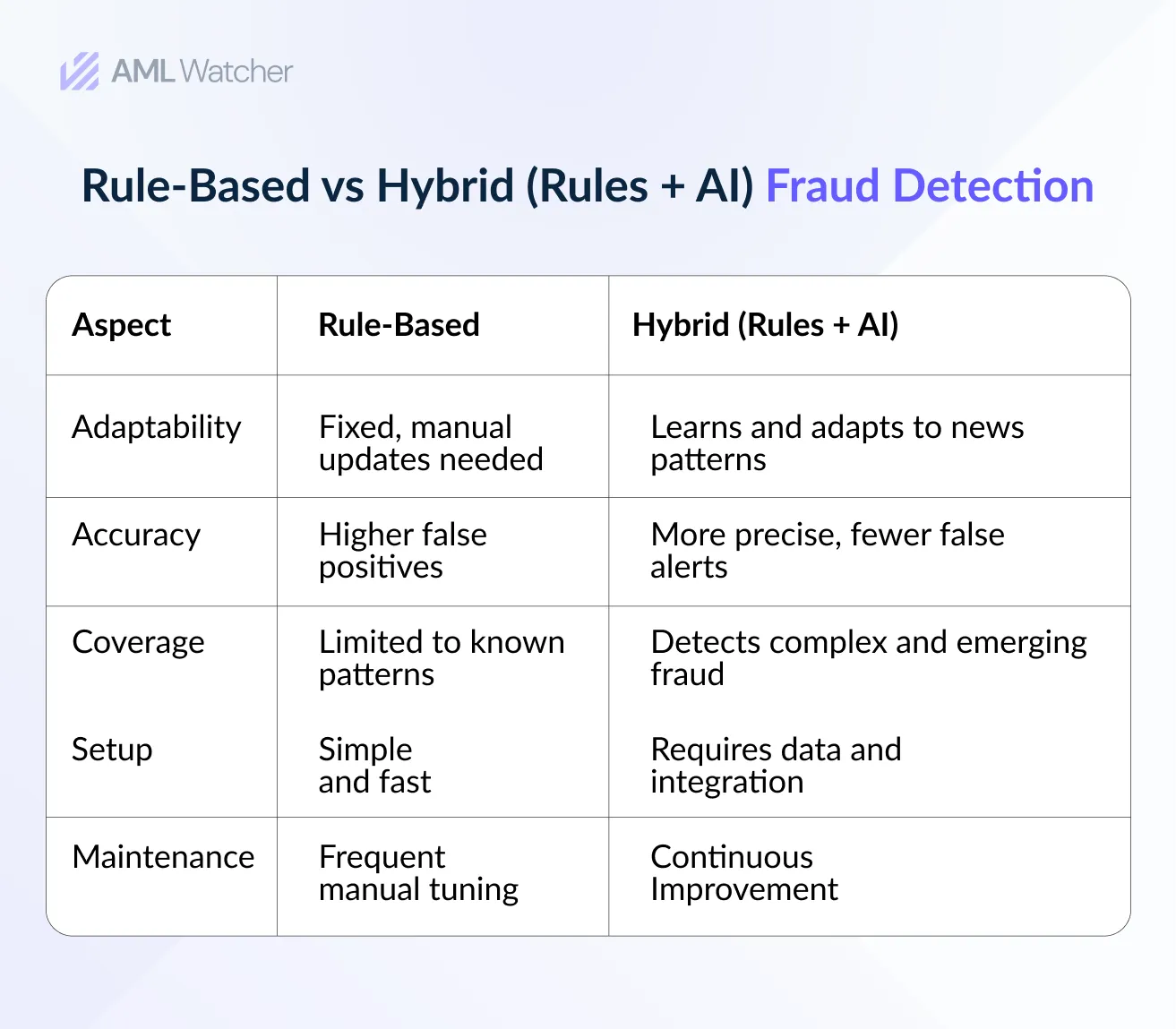

Rule-based anti-fraud has been the cornerstone of monitoring systems for a long time, but banks are now moving towards more intelligent and responsive approaches. With the integration of rule-based systems with artificial intelligence, machine learning, and behavioral analytics, anti-fraud are able to transcend fixed boundaries in order to detect complex and changing patterns of fraud.

AI-based fraud detection adds a predictive layer to such systems. Through past transactions and real-time activity, AI-driven algorithms are able to detect subtle anomalies that rule-based systems might miss. This improves accuracy, minimizes false positives, and enables institutions to respond more quickly to emerging fraud strategies.

To get a clearer picture of this change, here’s a brief comparison between rule-based and hybrid (rules + AI) fraud detection:

This shift isn’t a one-time change—it requires continuous tuning to keep pace with evolving fraud tactics.

Why Is Continuous Refinement of Fraud Prevention Rules So Important?

Fraud strategies are constantly being refined, and the current method may not be effective in the future. Fraud detection is never a set-and-forget process. Threats change, rules tighten, and customer behavior shifts. Those who fail to update their rules on a regular basis become reliant on out-of-date thresholds that no longer reflect true risk.

Continuous refinement is what keeps detection systems sharp. It involves sifting through alert information, researching false positives, examining new patterns of fraud, and refreshing rules to accommodate the threat environment of today. It’s also about tuning systems so that alerts are useful rather than overwhelming.

By keeping fraud detection rules as dynamic frameworks that change with every new threat, institutions have the ability to keep good defenses strong and ahead of the game. Those that do not adapt risk becoming easy targets for increasingly agile fraud networks.

This is where the latest technology comes into play, bridging the gap between dynamic threats and static systems.

How AML Watcher Strengthens Fraud Detection Strategies?

As financial crime becomes more sophisticated, institutions require solutions that shift from conventional monitoring to intelligent, responsive detection. AML Watcher delivers end-to-end fraud and AML compliance—merging precision, velocity, and intelligence into a single platform.

Reliable data is at the core. AML Watcher continuously updates data covering 215+ sanction regimes, 2.6M PEP profiles, and 415+ adverse media categories in 80+ languages. This identifies the connection between fraud networks, high-risk persons, and sanctioned parties.

With financial institutions struggling with the dual threat of AML regulation compliance and preventing expensive fraud, they require smarter, integrated solutions. Instead of managing these separately, institutions can implement an integrated FRAML (Fraud + AML) approach. AML Watcher enables this framework, where suspicious transactions can be cross-checked against sanctions or PEP data to assess whether they are one-offs or part of more significant laundering operations. This integration improves accuracy, reduces operational costs, and improves real-time risk awareness.

Its real-time monitoring and adverse media monitoring identify emerging threats and suspicious associations with cybercrime or embezzlement early. These insights help institutions strengthen their fraud score by detecting anomalies sooner. Fraud rules are jurisdiction- and industry-specific, supporting regulators such as FATF, OFAC, and EU payment authorities.

With integrated audit trails, monitoring logs, and compliance alignment, AML Watcher provides more timely alerts, fewer false positives, and consolidated oversight—keeping detection rules dynamic and regulators assured.

Move Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries