How CTR in Banking Stimulates the Financial Operations?

Others

March 14, 2025

- What is a Currency Transaction Report and Its Affiliation in Banking?

- CTR Filing Requirements Every AML-Compliant Financial Institution Must Follow

- Prominent AML Regulations Stressing CTR Monitoring

- Recent CTR Compliance Failures and Lessons Learned

- Implications of CTR Anti-Money Laundering Compliance

- Key Strategies to Ensure Credible Cash Transaction Report Filing

- How are SARs and CTRs Different?

Did you know that one of the key red flags for money laundering is unusually high-value transactions?

Such transactional practices often raise financial concerns for the institutions. So, how can US-based financial institutions protect themselves from such risky transactional activities? The Currency Transaction Report (CTR) is the answer to this question, as it protects banks from these risks.

The Bank Secrecy Act (BSA) released the CTR requirements in 1970, and after 50 years of being in effect, these reporting requirements remain a central constituent of AML compliance in fighting against money laundering risks. But what is a CTR, and are these measures still as effective as they were decades ago in the US?

In the United States, the Currency Transaction Report (CTR) is filed for any currency transaction exceeding $10,000. It involves the documentation of every currency transfer from one person to another, whether in the form of cash withdrawals or direct currency exchanges.

Interested in examining the significance of CTR in Banking? The next section expands on what is CTR in Banking and its role in eliminating money laundering risks.

What is a Currency Transaction Report and Its Affiliation in Banking?

According to FinCEN’s Year-In-Review report of 2023, approximately 20.8 million CTRs were filed by the banking institutions. A CTR is a regulatory requirement that mandates banking institutions to file a transaction exceeding the threshold limits.

The reporting of currency transactions enables banks and other institutions to seamlessly comply with the AML regulations. The filing of CTR is crucial for regulating virtual currency exchanges and peer-to-peer payments.

US-based financial institutions are required to file a currency transaction report in case of the following supposedly suspicious activities:

- Any regular, fintech, or neobank transaction exceeding $10,000 must be reported to the Internal Revenue Service (IRS) to ensure compliance with the country’s tax regulations.

- If a financial institution suspects a customer to be involved in multiple transactions exceeding $10,000 within 24 hours, the respective bank is mandated to file a CTR to identify the illicit transactional pattern.

Let’s now evaluate how a currency transaction report is filed within a bank and what its prerequisites are:

- US-based banking institutions are required to file a CTR through FinCEN form 112. Effective in 2020, this form captures the customer’s transactional information to understand whether their financial patterns align with the AML regulations.

- Many financial intermediaries initiate currency transaction reports through the BSA’s e-filing system. The electronic filing automates the submission of credible customer information to prevent the facilitation of money laundering activities.

- FinCEN requires banking institutions to keep records of the reported transactions to ensure compliance with the AML guidelines.

CTR Filing Requirements Every AML-Compliant Financial Institution Must Follow

What do the drug cartels and terrorist organizations have in common?

They all heavily rely on the flow of currency across the globe. This calls for strict CTR measures to minimize the flow of unauthorized activities and abide by the AML/CFT guidelines. Thereby, some of the critical CTR filing requirements that every financial institution must follow are:

- According to section 8.1 of the Bank Secrecy Act, financial institutions are mandated to provide credible customer information on the CTR, including the name, social security number, taxpayer identification number, and street address.

- All the cash transaction reports filed with the IRS are to be stored in the FinCEN database to keep track of the customer’s transactional patterns. According to the FinCEN guidelines, the FIs must file the reports within 15 days to avoid future financial repercussions.

- To ensure efficient AML measures and reduce the CTR burden, certain entities are exempted due to their routine currency operations. Interbank transactions don’t necessarily require CTR filings due to their internal regulatory operations.

- However, these exemptions are thoroughly examined to ensure no illegal activity emerges. Furthermore, publicly traded companies and transactions carried out by government organizations are also exempted from the CTR filing.

Prominent AML Regulations Stressing CTR Monitoring

In light of the FATF suspicious transaction reporting recommendations, countries have adopted effective CTR requirements to identify and exempt unauthorized activities.

The FIUs (Financial Intelligence Units) are required to evaluate the feasibility of DNFBP’s (Designated Non-Financial Business and Professions) and FI’s reporting systems, where all the domestic and international currency transactions are conducted.

It is done to ensure that no suspicious currency transaction goes unreported, leading to money laundering concerns.

Currency transaction reporting (CTR) is a regulatory measure formulated by FinCEN under the Bank Secrecy Act. BSA’s CTR requirements optimize the financial institution’s ability to seamlessly identify suspicious transactions in order to alleviate the financing of money laundering activities.

Section 7(3) of AMLA specifies that all currency transaction reports are to be filed with the regulatory bodies within 7 working days as soon as the respective currency transaction takes place.

Under the AML guidelines of BSA, examiners are mandated to assess the adequacy of the bank’s internal CTR policies and processes. The examiners must determine whether their applied reporting policies are effective enough to tackle and mitigate ML/TF activities.

Recent CTR Compliance Failures and Lessons Learned

The filing of CTRs is of critical significance when it comes to ensuring the bank’s compliance with the AML efforts in reporting malicious financial activities.

However, several cases have emerged over the recent few years, representing banks’ failures to comply with the CTR regulations. Here’s a quick overview:

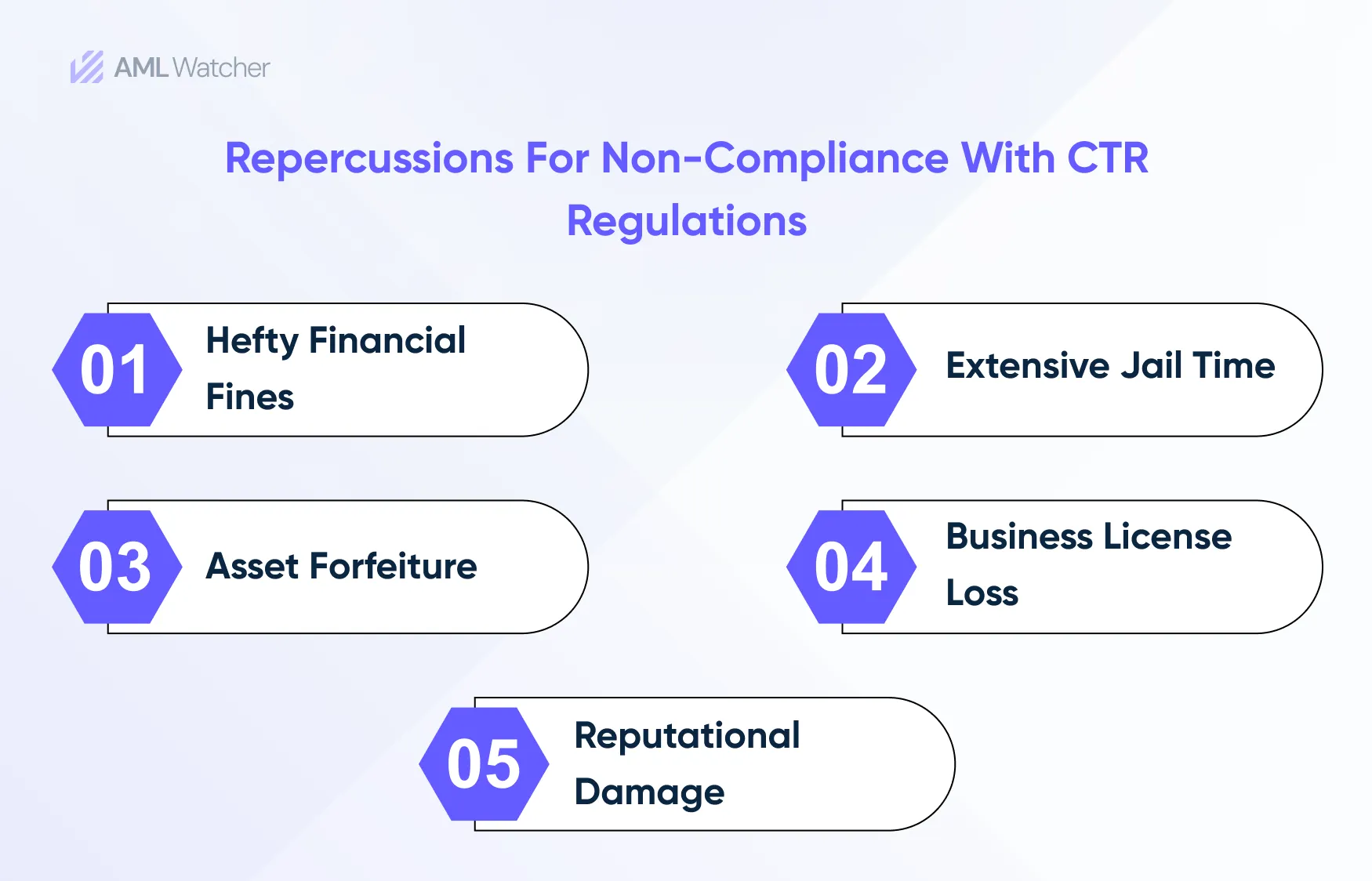

Wells Fargo’s Transaction Reporting Deficiencies

In 2024, the Office of the Comptroller of the Currency (OCC) signed an agreement with Wells Fargo, a multinational American Financial company.

This agreement was formulated to identify the deficiencies in the bank’s financial crime risk management practices and AML internal controls, resulting in violations of various laws and regulations.

Due to the non-regulated currency transaction reporting, the bank failed to identify the malicious transactions that were conducted through its network.

Therefore, the agreement mandated the establishment of a compliance committee to optimize the reporting of currency transactions and enhance the overall AML risk management of the company.

Michael J. Miske Jr. CTR Failure

A former Honolulu-based business owner, Michael J. Miske Jr., was found to be involved in criminal activities during the trial in May 2024.

To avoid the bank’s reporting of transactions that exceeded $10,000, Miske facilitated structured transactional activities through its server.

During the trial, it was revealed that funds were moved through multiple accounts to evade reporting requirements so that funds could be laundered for illicit operations.

This case emphasizes the importance of effective and AML-compliant transaction reporting measures to overcome the challenges associated with structured money laundering practices.

Implications of CTR Anti-Money Laundering Compliance

Strengthening the company’s anti-money laundering measures is crucial in integrating effective currency transaction reporting measures.

Banks can stay a step ahead of their competitors for reliable and secure transactional flow, by demonstrating transparent financial reporting.

Here’s how credible CTR filings promote streamlined AML-compliant measures:

- BSA’s primary goal of stressing the filing of currency transaction reports is to prevent money laundering. CTRs help banking institutions restrict the flow of large monetary sums across borders to prevent tax evasion, terrorist financing, corruption, and money laundering offenses.

- The documentation of all sorts of transactions, including loan repayments, treasury bills, ATM transactions, and currency exchanges, allows FinCEN to track the customer’s previous financial patterns in real time. This ensures protection from unforeseen money laundering attempts, which is crucial for complying with the AML regulations.

- Through impeccable CTR documentation, compliance officers keenly pinpoint the customers that trigger frequent high-risk transactions across the globe. These transactional reports enable examiners to conduct further AML screening of risky customers against sanction lists and adverse media channels to analyze their financial histories and risk profiles.

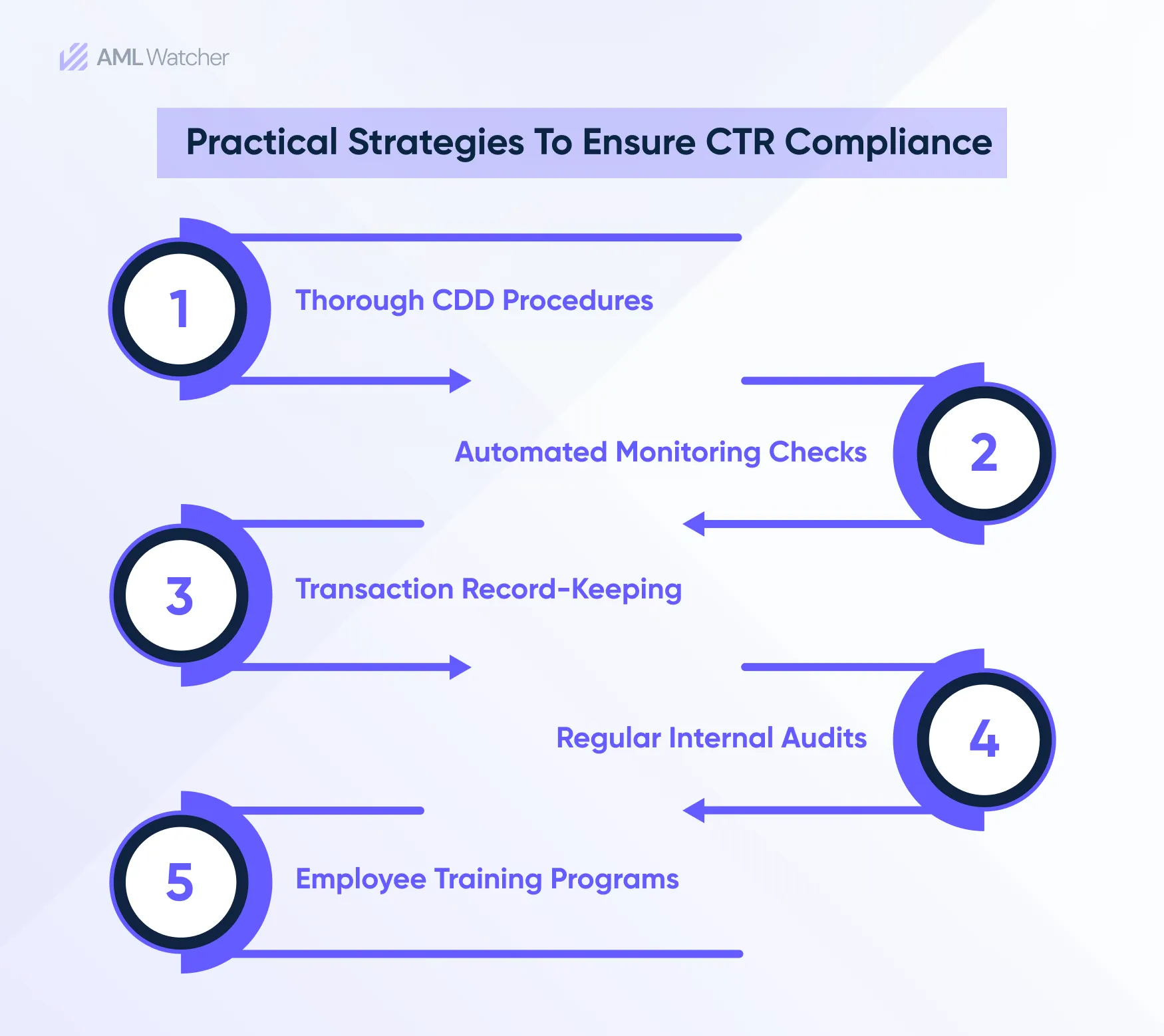

Key Strategies to Ensure Credible Cash Transaction Report Filing

Accurate and timely reporting of suspicious cash transactions is crucial for fulfilling compliance with AML/CFT regulatory measures. Some of the effective strategies for stimulating the effectiveness of CTR measures across banking institutions include:

- CTR measures can accommodate AML-compliant measures in financial institutions through data-driven and advanced transaction monitoring modules. BSA’s e-filing CTR forms automate the collection of customer’s financial information. Additionally, enhanced transaction monitoring checks help with the flagging of transactions that exceed the threshold amount in real time.

- Banks must optimize their internal control and risk management mechanism by segregating the transaction review procedures to ensure that all suspicious financial activities are reported in a timely manner.

- Banks are required to educate employees regarding the CTR requirements to ensure accurate filings and reporting of malicious financial transactions. Additionally, the bank’s compliance departments must stay informed about the changing currency transaction reporting guidelines for smoother AML-compliant financial operations.

How are SARs and CTRs Different?

While both the Suspicious Activity Reports (SARs) and Currency Transaction Reports (CTRs) are significant for identifying financial crimes, they both serve different purposes.

A CTR is filed when transactions exceed $10,000, regardless of money laundering suspicions. Whereas, a SAR is filed whenever a malicious activity is recognized, irrespective of the size of the transaction.

The compliance officers ensure that proper CTR documentation is initiated to help institutions avoid fines and illicit activities by flagging higher currency transactions.

Therefore, financial institutions should invest in credible reporting and customer risk monitoring policies that comply with the country’s regulatory requirements.

For businesses aiming to optimize their compliance efforts, solutions like AML Watcher can provide enhanced reporting and customer due diligence monitoring checks. This ensures that CTRs can be monitored for actual links to suspicious activities.

Our customizable risk engines, sanctions screening, and adverse media monitoring services help assess high-risk individuals and then make an informed decision on whether a currency transaction report (CTR) could also be associated with suspicious activity. With this, the authenticity of millions of transactions is regularly examined that cater to businesses of diverse niches to prevent financial crimes and monetary losses.

- No commitment needed

- Complete AML Database at your service

- Access our all-in-one dashboard

Tier-2 PSPs in ... must demonstrate automated monitoring, layered CDD, &...

See the Full Regulatory Expectation70–80% less manual work, 95% less fatigue, TruRisk Agent makes compliance effortless.

Experience Agentic AMLMove Beyond Articles. Activate AML Intelligence.

Switch to AML Watcher today and reduce your current AML cost by 50% - no questions asked.

- Find right product and pricing for your business

- Get your current solution provider audit & minimise your changeover risk

- Gain expert insights with quick response time to your queries