How Criminals Exploit Money Remittance: Understanding The Risks And AML Solutions

Anti Money Laundering

October 25, 2024

- Is Money Remittance and Cross-Border Payment a New Hawala?

- What Are The Money Laundering Risks In The Modern Remittance Industry?

- Global AML Remittance Regulations: Are They Enough to Curb Financial Crime?

- What Are The Red Flags To Watch Out For Remittance Fund Transfers?

- Solving AML Compliance Challenges In Cross-Border Transfers And Money Remittances

Behind every cross-border fund transfer, there’s more than just money—sometimes it’s hope, and sometimes it’s a crime.

For families around the world, money remittance is a vital resource, but for criminals, it’s an opportunity to exploit.

“We don’t ask questions; we just offer services,” says a Somalian hawaladar (broker), highlighting how easily money can flow without oversight in remittance networks.

Money remittance systems and foreign exchange platforms, integral components of the money services business (MSB), help traders, businesses, and diasporas send money across borders quickly and efficiently.

However, these same money transfer systems are exploited by criminals who set up fake companies and charities, bypassing weak Know Your Customer & Anti-Money Laundering protocols to move illicit funds through non-banking channels.

Despite various efforts to enforce Anti Money Laundering regulations and implement customer due diligence practices, these systems remain a preferred method for launderers to transfer funds quickly.

Although modern money remittance services and foreign exchange platforms have replaced informal systems like the hawala, the vulnerabilities remain there.

Illicit actors continue to take advantage of these channels, often hiding behind weak AML/CFT measures that promote anonymous fund exchanges.

Global remittance flows surged from $43.5 billion in 2008 to $689 billion in 2018 with 7.3% more growth in 2021, with expectations to reach a trillion dollars in the coming years.

-World Bank Group

With this growth in remittance flow comes an increased risk of money laundering and financial crime, making it critical for businesses to stay vigilant and avoid any illegal transfer.

To explore what are cross-border transactions, tactics criminals use to launder money under Money Remittance, global AML regulations, and advanced AML screening solutions to spot all high-risk individuals, continue reading this article.

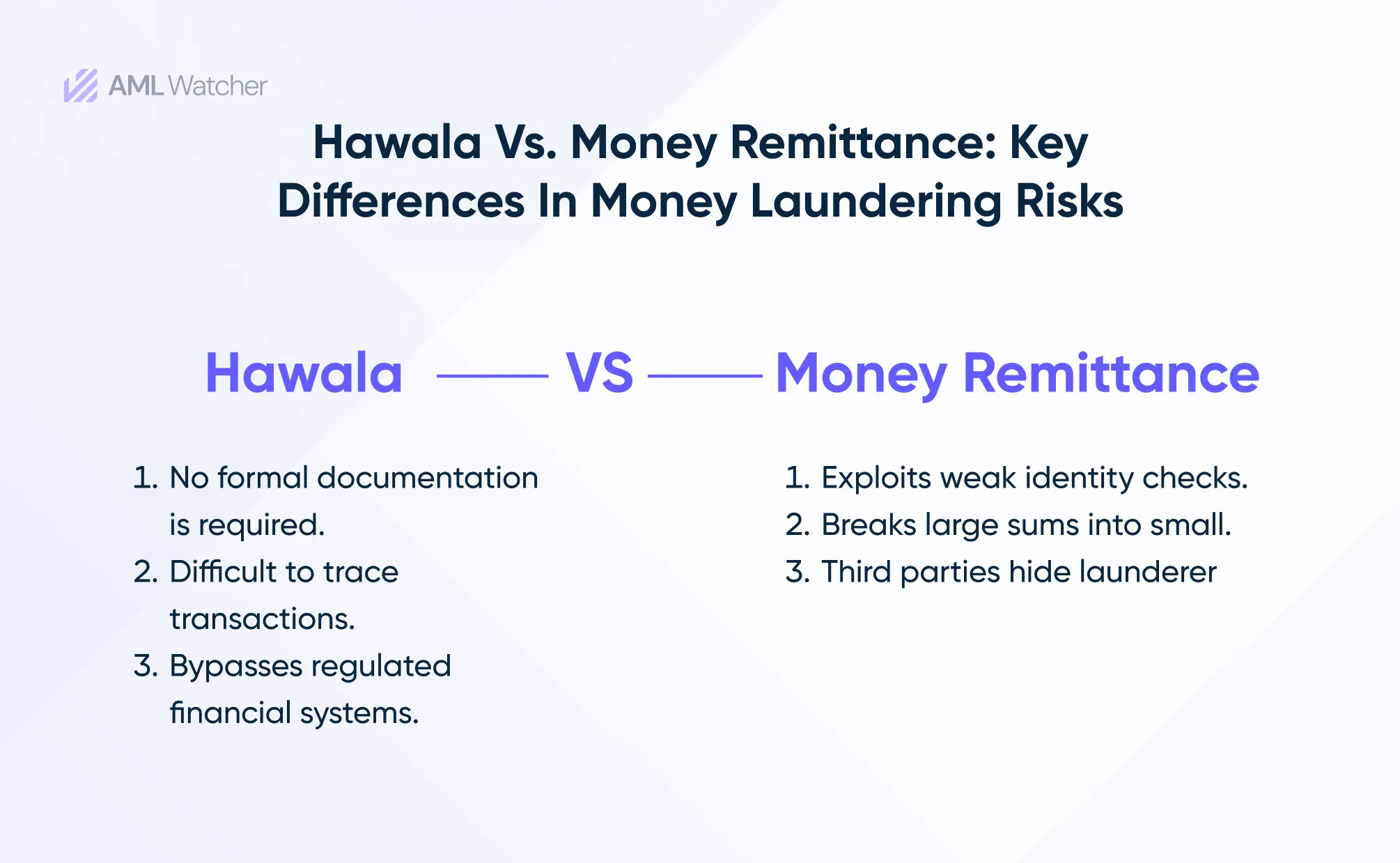

Is Money Remittance and Cross-Border Payment a New Hawala?

Modern remittance and foreign exchange channels have revolutionized how we send money from the local remittance shop to mobile money transfer services to sophisticated cross-border AML payment systems.

But behind this transformation lurks a dangerous parallel: Are these systems simply the new, upgraded version of hawala?

Criminals gravitate toward these channels for a simple reason: speed and anonymity.

In a world where money can move at lightning speed, the vulnerabilities in these systems are perfect opportunities for dirty cash to slip through undetected.

The Financial Action Task Force (FATF), the global authority on combating financial crime, has repeatedly warned that despite AML regulatory advancements, remittance systems remain vulnerable throughout the world.

Weak AML/CFT protocols and regulatory gaps between countries, make it as easy to launder money today as it was through traditional hawala channels.

This isn’t just a problem for developing countries. Even in the most advanced economies, criminals manipulate remittance services to swiftly move illicit funds, often faster than any law enforcement can react.

Now the real question isn’t limited to whether money remittance is the new hawala, it’s whether we’re doing enough to prevent history from repeating itself.

What Are The Money Laundering Risks In The Modern Remittance Industry?

Criminals see money remittance as a prime opportunity due to inconsistent global regulations and the ease of exploitation through digital platforms.

Regulatory differences between countries and cross-border compliance disparities lead to poor communication between authorities, enabling criminals to avoid thresholds and evade suspicious activity reporting.

To effectively combat money laundering, compliance teams need to grasp a clear understanding of the specific risks associated with this sector emerging from various channels; like,

Digital Platforms

The rise of digital remittance services has introduced new vulnerabilities. These online systems are more difficult for financial authorities to monitor which allows criminals to bypass customer due diligence protocols, particularly in non-banking remittance firms.

Prepaid Cards

Certain prepaid cards, which can be anonymously loaded and used to send money or withdraw cash from ATMs, pose another threat. Open-loop cards linked to global ATM networks enable illicit actors to move money around the world without direct contact or oversight.

Money Mules

The anonymous nature of remittance services allows criminals to enlist third parties, known as money mules, to transfer money on their behalf. These mules, whether coerced or paid, help conceal the launderer’s real information to transfer funds.

The ‘anonymity of the sender and recipient poses one of the main AML risks in money remittances.’

Ownership Manipulation

With the growing number of remittance services, illicit actors may aim to take control of a remittance company to sidestep AML regulations. They could either establish their firms or take advantage of existing owners to bypass AML compliance.

Structuring

To obscure the source of illegal money, criminals often break down large sums into smaller transactions across multiple remittance channels. This structuring tactic makes it more difficult for compliance teams and AML regulators to track the flow of illicit funds.

Global AML Remittance Regulations: Are They Enough to Curb Financial Crime?

Global AML remittance regulators are working effortlessly to reduce the misuse of money remittance systems & foreign exchange channels by enforcing strict laws, including;

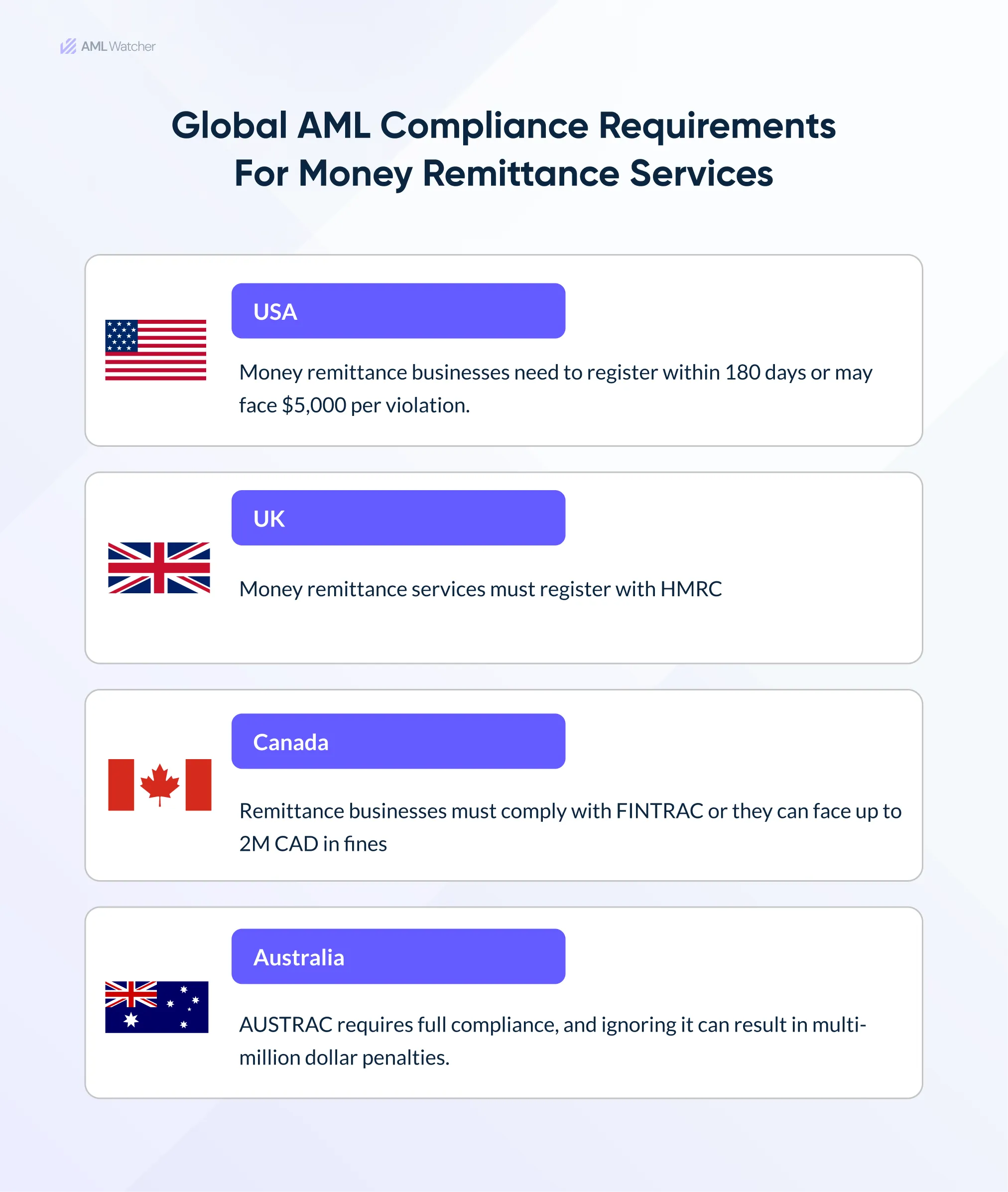

United States Of America

In the US, money transfer companies must comply with cross-border regulations enforced under the Bank Secrecy Act of FinCEN.

Foreign Exchange and money remittance businesses must register within 180 days of their establishment as per Form 107, “Registration of Money Services Businesses.”

Complying with the Bank Secrecy Act isn’t limited to this time affair, a single noncompliance can cause 5,000 dollars per violation, and renewing the registration every two years is essential to stay updated with the latest regulations and challenges.

Curious to know further details of AML regulations in the USA and what happens if you don’t comply. Read our AML compliance coverage in the USA for further clarity.

United Kingdom

In the United Kingdom, Money remittance and Foreign Exchange businesses are obliged to register with His Majesty’s Revenue and Customs (HMRC) under the UK’s money laundering regulations.

In 2021, the UK-based MSB; ‘MT Global was handed a jaw-dropping $32.4 million fine for AML regulation breaches.’ This highlights the reality that failing to adhere to money remittance compliance doesn’t just result in legal penalties, it leads to serious financial consequences.

Australia

In Australia, Remittance Service Providers (RSP) must register their businesses with AUSTRAC.

Non-compliance can lead to hefty multi-million dollar fines, so Remittance Service Providers (RSPs) must have a robust AML compliance program in place.

This goes beyond just basic CDD processes; it involves diligent transaction monitoring, continuous monitoring and a proactive, risk-based approach to spotting potential threats.

Canada

Canada takes a no-nonsense approach to AML Solutions that helps Money transfer businesses stay vigilant.

Registering a money remittance business (MSB) with FINTRAC regulations is essential in Canada where nearly 20 percent of the population consists of foreign-born residents.

The higher the number of foreigners the higher the risks. That’s why failure to register MSB in Canada can lead to penalties of up to 2 million CAD ($1.5 million) or, in some cases, up to five years imprisonment.

What Are The Red Flags To Watch Out For Remittance Fund Transfers?

Remittance service providers & foreign exchange dealers must remain vigilant when monitoring for suspicious behavior. Here are some common red flags that may indicate money laundering:

- Unusually frequent or high-value exchanges that don’t match a customer’s typical behavior.

- Fund transfers that exceed reporting thresholds or involve PEPs or sanctions-listed individuals.

- Customers who try to conceal their personal details or provide incomplete information.

- Multiple dealings are connected in a way that suggests structuring to avoid detection.

Solving AML Compliance Challenges In Cross-Border Transfers And Money Remittances

AML Watcher with its unique features can help money remittance service providers or foreign exchange dealers ensure AML compliance and reduce risk.

How?

Through Global Database Coverage

AML Watcher ensures thorough coverage even in smaller or high-risk jurisdictions frequently involved in money remittance activities by screening clients across 235 countries with over 100,000 data sources.

This lowers the risks of dealing with individuals placed on sanctions lists or who have committed financial crimes.

With PEP Screening across risk levels 1-4

AML Watcher helps remittance service providers avoid high-risk individuals involved in money laundering or corruption with its wide access to global PEP databases covering PEP risk levels 1-4, thereby preventing AML regulatory violations in cross-border transfers.

Providing Conflicted Zone Coverage

It offers comprehensive client screening coverage in disputed and high-conflict regions, enabling remittance service providers to function safely in these difficult settings without being exposed to financial crime risks.

Through Updated Sanction Screening

Remittance service providers can maintain AML compliance by screening clients against 200+ global sanction regimes, and by its real-time update ensure that funds aren’t transferred to or from entities or individuals on international watchlists.

Via Adverse Media Screening

AML Watcher flags individuals and entities based on negative media reports from international and local sources, helping remittance service providers spot individuals involved in illicit activities on time.

With Custom Risk Scoring

Adjust risk levels based on the unique nature of the service providers, ensuring that even lower-risk profiles are appropriately flagged for further due diligence. Institutions can even select customized databases to get custom search results with near-to-zero false positives.

Sharing Localized Data Integration

AML Watcher’s ability to tap into local databases, including smaller or less-regulated regions, offers remittance businesses a thorough client screening with lower false positives and false negatives that ensures even individuals in less monitored areas are screened against relevant watchlists and PEP databases.

Move Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries